Authors: Block Analytics Ltd, Merkle 3s Capital

An IPO Priced Half a Year Ahead

On June 12, SpaceX will list on Nasdaq with a valuation of $1.75 trillion, becoming the largest IPO in human capital market history. This figure exceeds Walmart, JPMorgan, and all traditional energy giants combined. A still-unprofitable aerospace company has an valuation that beats most of the S&P 500.

But what truly supports this $1.75 trillion valuation is not the Starship repeatedly exploding in Texas, but the over 8,000 little white dishes called Starlink in orbit. Rockets are just the entry ticket; satellite internet is the cash machine. This is the contrast the market has been digesting over the quarter since SpaceX's prospectus was filed.

More intriguing are the related concept stocks. From the prospectus leak on March 25th to now—TSLA +10%, RKLB +88%, FLY +70%, QCOM +56%, DXYZ +79%—a funding frenzy surrounding SpaceX has largely run its course. Are retail investors joining the party now, or are they buying into a top? Let's examine each company closely.

The Three Faces in the Prospectus

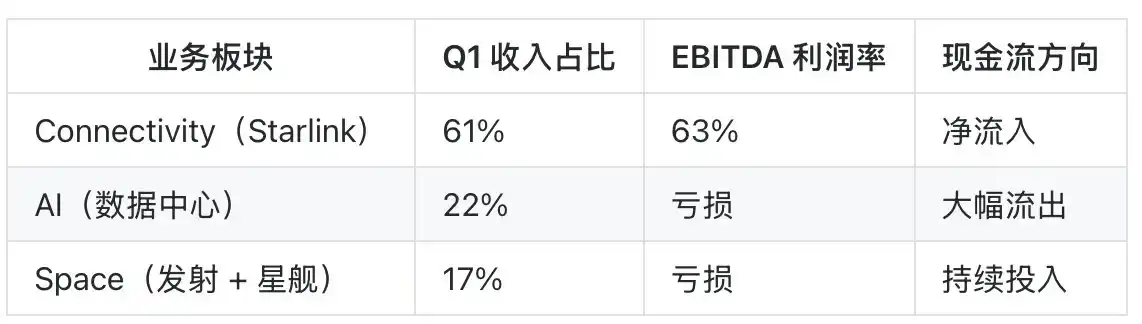

SpaceX has divided its business into three segments: Space (Launch & Starship), Connectivity (Starlink), and AI (Data Centers & Computing Power). It sounds balanced, but financially it's a severely skewed machine.

Starlink is the true cash cow. As of Q1 2026, paying users have exceeded 10.3 million, contributing 61% of the group's quarterly revenue, with an EBITDA margin as high as 63%. This is a figure higher than most SaaS companies. Once the satellite internet business crosses the critical point of scale, marginal costs are almost zero—SpaceX has already crossed that threshold.

The ARPU trend is another key aspect of this story. In 2023, Starlink's average monthly fee was in the $110-130 range. In 2024, it dropped to $90-100 as emerging markets gained traction. By H2 2025, due to the dilution from Direct to Cell entry-level plans and enterprise long-tail users, it has fallen to the $75-85 range. User numbers are doubling while revenue per user is halving—a classic "volume over price" story.

The benefit is that TAM is expanding—markets like India, Southeast Asia, and Africa, with low ARPU, weren't in Starlink's early business model. The downside is pressure on gross margins, as hardware subsidies are higher in low-end markets, and the payback period per user extends from 14 months to 22-28 months. We prefer to view Starlink as a "user growth over ARPU" story until at least 2027. Don't overreact to single-point ARPU declines in quarterly reports, but be wary of the potential risk of simultaneous slowdown in both user growth and ARPU.

The AI business is the other extreme. Q1 capital expenditure burned $7.7 billion, most of which went into the Phase 2 data center in Memphis, Texas. The monthly $1.25 billion compute contract with Anthropic sounds impressive, but the contract clearly states: 90-day unilateral termination right. This means the booked AI revenue could vanish at any time.

The Space segment continues to lose money due to Starship R&D. The logic of this business is: make rockets dirt cheap, then charge tolls via Starlink, and finally use AI data centers to consume all the compute power. All three puzzle pieces are essential, but only Starlink generates cash.

