Securitize, a company focused on tokenizing securities, said Tuesday it plans to launch what it calls the first compliant, onchain trading experience for public stocks that are issued as tokens representing real share ownership.

According to the announcement, Securitize’s stock product is expected to launch in the first quarter of 2026. The company said the offering is designed to avoid structures that mirror stock prices without conveying ownership, and instead, the tokens “are real, regulated shares: issued onchain, recorded directly on the issuer’s cap table.”

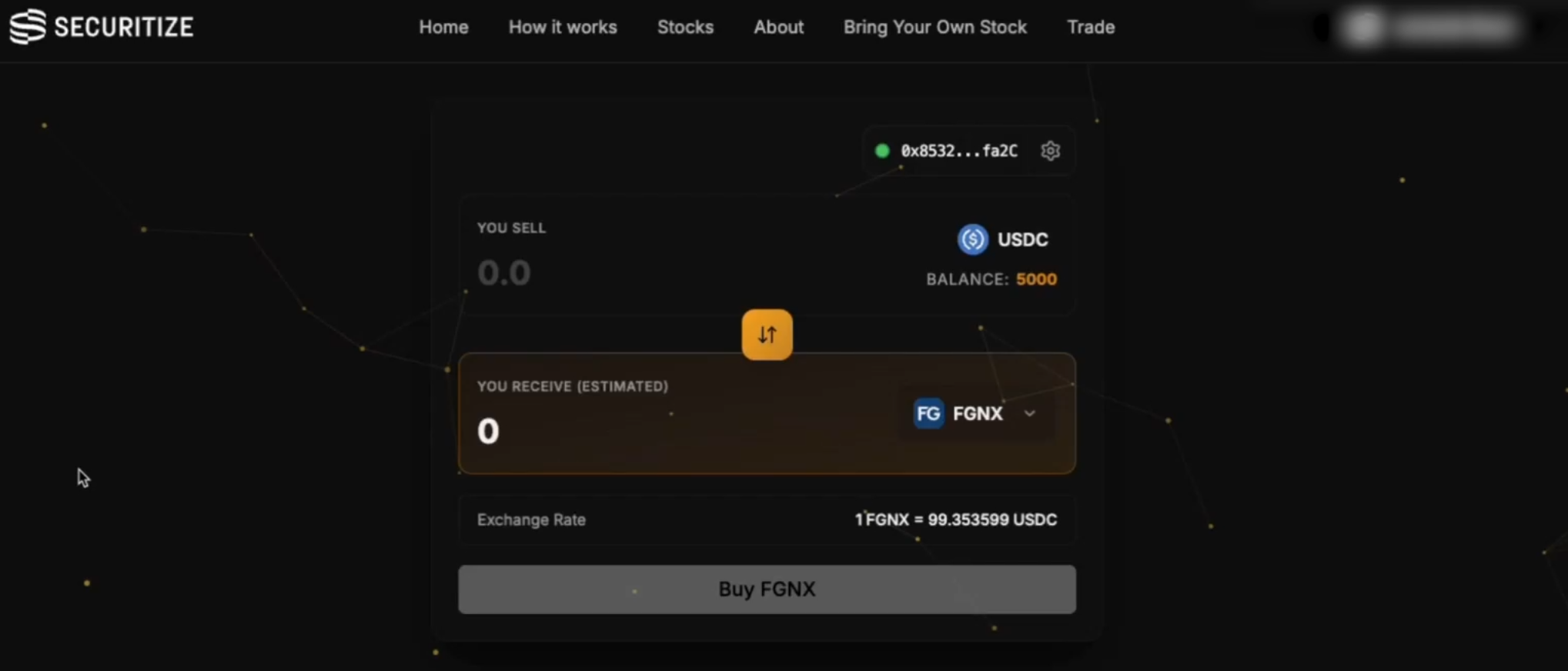

It also said trading will be presented in a “swap-style” interface familiar to users of decentralized finance, or decentralized finance (DeFi).

Securitize argued that natively tokenized public stocks, in which tokens represent actual stock ownership, were held onchain but mostly traded through traditional offchain processes. Its pitch is that buyers and sellers will be able to trade “fully on-chain” in real time, including during hours when traditional markets are closed.

Related: Binance hints at stock perps in push to join global tokenized equities race

A compliant tokenized stock ecosystem

Securitize criticized the recent wave of tokenized stock products, claiming they “offer exposure, not ownership.” The company said some products rely on special-purpose vehicles or offshore structures that can add counterparty risk or create pricing mismatches.

It also criticized tokenized stock products, which it said “are not even compliant, since they are issued as permissionless assets without Know Your Customer (KYC) or Anti-Money Laundering (AML) controls.

Still, the company notes that traditional stock infrastructure is antiquated and needs disintermediation and rebuilding, with investors rarely holding “shares in their own name, settlement takes at least a day.”

“If tokenization is going to matter at public-market scale, it must deliver ownership, real securities and maintain investor protections.“

Securitize said its approach is built around regulated securities and compliance requirements, including controls that limit transfers to approved, or whitelisted, wallets.

Related: Ondo wins Liechtenstein approval to offer tokenized stocks in Europe

Regulated shares make their way to DeFi

Securitize said it will act as the transfer agent for the shares, describing itself as registered with the US Securities and Exchange Commission. Transfer agents maintain shareholder records and process changes in ownership. By pairing that role with blockchain-based issuance, the company said the tokens would be legally recognized shares rather than a proxy claim.

Securitize downplayed faster settlement as the main selling point, saying the larger opportunity is programmability, or the ability for tokenized securities to interact with smart contracts and onchain financial applications.

It further argued that this programmability allows tokenized securities to be integrated with DeFi platforms “without compromising compliance or user protections.”

“This is not about replacing traditional finance. It’s about upgrading it,“ Securitize said.