This report is written by Tiger Research. The cryptocurrency market continues to be in a prolonged downturn. In this environment, the projects that can survive are those that demonstrate pragmatism and a realistic vision.

Core Points

- Projects that solve real, specific problems can maintain resilience even during market downturns.

- Hyperliquid, Canton, and Kite target different problem areas, but they share a common trait: providing practical and realistic solutions, rather than abstract narratives.

- To assess this realism, analysis should focus on three factors: the problem the project aims to solve, the structure of the solution, and the team's ability to execute in practice.

1. Conditions for Survival in a Bear Market: Does it Work in Practice?

Source: Tiger Research

Bitcoin has fallen below $70,000. Among the top 100 cryptocurrencies by market cap, only 7 remain above their 200-day moving average. In contrast, 53 components of the Nasdaq 100 index are still trading above this threshold.

The market conditions are undeniable. Nevertheless, some crypto assets still manage to survive in the harshest environments.

Their resilience cannot be simply attributed to artificial market making or coincidental rebounds. A closer look at their development trajectory reveals a different explanation.

These projects no longer rely solely on vague visions or technical complexity. Instead, they share a common feature: solving core market problems with solutions rooted in practical reality. Their approach typically aligns with three directions:

- Do they solve a problem the market is currently facing?

- Are they ready for practical application in the near term?

- Are they building infrastructure that the industry will rely on long-term?

Ultimately, the ability to solve real problems in practice remains the most powerful fundamental.

2. Three Directions Chosen by the Market

Projects that can answer the above questions have successfully survived. Their approach is: 1) clearly identify a market problem; 2) propose a practical solution that matches a specific timing.

