Author: Ryan Yoon

Compiled by: Deep Tide TechFlow

Deep Tide Introduction: As the market enters a downward cycle, skepticism towards the crypto market is growing. Tiger Research believes this time is different from the past: previous winters were triggered by internal issues (Mt. Gox hack, ICO scams, FTX collapse), while this cycle's rise and fall are both driven by external factors (ETF approval brought the bull market, tariff policies and interest rates caused the decline).

Post-regulation, the market has split into three layers: the compliant zone, the non-compliant zone, and shared infrastructure. Capital no longer flows via 'trickle-down' effects as it did before. ETF capital stays with Bitcoin and does not flow into altcoins.

The next bull run requires two conditions: a killer app must emerge from the non-compliant zone + a supportive macro environment.

Full text below:

As the market enters a downward cycle, skepticism towards the crypto market is growing. The question now is, have we entered a crypto winter?

Core View

- Crypto winters follow a sequence: Major event → Collapse of trust → Talent drain

- Past winters were caused by internal problems; the current rise and fall are driven by external factors; it is neither winter nor spring

- Post-regulation, the market has split into three layers: Compliant zone, Non-compliant zone, Shared infrastructure; The trickle-down effect has disappeared

- ETF capital stays with Bitcoin; it does not flow out of the compliant zone

- The next bull run requires a killer use case + a supportive macro environment

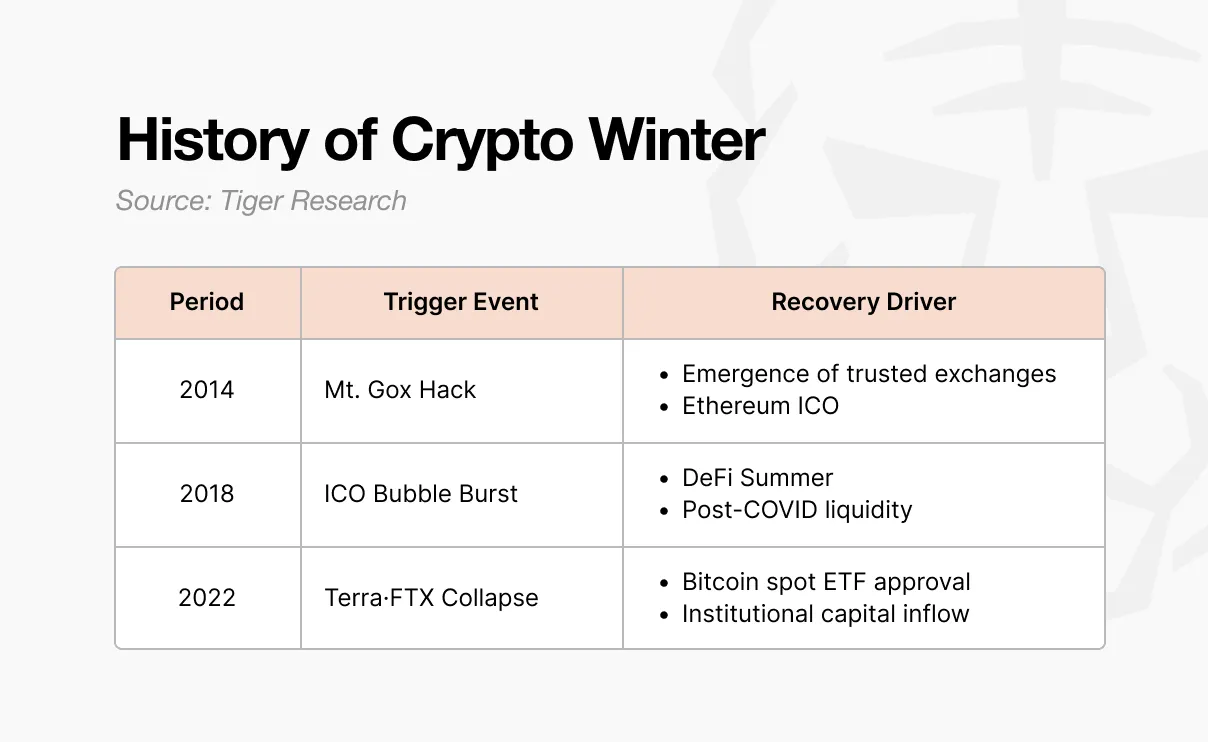

1. How did the previous crypto winters unfold?

The first winter occurred in 2014. Mt. Gox was the exchange handling 70% of global Bitcoin trading volume at the time. Approximately 850,000 BTC disappeared in a hack, causing a collapse in market trust. New exchanges with internal controls and audit functions emerged, and trust began to recover. Ethereum also entered the world through ICOs, opening up new possibilities for vision and fundraising methods.

