Original Author: @BlazingKevin_, the Researcher at Movemaker

SEC Chairman Paul Atkins pointed out that the entire U.S. financial market, including stocks, fixed income, treasury bonds, and real estate, may fully migrate to the blockchain technology architecture that underpins cryptocurrencies within the next two years. This could be the most significant structural change in the U.S. financial system since the advent of electronic trading in the 1970s.

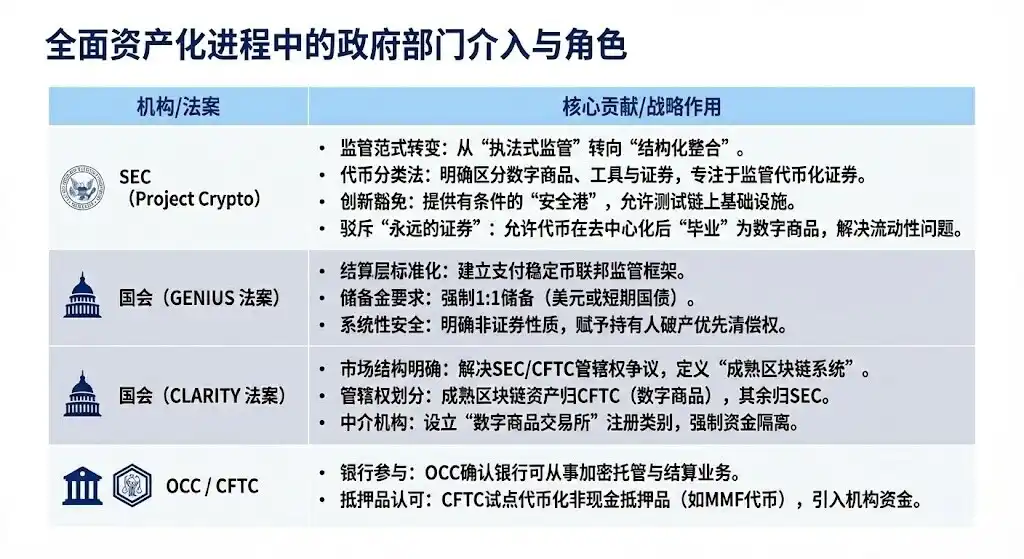

1. The Cross-Departmental Collaboration Framework and Actual Contributions of Full-Scale On-Chaining

The "Project Crypto" initiative promoted by Atkins is not a unilateral action by the SEC; it is built on systematic cooperation spanning legislation, regulation, and the private sector. Achieving the full-scale on-chaining of the U.S. financial market, valued at over $50 trillion (including stocks, bonds, treasury bonds, private credit, real estate, etc.), requires clear roles and contributions from multiple institutions.

1.1 Government Departments Involved in Comprehensive Assetization

It is necessary to add that the "Project Crypto" and the "Innovation Exemption" mechanism acknowledge the incompatibility of blockchain technology with existing financial regulations, providing a controlled experimental environment that allows traditional financial institutions (TradFi) to explore and implement tokenized infrastructure without violating core investor protection principles.

The GENIUS Act, by creating compliant, fully reserve-backed stablecoins and explicitly transferring regulatory authority to banking regulators, solves the Cash Leg problem necessary for institutions to conduct transactions and collateralize on-chain.

The CLARITY Act, by delineating the jurisdiction of the SEC and CFTC, specifically targets crypto-native platforms and creates a definition of "maturity," enabling institutions to clearly understand under which regulatory framework their held digital assets (such as Bitcoin) operate, while providing a pathway for crypto-native platforms to register as federally regulated intermediaries ("broker/dealers").

The OCC, established in 1973, specializes in providing clearing and settlement services for options, futures, and securities lending transactions, promoting market stability and integrity. The CFTC is the primary regulator of futures markets and futures merchants.

This cross-departmental synergy is a prerequisite for the full-scale on-chaining of the U.S. financial market, laying a solid foundation for the subsequent large-scale deployment by giants like BlackRock and J.P. Morgan and the integration of core infrastructure like DTCC.

2.2 Collaboration of Traditional Financial Giants

In the collaborative blueprint of U.S. traditional financial giants, the in-depth layouts of various institutions reflect more specific strategic focuses and technical details. BlackRock launched the first tokenized U.S. Treasury fund on a public chain (Ethereum), establishing its foundational role as an asset manager bringing traditional financial yields into the public chain ecosystem.

