Author: Jademont, Evan Lu, Waterdrip Capital

Reviewing the Volatile 2025, Looking Ahead to the Long AI Cycle

The New Industrial Revolution: Computing Power Becomes the Engine of Economic Operation

"In this world, very few people can be like Edwin Drake, inadvertently opening an era that changes human history... His drill bit, penetrating deep into the ground, touched not only black liquid but also the artery of modern industrial civilization."

In 1859, in the mud of Pennsylvania, people gathered around Colonel Edwin Drake, laughing mockingly. At that time, the world's lighting still relied on increasingly scarce whale oil, but Drake firmly believed that the underground "rock oil" could be extracted on a large scale. This was widely considered a madman's delusion. Until the first gush of black liquid erupted, no one could have imagined that the emergence of oil would not only replace whale oil as a lighting energy source but would even become the cornerstone of the next two hundred years of human society's struggle for discourse power, further restructuring global power and geopolitics for the next century. Human history also reached a turning point: old wealth relied on trade and shipping, while new wealth was rising with the emergence of railroads and energy (oil).

In 2025, we are in the midst of an extremely similar game. Only this time, what's gushing out wildly is the computing power flowing in silicon chips, and this era's "gold" is code engraved on the chain; the new era's "gold" and "oil" are reshaping all our consensus on productivity and store-of-value assets. Looking back at 2025, the market experienced unexpectedly severe volatility. Trump's aggressive tariff policies forced global supply chains to relocate, triggering a significant rebound in inflation; gold historically broke through $4,500 amid geopolitical uncertainties; the crypto market welcomed the epic positive news of the GENIUS Act at the beginning of the year but experienced the painful burst of deleveraging in early October.

Amid the noise of macro fluctuations, industry consensus in the field of AI computing power is rapidly fermenting: Nvidia, the "AI water seller," reached a milestone market capitalization of $5 trillion in October. Additionally, the three giants—Google, Microsoft, and Amazon—have invested nearly $300 billion in AI infrastructure within the year. For example, the completion of xAI's million-GPU cluster by the end of the year预示着 (signifies) computing power. Musk's xAI built the world's largest AI data center in Memphis in less than half a year and plans to expand to an astonishing scale of 1 million GPUs by the end of the year.

The Digital Intelligence Era: The Main Theme of the Next Industrial Revolution

Ray Dalio, founder of Bridgewater Associates, once said: "The market is like a machine, you can understand how it operates, but you can never precisely predict its behavior." Even though the macro environment is random and unpredictable, it is undeniable that AI remains the main long-term growth channel in the U.S. stock market. AI technology, in the next decade, has become the most critical core gear in the market machine; and it continues to affect governments, enterprises, and individuals in every aspect.

Although debates about an "AI bubble" have never ceased, with many institutions warning that the AI investment boom already shows signs of froth: Morgan Stanley research pointed out that in 2025, investment growth in the AI field led to soaring tech stock valuations while productivity improvements were not yet obvious, and this divergence was compared to the bubble signs during the Internet boom of the 1990s.

But an unavoidable fact is: the productivity revolution driven by AI has gradually entered a substantial monetization phase. From an investment logic perspective, AI is no longer just a narrative for tech giants; the efficiency dividends and extreme cost optimization it brings are the main drivers for boosting profits and productivity in non-tech companies. But the cost behind it also corresponds to extremely残酷 (cruel) employment replacement. AI's replacement of labor, especially the white-collar class, is unquestionable. The most direct manifestation is the multiple reductions in entry-level positions; basic code writing, accounting and auditing, or初级 (junior) management consulting and legal practice positions may all become the first targets of AI replacement.

As AI applications deepen, unemployment risks are accumulating in industries like healthcare, education, and even retail. Recently, a残酷调侃 (cruel joke)流行 (became popular) in the U.S. investment circle: software engineers in the future will be like "civil engineers" today; the future might be as Elon Musk emphasized in an interview, AI will replace everyone's jobs. But it also预示着 (signals) the arrival of a new industrial era belonging to AI, an era called the "Digital Intelligence Era."

