June 3, 2026, Marvell Technology $MRVL's stock price touched $290, a new all-time high.

It's up 254% over the past 12 months, and was less than $40 just three years ago.

If you go back to when Matt Murphy became CEO in 2016—when the stock was under $10 and its market cap was less than $2 billion—that's a 30x gain.

But the magnitude of the increase is certainly not what this article aims to discuss.

What this article truly wants to understand is: What exactly is the market pricing into Marvell? Behind this price, are people still using an outdated framework to understand this company?

Many on the Street call Marvell the "small Broadcom"—the #2 in custom AI chips, picking up the hyperscaler scraps behind Broadcom. This isn't entirely wrong, but it has a fatal blind spot: It assumes Marvell is a smaller version of Broadcom. But the part of Marvell that is truly valuable is precisely the part that is completely different from Broadcom.

Marvell occupies a unique niche. AI infrastructure is shifting from "stacking GPUs" to "building systems," and this position will become increasingly valuable.

This article will try to explain this clearly.

The full article is approximately 15,000 words. Please read slowly~

I. What Does Marvell Actually Sell?

To understand Marvell, the first step is to throw away the label "chip company." It doesn't make GPUs, doesn't build CPUs, doesn't sell memory. It sells "connectivity"—making data flow at the speed of light between AI chips, between servers, and between data centers.

Breaking it down, three businesses:

First: Optical Interconnect — The Moat

Marvell is the absolute leader in high-speed optical DSPs. Roughly 70% of the DSP chips in global 400G+ data center optical modules come from Marvell.

Every time you see news about "surges in AI data center optical module shipments," Marvell is quietly collecting money in the background.

Why is 70% share hard to challenge? A high-speed optical DSP isn't an ordinary chip. It has to handle signal modulation, demodulation, error correction, and clock recovery simultaneously. At rates like 800G and 1.6T, managing signal attenuation and noise at the physical layer is insanely complex.

After the roughly $10 billion acquisition of Inphi in 2021, Marvell has accumulated over five years of mass production experience in this field, iterating from 5nm to 3nm. Broadcom is chasing too, but this first-mover advantage isn't something money can easily erase.

In March 2026, Marvell launched four 1.6T DSPs at once—Ara T, Ara X, Petra, Aquila M—covering everything from short-reach to long-reach, Ethernet to InfiniBand. Murphy said something very honest on the FY2027 Q1 earnings call: the growth expectation for the optical interconnect business in FY2027 was raised from 50% to 70%+.

It's not that the market changed; it's that they themselves underestimated how strong the demand would be.

Second: Custom AI Chips — The Growth

This is the part the market watches most closely. The logic is simple: Amazon doesn't want to pay a GPU tax to Nvidia for every chip, so it designed its own AI training chip called Trainium. But Amazon doesn't manufacture chips—it needs someone to help with design and production. That someone is Marvell.

Currently, Marvell has 18 custom XPU design projects, covering three hyperscalers—Amazon, Microsoft, Google. The lifetime revenue funnel is $75 billion. FY2026 full-year custom chip revenue was about $1.5 billion, expected to more than double by FY2028.

But there's an uncomfortable aspect to this business: gross margins are lower than for standard products. FY2027 Q1 non-GAAP gross margin was 58.9%, while Broadcom's was 77.5%. The reason is straightforward—you're working for Amazon, not selling your own standard products; R&D investment is heavy, and customer bargaining power is strong.

We'll expand on this later.

Third: Switch Chips & Enterprise Storage — The Cash Cow

Ethernet switch chip revenue is expected to exceed $600 million in FY2027 (doubling year-over-year), benefiting from the rigid demand for high-speed switching as AI clusters scale from hundreds of GPUs to over 100,000. Enterprise SSD and HDD controllers are the legacy businesses, contributing stable cash flow, but their share is shrinking year by year under pressure from the AI business.

Putting these three pieces together, the picture becomes clear: Marvell isn't a "chip company that does everything," but a company built around "AI data movement" with full-stack connectivity capabilities. From SerDes inside chips, to PCIe/CXL switching between chips, to optical DSPs between racks, to coherent optical modules between data centers—it has a hand in every link.

Understanding this explains why Nvidia invested $2 billion in it. It also helps gradually understand why calling Marvell the "small Broadcom" is a misreading.

II. In the AI Era, "Connectivity" Becomes the Star

Over the past two years, the spotlight has been entirely on GPUs. Compute is muscle, the bigger the better. But when AI clusters scale from thousands of GPUs to 100,000, 500,000, a problem at the level of physical law emerges: copper cables can only transmit about 3 meters; beyond that distance, signal attenuation makes them unusable.