Regarding control, Musk holds 85.1% of the voting rights. This is an even more absolute control structure than Mark Zuckerberg had during Meta's early days, meaning the essence of retail buying is "faith." SpaceX's stated TAM in the prospectus is $28.5 trillion, broken down as: Satellite broadband $1.2T, Government/Defense launches $400B, AI compute $12T, Deep space & Lunar economy $9T, with the rest being industrial space. Most of these figures won't be verifiable until around 2040.

TSLA: The "Covert Protagonist" Mentioned 87 Times in the Prospectus

If you can only pick one SpaceX concept stock, the answer isn't a rocket company; it's Tesla.

The SpaceX prospectus mentions Tesla 87 times, far more than any other entity. The two companies share chip design teams, Dojo compute architecture, and capacity at the Texas Terafab chip factory. Musk's publicly announced "Galactic Heart" plan in early 2026 essentially connects SpaceX's compute power with Tesla's FSD training data pool—these aren't two separate companies; they are a tech empire deliberately split in two.

The capital market is already voting with its feet. From the prospectus filing on March 25th to now, TSLA is up 10.24%. This gain might seem less dazzling compared to many small-cap concept stocks, but consider that Tesla's market cap base is in the trillions—a 10% gain means adding an entire Ford Motor Company's worth of market value. What is the market betting on? That upon SpaceX's IPO, Tesla's indirect equity stake in SpaceX will be repriced.

A more aggressive bet is a merger. Expectations for a "merger of the two companies around 2027" do exist in the market, but its probability depends on tax structure and Musk's own patience with the Tesla board. We prefer to view TSLA as a "high-conviction side pocket" for the SpaceX IPO, rather than a "merger lottery ticket."

If you like SpaceX's AI compute story, Tesla's Dojo is the closest version you can buy directly in the secondary market. If you like SpaceX's cash flow story, Tesla is not the optimal choice—it doesn't have direct business links to Starlink.

Three Direct Competitors: RKLB, ASTS, FLY

The most awkward aspect of SpaceX's IPO isn't for SpaceX itself, but for these three companies. They benefit from "aerospace sector premium," yet must prove "they won't be eaten by SpaceX."

Rocket Lab (RKLB): Mini SpaceX, The Only Substitute

RKLB is the champion of this rally, up +88.85% since late March. The logic is simple: retail can't buy SpaceX, so buy the company that looks most like SpaceX. Rocket Lab's Electron small rocket has achieved commercial steady-state launches, and the Neutron medium-lift rocket under development targets Falcon 9, with first flight expected by end of 2026.

The Neutron timeline is the most sensitive variable for RKLB. In 2024, the company targeted end of 2025 for first flight, adjusted to Q1 2026 in mid-2025, and postponed again to Q4 2026 by end of 2025. The two postponements corresponded to 15-25% price corrections, indicating the market's intense focus on this milestone; any news about engine tests, integration rehearsals, or weather windows can trigger short-term volatility.

The Archimedes engine has completed long-duration firing tests. The second-stage recovery plan borrows from Falcon 9 but simplifies it, opting for more conservative parachute recovery instead of grid fins. If Neutron successfully launches in late 2026, RKLB will gain entry to compete for NASA's NSSL Phase 3 Lane 1 contracts, a five-year pool worth a cumulative ~$5 billion in government orders. Conversely, if the first flight slips to 2027, the entire valuation anchor loosens—the market's patience for a "substitute" play is limited.

However, RKLB's true moat isn't rockets; it's quietly becoming an "Aerospace IDM"—building its own rockets, satellite buses, providing launch services, and operating constellations. This vertical integration strategy mirrors SpaceX's path, and the market is willing to grant it a valuation premium.

The risks are also evident. If Neutron experiences delays or a failed first flight, the entire "substitute" narrative will be repriced by the market. And the SpaceX IPO itself is a valuation vacuum—when you can buy the real SpaceX, how much is the substitute worth?

AST SpaceMobile (ASTS): The AT&T of Space

ASTS takes a different path: direct-to-phone satellite connectivity. No special terminal needed; ordinary iPhones and Android phones can connect to space-based cell towers. The explosive point of this story is that it directly challenges the same TAM as Starlink Direct to Cell.

