Written by: Anna Irrera, Bloomberg

Compiled by: Saoirse, Foresight News

For years, major banks largely watched from the sidelines as stablecoins evolved from a niche cryptocurrency category into payment networks handling trillions of dollars in annual flow. Now, the banking industry aims to replicate the collaborative model that built Zelle, hoping that building shared infrastructure will stem the ongoing erosion of their business territory by various forms of digital dollars.

Leading banks including JPMorgan Chase, Bank of America, HSBC Holdings, Citigroup, and Wells Fargo recently unveiled a joint plan to establish an interoperable network for tokenized bank deposits. Tokenized bank deposits are digital representations of funds held within the commercial banking system, which can be transferred using blockchain payment rails – a technology originally popularized by the crypto industry.

The Zelle logo on a smartphone. Photographer: Tiffany Hagler-Geard / Bloomberg

This initiative, to be operated by The Clearing House (TCH), marks the first large-scale coordinated effort by the US banking sector to counter stablecoins. Stablecoins, typically pegged to the US dollar, can process payments and settlements around the clock and are seeing their use cases expand.

Banks are increasingly recognizing that the competitive threat posed by stablecoins is no longer theoretical. While initially used mostly for crypto trading, stablecoins are now being adopted by a growing number of payment firms and financial institutions seeking cheaper, faster channels for fund movement. Data from analytics firm Artemis Analytics shows stablecoin transaction volume surged 72% last year to approximately $33 trillion; Bloomberg Intelligence predicts stablecoin payment flows could exceed $50 trillion by 2030.

The banking industry's move clearly references Zelle as a model. Over a decade ago, banks joined forces to create a peer-to-peer shared payment network to compete with rapidly rising consumer payment apps like Venmo. The project took years to materialize, but Zelle now handles over $1 trillion in payments annually, standing as one of the industry's most successful defenses against external competitors.

However, whether banks can replicate this success is highly uncertain. The market is evolving rapidly, and dozens of rival institutions need to agree on technical standards, governance rules, and commercial incentives. The financial sector has a history of alliance projects stalling due to divergent interests slowing decision-making and investment.

Alessandro Hatami, Managing Partner at fintech consultancy Pacemakers.io and former Head of Digital Payments at Lloyds Bank, stated: "These are the same banks that have been announcing various blockchain projects for the past decade. Banks compete with each other, making it inherently difficult to build shared infrastructure."

With regulatory winds shifting towards leniency during the Trump administration, Wall Street has been pushing forward with tokenization efforts. US policymakers believe dollar-pegged tokens can reinforce the dollar's global dominance while boosting demand for US Treasuries.

The passage of the GENIUS Act last year, establishing a comprehensive regulatory framework for stablecoins, served as a clarion call for their mainstream adoption. The policy debate has since shifted towards market regulations and whether to allow stablecoin issuers to offer yield or rewards – a move that could severely divert bank deposits.

Nicole Sandler, Chief Ecosystem Officer at tokenized settlement startup Ubyx, said: "The competitive threat is now visible and quantifiable. Banks are constantly discovering clients moving money via stablecoins. This is completely different from the distant, abstract potential threat of the past."

Connecting Various Payment Channels

Banks have been experimenting with blockchain technology for years, both individually and collectively. Major institutions like JPMorgan, Citi, and Bank of New York Mellon have launched their own blockchain-based payment systems, allowing clients to transfer funds 24/7.

While these proprietary platforms share some characteristics with stablecoins and benefit from being bank money – such as earning interest and enjoying deposit insurance – transfers are often limited to clients within the same bank. In contrast, stablecoin users can send funds to anyone globally, regardless of their banking institution.

A core goal for The Clearing House is to achieve interoperability between different digital currency systems, thereby vastly expanding reach and transaction scale.

Debopama Sen, Head of Payments for Citi's Services business, pointed out: "Achieving interoperability and building a scalable platform to simplify operations for clients is crucial. Many of our large clients operate globally and bank with multiple institutions."