Looking Ahead to 2026, Demand for AI Will Continue to Expand

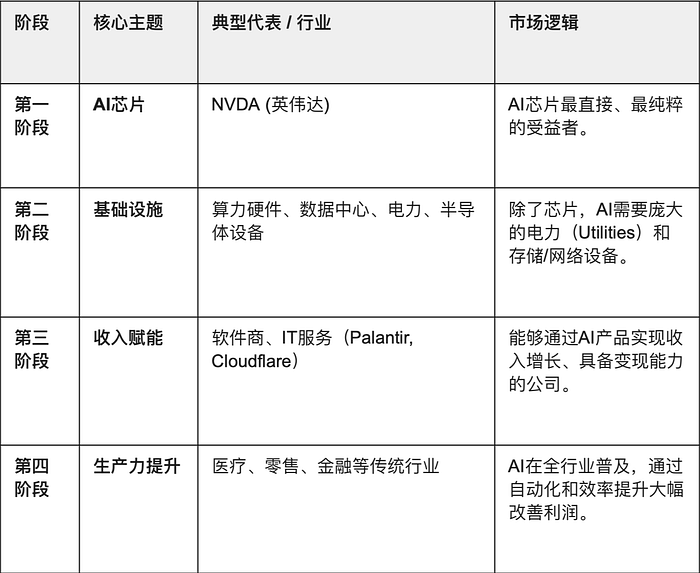

4 Stages of AI Industry Investment

As the AI boom moves from concept to full industry diffusion, and with the market having fully priced in the MAG7 (Magnificent 7 U.S. stocks), where is the next wave of growth for the AI theme? The "AI Investment Four-Stage Model" proposed by Goldman Sachs equity strategist Ryan Hammond points the way forward: AI investment will sequentially go through the chip, infrastructure, revenue enablement, and productivity improvement stages.

AI Investment Four-Stage Model, Reference Source:https://www.goldmansachs.com/insights/articles/ai-infrastructure-stocks-poised-to-be-next-phase

Currently, the AI industry is just at the intersection transitioning from "infrastructure expansion" to "application landing," i.e., the period transitioning from Stage 2 to Stage 3. AI infrastructure demand is in an explosive stage:

-

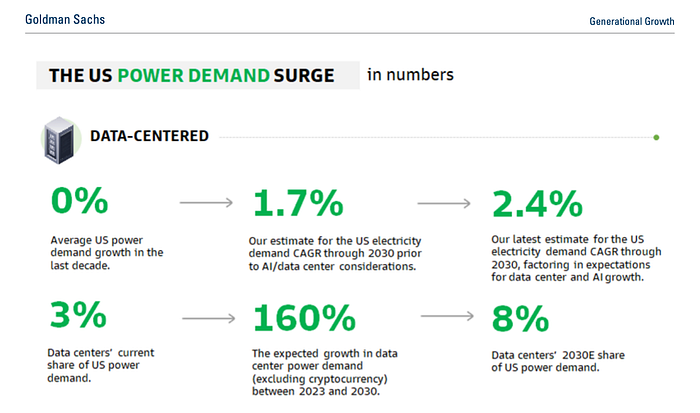

It is predicted that by 2030, global data center power demand will increase by 165%

-

From 2023 to 2030, the compound annual growth rate (CAGR) of U.S. data center power demand will be 15%, which will increase the proportion of data centers in total U.S. power demand from the current 3% to 8% by 2030."

-

It is estimated that by 2028, global cumulative spending on data centers and hardware will reach $3 trillion.

Goldman Sachs Forecast for U.S. Data Center Power Demand, Image Source:https://www.goldmansachs.com/pdfs/insights/pages/generational-growth-ai-data-centers-and-the-coming-us-power-surge/report.pdf