After renaming its blockchain business to Kinexys, J.P. Morgan allows banks to complete atomic swaps of tokenized collateral and cash within hours instead of days, significantly optimizing liquidity management; simultaneously, its pilot of JPMD on the Base chain is seen as a strategic step towards extending into the broader public blockchain ecosystem, aiming for stronger interoperability.

Finally, the specific breakthrough by the Depository Trust & Clearing Corporation (DTCC) was achieved by its subsidiary, the Depository Trust Company (DTC). As the world's most critical transaction infrastructure provider, the SEC's "no-action letter" it received enables it to connect the traditional CUSIP system with the new token infrastructure, thus formally initiating a pilot for the tokenization of mainstream assets, including Russell 1000 component stocks, in a controlled environment.

2. Analysis of the Financial Environment and Impact After Full Tokenization

The core goal of asset tokenization is to break the "silo effect" and "time constraints" of traditional finance, creating a globalized, programmable, 24/7 financial system.

2.1 Significant Enhancement of the Financial Environment: A Leap in Efficiency and Performance

Tokenization will bring efficiency and performance advantages that are difficult for traditional financial systems to match:

2.1.1 Leap in Settlement Speed (T+1/T+2 to T+0/Second-Level):

Improvement: Blockchain enables near real-time (T+0) or even second-level settlement and delivery, in stark contrast to the T+1 or T+2 settlement cycles typically required in traditional financial markets. UBS's digital bond issuance on SDX demonstrated T+0 settlement capability, and the European Investment Bank's digital bond issuance reduced settlement time from five days to one day.

Pain Points Addressed: Greatly reduces counterparty credit risk and operational risk caused by settlement lags. For time-sensitive transactions like repo and derivative margin calls, the improvement in settlement speed is crucial.

2.1.2 Revolution in Capital Efficiency and Liquidity Release:

Improvement: Achieves "atomic delivery," where assets and payment occur simultaneously in a single, indivisible transaction. Meanwhile, tokenization can release "sleeping capital" currently locked in settlement waiting periods or inefficient processes. For example, programmable collateral management could release over $100 billion in trapped capital annually.

Pain Points Addressed: Eliminates principal risk in traditional "delivery versus payment" operations. Reduces the need for high margin buffers at clearing houses. Additionally, Tokenized Money Market Funds (TMMFs) can be transferred directly as collateral, preserving yield and avoiding the liquidity friction and yield loss associated with redeeming cash and reinvesting in traditional systems.

2.1.3 Enhanced Transparency and Auditability:

Improvement: Distributed ledgers provide a single, immutable authoritative record of ownership, with all transaction history public and verifiable. Smart contracts can automatically execute compliance checks and corporate actions (e.g., dividend payments).

Pain Points Addressed: Completely solves the inefficiencies of data silos, multiple bookkeeping, and manual reconciliation in traditional finance. Provides regulators with an unprecedented "God's perspective," enabling real-time,穿透式 supervision and effective monitoring of systemic risk.

2.1.4 24/7/365 Global Market Access:

Improvement: Markets are no longer limited by traditional banking hours, time zones, or holidays. Tokenization makes cross-border transactions smoother, allowing assets to be transferred peer-to-peer globally.

Pain Points Addressed: Overcomes the time lags and geographical restrictions in traditional cross-border payments and liquidity management, particularly benefiting the cash management of multinational corporations.

2.2 Participants Most Affected

The changes brought by tokenization are disruptive, with the greatest impact on the following types of market participants:

Main Challenges and Risks:

- Trade-off between Liquidity and Netting: DTCC currently achieves enormous capital efficiency by netting millions of transactions, reducing the actual amount of cash and securities that need to be transferred by 98%. Atomic settlement (T+0) is essentially Real-Time Gross Settlement (RTGS), which may lead to a loss of netting efficiency. The market needs to find hybrid solutions balancing speed and capital efficiency, such as intraday repos.

- Privacy Paradox: Institutional finance relies on transaction privacy, while public chains (like Ethereum) are transparent. Large institutions cannot execute block trades on a public chain without being "front-run." Solutions include using privacy-preserving technologies like zero-knowledge proofs or operating on permissioned chains (like J.P. Morgan's Kinexys).

- Amplification of Systemic Risk: 24/7 markets eliminate the "cooling-off period" of traditional markets. Algorithmic trading and automated margin calls (via smart contracts) could trigger large-scale chain liquidations during market stress, amplifying systemic risk, similar to the liquidity stress in the UK's LDI crisis of 2022.