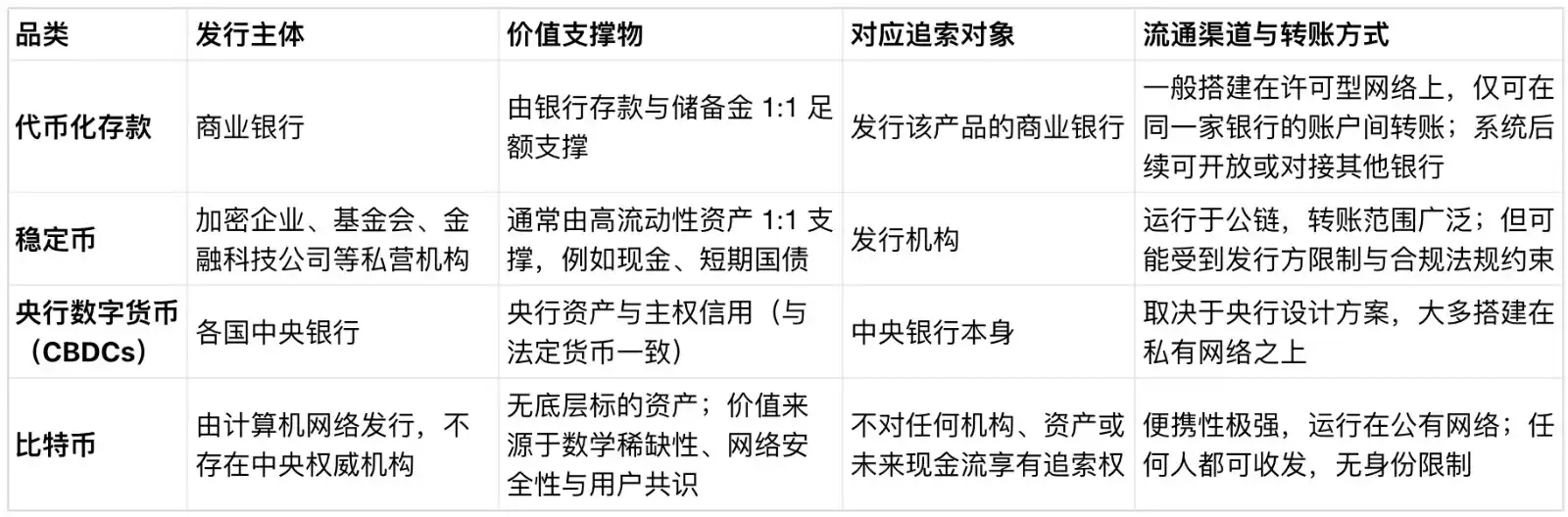

Blockchain-Based Forms of Money, Source: Bloomberg

The Clearing House's plan involves connecting financial institutions that collectively manage trillions in deposits and serve tens of millions of customers. The resulting network's scale and reach would far exceed the current stablecoin market.

Christopher Ward, Head of Corporate Payments at Truist Financial, said: "The logic is no different from when the US pushed for real-time payments. Parties came together, established common rules, and achieved widespread adoption. The current project follows the same thinking."

The Clearing House, with its deep experience in operating industry networks, is well-suited to coordinate among the diverse interests of community banks, regional banks, multinational giants, and foreign banks operating in the US. The project is slated for launch next year.

Elena Casal, Chief Customer Officer at The Clearing House, said: "Building shared industry infrastructure is in our DNA. We already have established governance frameworks and regulatory compliance processes, which can help accelerate project implementation."

Elena Casal mentioned that demand is primarily in the wholesale payments space, particularly for corporate treasury management and liquidity movements. The network could also provide digital cash for the clearing and settlement of tokenized securities, empowering the development of tokenized capital markets. The Clearing House is currently selecting technology service providers, and the network is designed with extensibility, potentially supporting stablecoin settlement in the future.

Crowded Field, Multiple Players Compete

Despite The Clearing House's strong foundation for success, the bank-led digital currency space is already crowded, with many similar projects initiated a decade ago. Banks participating in multiple parallel projects risk further fragmenting the industry, hindering the formation of a united front.

Last week, payments messaging giant SWIFT revealed that over 17 banks are preparing to pilot cross-border tokenized payments on its new distributed ledger. Additionally, Goldman Sachs, Deutsche Bank, Bank of America, Spain's Santander, and others formed an alliance late last year to develop a stablecoin-like digital currency.

Manish Kohli, Global Head of Payments Solutions at HSBC, analyzed that platforms built by upgrading existing, proven systems have a much higher chance of success than projects built from scratch. Citing The Clearing House's current plan: "The project leverages existing infrastructure, has a stable membership base, clear use cases in the US domestic market, making the implementation risk much lower." HSBC is participating in multiple projects, including the SWIFT pilot, the UK's "UK Tokenized Deposit Initiative," and Hong Kong's Ensemble project.

The Difficult Task of Self-Reinvention

While banks hold significant advantages in asset size and regulatory standing, their inherent weakness is slow decision-making and execution. Zelle itself took years to develop and might not have flourished without pressure from competitors like Venmo; even after the technology was ready, alliance members argued over the product name.

