A transaction that could rewrite the global payment industry landscape is quietly brewing.

On February 24, Bloomberg reported: Private payment giant Stripe, led by the Collison brothers, is considering acquiring all or part of the business of the veteran payment pioneer PayPal. On the day the news broke, PayPal's stock price surged nearly 7%.

One is a private unicorn valued at $159 billion, the other is a former king with a market cap of only $43 billion but a vast user network. Behind this potential deal lies not just a shift in market share, but a deeper game about the future form of payments—especially crypto/stablecoin payments.

PayPal's Dilemma and Trump Cards

To understand why this potential deal has caused such a stir, first look at two sets of numbers.

Over the past 12 months, PayPal's stock price has fallen nearly 46%, with its market capitalization hovering around $40 billion. Meanwhile, the yet-to-be-publicly-listed Stripe recently valued itself at $159 billion in an employee stock buyback—the former is less than a third of the latter.

Behind this inversion is PayPal's business being squeezed from multiple dimensions.

The competitive landscape has long been turned upside down. Apple Pay and Google Pay have locked down the consumer entry point via mobile operating systems, while new forces like Adyen and Stripe are constantly encroaching on the territory with their technical flexibility on the business side. PayPal, which once made its name as a "third-party guarantor," is gradually losing the scarcity of being a connector in an era of increasingly diversified payment entry points.

User habits are also quietly evolving. With the explosion of social payments and embedded finance, people prefer to complete transactions at the moment of consumption rather than jumping to a heavy third-party page. Whether it's Stripe's one-click payment or Apple Pay's biometrics, they seem more convenient than that blue icon interface that requires remembering a password. Although PayPal holds the social ace Venmo, it has always struggled to convert it into a commercial engine.

The most fundamental pain point is the loss of market confidence in its growth potential. In the old world of fiat payments, PayPal's imagination has nearly reached its ceiling; in its foray into crypto, it launched the stablecoin PYUSD but was criticized for being "compliant but lacking endogenous transaction demand," failing to penetrate the DeFi ecosystem or create unique value in its own B2B cross-border scenarios.

However, despite its beleaguered fundamentals, PayPal still holds several "chips" that tech giants covet.

First is Braintree, processing about $700 billion in payments annually, valued by Bernstein at $10 to $15 billion. If acquired, Stripe's total payment volume would jump to $2.1 trillion, widening the gap in competition with rivals like Adyen.

Second is Venmo, a P2P app with over 100 million monthly active users, valued at about $5 billion. For Stripe, which has long "stayed behind the scenes," this is a valuable consumer touchpoint: a form of "last-mile visibility."

Third is a global network沉淀 (precipitated) over nearly three decades: clearing infrastructure deeply embedded in cross-border trade across more than 200 countries, and 438 million active accounts with real card bindings and credit history. Although it appears old, it is the most stable bridge to the global commercial periphery. PayPal recently launched the PayPal World plan, potentially reaching over 2 billion users through partnerships with Tenpay, UPI, etc. This "interoperability" connecting Eastern and Western payment systems is precisely the strategic entry ticket that is difficult for any competitor to replicate.

Nearly three decades of accumulation have not been in vain. It's just a pity that the one who best knows how to use this ticket may no longer be PayPal itself.

Stablecoins Become the Hidden Main Line

However, a word repeatedly mentioned by Wall Street analysts reveals the deeper ambition of this deal: stablecoins.

"A combined Stripe and PayPal could become a significant player in the stablecoin space, as stablecoins are increasingly becoming a more critical part of global commerce," Mizuho analyst Dan Dolev said bluntly.

Looking at the actions of both companies over the past two years, it's not hard to see that cryptocurrency—especially stablecoins—has become a future they are both betting on. But their strategic paths are截然不同 (distinctly different).