A GPU can be the world's most powerful brain, but if the signal transmission between neurons can't keep up, even the highest IQ is useless. In a 100,000-GPU cluster, each GPU might spend 30%-50% of its runtime "waiting for data."

This is why optical interconnect takes center stage. Light can travel hundreds of meters or even kilometers with almost no attenuation. The larger the cluster and the more GPUs, the higher the proportion of optical connectivity—not linearly, but super-linearly.

Barclays estimates that optical port shipments will double in 2026 and double again in 2027. Marvell's optical interconnect business is expected to grow about 90% year-over-year this year and next—wait, now raised to 70%+, but based on actual numbers, even 90% might be conservative.

Key point: This trend isn't a one- or two-year story. As long as AI model parameters continue to expand and training/inference clusters continue to grow, the demand curve for optical interconnect won't flatten.

This isn't a cyclical issue; it's a long-term structural trend dictated by physical laws.

An analogy: AI infrastructure is a city undergoing crazy expansion. GPUs are the buildings themselves. Marvell sells the plumbing, wiring, and highways. Different architects can build the houses, but once the infrastructure is laid, it's much harder to replace than building houses.

III. From $10 to $290: An Underestimated CEO

In 2016, Marvell was a stock the market had given up on.

Founders Sehat Sutardja and Weili Dai were forced to step down due to accounting investigations and governance crises, with the SEC involved. The business was spread too thin—mobile communications, printers, consumer electronics—but none was a top-three player. The stock was under $10, and customers started worrying if the company would survive.

That year, activist hedge fund Starboard Value stepped in, orchestrating a textbook management reshuffle. They brought in Matt Murphy from Maxim Integrated as CEO.

I personally think Murphy deserves more mention: He spent 22 years at Maxim, rising from a frontline sales role to Executive Vice President, overseeing company-wide product development, sales, and P&L. He's not the "technical genius" type of semiconductor CEO—he's the extremely pragmatic, extremely focused businessman type.

One thing he said stuck with me: "My dad was on Apple's first sales team. I learned from a young age—no matter how good the technology, if you can't sell it, it's zero."

After taking over, Murphy did three things that sound simple but are extremely hard to execute:

First, Cut.

Cut mobile communications. Cut printer chips. Cut consumer electronics. Sold the Wi-Fi/Bluetooth business for $1.76 billion to NXP (2019). Sold automotive Ethernet for $2.5 billion to Infineon (2025).

All resources focused on one direction: Data Center Infrastructure.

Second, Buy.

2018: $6 billion for Cavium (ARM server CPUs, DPUs). 2021: $10 billion for Inphi, the optical DSP—this deal changed Marvell's fate. Late 2025: $3.25 billion for Celestial AI (silicon photonics/photonic fabric). Early 2026: $540 million for XConn (PCIe/CXL switching).

Four acquisitions, each filling a piece of the "AI connectivity" puzzle.

Third, Lock.

Murphy pursued something called "long-term visibility"—multi-year predictable revenue certainty. Signed a five-plus-year master agreement with AWS covering custom AI chips, optical DSPs, AEC DSPs, PCIe retimers, DCI optical modules, and Ethernet switches—not a single deal, but a comprehensive system-level partnership.

The 10-K discloses some capacity reservation agreements lasting 4 to 10 years.

The result? Upon taking over, FY2016 revenue was about $2.65 billion (FY2017 reported $2.32 billion), with meager profits. FY2026 revenue was $8.2 billion (+42% YoY), non-GAAP EPS $2.84 (+81% YoY).

A decade: A second-tier chipmaker crawling out of a governance crisis transformed into a core supplier of AI infrastructure.

In investing, there's a rule I've repeatedly validated: "Change CEO → Strategic Focus → Major Acquisitions → Lock-in Major Customers"—when this entire chain is executed successfully, and each step is evident in the financial numbers—such a company deserves serious research time.

IV. Nvidia's $2 Billion: Endorsement or Acquisition?

March 31, 2026, Nvidia announced a $2 billion strategic investment in Marvell—subscribing to 200 million convertible preferred shares, with an initial conversion price of approximately $91.84, representing about 2.4% ownership if fully converted.

Marvell jumped 13% that day. But the market's excitement at the time and what I later pondered repeatedly were not the same.