ASTS has signed partnerships with operators like AT&T, Verizon, Vodafone, and Rakuten. BlueWalker 3 in-orbit testing achieved speeds of 14 Mbps. However, its satellite deployment progress lags far behind Starlink's, requiring 18-30 more months for full constellation operation.

High volatility is the norm for ASTS—single-day moves of +/-10% are common. If your portfolio has low-risk tolerance, this stock is unsuitable as a core holding. But if you're betting on "operators not wanting Starlink to dominate," ASTS is the sharpest tool for that logic.

Firefly Aerospace (FLY): Underestimated Dark Horse

FLY is a severely undervalued player this round. Its +70.38% gain seems substantial, but its fundamental support might be even stronger than RKLB's. The Alpha rocket has completed multiple commercial launches, and the Blue Ghost lunar lander is a key contractor for NASA's Commercial Lunar Payload Services (CLPS).

FLY's core narrative is the "cislunar ecosystem chain"—full-stack capabilities from Low Earth Orbit to the lunar surface. As SpaceX's Starship turns the lunar economy from science fiction into reality, FLY is among the most direct beneficiaries. It lacks RKLB's brand recognition, but its ability to secure NASA contracts might be the strongest among these three.

The shared risk for all three: after SpaceX's IPO, "substitute capital" parked in them might flow out toward SpaceX itself. This is a classic "sell the news" risk, requiring position trimming ahead of the event, not chasing highs.

Partnership Ecosystem: SATS, PL, AMZN, TMUS, QCOM, FLYX

The SpaceX IPO is a "shot in the arm" for partners—proving the ecosystem itself can create market value, so all upstream and downstream players will be repriced.

EchoStar (SATS): The Spectrum Seller

SATS is one of the biggest winners in this ecosystem game. In late 2025, it sold its S-band and part of its AWS-4 spectrum to SpaceX for $8.5 billion in cash plus $8.5 billion in SpaceX stock. This deal transformed SATS overnight from a struggling satellite TV company into a significant shareholder of SpaceX.

SATS is up 23.81% since late March, seemingly modest, but this gain hasn't fully reflected the valuation release of the SpaceX stock portion post-IPO. If SpaceX's valuation holds at $1.75 trillion post-listing, the actual value of the $8.5 billion in stock consideration held by SATS would be significantly higher than book value.

Planet Labs (PL): The Most Loyal Passenger

PL is a frequent customer of SpaceX rideshare launches, with over 90% of its satellites launched via Falcon 9. It's up +30.76% since late March. The company itself is a leader in Earth observation, scanning the entire Earth's surface daily, selling data products to governments, agriculture, insurance, and hedge funds.

PL and SpaceX have a true symbiotic relationship. SpaceX's listing won't change PL's fundamentals, but it will prompt the market to re-evaluate the ceiling of the "Earth observation" sector. If you believe in the "data-as-an-asset" logic, PL is the cleanest play on that line.

Amazon (AMZN): The Dramatic Shift from Foe to Partner

Amazon's Kuiper constellation was originally Starlink's biggest potential challenger. But in H2 2025, AMZN surprisingly awarded some Kuiper satellite launch contracts to SpaceX—citing insufficient launch capacity from ULA and Blue Origin.

This is a classic case of business logic overriding corporate rivalry. For AMZN, SpaceX's listing means a comparable valuation benchmark now exists for the Kuiper project. The synergistic value of Amazon Web Services (AWS) + Kuiper might be rediscovered by the market. However, AMZN's size is too large; the SpaceX IPO is more of a "marginal positive" for it, not a core driver.

T-Mobile (TMUS): The Top Ally for Direct to Cell

TMUS is Starlink's exclusive US carrier partner for its direct-to-phone service. Starting in 2025, T-Mobile users could send/receive texts via Starlink satellites in areas with no signal, expanding to voice and data in 2026. This is a revolutionary story allowing carriers to bypass traditional cell tower builds.

TMUS's stock reaction has been relatively muted, but it's locked into a 10-year cooperation framework. If Starlink Direct to Cell user penetration exceeds expectations, TMUS is the most stable cash flow beneficiary on this line.

Qualcomm (QCOM): The Enabler in the Basement

QCOM is up 56.59%, surprising many. The logic lies in deep cooperation with SpaceX on Starlink's satellite baseband chips, Direct to Cell's handset-side modems, and some communication chips for SpaceX data centers.