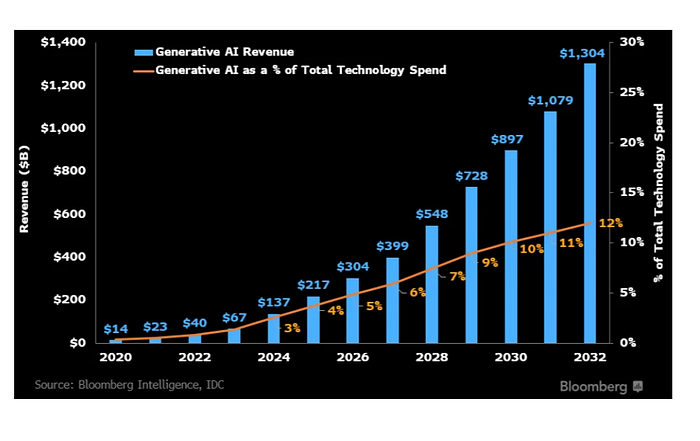

At the same time, the generative AI application market is also experiencing explosive growth, projected to grow to $1.3 trillion by 2032. In the short term, the construction of training infrastructure will drive the market to grow at a compound annual growth rate of 42%; in the medium to long term, the growth momentum will gradually shift to inference equipment for large language models (LLMs), digital advertising, professional software, and services.

Bloomberg: Generative AI Growth Forecast for the Next 10 Years, Data Source:https://www.bloomberg.com/company/press/generative-ai-to-become-a-1-3-trillion-market-by-2032-research-finds

This judgment will be verified in 2026. Goldman Sachs pointed out in its latest 2026 macro outlook: 2026 will be the "year of realization" for AI return on investment (ROI). AI will have a substantial cost-reduction effect on 80% of non-technology companies in the S&P 500 index. That is, it will verify whether AI can truly transition from "potential" to "performance" on corporate balance sheets.

Therefore, the market's focus in the next 2-3 years will no longer be limited to单一的 (single) tech giants but will further扩散 (diffuse): digging deeper into AI infrastructure (such as power, computing hardware, data centers), and寻找 (searching for) those泛化行业 (generalized industry) companies that successfully transform AI into profit growth.

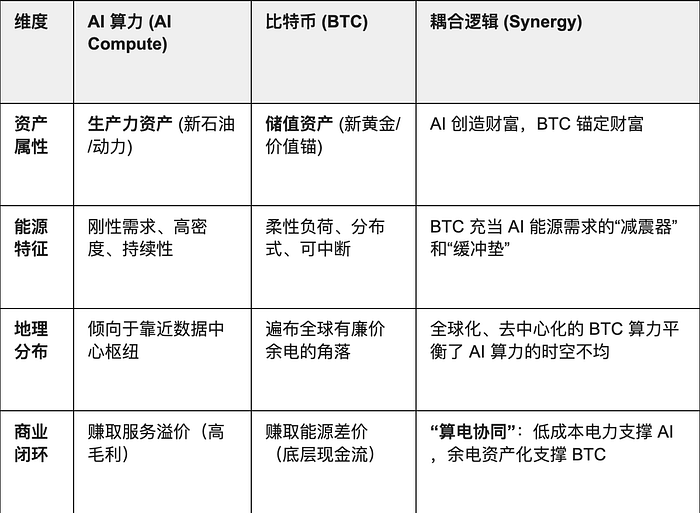

AI Computing Power is the "New Oil," BTC is the "New Gold"

If AI computing power is the "new oil" of the digital intelligence era, driving the exponential leap in productivity, then BTC (Bitcoin) will be the "new gold" of this era, acting as the ultimate underlying layer for value anchoring and credit settlement.

AI, as an independent economic entity, does not need the human banking system; the only thing it needs is energy. And BTC is a pure "digital energy storage device." In the future, AI will be the "fuel" of the economy, while BTC will be the "anchor" behind economic value. The issuance of BTC is entirely determined by the Proof-of-Work (PoW) based on electricity consumption, which完全契合 (perfectly aligns) with the essence of AI (converting electricity into intelligence).

Secondly, AI computing power, as a consumable productive asset, has its core cost源于 (originating from) electricity, and its value output depends on algorithm efficiency; while BTC, as a decentralized store-of-value asset, is essentially the monetization of energy, naturally possessing the function of a "reservoir" to balance the uneven global distribution of computing power across time and space. AI requires持续稳定的 (continuous and stable) electricity, while BTC mining can consume waste electricity generated by grid imbalances. That is, BTC mining stabilizes the grid through "Demand Response": when there is excess electricity (e.g., peak wind or solar power), computing power can act as a load to absorb the surplus; when electricity is scarce (AI computing peak), mining computing power can shut down instantly, releasing electricity to higher-value AI clusters.