The market saw: Nvidia putting real money to stamp—"This guy is a partner I endorse." Not wrong logically. $2 billion isn't PR money; it's strategic investment. In 2026, Nvidia intensively invested in a string of optical interconnect companies—Coherent ($2B), Lumentum ($2B), Marvell ($2B)—$6 billion poured into the same field. This signal is louder than any analyst report.

But we should pay more attention to the collaboration framework—NVLink Fusion.

NVLink Fusion is an "infrastructure platform for semi-custom AI" pushed by Nvidia. Third-party vendors (like Marvell) can provide custom XPU accelerators directly connecting to Nvidia's high-speed interconnect network. Nvidia itself provides Vera CPUs, ConnectX NICs, BlueField DPUs, NVLink interconnects, and Spectrum-X switches.

Translating: "You hyperscalers want to use your own custom chips to replace GPUs? No problem, I'll use NVLink Fusion to plug your chips into my ecosystem too. You get someone else to make the chips, but the connectivity layer remains mine."

Just incredibly shrewd. Turns "enemies" into "customers"—the more hyperscalers try to escape Nvidia's GPUs, the more they need Nvidia's network. And Marvell happens to be the one helping hyperscalers build custom chips, while also helping Nvidia build the interconnect ecosystem.

The snipe and the clam grapple, the fisherman profits.

The Next Web had an analysis with a sharp but accurate title: "Nvidia's $2B investment in Marvell isn't an investment, it's a toll booth."

Through this investment, Nvidia sets up checkpoints at every entrance of the ecosystem. But from another angle—Marvell itself is part of the toll booth. Left hand helping cloud vendors build chips, right hand helping Nvidia build the network.

Both sides can't do without it; both sides are sending it money.

Of course, this also means an ever-present tension: Nvidia $NVDA is both partner and competitor. It makes its own networking chips, is also laying out silicon photonics; the line between cooperation and competition has always been blurry.

But my personal judgment is: At this "building systems" stage of AI infrastructure, Nvidia needs Marvell more than Marvell needs Nvidia. Because hyperscaler demand for custom chips is structural and irreversible. Nvidia refusing to cooperate would just hand the entire cake to Broadcom.

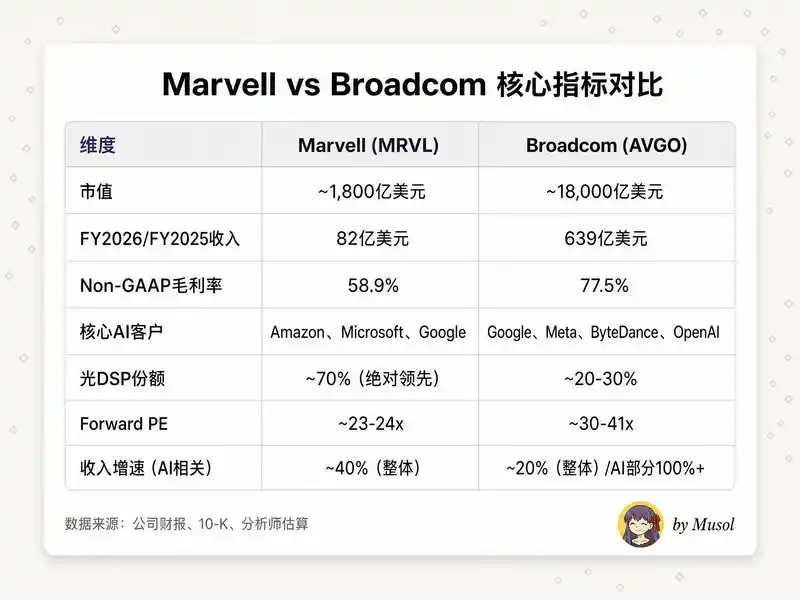

V. Compared to Broadcom, What's the Real Difference?

Many looking at this table quickly conclude: "Broadcom is better—ten times the size, twenty points higher margins, valuation not too much more expensive."

Not wrong, but it misses two most critical things.

First, the gross margin gap has structural reasons, not that "Marvell doesn't know how to make money."

Broadcom's 77.5% isn't pure semiconductor: includes VMware's software revenue, with EBITDA margins around 67%, severely boosting the consolidated gross margin.

Looking at the semiconductor part alone, it's roughly 60%-65%. Marvell's 58.9% is indeed lower, but the gap isn't as dramatic as it seems. And as Custom ASIC production scales up and R&D expenses amortize, there's a clear path for gross margin improvement—the company targets a mid-term non-GAAP operating margin of 38%.

