Author: Suvashree Ghosh, Bloomberg

Compiled by: Saoirse, Foresight News

Editor's Note: Recently, the global cryptocurrency market has continued to slump, and China has once again tightened regulations on cryptocurrencies and stablecoins, explicitly prohibiting the issuance of RMB-pegged stablecoins overseas without approval, directly impacting the progress of Hong Kong's digital asset hub construction. This article focuses on the market reaction and industry impact after the policy implementation, revealing the core contradiction between capital controls and crypto innovation. Against the backdrop of intensified industry reshuffling and accelerated capital withdrawal, the crypto sector is returning to pragmatic development. The regulatory boundaries and future direction are worth continuous attention.

November 26, 2025, a cryptocurrency exchange storefront in Hong Kong. Photo: Lam Yik/Bloomberg

Setback in the Digital Realm

Last year, an increasing number of crypto industry commentators believed that China's stance on the digital asset sector might be softening.

After People's Bank of China Governor Pan Gongsheng proposed the vision that the RMB has the potential to challenge the dominance of the US dollar, market talk of a "policy thaw" kept emerging.

But on February 7th, all these expectations came to an abrupt halt.

Amid the latest round of cryptocurrency crash, China tightened regulations on cryptocurrencies and the tokenization of physical assets, prohibiting domestic institutions from issuing digital tokens overseas and banning the issuance of RMB-pegged stablecoins abroad without approval. Officials stated this move was to prevent monetary sovereignty risks.

Angela Ang, Head of APAC Policy and Strategic Partnerships at blockchain intelligence firm TRM Labs, said: "China's attitude towards stablecoins has been tentative at best and has cooled significantly in recent months."

She stated that the central bank's latest announcement "completely dashes any hope for the launch of an offshore RMB stablecoin in the short term — certainly not in Hong Kong, and most likely not elsewhere either."

For Hong Kong and its years-long goal of building a digital asset hub, this is a major setback.

In June last year, Hong Kong's Secretary for Financial Services and the Treasury, Christopher Hui, had said that, subject to regulatory requirements, the possibility of pegging Hong Kong stablecoins to the RMB was not ruled out. It is now widely believed that he will shut this door completely.

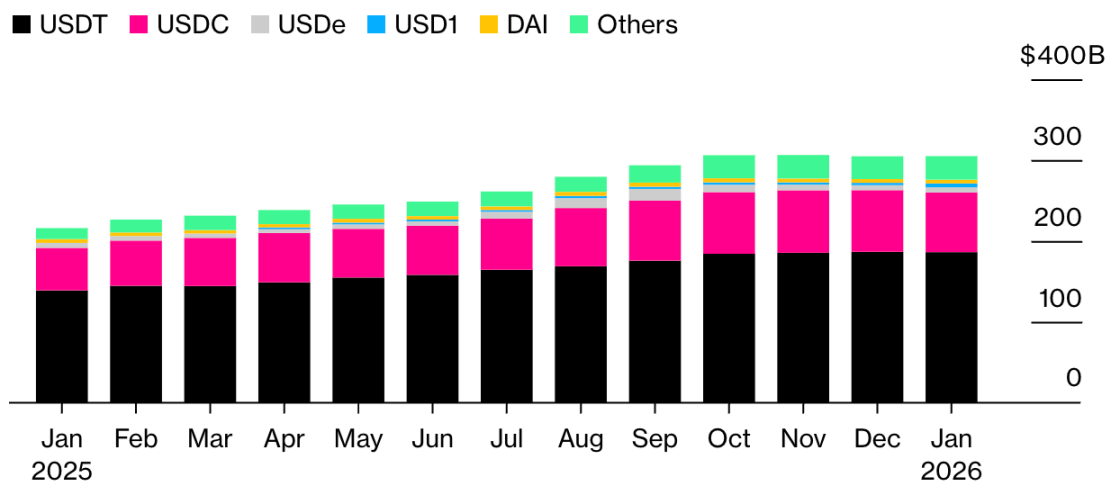

Surge in USD Stablecoin Supply During Trump Administration

Source: Artemis Analytics

As Angela Ang mentioned, signals of this regulatory tightening had already emerged.

As early as last August, China had required local securities firms and related institutions to stop publishing stablecoin research reports and hosting related promotional seminars to curb overheated market sentiment.

Patrick Tan, General Counsel at blockchain intelligence firm ChainArgos, said last week's policy announcement "removes the uncertainty hanging over the market regarding the private issuance of RMB stablecoins. Issuers now know exactly where the red lines are."

Entities applying for licenses can only focus on issuing stablecoins pegged to the Hong Kong dollar.

Bloomberg News previously reported that up to 50 companies in Hong Kong planned to apply for stablecoin licenses last year, including tech giants Ant Group and JD.com. But according to an October report by the Financial Times, these companies were forced to suspend their stablecoin plans after intervention from Beijing.

Ant Group and JD.com did not respond to requests for comment.

As of this Tuesday, Hong Kong had issued licenses to 11 cryptocurrency exchanges, while approving 62 companies to conduct digital asset trading for clients. The list includes China-backed institutions such as CMB International Securities Limited, Guotai Junan Securities (Hong Kong) Limited, and Tinful Futures Limited.

But industry players worry that without access to the RMB, the entire setup might be in vain.

"The issue was never about Hong Kong's regulatory framework, but always about whether China would tolerate RMB-denominated instruments circulating outside its control," Patrick Tan said, adding, "Capital controls and stablecoin liberalization are fundamentally incompatible."

Market Data Continues to Weaken

Bitcoin Perpetual Futures Open Interest Continues to Decline

Source: Coinglass

Bitcoin perpetual futures open interest has failed to rebound since starting to decline last October, highlighting the lack of confidence supporting this rally. Data from Coinglass shows it has fallen by about 50% from the October high.

Capital Outflow: $3.3 Billion

Data compiled by Bloomberg Intelligence shows that investors have withdrawn approximately $3.3 billion from US Ethereum ETFs since the crash in early October, with over $500 million withdrawn this year. Data shows that Ethereum ETF assets have fallen below $13 billion, the lowest level since last July.

Industry Perspectives

"The market is consolidating around what actually works. Even well-funded crypto-native VCs are pivoting heavily into fintech, stablecoin businesses, and prediction markets; it's hard to get attention for anything else."

— Santiago Roel Santos, Founder and CEO of crypto private equity firm Inversion

Venture capital funds in the crypto industry are shifting their focus to better-performing areas, such as stablecoin infrastructure, on-chain prediction markets, and expanding into related adjacent fields.

Twitter:https://twitter.com/BitpushNewsCN

BitPush TG Discussion Group:https://t.me/BitPushCommunity

BitPush TG Subscription: https://t.me/bitpush