GENIUS Act: The Starting Point for the Convergence of Stablecoins + RWA + On-Chain Computing Power

With the passage of the GENIUS Act in the U.S. in 2025, the U.S. dollar is also preparing to complete its digital transformation gradually. Stablecoins are纳入 (incorporated into) the federal regulatory framework and become the "on-chain extension" of the dollar system. This act not only injects a trillion-dollar new on-chain liquidity pool into U.S. Treasury bonds but also provides a referable paradigm for designing stablecoin regulatory systems in important jurisdictions worldwide (such as the EU, UK, Singapore, and Hong Kong).

The establishment of this compliance framework first injects strong institutional momentum into the RWA (Real World Assets) market: with regulated stablecoins enhancing global liquidity and supporting efficient cross-border settlement and transactions, the issuance and circulation of RWA will become more convenient. Stablecoins have become the primary payment method for on-chain investments in real estate, bonds, artwork, and other RWAs, supporting fast global cross-border clearing.

Among them, AI computing power assets, due to their high investment cost, stable收益 (returns), and heavy asset attributes, and naturally meeting the requirements for on-chain digital management, are gradually being regarded as a standardized RWA: whether it's GPU cloud computing, AI inference resources, or the operational capacity of edge computing nodes, parameters such as pricing methods, lease cycles, load rates, and energy efficiency ratios can all be quantitatively mapped through on-chain smart contracts. This means that future businesses like computing power leasing,收益拆分 (profit sharing), transfer, and抵押 (collateralization) will fully migrate to on-chain financial infrastructure for trading, settlement, and refinancing; additionally, computing power can provide real-time insights into equipment operation and收益 (returns) through on-chain data, ensuring transparent and verifiable回报 (returns); meanwhile, computing power supply can be flexibly scheduled on demand, reducing the risks of capital occupation and resource idle (idleness) in traditional heavy-asset models, guaranteeing the stability and transparency of收益 (returns).

Even more值得畅想 (worth imagining) is that, much like the oil exchanges that emerged on Wall Street after the discovery of oil two hundred years ago, once AI computing power借助 (with the help of) RWA becomes a financial asset that can be standardized, traded,抵押 (collateralized), and leveraged, it is expected to achieve innovative financial operations such as on-chain financing, trading, leasing, and dynamic pricing; a new generation of "computing power capital markets" based on RWA will have more efficient value circulation channels and potential application spaces with unlimited potential.

New Opportunities Under the "Dual Consensus"

In the new era where AI is fully integrated into our lives, computing power will serve as the consensus for efficient productivity, and accompanying the extreme liquidity of efficient productivity — BTC will become the new definition of the store-of-value consensus.

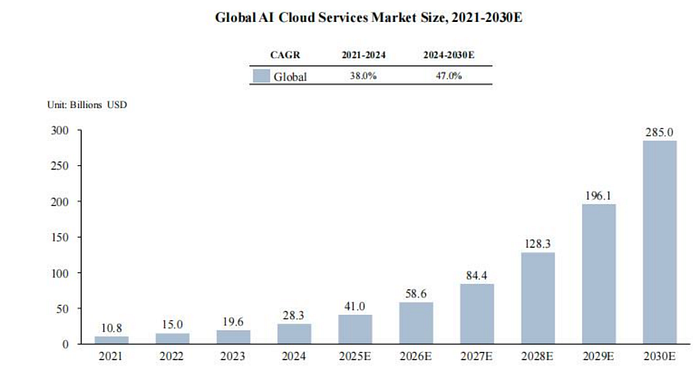

Then, companies that can master either the "productivity" or "asset" end in the future will become the most valuable entities in the future cycle, and cloud service providers are precisely at the intersection of the "BTC Store-of-Value Consensus" and the "AI Productivity Consensus." If computing power is the high-energy fuel driving the high-speed operation of the digital economy, then cloud services are the intelligent pipelines that carry and distribute this power.

Global AI Cloud Service Market Size Forecast, Data Source: Frost & Sullivan

This includes several giants: Microsoft, Amazon, Google, xAI, Meta. They are also known as "Hyperscalers" (超大规模云服务商). Their main business is primarily IaaS (Infrastructure as a Service)面向通用需求 (catering to general needs). Although they have large computing power resource pools, they may be inefficient when encountering scenarios requiring computing resource scheduling. Hyperscalers are also the most upstream in AI computing power services, controlling the vast majority of computing power resources in the market, and are still continuously布局 (laying out) computing power infrastructure:

-

Microsoft: Launched the $100 billion "Stargate" project aimed at building a million-GPU cluster to provide极限算力支持 (ultimate computing power support) for the evolution of OpenAI's models.