This ICO wave became the catalyst for the next bull market. When anyone could issue a token and raise funds, the 2017 boom was ignited. Projects raising billions with just a whitepaper flooded in, but most had no substance.

In 2018, regulatory measures poured out from South Korea, China, and the US, the bubble burst, and the second winter arrived. This winter did not end until 2020. Post-COVID, liquidity poured in, and DeFi protocols like Uniswap, Compound, and Aave gained attention, bringing capital back.

The third winter was the most severe. When Terra-Luna collapsed in 2022, Celsius, Three Arrows Capital, and FTX collapsed in turn. This wasn't just a simple price drop; the very structure of the industry was shaken. In January 2024, the US SEC approved the spot Bitcoin ETF, followed by the Bitcoin halving and Trump's pro-crypto policies, and capital began to flow in again.

2. The Crypto Winter Pattern: Major Event → Collapse of Trust → Talent Drain

All three winters followed the same sequence. A major event occurs, trust collapses, talent leaves.

It always starts with a major event. The Mt. Gox hack, ICO regulation, and the FTX bankruptcy following the Terra-Luna collapse. The scale and form of each event were different, but the result was the same. The entire market was thrown into shock.

Shock quickly spread into a collapse of trust. Those who had been discussing what to build next began to question whether cryptocurrency was truly meaningful technology. The collaborative atmosphere among builders disappeared, and they began to blame each other for who was responsible.

Doubt led to a talent drain. The builders who had been creating new momentum in blockchain fell into doubt. In 2014, they moved to fintech and big tech companies. In 2018, they moved to institutions and AI. They went to places that seemed more certain.

3. Is the current situation a crypto winter?

The pattern of past crypto winters is visible today.

- Major Event:

- Trump's tariff policies caused market turbulence

- Shift in Federal Reserve interest rate policy

- Overall crypto market decline

- Collapse of Trust: Skepticism is spreading within the industry. The focus has shifted from what to build next to mutual blame.

- Pressure of Talent Drain: The AI industry is growing rapidly. It promises faster exits and greater wealth than crypto.

However, it's hard to call this a crypto winter. Past winters erupted from within the industry. Mt. Gox was hacked, most ICO projects were exposed as scams, FTX collapsed. The industry itself lost trust.

Now it's different.

ETF approval started the bull market, tariff policies and interest rates drove the decline. External factors lifted the market, external factors also pushed it down.

Builders are not leaving either.

RWA, perpDEX (perpetual decentralized exchanges), prediction markets, InfoFi, privacy. New narratives keep emerging, they are still being created. They haven't pulled the entire market like DeFi did, but they haven't disappeared either. The industry hasn't collapsed; the external environment has changed.

We didn't create spring, so there is no winter.