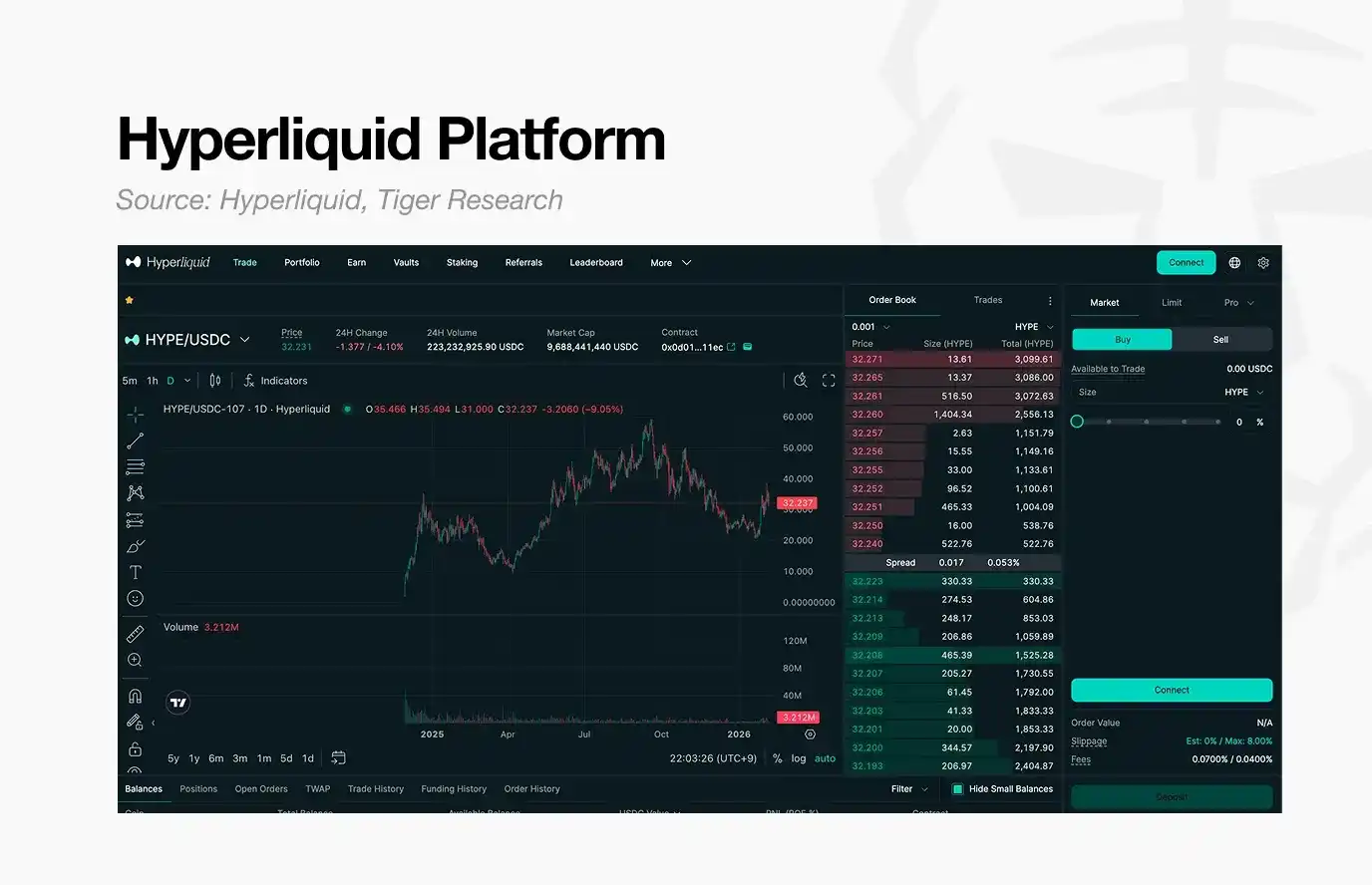

2.1. Hyperliquid: Solving Immediate Trading Friction

Centralized exchanges have traditionally been seen as responsible intermediaries. However, in practice, when problems arise, they often fail to align with investor interests. Decentralized exchanges emerged as an alternative, but poor user experience and performance have caused many investors to steer clear.

In this context, Hyperliquid introduced the concept of a perpetual contracts decentralized exchange (perp DEX). Through its HLP mechanism, it brings the features investors value in centralized exchanges—such as high leverage, fast execution, and stable liquidity—into an on-chain environment.

Early usage was partly driven by demand for the $HYPE token airdrop. However, continued engagement post-airdrop reflects user satisfaction with the platform's performance.

Ultimately, Hyperliquid's resilience stems from solving a persistent, real-world problem: dissatisfaction with centralized exchanges.