-

Amazon (AWS): Committed to investing $150 billion over the next 15 years to accelerate the deployment of its self-developed chip Trainium 3, achieving decoupling from external supply and computing power costs through hardware autonomy.

-

Google: Maintains annual capital expenditure at a high level of $80-90 billion, relying on the high energy efficiency of its self-developed TPU v6 to rapidly expand AI-specific clouds (AI Regions) globally.

-

Meta: Zuckerberg clearly stated in the earnings call that Meta's capital expenditure (Capex) will continue to grow, with the 2025 guidance already raised to $37-40 billion. Through liquid cooling technology upgrades and a reserve of 600,000 H100 equivalent computing power, it is building the world's largest open-source AI computing power pool.

-

xAI: With the "Memphis speed," it completed the world's largest single supercomputing cluster, Colossus, aiming to冲刺 (sprint to) a scale of 1 million GPUs, demonstrating extremely aggressive and efficient infrastructure delivery capabilities.

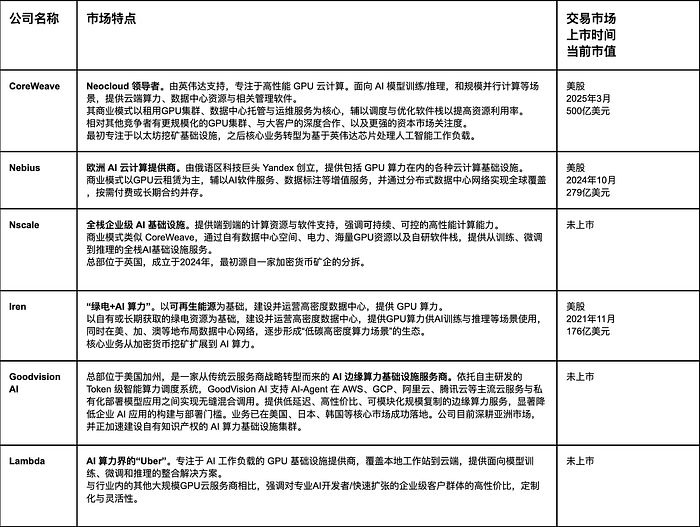

Other emerging cloud service providers like CoreWeave, Nebius, etc., are called NeoClouds. Their main business expands to IaaS + PaaS (Platform as a Service). Compared to the general cloud platform services provided by giants, Neo Clouds focus on building high-performance computing platforms for AI training and inference, not only providing more flexible computing power leasing solutions but also offering computing power scheduling solutions specifically tailored for AI training and inference needs, with faster response times and lower latency.

They also hoard the top-tier GPUs (H100, B100, H200, Blackwell, etc.) and build their own high-performance AIDCs (AI Data Centers), pre-installing entire机组 (machine groups), liquid cooling, RDMA networks, and scheduling software, and quickly deliver them to customers through flexible leases charged by the整机 (entire machine) or整园区 (entire campus) + per day.

The head player among Neo Clouds is undoubtedly Coreweave; as one of the most eye-catching tech stocks in 2025, Coreweave's current core business is cloud computing and GPU-accelerated infrastructure services偏向 (leaning towards) AI training and inference scenarios. Of course, companies eyeing computing power rental are not limited to CoreWeave; Nebius, Nscale, and Crusoe are all its strong competitors.

Different from Neo Clouds like CoreWeave博弈 (gaming) in the heavy-asset computing power cluster scale in European and American markets, GoodVision AI represents another possibility for computing power globalization — through intelligent scheduling and management of multiple computing power users, it builds rapidly deployable, low-latency, cost-effective AI infrastructure in emerging markets with relatively weak power and infrastructure, achieving the equalization of computing power. On one hand, giants are building million-GPU clusters in places like Memphis for training larger-parameter models; on the other hand, GoodVision AI addresses the "last hundred kilometers" latency response problem for AI application落地 (landing) through modular inference computing power nodes distributed in emerging markets like Asia.