QCOM is the most "foundational" pick-and-shovel seller in the SpaceX ecosystem. It doesn't bet on any single application, but can take a cut from each one that booms—a logic identical to its role in the smartphone era.

flyExclusive (FLYX): Starlink Aviation Dealer

FLYX is a private jet charter service and a core distributor for Starlink Aviation in the private aviation sector. The company is small, high-beta, but its story's ceiling is clear—the entire private aviation market is limited.

If you want leverage, FLYX provides it; if you want certainty, FLYX isn't the answer. This is a typical "small-cap beta" play.

Premium Access Channels: GOOGL, BAC, DXYZ, XOVR, VCX

This group's characteristic is "indirect holders of SpaceX equity." Pre-IPO, they were the only way for retail to get SpaceX exposure; post-IPO, the value of this channel will fundamentally change.

GOOGL & BAC: The Giants Riding Along

Google holds ~7% of SpaceX, a legacy from a 2015 investment round. At a $1.75T valuation, this stake's book value is ~$120B. For GOOGL, it's a "sleeping asset" that won't change fundamentals but will add a sizable revaluation to its financials.

BAC is a lead underwriter for the SpaceX IPO, with estimated underwriting fees of $500-800 million. For a bank of BAC's size, this won't move the valuation needle, but it will be the "star deal" of the quarter. Capital markets love star deals.

DXYZ, XOVR, VCX: The Last Window for Retail to Buy SpaceX

These three are essentially "closed-end funds packaging SpaceX equity." DXYZ is Destiny Tech100, XOVR is ERShares Private-Public Crossover ETF, and VCX is Vinia Capital. They all hold significant SpaceX shares via secondary markets or private placements.

Since late March, DXYZ is up 79.56%, with its market price premium to NAV once exceeding 200%. This is a very dangerous signal. This premium exists solely because "retail has no other way to buy SpaceX." When SpaceX itself lists and retail can buy the shares directly, there's no reason for this premium to exist.

History offers an identical playbook. GBTC maintained a persistent 30%+ premium before Bitcoin ETF approval in 2021, immediately switching to a 20%+ discount post-approval. DXYZ, XOVR, and VCX will likely replicate this process, and with a higher starting premium, the potential drop could be even sharper.

If you hold these funds now, seriously consider: are you profiting from SpaceX's valuation increase, or from the scarcity premium of "no retail access"? If it's the latter, June 12th is the day that scarcity goes to zero.

RDW Redwire: Another Play in the Aerospace Pick-and-Shovel Game

Redwire isn't on most media concept stock lists, but we believe it deserves its own chapter—because its investment logic differs from all the companies above.

Rocket companies earn transport fees, satellite companies earn bandwidth fees, while Redwire earns "parts fees for building satellites." Solar arrays, deployable structures, camera payloads, space 3D printing equipment—hardware components needed by all spacecraft. Redwire is a hidden champion in this niche market.

In late 2025, RDW acquired Edge Autonomy, a company specializing in military drones and military space payloads. This acquisition transformed Redwire from a purely commercial space company into a "dual-use" defense contractor. In the current US defense budget structure, dual-use companies receive significantly higher valuation multiples than pure commercial ones.

More interesting is the microgravity pharma line. Redwire's PIL-BOX microgravity cultivation device has completed multiple protein crystal growth experiments on the ISS. Certain drugs produced in microgravity have purity far exceeding ground-based production, an early-stage sector with a TAM potentially reaching hundreds of billions.

Specifically, PIL-BOX's current clientele includes top-tier pharma like Bristol Myers Squibb and Eli Lilly, focusing on optimizing crystal forms for monoclonal antibodies. Ground-based cultivation yields only one stable crystal form, while microgravity can screen multiple forms, corresponding to different drug solubility, stability, and half-life. The commercial value isn't "making drugs in space," but "using space data to guide ground-based processes"—a classic high-value-add data business, with single-experiment pricing in the $2-5 million range.

Further applications include stem cell culture and tissue engineering. 3D cell culture in microgravity avoids sedimentation issues present on Earth, theoretically enabling the creation of truly three-dimensional organoids. This route is still pre-clinical, with the first IND-enabling data unlikely before 2028. But if successful, Redwire wouldn't be held as an aerospace stock, but as a biotech stock—valuation logic completely different, with P/S multiples jumping from aerospace's 3-5x to biotech's 15-25x.