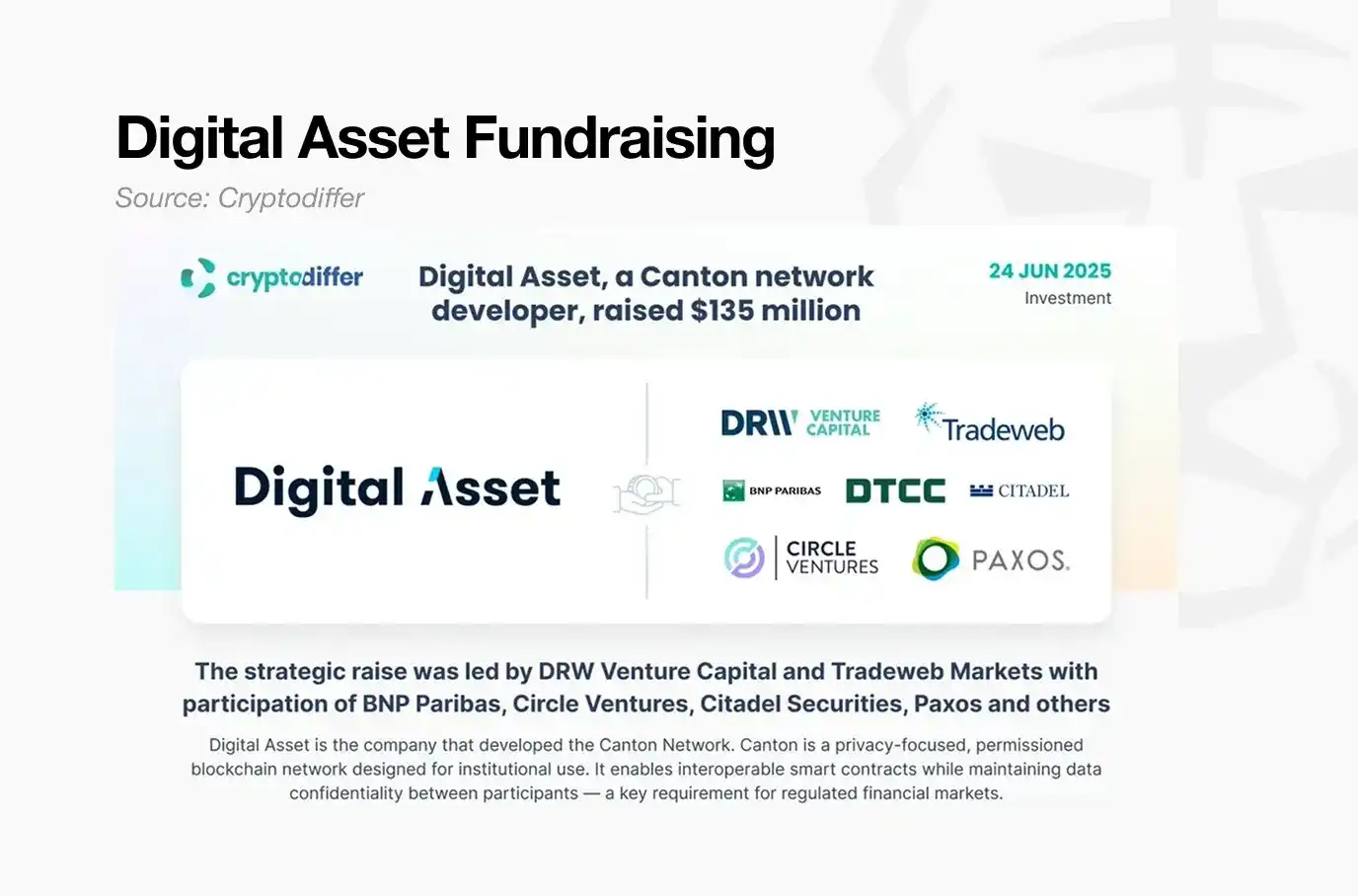

2.2. Canton Network: Preparing for the Era of Institutional Finance

Canton proposes a solution for the near future. As interest in real-world assets (RWA) continues to rise, institutions are beginning to see blockchain as financial infrastructure, not a public network. In this context, what institutions need is not complete data transparency, but a selective privacy model that supports regulatory compliance and confidentiality.

The Canton Network was born. Through DAML, Canton can provide configurable data disclosure for each participant.

This allows institutions to maintain transaction confidentiality while sharing information only to the necessary extent. Instead of imposing a provider-driven design, Canton builds infrastructure that aligns with institutional needs.

Another key factor is that Canton, from the outset, has focused on scaling its ecosystem with real-world deployments, supported by early partnerships with financial institutions.

Most notably, its partnership with DTCC establishes a pathway for assets managed by the traditional financial system to extend into a Canton-based environment. DTCC handles approximately $3.7 quadrillion in transactions annually, highlighting the practical feasibility of the Canton Network's approach.

Ultimately, the Canton Network provides a structural solution designed to meet three institutional requirements simultaneously: privacy protection, regulatory compliance, and integration with the existing financial system.