2.3 Core Value Proposition of Tokenized Funds (TMMF)

The tokenization of Money Market Funds (MMFs) is the most representative case in RWA growth. TMMFs are particularly attractive as collateral:

- Yield Retention: Unlike non-interest-bearing cash, TMMFs used as collateral can continue to earn yield until actually utilized, reducing the opportunity cost of "collateral drag."

- High Liquidity and Composability: TMMFs combine the regulatory familiarity and safety of traditional MMFs with the instant settlement and programmability brought by DLT. For example, BlackRock's BUIDL fund, through Circle's USDC instant redemption channel, addresses the T+1 redemption pain point of traditional MMFs, achieving 24/7 instant liquidity.

3. The Role of DTCC/DTC in the Tokenization Process

DTCC and DTC are indispensable core systemic institutions in U.S. financial infrastructure. The scale of assets custodied by DTC is enormous, covering the vast majority of stock registration, transfer, and custody in the U.S. capital market. DTCC and DTC are regarded as the "central warehouse" and "general ledger" of the U.S. stock market. The involvement of DTCC is key to fundamentally ensuring the compliance, security, and legal validity of the tokenization process.

3.1 Core Role and Responsibilities of DTC

- Identity and Scale: DTC is responsible for central securities custody, clearing, and asset servicing. As of 2025, DTC custodies assets worth $100.3 trillion, covering 1.44 million security issues, dominating the registration, transfer, and confirmation of rights for the vast majority of U.S. stocks.

- Tokenization Bridge and Compliance Assurance: DTCC's involvement represents the official endorsement of digital assets by traditional financial infrastructure. Its core responsibility is to act as a trust bridge between the traditional CUSIP system and emerging tokenization infrastructure. DTCC promises that tokenized assets will maintain the same high level of security, robustness, legal rights, and investor protection as traditional forms.

- Liquidity Integration: DTCC's strategic goal is to achieve a single liquidity pool between TradFi (Traditional Finance) and DeFi (Decentralized Finance) ecosystems through its ComposerX platform suite.

3.2 DTC Tokenization Process and SEC No-Action Letter

In December 2025, DTCC's subsidiary DTC obtained a landmark no-action letter from the U.S. SEC, which is the legal basis for its large-scale advancement of tokenization business.

3.3 Impact of DTC Tokenization

The approval of the DTC NAL is considered a milestone for tokenization, and its impact is mainly reflected in:

- Certainty of Official Tokens: DTC's tokenization means officially backed tokenized U.S. stocks are coming. Future projects conducting U.S. stock tokenization may directly access DTC's official asset tokens rather than building their own asset-on-chain infrastructure.

- Market Structure Integration: Tokenization will push the U.S. stock market towards a "CEX + DTC Custody Trust Company" model. Exchanges like Nasdaq may directly act as CEXs, while DTC manages token contracts and allows withdrawals, achieving complete liquidity打通 (liquidity打通 -打通 means打通, likely meaning打通 liquidity flow or integration).

- Enhanced Collateral Liquidity: DTC's tokenization services will support enhanced collateral liquidity, enabling 24/7 access and asset programmability. DTCC has been exploring the use of DLT technology to optimize collateral management for nearly a decade.

- Elimination of Market Fragmentation: Stock tokens are no longer a digital type fragmented from traditional assets but are fully integrated into the general ledger of the traditional capital market.

About Movemaker

Movemaker is the first official community organization authorized by the Aptos Foundation, jointly initiated by Ankaa and BlockBooster, focusing on promoting the construction and development of the Aptos Chinese-speaking ecosystem. As the official representative of Aptos in the Chinese-speaking region, Movemaker is committed to connecting developers, users, capital, and numerous ecosystem partners to build a diverse, open, and prosperous Aptos ecosystem.

Disclaimer:

This article/blog is for reference only and represents the author's personal views, not the position of Movemaker. This article is not intended to provide: (i) investment advice or recommendations; (ii) an offer or solicitation to buy, sell, or hold digital assets; or (iii) financial, accounting, legal, or tax advice. Holding digital assets, including stablecoins and NFTs, is extremely risky, with high price volatility, and may even become worthless. You should carefully consider whether trading or holding digital assets is suitable for you based on your financial situation. Please consult your legal, tax, or investment advisor for specific situations. The information provided in this article (including market data and statistics, if any) is for general reference only. Reasonable care has been taken in compiling this data and charts, but no responsibility is accepted for any factual errors or omissions expressed therein.