Second, Marvell in optical DSPs isn't "#2," it's "#1."

70% market share; in this field, Broadcom is the one chasing. And optical DSPs happen to be the segment that benefits most as AI infrastructure shifts from "training-focused" to "inference-focused"—inference clusters are far more distributed than training clusters, requiring a higher density of optical interconnect.

Duan Yongping has a classification framework I've always found useful: "Type B businesses" are those you do better than others, but others also do them; "Type A businesses" are those where what you do, others simply can't do, or can't catch up even if they try. Marvell's optical DSP is closer to Type A; Custom ASICs are closer to Type B, but with extremely high customer lock-in and switching costs, the quality of this Type B business isn't low.

The market uses the "small Broadcom" framework to look at Marvell, naturally calculating "not worth $180 billion." But using the three-dimensional framework of "optical interconnect leader + custom chip #2 + Nvidia ecosystem partner," the valuation logic is different.

VI. Numbers Don't Lie

Financial data is the "sole standard" for testing any narrative. Look at Marvell's latest report and guidance:

Key numbers for FY2027 Q1:

· Quarterly revenue $2.418 billion, +28% YoY, +9% QoQ, a new high. Beat guidance midpoint by $18 million.

· Data center revenue $1.833 billion, 76% of total, +27% YoY, +11% QoQ.

· Non-GAAP EPS $0.80, in line with expectations. Operating cash flow $639 million—also a record high.

· Q2 guidance: Revenue approximately $2.7 billion (midpoint), +12% QoQ / +35% YoY. Data center expected mid-to-high teens sequential growth.

A few trends are very noteworthy:

Growth is accelerating.

FY2026 full-year +42%, FY2027 guidance +40%, FY2028 target +45%. Accelerating on an $8 billion base shows this isn't inventory restocking or a cyclical rebound—it's structural demand ramping up.

Operating leverage is emerging.

EPS growth (81%) far outpaced revenue growth (42%). Combined effects of custom chip scale, optical DSP production yield improvements, and Murphy's strict cost control.

There's a "hidden gold mine" in custom chips—attach. At the 2025 Custom AI Investor Event, the company disclosed an easily overlooked data point: By 2028, the TAM for custom XPUs is about $40.8 billion, while the TAM for attachments around the XPU (NICs, scale-up fabric, security co-processors, memory pooling chips, etc.) is about $14.6 billion—with the latter growing at a 90% CAGR. Many only watch "who designs the most expensive AI chip," but the real profits hide in the supporting roles.

Quick PEG calculation: Forward PE around 23-24x, revenue growth around 40%, PEG around 0.6.

Compare to Broadcom: Forward PE around 30-41x, revenue growth around 20%, PEG around 1.5-2.0. Using this simple lens, Marvell's current pricing isn't expensive. Of course, PEG is just a rough starting point—whether growth can be sustained, whether margins can improve, whether competition will intensify are the real variables.

VII. The Light Story: Celestial AI and the Next Chapter

Optical DSP is Marvell's present; Celestial AI is its future.

In December 2025, Marvell announced the $3.25 billion acquisition of Celestial AI—a startup working on "photonic fabric" technology. $3.25 billion is the upfront payment; if Celestial AI reaches cumulative revenue of $2 billion before FY2029, the total consideration could reach $5.5 billion.

Not cheap. Why was Murphy willing to pay?

Because Celestial AI addresses the next physical bottleneck in AI chip interconnection: copper cables have hit their limit.

Inside current AI servers, GPUs connect via NVLink—fast but short-range. An accelerator card with 8 GPUs, a rack with 4 cards, a cluster with hundreds of racks—the physical limit of copper becomes the entire system's bottleneck.

Celestial AI's Photonic Fabric uses light instead of electricity for direct chip-to-chip optical interconnect—16 Tbps bandwidth per chiplet, half the power consumption, nanosecond latency.

In plain terms: Optical DSPs are widening the data center's internal highways from two lanes to eight; Celestial AI is installing teleporters between every building.

There's another detail in this acquisition: Amazon supported the deal.

Marvell even issued a warrant to Amazon, allowing Amazon to purchase up to $90 million of Marvell stock based on Photonic Fabric product purchases. Amazon doesn't casually endorse a supplier's acquisition—it does so because it genuinely needs the technology.

Marvell expects Celestial AI to start contributing meaningful revenue in H2 FY2028, with run-rate revenue reaching $500 million by Q4 FY2028 and $1 billion by Q4 FY2029. If the roadmap delivers, the optical interconnect business transforms from "business #1" into a "super business"—a full-stack optical connectivity platform spanning DSPs, silicon photonics, and photonic fabric.

