Written by: Vaidik Mandloi

Compiled by: Saoirse, Foresight News

Perpetual futures (Perps) trading volume exceeded $90 trillion last year, a figure surpassing the combined economic output of the world's top ten largest economies by GDP. Perpetual contracts now account for three-quarters of total crypto derivatives trading volume, exhibiting growth unmatched by any other modern financial product.

However, prior to this, no entity in the U.S. could legally offer perpetual futures trading—a stalemate broken last Friday. On May 29, the U.S. Commodity Futures Trading Commission (CFTC) approved Kalshi to list the nation's first regulated Bitcoin perpetual futures contract; on the same day, regulators greenlit Coinbase to route its users to global perpetual and options products via the Dubai-based Deribit platform.

Following the news, HYPE, the native token of the leading on-chain perpetuals platform Hyperliquid, surged over 30% intraday. Hyperliquid is currently the largest decentralized perpetual futures exchange by volume and does not serve U.S. users. CFTC Chairman Michael Selig wrote in a CoinDesk op-ed, defining perpetual futures as "an indispensable tool for risk management and price discovery in the global crypto asset market." For those within the crypto industry witnessing this regulatory shift firsthand, the implications are profound. The article below details the far-reaching significance of this development.

What are Perpetual Futures? How Did They Grow to a $90 Trillion Market?

The conceptual blueprint for perpetual futures dates back to 1993 when Nobel laureate in economics Robert Shiller published a paper proposing a futures contract without an expiration date: allowing homeowners to hedge against falling property prices without needing to sell their actual homes.

Source: WSJ

Although theoretically valuable, implementation was not feasible under the derivative market rules of the time. The entire industry then was built around futures with fixed expiration and settlement dates, with clearing systems and margin controls designed for periodic settlement; agricultural futures settled monthly, bond futures aligned with coupon dates—the infrastructure for perpetual products was absent, leaving the theory confined to academic literature for decades.

In May 2016, Arthur Hayes, Ben Delo, and Sam Reed founded BitMEX in Hong Kong, realizing a refined version of Shiller's vision: launching Bitcoin futures with no expiry, introducing a funding rate mechanism to peg prices to the spot market, and offering leverage up to 100x. Within 18 months of launch, BitMEX became the world's leading crypto derivatives exchange.

How Perpetual Futures Work

Traditional futures specify a fixed delivery date. For example, a Bitcoin futures contract expiring in June 2026 forces settlement at the market price upon expiry in June. Traders wishing to maintain their position must roll over into the next contract cycle; frequent rolling incurs transaction costs and creates gaps in exposure.

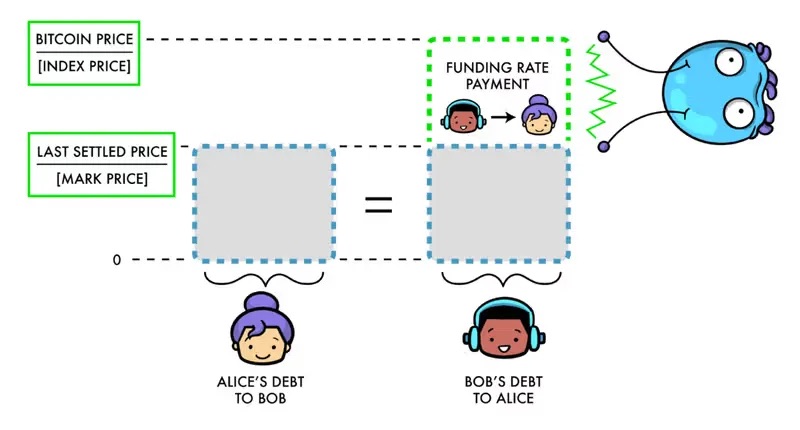

Perpetual futures eliminate the expiry mechanism entirely, allowing users to hold positions indefinitely, choosing to close them in five minutes or five months. Without the forced settlement of traditional futures to anchor prices to spot, perpetuals rely on the funding rate to continuously narrow the gap between the contract price and the underlying spot price, ensuring it reflects the true market.

Source: Paradigm.xyz

A core advantage driving the rapid rise of perpetual exchanges is liquidity aggregation. Traditional futures fragment liquidity across separate order books for quarterly contracts (March, June, September, December), while perpetuals concentrate all liquidity into a single order book, significantly enhancing trading efficiency. Financial markets benefit from an efficiency compounding effect: more traders lead to narrower bid-ask spreads, attracting further incremental capital.

Offshore perpetuals trading volume skyrocketed from $28 trillion in 2023 to over $90 trillion in 2025. Growth in decentralized, on-chain perpetuals was even more explosive, with volume reaching $6.7 trillion in 2025, a 346% year-over-year surge. In daily trading, perpetuals volume is 10 to 15 times that of spot markets, cementing crypto asset pricing dominance within derivatives. Daily Bitcoin price swings of around 5% often originate in perpetuals markets, where cascading liquidations of leveraged positions trigger waves of selling or buying, with spot prices following passively.