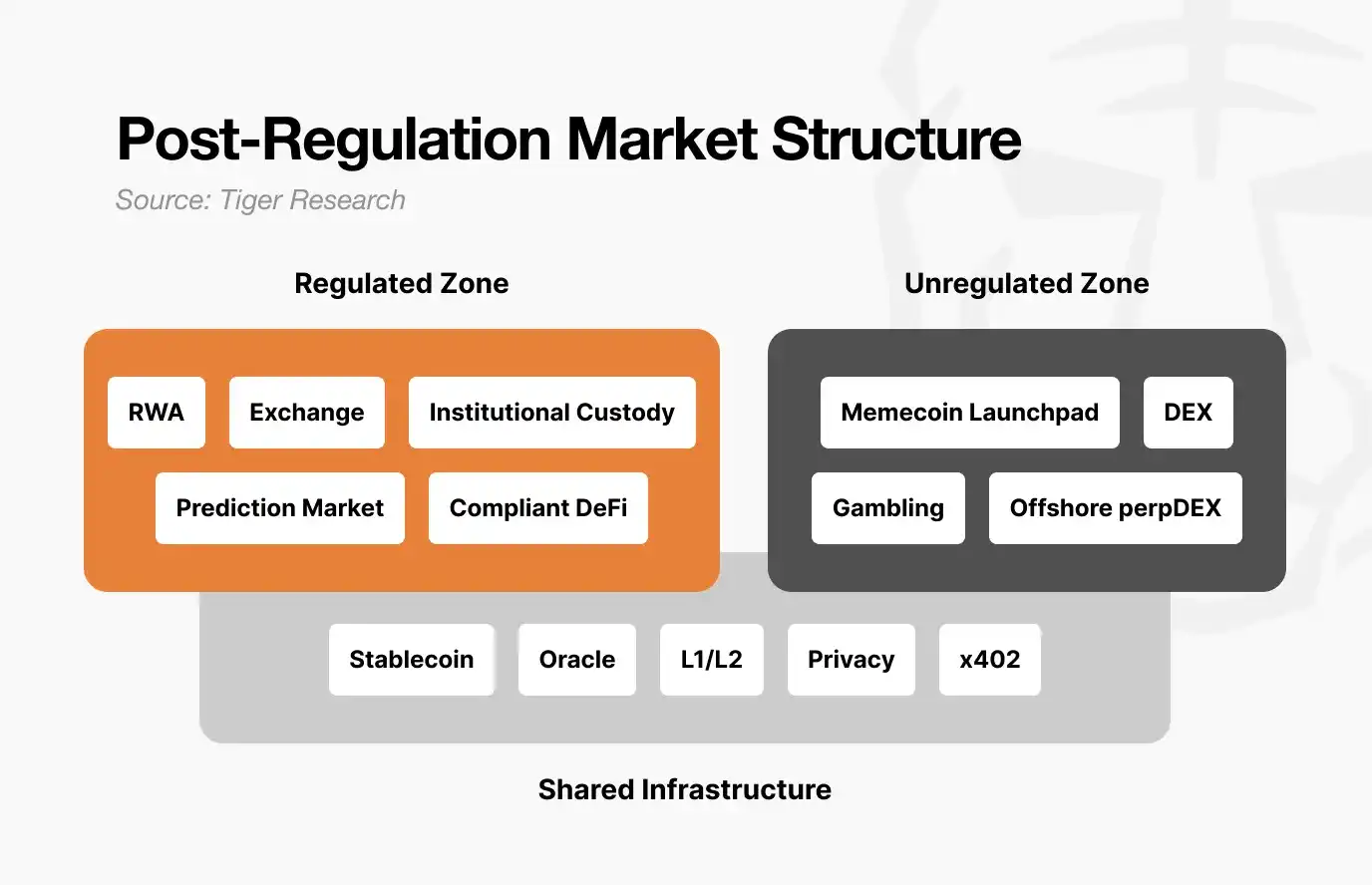

4. Changes in Market Structure Post-Regulation

Behind this is a major shift in market structure post-regulation. The market has split into three layers: 1) The Compliant Zone, 2) The Non-Compliant Zone, and 3) Shared Infrastructure.

The Compliant Zone includes RWA tokenization, exchanges, institutional custody, prediction markets, and compliance-based DeFi. They undergo audits, make disclosures, and have legal protection. Growth is slow, but the capital scale is large and stable.

However, once in the compliant zone, it's hard to expect explosive returns like in the past. Volatility is lower, and potential upside is limited. But downside risk is also limited.

On the other hand, the Non-Compliant Zone will become more speculative in the future. The barrier to entry is low, and speed is fast. Scenarios of 100x in one day and -90% the next will happen more frequently.

However, this space is not meaningless. Industries born in the non-compliant zone are creative, and once validated, they move into the compliant zone. DeFi did this, prediction markets are doing it now. It acts as an experimental field. But the non-compliant zone itself will become increasingly separated from compliant zone businesses.

Shared Infrastructure includes stablecoins and oracles. They are used in both the compliant and non-compliant zones. The same USDC is used for institutional RWA payments and for Pump.fun trading. Oracles provide data for tokenized treasury validation and for anonymous DEX liquidations.

In other words, as the market splits, capital flows have also changed.

In the past, when Bitcoin rose, altcoins rose too through a trickle-down effect. Now it's different. Institutional capital entering through ETFs stays with Bitcoin, full stop. Compliant zone capital does not flow into the non-compliant zone. Liquidity only stays where value has been proven. And even Bitcoin has not yet proven its value as a safe-haven asset relative to risk assets.

5. Conditions for the Next Bull Run

Regulation is being sorted out. Builders are still building. So two things remain.

First, a new killer use case must emerge from the non-compliant zone. Something that creates value that didn't exist before, like DeFi Summer in 2020. AI agents, InfoFi, and on-chain social are candidates, but they haven't reached the scale to drive the entire market yet. The process where experiments in the non-compliant zone are validated and move into the compliant zone must be recreated. DeFi did this, prediction markets are doing it now.

Second, the macroeconomic environment. Even if regulation is sorted out, builders are building, and infrastructure is accumulating, if the macroeconomic environment is not supportive, the upside is limited. The 2020 DeFi Summer erupted when liquidity was released post-COVID. The post-ETF approval rise in 2024 also coincided with expectations of rate cuts. No matter how the crypto industry performs, it cannot control interest rates and liquidity. For what the industry builds to gain traction, the macroeconomic environment must turn.

A 'crypto season' where everything rises together like in the past is unlikely to reappear. Because the market has split. The compliant zone grows steadily, the non-compliant zone experiences big rises and falls.

The next bull run will come. But it won't come for everyone.