It is worth mentioning that most top AI computing power service providers have a clear characteristic: their founding teams or core architectures are deeply rooted in crypto mining. Transitioning from mining to AI computing power is not a跨行 (cross-industry move) but a strategic reuse of core capabilities. BTC mining and AI high-performance computing are高度同构 (highly isomorphic) at the underlying logic, both极度依赖 (heavily relying on) large-scale electricity acquisition, high-power consumption center deployment, and 7×24-hour extreme operation and maintenance. The experience in cheap electricity channels and hardware management accumulated by these companies in their early years has become the most scarce premium asset under the AI wave.

As AI computing power demand grows exponentially, they naturally switch these existing infrastructures from "mining store-of-value assets (BTC)" to "outputting productive computing power (AI)." And as "bidirectional switching" technology matures, BTC can很好地平衡掉 (well balance) the problem of uneven distribution of energy across time and space. Therefore, entering the digital intelligence era, the "fuel" driving the productivity leap will change from oil to computing power, and the "underlying asset" carrying its value anchor will also evolve from gold to BTC.

Combining blockchain technology to put computing power on-chain as an RWA asset can not only achieve verifiable records of computing power source, usage efficiency, and operational收益 (returns) but also build cross-regional, cross-temporal smart contract settlement mechanisms, thereby reducing credit risk and intermediary costs and expanding its application scenarios in DeFi and cross-border computing power leasing. For example, edge computing power nodes, whose load rates, energy efficiency ratios, and other parameters can be quantified through intelligent scheduling providing PoW proof and smart contracts, can make edge inference computing power a transferable,抵押 (collateralizable) standardized financial product, realizing an "on-chain computing power market." The combination of computing power and RWA will further enrich the types of on-chain assets, opening up a全新的 (brand new) liquidity space for the global capital market.

Connecting Productivity and Store of Value: Towards a Future of Monetized Computing Power

This is the现实印证 (real-world confirmation) of the "dual consensus" logic we proposed earlier: BTC is the top-level value anchor of energy, while AI is the productive application of energy. From this perspective, the era of "computing power as currency" is coming faster and more disruptively than imagined. As humanity enters the digital intelligence era, the "fuel" driving the productivity leap is shifting from oil to computing power, and the "underlying asset" supporting its value consensus is also evolving from gold to BTC.

At this moment, we are like the onlookers standing on the muddy land of Pennsylvania in 1859, unable to imagine how that drill bit penetrating deep into the ground would open a new era of industrial civilization. Today, fiber optic cables extending to data centers around the world are quietly构筑 (building) the arteries of the new era. And those pioneers who first bet on computing power and BTC will also play the role of new "oil tycoons" in this transformation, redefining the distribution of wealth and power in the new cycle.

References:

John S. Gordon [US]: 《The Great Game: The Emergence of Wall Street as a World Power》

Daniel Yergin [US]: 《The Prize: The Epic Quest for Oil, Money & Power》

Goldmansachs: AI infrastructure stocks are poised to be the next phase of investment

https://www.goldmansachs.com/insights/articles/ai-infrastructure-stocks-poised-to-be-next-phase

Goldmansachs: AI, data centers and the coming US power demand surge

https://www.goldmansachs.com/pdfs/insights/pages/generational-growth-ai-data-centers-and-the-coming-us-power-surge/report.pdf

Bloomberg: Generative AI to Become a $1.3 Trillion Market by 2032, Research Finds

https://www.bloomberg.com/company/press/generative-ai-to-become-a-1-3-trillion-market-by-2032-research-finds/

KPMG: Bitcoin’s role in the ESG imperative

https://kpmg.com/kpmg-us/content/dam/kpmg/pdf/2024/bitcoins-role-esg-imperative.pdf

Square: Bitcoin is Key to an Abundant, Clean Energy Future

https://assets.ctfassets.net/2d5q1td6cyxq/5mRjc9X5LTXFFihIlTt7QK/e7bcba47217b60423a01a357e036105e/BCEI_White_Paper.pdf

Arthur Hayes: Bitcoin will be the currency of artificial intelligence

https://www.theblock.co/post/238311/bitcoin-ai-currency-arthur-hayes

36Kr: CoreWeave: In the Era of Computing Power, Holding the "Golden Shovel"

https://36kr.com/p/3501795977632640

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush