Original link:https://x.com/chamath/status/2029650649819009211

Original author:Chamath Palihapitiya

Compiled by: Ken, Chaincathcer

The modern stock market is built on infrastructure that predates the digital network by a long time.

The global stock market has a market capitalization of over $150 trillion, but trading hours are still limited, settlement still relies on multiple layers of intermediaries, and investment opportunities in many high-growth companies are still restricted to a small number of investors.

These structural limitations constrain how capital flows, who can participate, and the speed of ownership changes.

Market infrastructure providers are already exploring how to use tokenization to modernize the system. Institutions including the New York Stock Exchange, Nasdaq, and DTCC have begun developing tokenized equity and settlement infrastructure.

With the adoption of equity tokenization, these barriers are beginning to erode.

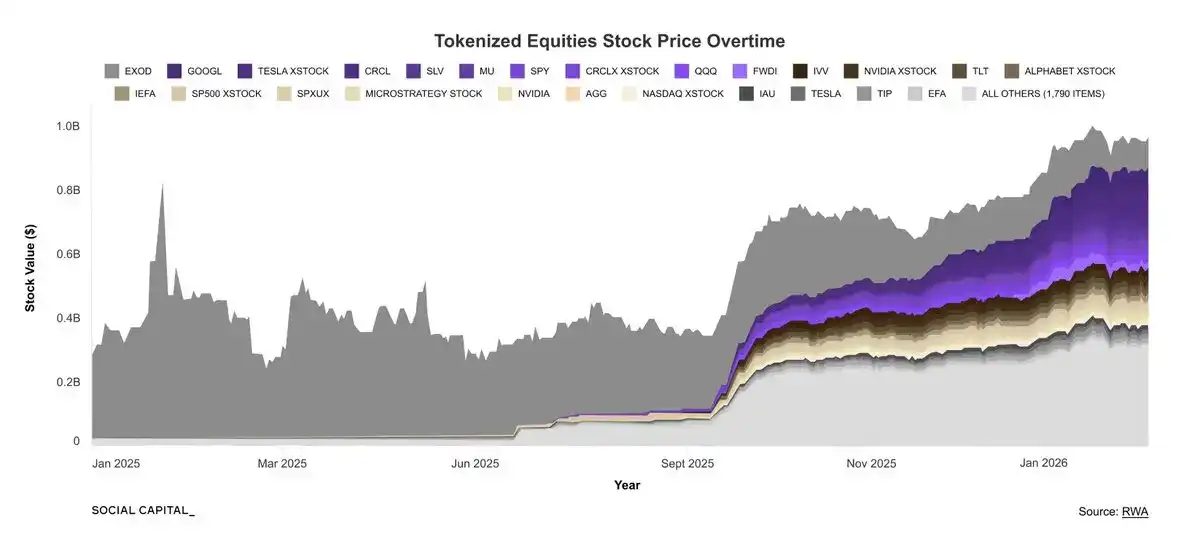

Since early 2025, the market capitalization of equity tokens has grown nearly 3.5 times, reflecting a broader shift towards the tokenization of real-world assets.

