Original | Odaily Planet Daily (@OdailyChina)

Author | Golem (@web 3_golem)

"xxx has sent you a cash red envelope!"

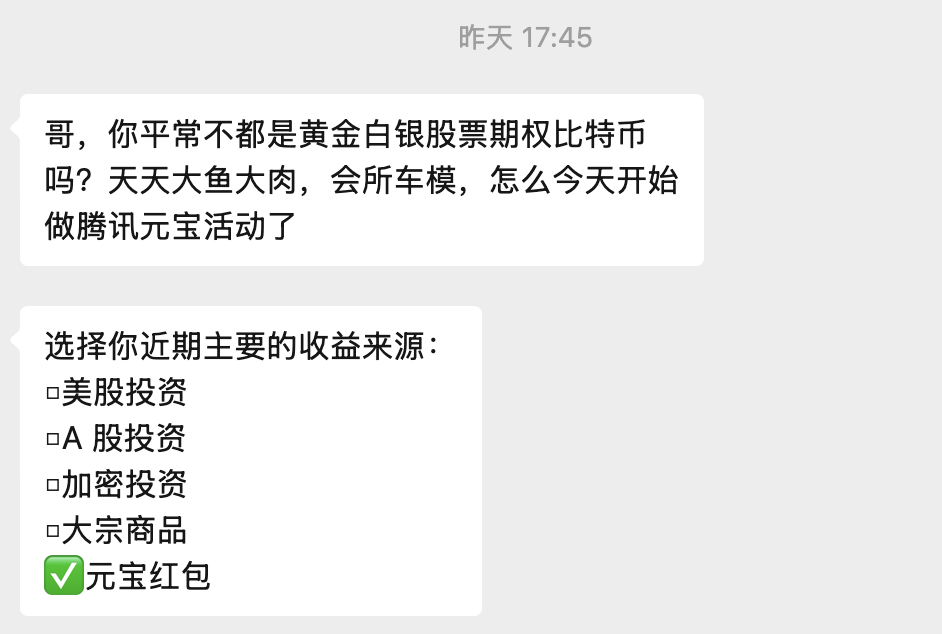

After Yuanbao's cash red envelope campaign began on February 1st, many long-dead project/research exchange groups have completely turned into "Yuanbao羊毛 (薅羊毛, meaning 'to grab benefits')" mutual assistance groups.

Transitioning from esteemed crypto traders to羊毛党 (those who seek small benefits) grabbing Yuanbao red envelopes is also a helpless move for people in the crypto circle.

Starting January 31st, global financial markets plummeted. Previously surging precious metals crashed rapidly, with spot silver nearly erasing its yearly gains, and spot gold once falling below $4500. The crypto market didn't fare much better. On February 2nd, Bitcoin broke below the $75,000 support level, hitting a low of $74,604. ETH dropped to a low of $2157.14, and SOL even fell below $100, touching a low of $95.95.

According to Coinglass data, the crypto market saw a total liquidation of $2.5615 billion on January 31st, setting a record for the highest single-day liquidation since the "10.11 crash." Thus, "too亏损 (loss) to speak" became the true psychological state of many in the crypto circle (like the silent Yi Lihua).

For crypto enthusiasts who just experienced a bloodbath, grabbing Yuanbao red envelopes, though a drop in the bucket for recouping losses, offers some psychological comfort and a temporary escape from the harsh market reality.

Jokes in group chats

Crypto Airdrops: From Swallowing Losses to Passionate Rights Protection

Calling Yuanbao's cash red envelopes the biggest airdrop for crypto people today is not just a gimmick.

The amount of cash red envelopes Yuanbao can distribute to each user isn't large, mostly ranging from a dozen to a few dozen RMB, but its value lies in its simplicity and truly zero cost. Users only need to spend a little time recruiting people and systematically experiencing product features to get cash red envelopes. The task cycle is short, allowing for quick returns.

In contrast, airdrops from crypto projects are first distributed in token form. Profit is only realized after the tokens are sold. Although the nominal amount received is often much larger than Yuanbao's, after deducting the costs of time, research, opportunity, wear and tear, and potential risk of being stuck with worthless tokens, how much is really left?

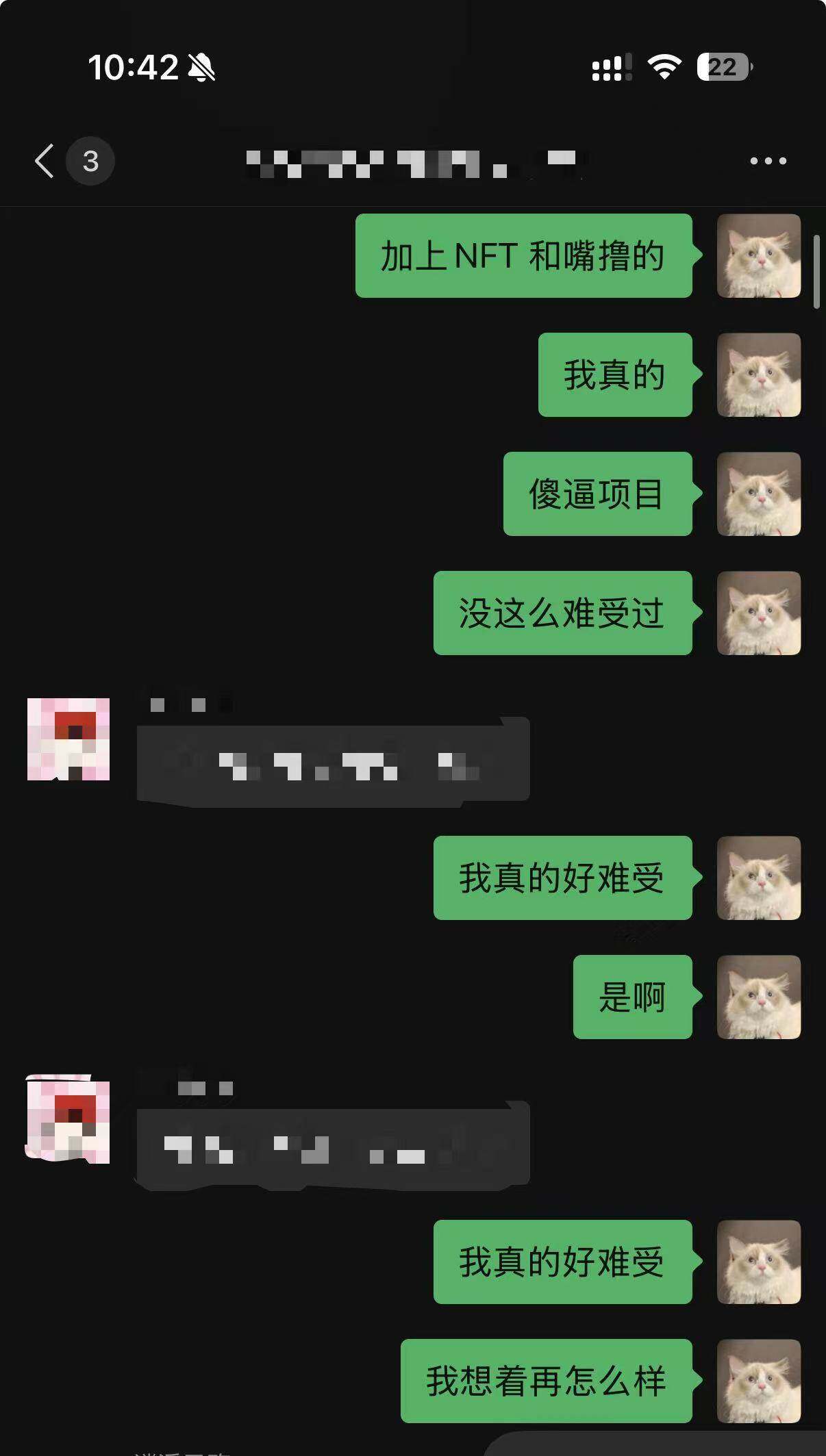

A user who accompanied Infinex for 406 days deeply feels this. On January 31st, the decentralized perpetual contract trading platform Infinex announced its TGE (Token Generation Event) and airdrop claims. The project team successfully landed, but the community was collectively反撸 (fǎn lū, meaning 'reverse-screwed' or 'exploited instead').

一千万是只猫 (X: @RXu107) is a typical example of being反撸. On February 1st, he posted that he spent over $11,900 (approximately 82,000 RMB) participating in this project (4400 U for NFT, 7500 U for public sale) and deeply accompanied it for 406 days as a community member. But by TGE day, not only had he not recovered his costs, but his paper loss also exceeded 100,000 RMB (2900 U + 11,284 locked INX tokens).

Faced with this反撸, the blogger had no choice but to repeatedly express his distress to friends.

The exploited blogger expresses distress to a friend about Infinex

At TGE, Infinex's fully diluted valuation was only $150 million. The total investment for Yuanbao's New Year red envelope event is approximately $140 million USD. What does this mean? It's equivalent to Tencent directly buying Infinex at its maximum valuation and giving it away for free to the whole nation.

Faced with the pain of being反撸 and deceived, most people in the community choose the same approach as "一千万是只猫"—swallowing the loss silently. But some choose to stand up and confront the project team.

Crypto blogger Ice Frog (X: @Ice_Frog666666) is a typical representative. He started by撸毛 (lū máo, 'wool hunting' or airdrop farming), but ironically, in 2025, Ice Frog was either engaged in airdrop rights protection or on his way to do so. He is still negotiating with the prediction market project Space (Odaily Note: Space raised $20 million publicly, the team privately took $13 million) and has even taken legal measures.

Web2 Can Afford Airdrops, Web3 Can't Fulfill Promises

The most ironic point is that today's imbalance between "input and return" in crypto airdrops is not due to the "moral bankruptcy" of a single project, but the result of a整套 (zhěng tào, 'complete set') of structural changes in the industry.

In 2020, Uniswap opened the era of crypto project airdrops. Since then, there have been constant major airdrops (大毛, dà máo) in the crypto space. Stories of getting a car from an airdrop, swapping an airdrop for a house, or reaching A8 (a net worth of 10 million) through airdrops attracted batch after batch of people into the撸毛赛道 (lū máo sài dào, 'wool hunting track'), presenting an aesthetic of "the industry is on the rise."

But by 2025, this changed. Market narratives dried up, primary financing weakened, secondary buying power was insufficient. Airdrops were no longer about sharing the future with early users, but more like mortgaging the future for present data, creating an exit path for the project team itself or securing the next round of financing. Thus, major airdrops disappeared, small airdrops shrank, and "being反撸" became the industry norm.

So-called airdrops are essentially rewriting advertising budgets into reward pools, bypassing third parties to directly establish growth relationships with users. Whether it's the 1 billion RMB from Web2's Yuanbao or the fixed airdrop allocation in Web3 project tokenomics, the essence is this same logic.

The difference is that Web2 giants use cash to buy user certainty, while Web3 offers token returns as a promise that might be fulfilled. This results in the same tactic leading to two different destinies.

The certainty of Yuanbao's cash red envelopes comes from cash flow and约束机制 (yuēshù jīzhì, 'binding mechanisms'). Tencent's strong cash flow ensures Yuanbao "can pay," and the binding mechanisms under mature laws ensure Yuanbao "cannot renege." Coupled with the "brain-dead simple" zero-threshold interaction, users naturally perceive it as a "welfare benefit."

In contrast, crypto participants not only incur costs several times higher than Web2羊毛党 (time, funds, energy) but also worry about being sybil attacked, token lock-up periods, and ever-changing airdrop rules. The most ironic part is that the returns from all this effort might ultimately be less than from Yuanbao.

Therefore, airdrops in the crypto space today have long degenerated from direct growth rewards into promises with constantly deferred fulfillment responsibilities, or even unfulfilled promises. If this situation does not change in 2026, user retention will be sacrificed along with it.

From User Growth to Retention, Airdrop Utility Can Only Last the First Half

Using airdrops for user growth has always been the most common and direct method in the business world to compete against powerful rivals.

Tencent invested 1 billion RMB cash to support Yuanbao because its competitor Doubao is strong enough—by the end of 2025, Doubao was the first AI product in China to reach 100 million daily active users. The same goes for Web3. In the prediction market赛道 (sài dào, 'track' or 'sector'), Polymarket dominates. To grab users, Opinion, predict.fun, and Limitless also use points airdrops for user growth, directly pulling users into their products.

In the short term, airdrops can indeed create a huge user influx entry point. But in the long run, what determines user retention is still product-market fit, user experience, and ecological linkages. In Web3's business history, there are no shortage of project cases that were bustling before the airdrop but deserted afterward. Therefore, both Web2 and Web3 face the same "post-airdrop problem": how to retain users.

Ten years ago, Tencent, a company adept at imitating and then surpassing, used "WeChat Red Packets" to push WeChat Pay into a national-level入口 (rùkǒu, 'entry point'), proving its familiarity with the "user growth → retention → habit" chain. Whether they can create another miracle for Yuanbao in the same way is still debated, but they at least have ample experience in "how to convert airdrops into retention."

To this end, Odaily Planet Daily contacted an internal Yuanbao staff member and asked, from a product perspective, how Web3 project airdrops should be improved. The answer was very practical:

"As one of the internet companies with the largest market cap, Tencent's experience might not be directly applicable to Web3 projects. But the core of user growth methods like airdrops is still improving retention. This requires a series of post-airdrop linkages. For example, PR and marketing need to think about how to further spread the玩法 (wán fǎ, 'gameplay' or 'mechanics'), and the product side also needs to take more actions to achieve this."

From the perspective of Web3 practitioners, merely discussing traffic tactics feels shallow. What product features, beyond the token, can truly retain users is worth more scrutiny.