PayPal has chosen a path of "controlling the network with a coin," its underlying logic继承 (inheriting) and延续 (continuing) the centralized thinking of the SWIFT era. PayPal crafted PYUSD as a carefully designed "digital dollar." When ordinary consumers see PYUSD in their PayPal wallet, they don't need to understand whether it's a digital currency or fiat, nor whether the underlying settlement is blockchain or the traditional banking system. The familiar UI interface makes the digital currency just another foreign currency type. PayPal aims to extend the advantages of its payment network to the on-chain world, thereby building a closed-loop ecosystem centered on PYUSD. In April this year, it even launched a "PYUSD Hold Rewards Program," offering users a 3.7% annualized yield, hoping to drive growth in cross-border payment business through stablecoin transaction volume.

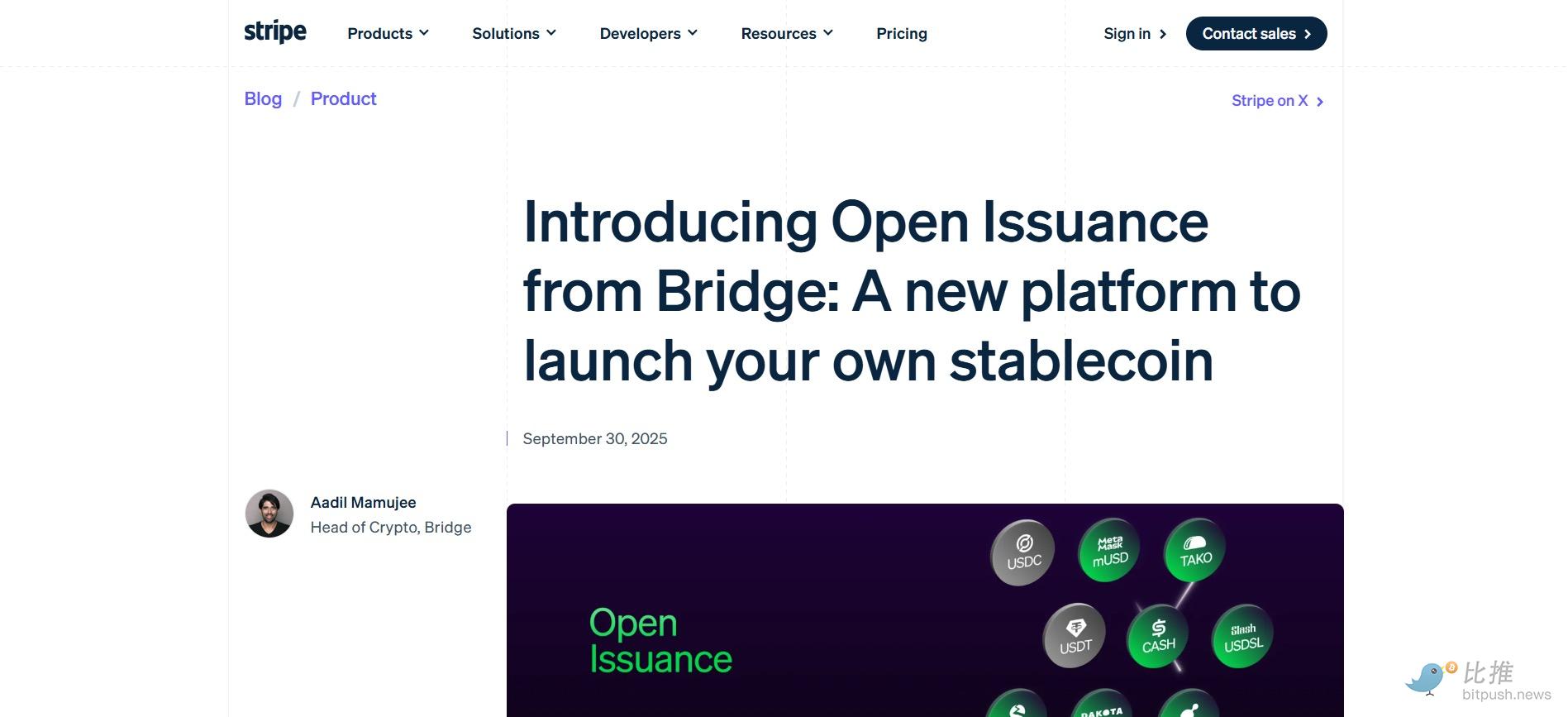

Stripe's layout is more systematic. In 2024, it acquired stablecoin infrastructure company Bridge for $1.1 billion, its largest acquisition to date. But the true ambition only became fully apparent with the launch of its "Open Issuance" platform—it is not fully betting on issuing its own stablecoin but is striving to become the "arsenal" in the stablecoin payment field, empowering other enterprises to issue, manage, and use stablecoins by building powerful infrastructure and developer tools.

The core of "Open Issuance" is that every enterprise can issue its own stablecoin through Stripe and enjoy reserve interest income. This "issuance as a service" model cleverly shifts value capture: while other traditional stablecoin issuers are still calculating basis point spreads, Stripe abandons reliance on reserve interest and instead builds a new profit model based on service fees. It shifts the value focus from "issuance" to "distribution."

The most critical piece is Tempo. Stripe is building this Layer 1 public chain focused on payments in partnership with Paradigm, targeting traditional clearing networks like SWIFT. Overlaying these two strategic maps, the logic behind Stripe's potential acquisition of PayPal becomes clearer: Stripe has the future-facing on-chain payment infrastructure (Tempo, Open Issuance), while PayPal has a ready-made user network (400 million accounts) and a market-tested stablecoin product (PYUSD).

If PYUSD is connected to the Tempo chain, leveraging its sub-second confirmation and low-cost features, and then reaching hundreds of millions of consumers through Venmo, a "Web3 payment closed loop"游离 (operating) outside the traditional banking clearing system would become a reality for the first time. This is not just complementary at the product level but a dimensional reduction strike on the existing global financial infrastructure.