Before this U.S. regulatory approval, the perpetuals sector, which dictates market-wide pricing, remained closed to domestic U.S. institutions.

What Changes Does U.S. Approval Bring to the Industry Landscape?

While the U.S. has legalized perpetuals, the domestic regulated product differs significantly from the global offshore market version. Even Coinbase must route user orders through its Bermuda subsidiary to Deribit in Dubai. The offshore market, having accumulated vast liquidity over years in a regulatory gray area, is unlikely to flow back to the U.S. mainland in the short term.

U.S. regulated perpetuals are capped at 10x leverage, with customer funds fully protected under CFTC segregation rules. In contrast, offshore markets commonly offer 50x-100x leverage. At 100x leverage, $1 of capital controls a $100 position, where a 10% price move can double the capital or wipe it out. For the same 10% price movement, a standard one-month Bitcoin call option might only yield about 3x profit, due to upfront premium payment and time decay. High leverage is the core appeal of offshore perpetuals; the U.S. regulated version is conservative and fundamentally different.

This is key to understanding HYPE's rally post-CFTC approval: initial market fears of capital flowing from Hyperliquid to U.S. platforms like Kalshi and Coinbase proved unfounded. Hyperliquid generated $907 million in revenue last year with zero U.S. users. The two user bases are inherently distinct: retail speculators opening 50x short positions on meme coins overnight won't switch to a U.S. platform for 10x Bitcoin trades; institutional capital requiring regulated custody and asset segregation wouldn't have been on Hyperliquid in the first place.

The U.S. regulatory move essentially provides official validation of the legitimacy of the perpetuals sector where Hyperliquid operates, constituting a fundamental positive for the platform.

Currently, U.S. regulated exchanges are only approved to list Bitcoin perpetuals as a single asset. Hyperliquid, however, has long moved beyond crypto: through community governance proposal HIP-3, anyone can list perpetuals for virtually any asset on the platform, with many already live. In February, silver perpetuals daily volume spiked to $4 billion; in April, crude oil perpetuals volume briefly surpassed Bitcoin's at times.

ICE (Intercontinental Exchange, parent of NYSE) CEO Jeffrey Sprecher remarked at a Bernstein industry conference just before the CFTC approval: "The firm we're talking about, Hyperliquid, has already surpassed Nasdaq in size." ICE teams are now proactively engaging with Hyperliquid to study its product architecture and questioning regulators on why traditional exchanges cannot replicate such products. Wall Street is beginning to learn from a two-year-old, venture-capital-free decentralized exchange.