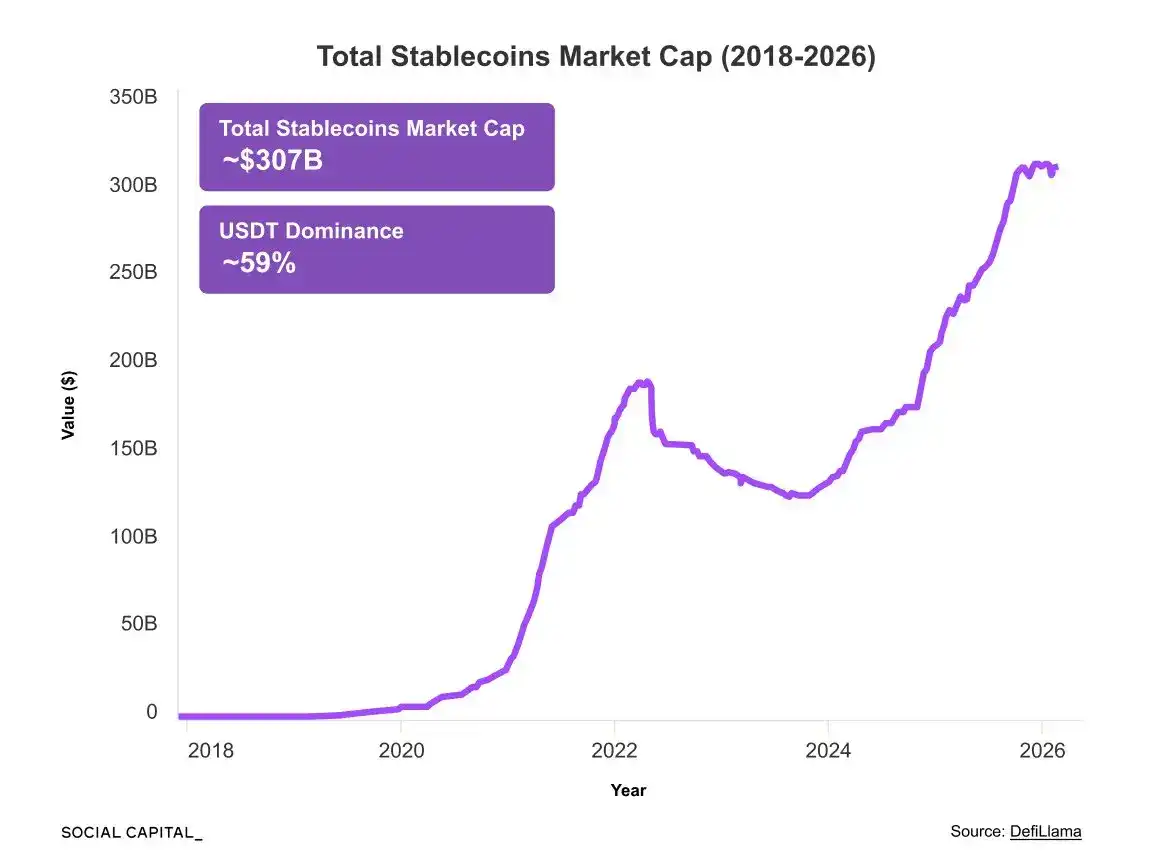

This expansion has occurred in parallel with the rise of stablecoins. These fiat-pegged tokens have grown more than tenfold in less than five years and have now become the primary settlement layer for on-chain financial activity:

While stablecoins function differently from equity tokens, their rapid adoption shows that when tokenized financial instruments offer clear infrastructure advantages, they can achieve significant scale.

Equity tokens represent the next test: can tokenization expand from payments to the ownership of financial assets.

What are Equity Tokens?

Equity tokens are not just traditional stocks placed on a blockchain.

Traditional stocks represent ownership in a company.

An equity token is a blockchain-based asset that represents shares in a company or structured rights related to those shares, with ownership tracked and transferred via Distributed Ledger Technology (DLT).

Tokenized Equity Can Address Three Major Market Gaps 24/7

-

24/7 Trading: Markets are shifting from a 5-day (or shorter) weekly trading model to uninterrupted 24-hour trading.

Even today, approximately 11% of U.S. stock trading occurs outside regular trading hours.

A 24/7 market structure allows new information to be priced in more quickly during after-hours sessions and better accommodates a global shareholder base, as foreign investors currently hold about 15% of U.S. stocks.

-

Ownership: In traditional finance, equity ownership records are spread across multiple intermediaries, including brokers, clearing firms, and central securities depositories.

Tokenization reduces reliance on these layers and allows for ownership to be tracked directly on a shared ledger.

This transforms equity from a static record into a programmable financial asset.

Owners can use the asset as collateral for on-chain loans. They can use it to secure credit. They can also place it into automated liquidity pools to generate yield.

In traditional markets, similar operations typically require multiple intermediaries and additional settlement steps. Each intermediary interaction incurs brokerage fees and commissions, costs that are ultimately passed on to the equity asset holder.

Even a modest reduction in post-trade friction is estimated to save the stock industry $5 billion to $10 billion annually.

-

Access Restrictions: While the first two advantages primarily apply to public market stocks, tokenization also addresses access restrictions in private markets.

Under current securities regulations, many private offerings are restricted to accredited investors. This typically requires an investor to have a net worth of $1 million (excluding primary residence), or an annual income of $200,000, or $300,000 jointly with a spouse.

Private companies must also control the number of shareholders to remain unlisted. U.S. regulations require companies to report to the SEC once they have more than 2,000 record shareholders or more than 500 non-accredited investors.

Furthermore, institutional venture capital funds often require limited partners to commit millions of dollars.

As a result, most investors have little access to these high-growth private companies before they enter the public markets.

Equity tokenization promises to bridge this access gap.