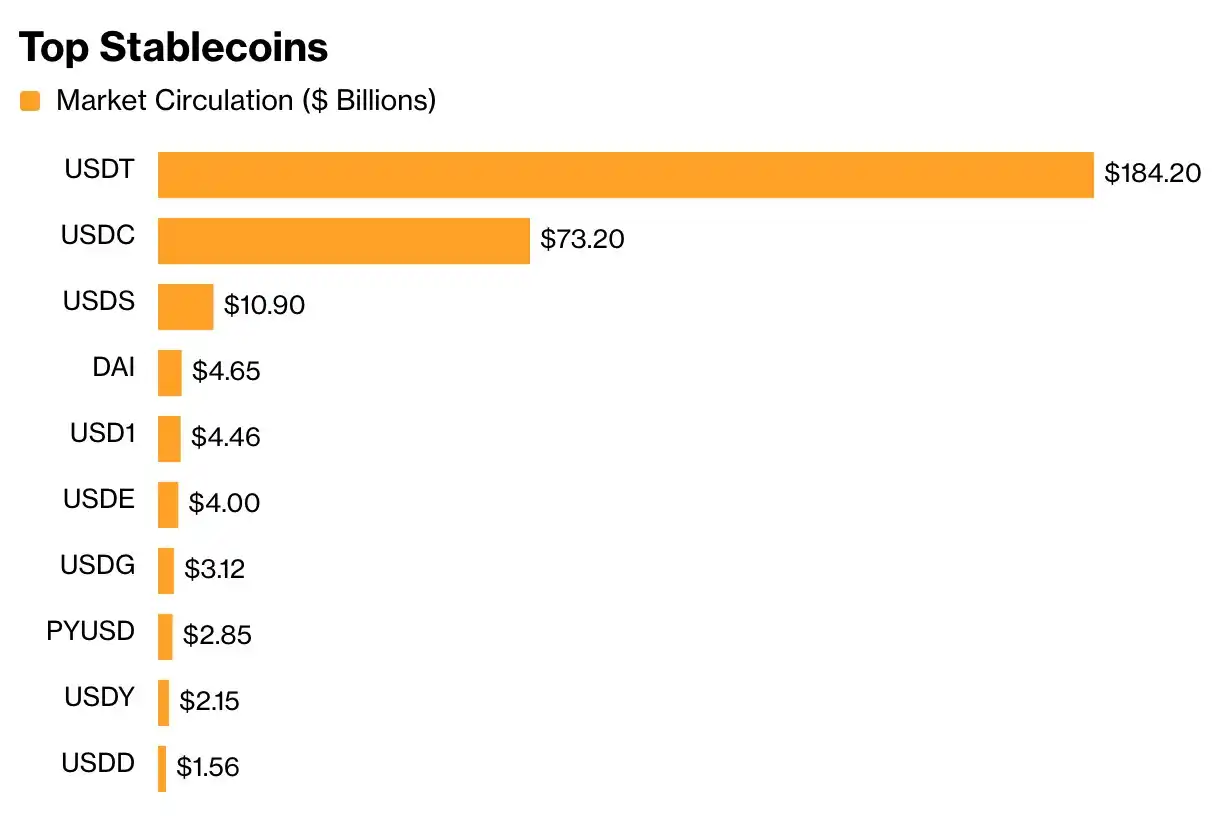

Furthermore, transformation isn't guaranteed even for established payment giants. PayPal launched its stablecoin PYUSD in August 2023, but adoption has been minimal, with a circulation of only $2.9 billion – negligible compared to leading stablecoins: Tether's USDT circulates at around $184 billion, and Circle's USDC at $73 billion.

Leading Stablecoins, Source: GoinGecko

From this perspective, leading stablecoin issuers need not panic just yet. Conversely, banks may not need to rush for first-mover advantage: many of the largest and most profitable corporate clients in banks' payment divisions currently have no urgent need for programmable dollars.

Marieke Flament, co-founder of digital currency consultancy Currency of Power, commented: "Banks may seem slow, but once they decide to move, they can mobilize massive resources. However, the crypto space moves extremely fast, and whether banks can keep pace remains a major challenge."

Reporting assistance from Paige Smith, Olga Kharif, Yizhu Wang

![How high can MemeCore [M] rally as it leads top 100 with 16% gains?](https://d1x7dwosqaosdj.cloudfront.net/images/2026-07/3d45ef1ea56e45f6a19ae78972d369b7.jpg)