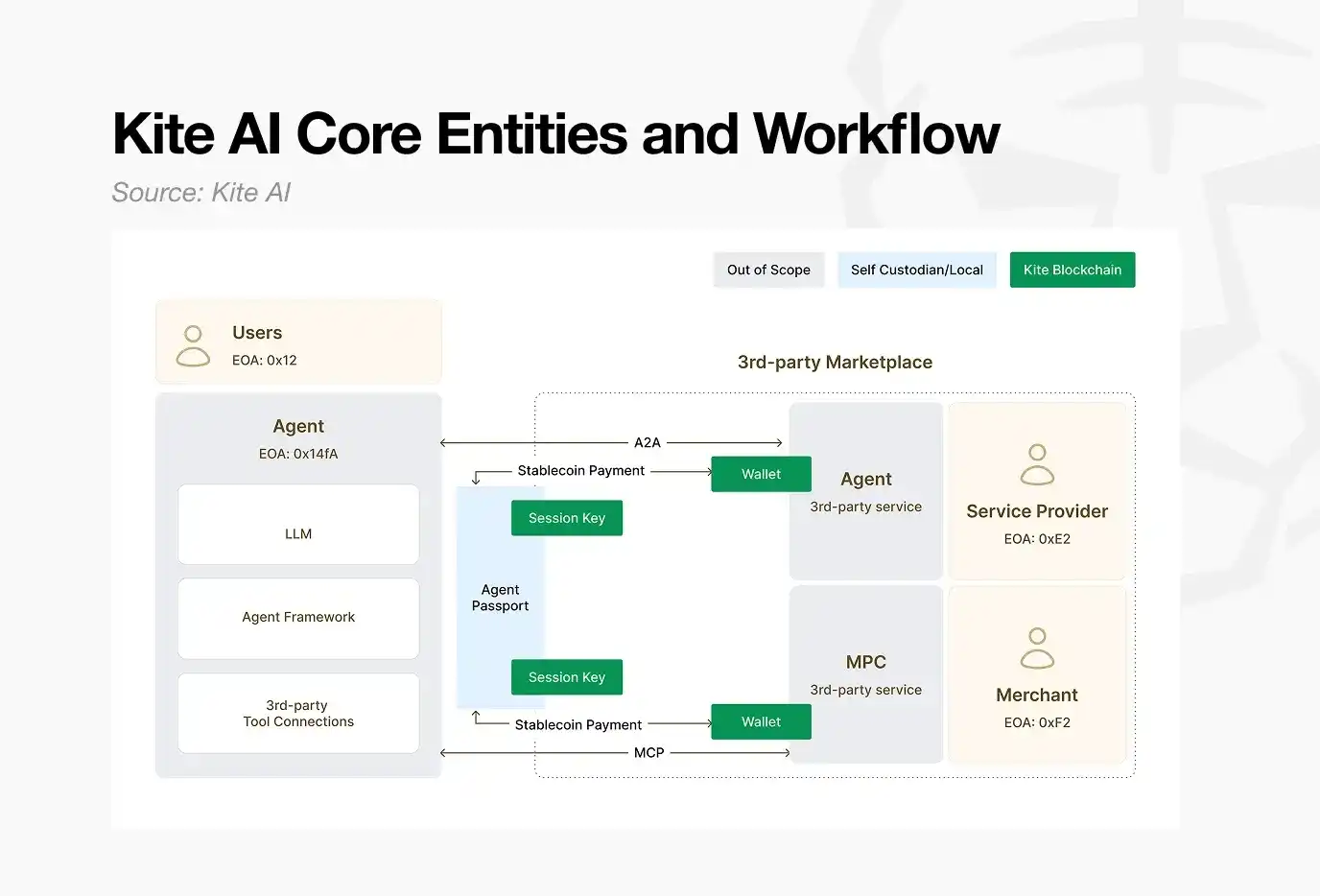

2.3. Kite AI: Building the AI Economy That Has Not Yet Arrived

Unlike the previous two examples, Kite AI currently has limited practical application. However, from the future perspective of AI agents operating as economic actors, its structural logic remains compelling.

There is broad consensus in both Web2 and Web3 about an agent-driven future. Few question scenarios where AI agents handle tasks like booking hotels or buying groceries on behalf of users.

However, such a future requires infrastructure that allows AI agents to independently initiate and execute payments. Existing transaction systems are designed for transfers between people, and for efficiency among human participants.

Therefore, for AI agents to operate as autonomous economic entities, new mechanisms are needed, including identity verification and automated payment frameworks.

Kite AI is building payment infrastructure for this environment. Its core components include an "Agent Passport" for identity verification and the x402 protocol functionality for enabling automated payments.

The vision proposed by Kite AI cannot be deployed at scale currently, simply because the future it targets has not yet materialized.

Nonetheless, the project's realism stems from a broader premise: when this widely anticipated future arrives, the underlying technology it is developing will be necessary. This alignment with a widely accepted development trajectory gives the project structural credibility, despite its current limited use.