Adding the $540 million acquisition of XConn in early 2026, Marvell now holds a complete "electrical + optical" interconnect puzzle: SerDes inside chips → PCIe/CXL switching between chips → intra-rack optical interconnect → inter-rack optical DSPs → inter-data center coherent optical modules.

On the AI interconnect track, no other company has an equally complete layout.

VIII. After a 254% Rise, Of Course Don't Forget the Risks

In investment research, the most important thing isn't finding "why it will rise"—in a bull market, reasons are everywhere. The important thing is finding "what would make it fall," then judging if you're willing to bear it. I think the risk control philosophy of @aleabitoreddit is something everyone should study carefully.

Risk One: Losing Trainium3, Customer Concentration is Higher Than You Think

Marvell recently lost the main design rights for Amazon's next-generation Trainium3—snagged by Taiwan's Alchip. The company emphasizes that Trainium2.5 continues with Marvell, and "there won't be a revenue cliff."

But the market sees another side: the biggest custom chip client didn't choose its old partner for the next-gen product. This isn't a good signal.

In FY2026, the top ten customers contributed 82% of revenue, with two exceeding 10% each. The 10-K states frankly: "The current level of capital expenditure in AI infrastructure may not be sustainable long-term."

If Amazon or Microsoft—either one—scales back custom chip plans, Marvell's revenue would take a direct hit.

Risk Two: Gross Margin Ceiling

Non-GAAP gross margin 58.9%, nearly 20 percentage points lower than Broadcom. This isn't temporary; it's structural. Custom ASIC is essentially a service business—helping clients design proprietary chips, clients own the final product; your pricing power is naturally limited.

Scale can improve it, but not fundamentally solve it.

If future revenue growth relies mainly on custom ASICs (lower margins) rather than optical DSPs (higher margins), a trade-off emerges between revenue growth and margin expansion. The market's valuation multiple might not be as generous as bulls expect.

Risk Three: Nvidia's "Toll Booth" Could Become "Toll Booth + Competitor"

Nvidia invested $2 billion, but is also building its own networking chip team. Spectrum-X switches, BlueField DPUs, NVLink interconnect—directly or potentially competing with Marvell's switch chips, custom ASICs. A 2.4% stake isn't control; it's ecosystem binding.

If Nvidia decides in the future to internalize more value-added parts of NVLink Fusion—like making more optical interconnect chips itself—Marvell's position could become awkward.

Risk Four: Insiders Are Selling

Since 2026, CEO Murphy has cumulatively sold about $5.3 million (three sales, prices from $98.70 to $177.26), CFO Willem Meintjes sold about $4.7 million, COO Chris Koopmans sold about $2.73 million, CDO Sandeep Bharathi sold about $13.14 million.

Not a single insider purchase.

The absolute amounts relative to holdings aren't huge (Murphy still holds about $131 million after sales), all executed via 10b5-1 pre-arranged plans.

But the signal is clear: Stock at an all-time high, the people who know the company best are selling, no one is buying.

At the very least, it should make you ask yourself one more time: Am I buying this stock because I understand its value, or because I see it's up 254%?

Risk Five: Supply Chain

The 10-K discloses the need to lock in capacity 26-52 weeks in advance, with some agreements spanning 4 to 10 years.

TSMC's 5nm/3nm capacity is fiercely competed for by GPU makers (like Nvidia, AMD); optical DSP lead times have already stretched to 6 months.

If Marvell misjudges demand—committing too much capacity only for demand to drop, or demand exceeds expectations but capacity is insufficient—the penalty hits the financials directly.

This AI infrastructure super-cycle doesn't just reward "those with the right technology," but also "those whose supply chains don't break."

After discussing all these risks, what's my conclusion?

These risks are real.

Losing Trainium3 isn't trivial; the structural gross margin issue won't be solved overnight; insider selling warrants caution. But I'm not siding with the bears on Marvell for three reasons:

First, the bad news of losing Trainium3 has been covered by the FY2028 custom chip revenue doubling guidance.

Losing the biggest client's next generation but still giving doubling guidance suggests the pipeline from other clients (Microsoft Maia, Google Axion, and that "undisclosed new hyperscaler") is stronger than the market thinks.

Second, the optical interconnect moat is real, and widening.

70% DSP share + Celestial AI silicon photonics + XConn PCIe/CXL switching = a full-stack capability no one can replicate in the short term.