RDW's current undervaluation stems from three reasons: SPAC legacy stigma, continuous losses, and revenue scale appearing small compared to rocket companies. None of these affect its core asset quality, but they all affect retail attention.

Catalyst-wise, the Trump administration's proposed "Iron Dome" (Golden Dome) missile defense plan creates direct demand for Redwire's Very Low Earth Orbit satellites and Edge Autonomy's payloads. This is a government order pool potentially worth tens of billions.

The specific technical path for Iron Dome is still under evaluation, but the general direction is set: a multi-layered architecture of "low-orbit multi-layer detection + high-orbit warning + terminal interception," an upgraded version of Israel's Iron Dome combined with the US SDI legacy. Redwire's low-orbit satellite buses, Edge Autonomy's tactical drones & high-altitude payloads, and PIL-BOX's space materials & sensor experiments can all tap into different sub-contracts of Iron Dome. The rarity of a single small/mid-cap company possessing all three asset types is the most overlooked point in Redwire's valuation story.

Timeline-wise, the Pentagon plans to issue the first RFPs in H2 2026, begin large-scale procurement in 2027, and complete initial deployment by 2030. This means RDW's current low-valuation window might only last 12-18 months—once orders start landing, the market will quickly reclassify it from "commercial space stock" to "defense contractor stock," leading to a structural re-rating in valuation multiples, similar to Palantir's shift from tech to defense in 2023.

We won't claim Redwire will become the next RKLB, but its investment logic is the dual attribute of "infrastructure + pick-and-shovel seller," more robust than betting on a single rocket company's success. If your portfolio already has high-beta exposure to RKLB or ASTS, RDW is a reasonably priced hedging allocation.

Risks & Outlook: A Story Largely Priced In

After reviewing all 17 companies, return to the most basic question—is all this already priced in?

It's been over 60 days since the prospectus filing, and almost every concept stock has delivered double- or triple-digit gains. This means the market has already priced in most of the benefits from the SpaceX IPO. On June 12th, the actual listing day, what's more likely isn't another broad rally, but profit-taking on "news sell-off."

Historical patterns support this. From Alibaba to Facebook, from Saudi Aramco to Saudi Aramco (the largest IPO ever), all mega-IPOs exceeding $500B in market cap have underperformed the broader market in their first year post-listing. Liquidity siphoning is real; valuation anchoring is real.

SpaceX's own fundamental risks can't be ignored either. Starship is still in testing, with its most recent test flight failing to complete the full mission profile; Starlink ARPU continues to decline, from an early $130/month to below $80/month now; the AI segment, while burning cash, grows slower than dedicated AI players like xAI, OpenAI, and Anthropic's in-house operations.

Our assessment: SpaceX is a great company, but $1.75 trillion is a valuation that requires flawless execution over the next three years to justify. Any single hiccup could create 20-40% downside risk. Among concept stocks, divergence will be more intense than a broad rally—true beneficiaries (TSLA, QCOM, SATS, RDW) and bag-holders (DXYZ, XOVR, VCX) will be quickly distinguished by the market within three months post-IPO.

Tail risks also deserve a separate mention. For a company of SpaceX's size, normal valuation fluctuations are 20-40% corrections. But what would cause structural capital to flee are low-probability, high-impact events: a fatal Starship accident before crewed missions, a black swan in Musk's health or legal situation, US government intervention in SpaceX's ownership structure on national security grounds, or escalation of space militarization to asset destruction.

Individually, each event has low probability, but if any materializes, the impact wouldn't be limited to SpaceX's own valuation, but would cause a liquidity discount across the entire 17-concept-stock sector. Historical precedents like the 2018 Tesla privatization turmoil and the 2022 Twitter acquisition contagion show: assets strongly tied to Musk have non-independent tail risks. Portfolio-wise, we prefer keeping total exposure to the SpaceX ecosystem within 10-15% of a portfolio, rather than overweighting the space theme due to short-term gains—tail risks are hedged with position sizing, not stock selection.

Everyone looks up when the rocket launches, but the real money-making moment often comes when the rocket lands and is recovered.