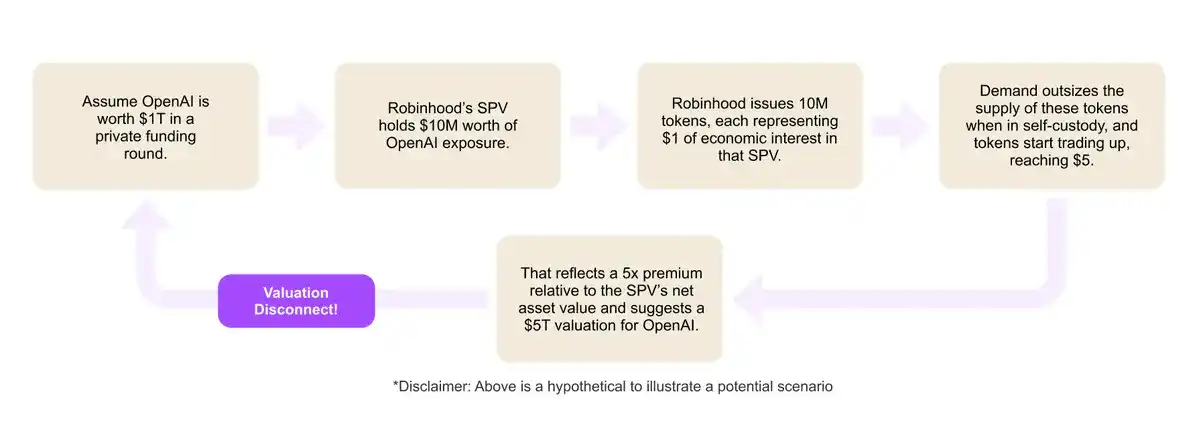

Equity tokens can be issued through various structural models, but the most common method currently relies on a Special Purpose Vehicle (SPV).

In this structure, the SPV holds the underlying shares, and the tokens represent economic claims on that entity. This allows issuers to give investors exposure to investments in private companies, opportunities that were previously limited to venture capital firms and institutional investors.

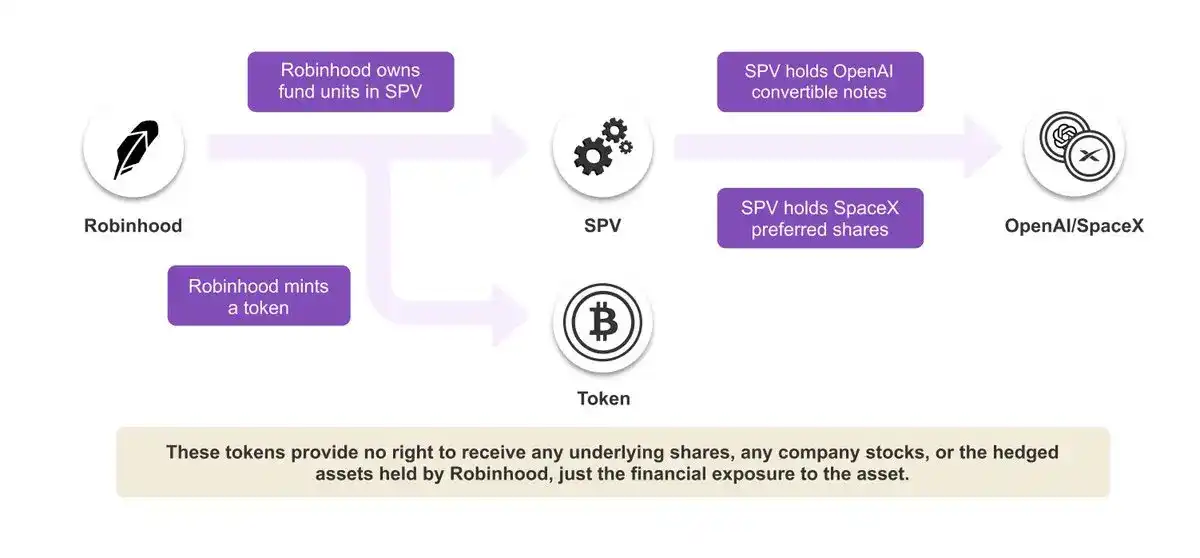

For example, Robinhood recently announced the rollout of tokens for OpenAI and SpaceX to eligible users in the EU.

These tokens give investors exposure to two of the world's hottest private companies. However, they do not represent direct ownership of OpenAI or SpaceX shares. Instead, the tokens represent financial interests linked to an intermediary entity.

This highlights a core challenge of equity tokenization: the rights represented by the token are not always standardized.

Different issuers can design tokens with substantially different economic rights. In Robinhood's case, it is currently unclear whether the SpaceX token provides preferred stock rights, or if the token can convert to common stock should SpaceX eventually go public.

Preferred and common stock differ in liquidation priority, voting rights, and return characteristics. Without clear articulation of these terms, it is difficult for investors to price or compare tokens pegged to the same company.

Consequently, many tokenized private equity offerings provide economic exposure rather than direct ownership. Because the token sits at a different legal level than the underlying share, investors must understand the structure before assuming what they own.

Despite these structural ambiguities, investor demand for access to private markets continues to grow. This is set against a backdrop where companies are also staying private for longer.

Surveys show that about 90% of Americans would be willing to allocate some of their retirement savings to private assets, with interest particularly strong among Gen Z and millennial investors.

Equity tokenization promises greater access to private markets, continuous liquidity, and new ways to structure financial ownership.