Michael Saylor used his Strategy World 2026 keynote on Feb. 25 to argue that Bitcoin-backed “digital credit” is moving beyond Wall Street wrappers and toward programmable distribution on crypto rails, naming Solana and Ethereum as part of that future. The pitch matters because it pushes Strategy’s Bitcoin treasury model into a broader product thesis: use Bitcoin as the capital base, then package credit, yield and liquidity for corporates, retail investors and eventually tokenized markets.

Bitcoin Capital, Credit Product

Saylor framed Bitcoin as the foundation of the stack and Strategy’s Stretch (STRC) as the credit layer built on top of it. In his telling, the company’s business is no longer just accumulating Bitcoin, but “converting capital into credit” by using long-duration capital structures to strip cash flow from a volatile asset and deliver it as a steadier yield product.

“What is Strategy doing? Our company is converting capital into credit. We’re converting economic wealth into a stream of cash flows,” Saylor said. “You need an operating company in order to take a block of economic energy and turn it into a currency, peg it to a currency, strip away the risk, damp the volatility, extract the cash flows in the form of yield and compress the duration to now.”

That framework sits at the center of his case for STRC. Saylor said Strategy arrived there only after working through what he described as increasingly durable forms of leverage, from exchange leverage and margin loans to senior debt, junior debt, convertibles and preferred structures.

The key variable, in his view, is not just headline maturity, but the “stochastic duration” of capital, how long a company can realistically rely on it before covenants, mark-to-market stress or refinancing pressure force a problem.

He argued that variable preferred credit offered the best compromise short of common equity because it maximized optionality and reduced the risk of getting squeezed out of the position during a drawdown.

Saylor also laid out a simple quantitative case for digital credit. Strategy, he said, uses three internal metrics: BTC rating, or collateral coverage; BTC risk, the probability that collateral falls below required levels by the end of the term; and the implied credit spread needed to compensate investors. He contrasted current benchmarks of 78 basis points for investment-grade bonds and 288 basis points for high-yield debt with what he said digital credit could deliver if Bitcoin compounds faster than traditional assets.

His model depends heavily on a constructive view of Bitcoin’s long-run returns. If Bitcoin appreciates at 30% annually, Saylor said, sizable volumes of investment-grade credit can be created against it. If Bitcoin goes nowhere, the same structure starts to look like distressed debt.

He used recent performance to sharpen that distinction. Since Bitcoin’s all-time high about four and a half months ago, Saylor said, Bitcoin had fallen 45%, while STRC had lost “0% of its value” and paid 4.5% in dividends through the drawdown. That, he argued, is the commercial opening: offer a less volatile yield instrument to buyers who want Bitcoin-linked economics without owning the asset outright.

Solana And Ethereum As Distribution Rails

The keynote’s most consequential turn came when Saylor described digital credit as “programmable.” He was not using the term narrowly.

“Programmable means I take the credit and I create it. I turn it into a token, a private fund, a public fund, an ETF, an ETP. I make it a bank account. I make it a crypto account,” he said. “Then I put it on a platform — the NASDAQ, the London Stock Exchange, Solana, Ethereum, Binance, Coinbase Base. There are a lot of different platforms I can put that on.”

BREAKING: Michael Saylor says the future of programmable digital credit will be deployed on Solanapic.twitter.com/F4scOmDaU3

— Solana (@solana) February 25, 2026

He went further, arguing that once credit is packaged as a modular product, issuers can tune volatility, liquidity, staking periods, payout frequency and currency exposure. In that framework, Solana and Ethereum are not the capital base (Bitcoin remains that in Saylor’s model) but potential rails for distributing tokenized versions of the credit product.

That leaves Strategy with a larger ambition than simply selling preferred stock. Saylor said the company intends to deepen STRC liquidity and scale the underlying asset base, while partners build “digital money” and “digital yield” products around it.

If that thesis holds, Strategy is betting Bitcoin-backed credit can move from a public-market niche into a cross-platform product category spanning brokerages, ETFs and on-chain ecosystems.

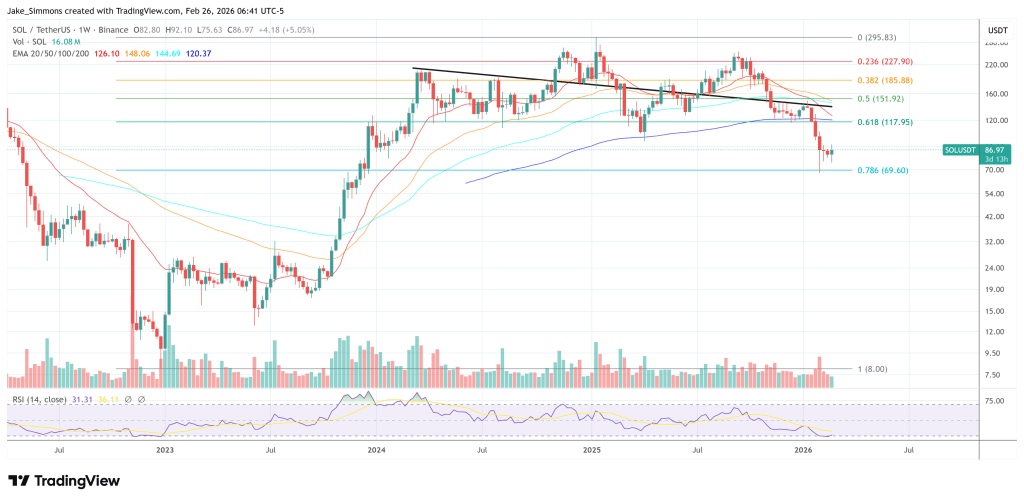

At press time, Solana traded at $86.97.