Competitors might snatch one or two custom chip orders, but no one can catch up to Marvell's optical interconnect accumulation in three to five years.

Third, PEG of 0.6 provides some margin of safety.

40% revenue growth paired with a 23x forward PE—this pricing isn't "the market is already hyping it as the next Broadcom," but rather "the market is still debating if it deserves to be cheaper than Broadcom."

IX. Some Thoughts on the Era

Peter Thiel in "Zero to One" offers an uncomfortable argument for many entrepreneurs: Competition is for losers; truly great companies create monopolies.

"All failed companies are the same—they failed to escape competition."

Applied to investing, this framework forces a sharp question: Is the company you're researching struggling in a highly competitive market, or occupying a monopolistic position in a market it defined itself?

The interesting thing about Marvell is it's doing both simultaneously.

In custom AI chips, it's Broadcom's follower—a "participant."

In optical interconnect and high-speed DSPs, it's the absolute market leader—a "monopolist."

Nvidia's $2 billion investment essentially confirms with real money Marvell's monopolistic value in the "connectivity" dimension.

Thiel says one characteristic of monopolies is that their market is smaller than it appears—"Monopolists usually disguise the extent of their monopoly to avoid attracting regulatory attention."

Marvell is precisely the opposite: Its monopolistic position is overlooked by the market because everyone is focused on its gap with Broadcom in custom chips.

A thought experiment: Marvell's current market cap is about $250 billion, corresponding to FY2027 revenue of about $11.5 billion, roughly a 21.7x Price-to-Sales ratio. But of that $11.5 billion, the data center portion is about $9.2 billion, growing at 50%+.

Valuing just this part using Broadcom's valuation multiples (around 25-30x P/S), it alone is worth $230-$276 billion.

The market's $250 billion valuation essentially discounts the data center business and throws in the other businesses for free.

Of course, this "sum-of-the-parts" valuation is overly simplistic—Marvell's data center business wouldn't truly command Broadcom's multiples, given different margin structures, higher customer concentration, and a weaker position in custom chips than Broadcom.

But it at least provides a starting point for thought: The market's pricing of Marvell likely still resides in the old narrative of "this is the company that lost Trainium3," not the new reality of "this is the only global company with scaled revenue simultaneously on three battlefields: optical DSPs, silicon photonics, and custom AI chips."

My judgment could also be wrong. Custom chip competition could be fiercer than I think, optical interconnect demand growth might not meet model forecasts, Celestial AI's $1 billion run-rate target might not be achieved.

But right now, I'm willing to bet on the "AI connectivity" direction. Not because Marvell is the best company, but because it's in the most correct position.

X. Epilogue: Light and Civilization

Writing here, I want to step out of the investment framework and say a few bigger things.

Every leap in human civilization, looking back, wasn't due to a single breakthrough point, but to an upgrade in "connection."

Writing allowed thoughts to traverse time, the printing press allowed knowledge to flow across social classes, the telegraph allowed information to cross oceans, the internet first connected all human brains into a network.

Each time, what truly changed the world wasn't the "content" itself, but the speed and breadth of its flow.

The AI era is replaying the same story.

We've focused too much attention on the "brain"—bigger models, stronger compute, smarter reasoning. But a brain never exists in isolation.

However intelligent a single person, if unable to communicate with others, they remain an island. The same goes for a 100,000-GPU cluster—if data cannot flow freely between them, even the strongest compute is just silent silicon.

Light is the messenger of this era.

From a physics perspective, light is the speed limit for information transmission in the universe. It took us millennia to learn to harness it—from beacon fires to fiber optics, from Morse code to 1.6T DSP signal processing. Now, as humanity attempts for the first time to build a true "silicon-based brain," we return to the same ancient question: How to let thought, whether carbon-based or silicon-based, flow at the speed of light?

On the surface, Marvell's story is a chip company's decade-long comeback. But thinking deeper, it touches a more fundamental proposition: In any complex system, the value of "connections" will ultimately surpass the value of "nodes."

In the internet era, the total value of routers and fiber optics eventually exceeded that of any single server.

In the social network era, the platform's value exceeded that of any single content creator.

In the AI era, the same logic is replaying—when everyone is vying for the crown of the "most powerful brain," the real winner might be the one quietly weaving the neural network.

We stand at a fascinating and delicate historical juncture. Humanity has, for the first time, the ability to build something smarter than itself, and whether this thing can truly become "intelligent" depends on solving a seemingly mundane engineering problem: letting light travel freely between chips.

That in itself carries a certain poetry.