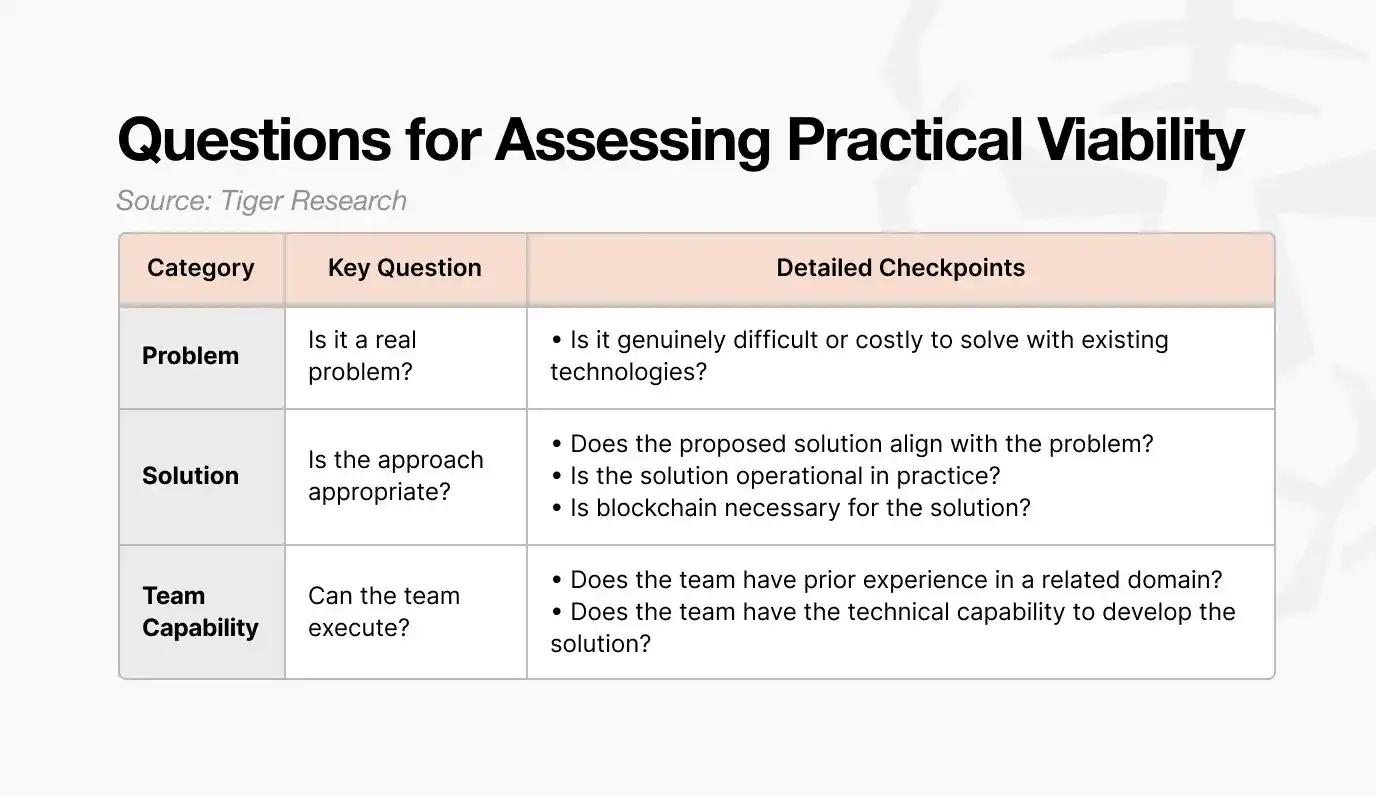

3. Three Key Questions for Assessing Practical Feasibility

Although these three projects have different timelines, they share a common characteristic: real-world feasibility.

Evaluations of the same project often diverge. Some believe it solves a real problem, while others see it as overhyped. To bridge this interpretation gap, at least three core questions must be asked:

Source: Tiger Research

- What problem does it solve? Is the problem the project targets real and is there market demand for it?

- How does it solve it? Is the proposed solution structurally sound and executable?

- Who is executing it? Does the team have the capability and resources to turn the vision into reality?

Since most projects promote optimistic future narratives, answering these questions correctly requires time and effort. Filtering out misleading or incomplete information is not easy. Projects that cannot confidently answer these three questions may experience short-term price increases, but when the next downturn comes, they will likely disappear.

The current state of the cryptocurrency market is clearly unfavorable. But that doesn't mean it's all over. New experiments will continue, and the task is to assess what these efforts truly represent.

What matters most now is realism.