Perpetual Futures Are Encroaching on the Entire Traditional Derivatives Market

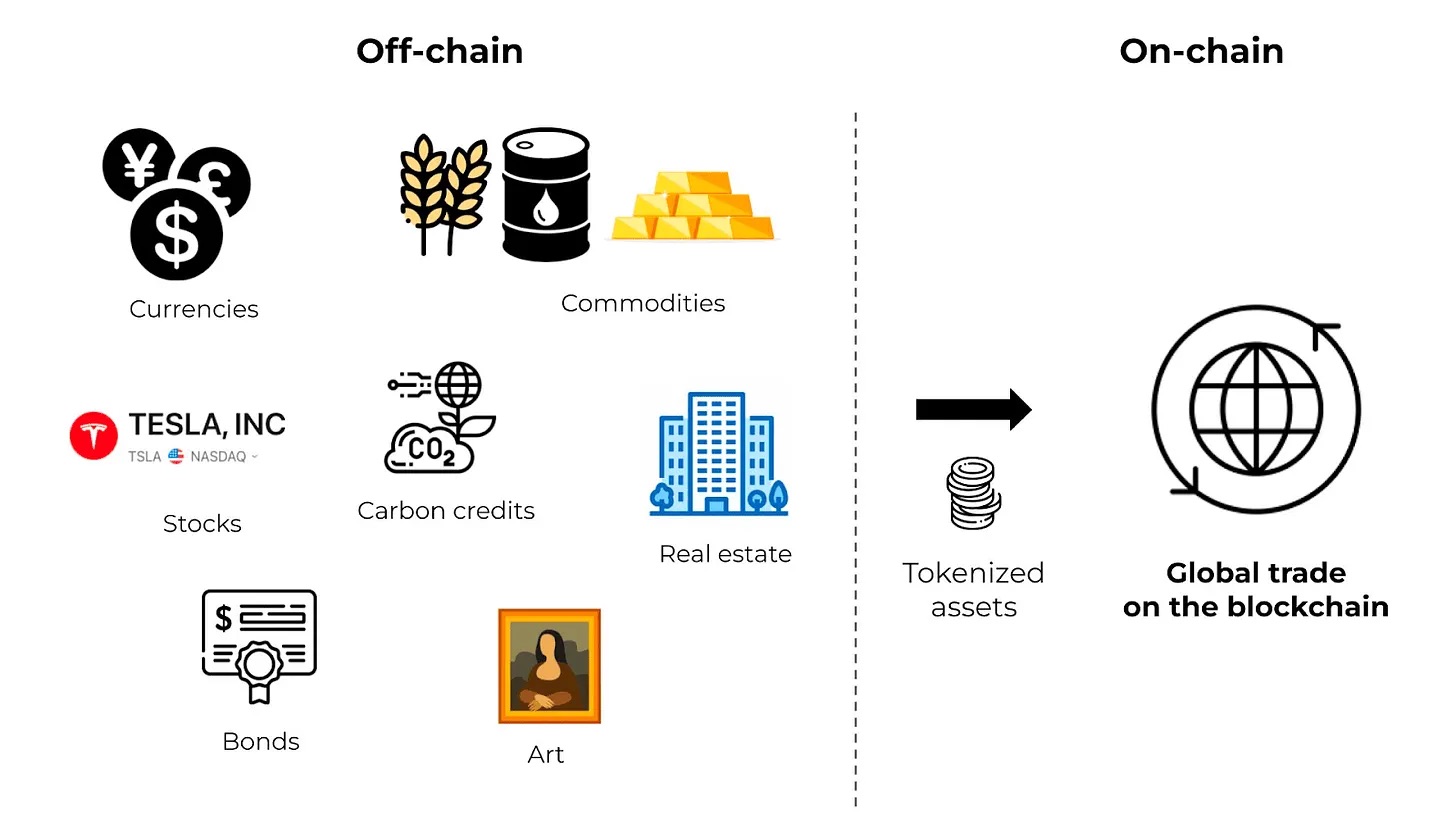

The deeper impact of this regulatory approval is that perpetual futures are no longer confined to the crypto sphere but are beginning to permeate all asset classes in financial markets.

The product evolution path: from native Bitcoin, extending to all altcoins; then launching for commodities like gold, silver, crude oil; expanding to individual stocks like Nvidia and Tesla, and even shares of private companies like SpaceX and OpenAI; with HIP-4 proposal, the platform now lists prediction market perpetuals.

Source: EBC Financial Group

In just two years, perpetuals have evolved from a niche crypto innovation into a standardized financial product offering 24/7 trading, no expiry, elimination of intermediate clearing layers, and the ability to reference any global asset. Traditional derivatives were born in the era of physical floor trading, with exchanges having fixed daily closures, and contract cycles designed for paper-based settlement rules.

In today's digitally interconnected global market operating around the clock, traditional products with fixed trading hours inherently create price gaps. For instance, an oil trader wanting to position before a weekend geopolitical event has no tool on traditional regulated exchanges, whereas Hyperliquid allows opening a position at any time. The CFTC's official research notes also explicitly state: due to digital infrastructure and global nature, crypto-linked derivatives are naturally suited for 24/7 trading.

The ensuing industry race will focus on whether U.S. regulated traditional exchanges can iterate quickly enough to defend their market share. A fee comparison: traditional centralized exchange futures fees are around 4 basis points, while Hyperliquid charges just 2 basis points; spot fees are ~15 bps on traditional platforms vs. as low as 5 bps on Hyperliquid. Switching platforms takes users only minutes, and capital naturally migrates to lower-cost venues.

The week of the approval, Compass Point analysts downgraded Coinbase to Sell, citing intensifying competition in the derivatives space, continuously squeezing the platform's pricing power and profit margins. In Q1 2026, Coinbase's perpetuals business generated $50 million in revenue, but retail spot revenue fell to its lowest since Q3 2024: as perpetuals expand, they continuously cannibalize the higher-margin spot business.

The profitability logic across all derivative categories is being compressed by perpetuals. With perpetuals, investors avoid the frequent rolling of quarterly futures to maintain positions (incurring double fees each roll). Most short-term traders hold positions for only hours to days, making the no-expiry perpetual experience far superior to traditional contracts requiring periodic rolling.

Short-term options also face substitution pressure. Both short-dated options and perpetuals can be used for directional leveraged trades, with options' only advantage being capped loss limited to the premium paid. In 2025, the average daily volume for 0DTE (zero days to expiry) single-day options on U.S. stocks was 2.3 million contracts, with the vast majority merely speculating on short-term price moves—a demand that perpetuals can fulfill at lower cost.

This article does not claim perpetuals will completely replace options and traditional futures; options' unique capped loss and non-linear payoff profiles are irreplicable by perpetuals. However, for the majority of short-term leveraged speculative demand—which constitutes the largest market share—perpetuals offer a superior solution with lower costs and no expiry, a value proposition validated by their $90 trillion annual trading volume.