An even more imaginative scenario is AI Agent payments. Unlike the traditional banking system, an AI Agent can have its own crypto wallet address, through which it can receive, store, and send funds. This makes automatic清算 (clearing) between AIs very convenient and efficient, especially suitable for micro-payment scenarios that are small in amount and have transaction context. The x402 payment protocol launched by Stripe this year is paving the way for this future—allowing developers to conduct automatic machine-to-machine settlements via the Base chain using USDC, expanding the payment scenario from "person-to-person" to "machine-to-machine." And PayPal's 400 million accounts are恰好 (precisely) the ideal "withdrawal exit" for these AI Agents.

Regulatory and Integration Challenges

Of course, the final落地 (landing) of this deal still faces huge uncertainties. Insiders emphasized that discussions are still in the early stages, and whether an agreement can be reached is still unknown.

Regulation is the sword of Damocles hanging overhead. The combination of two payment giants (combined TPV nearly $3.7 trillion) will inevitably attract high attention from antitrust agencies. Raymond James analysts believe potential acquirers could include large tech companies like Alphabet, Meta, Microsoft, Amazon, and Apple, but the feasibility of a deal is questionable given the limited financial information available for the private company Stripe.

Furthermore, the difficulty of cultural integration should not be underestimated. Stripe is known for its geek culture and developer-friendly approach, with co-founder John Collison recently stating the company is "in no rush to go public"; while PayPal is a publicly listed company with 400 million C-end users. How to reconcile these two截然不同 (distinctly different) genes will be a challenge the Collison brothers must face.

Even so, the rumor itself is symbolic enough. It marks that the global payment industry is undergoing a profound revaluation: the scale of the old era is no longer a moat, and the infrastructure capability面向未来 (facing the future) is becoming the key weight determining discourse power.

For Stripe, if the acquisition of PayPal succeeds, it will be an intergenerational "snake swallowing an elephant"; if it fails, at least the market has seen its ambition: it not only wants to become the payment base of the internet but also wants to become the rule-maker of the next generation of the financial world.

Author: Coconut Shell

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush