This weekly report covers the period from January 2, 2026, to January 9, 2026.

This week, the total on-chain market capitalization of RWA grew steadily to $19.8 billion, with holders surpassing 600,000; the total market capitalization of stablecoins slightly decreased, but the monthly transfer volume surged by 29.04%, highlighting that institutional large-scale settlements have become the main driver of activity under the "stock efficiency-driven" trend, forming a structural divergence from the low activity of retail investors.

Regulatory frameworks in multiple countries continue to improve: The People's Bank of China has clarified that it will steadily develop the digital yuan, and cross-border scenarios continue to be implemented, with MyBank completing the first cross-border scan-to-pay transaction between China and Laos; South Korea plans to require stablecoin issuers to be bank-led, and Russia is accelerating the application of the digital ruble in the budget system.

Projects are taking frequent actions: Jupiter launched the compliant reserve-backed stablecoin JupUSD, and Tempo released the TIP-20 token standard designed for payments. Traditional financial institutions are accelerating the integration of on-chain settlements and asset tokenization processes: UAE's RAKBank received approval to issue a dirham-pegged stablecoin, Lloyds Bank completed the UK's first tokenized deposit bond purchase transaction, and J.P. Morgan expanded JPM Coin to the Canton network. Additionally, former Brazilian central bank officials launched the yield-sharing stablecoin BRD, and Wyoming's official stablecoin FRNT was officially launched to the public, further enriching the forms and geographical distribution of stablecoins.

Data Insights

RWA Sector Overview

Latest data from RWA.xyz reveals that as of January 9, 2026, the total on-chain market capitalization of RWA reached $19.8 billion, a slight increase of 6.04% compared to the same period last month, maintaining steady growth rate, indicating continued activity in on-chain native financial activities; the total number of asset holders increased to approximately 607,400, a strong increase of 7.13% compared to the same period last month, indicating a continuously broadening investor base.

Stablecoin Market

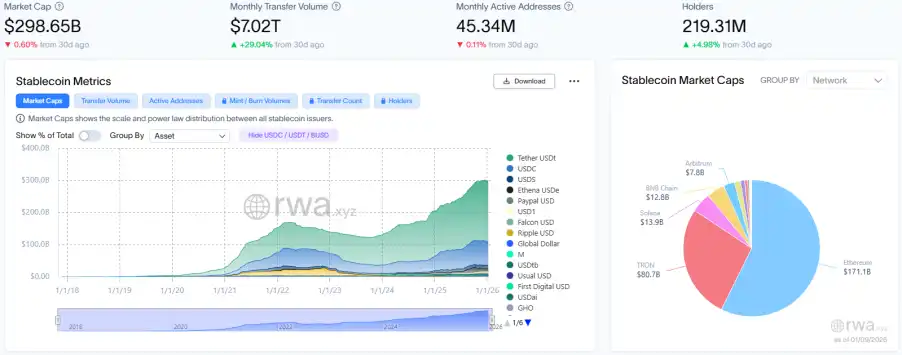

The total market capitalization of stablecoins reached $2.9865 trillion, a slight decrease of 0.6% compared to the same period last month, with the overall scale continuing to contract; the monthly transfer volume surged to $7.02 trillion, an increase of 29.04% compared to the same period last month, indicating a significant improvement in the turnover efficiency of existing funds; the total number of monthly active addresses decreased to 45.34 million, a slight drop of 0.11% compared to the same period last month; the total number of holders steadily increased to approximately 219 million, a slight increase of 4.98% compared to the same period last month. The continued divergence between the two indicates a structural differentiation in the market characterized by "institution-driven high-frequency settlements and stagnant retail activity."

The data reflects that the market has entered a stage of "stock efficiency-driven but weakened ecological foundation," where the high growth in transfer volume is mainly supported by institutional large-scale settlements, while retail participation remains persistently low.

The leading stablecoins are USDT, USDC, and USDS, among which USDT's market capitalization increased slightly by 0.44% compared to the same period last month; USDC's market capitalization decreased by 3.95% compared to the same period last month; USDS's market capitalization increased slightly by 2.11% compared to the same period last month.

Regulatory News

People's Bank of China: To Strengthen Virtual Currency Trading Supervision and Steadily Develop Digital Yuan in 2026

The People's Bank of China work conference for 2026 was held on January 5-6. The conference summarized the work in 2025, noting that in 2025, it actively promoted the improvement of global financial governance reform, further enhanced financial management and service levels, advanced the precise governance of fraud and gambling-related "capital chains," strengthened the supervision of virtual currency trading, enhanced cash supply security, and optimized the management system of the digital yuan. Key tasks for 2026 include: improving the infrastructure for cross-border use of the yuan, strengthening virtual currency supervision, continuously cracking down on related illegal activities, deepening technology management and innovative applications, and steadily developing the digital yuan.

Additionally, Caixin disclosed that currently, only real-name digital yuan wallets can accrue interest, meaning Category I, II, and III wallets can accrue interest, while Category IV non-real-name wallets do not (Category IV wallets cannot confirm the owner). After January 1, the mobile banking apps of participating operating banks and payment platforms such as WeChat and Alipay will gradually gain the authority to open digital yuan wallets.

South Korea Plans to Require Stablecoin Issuers to Be Bank-Controlled, with Paid-in Capital of at Least 5 Billion Won

According to Techinasia, South Korea's plan to allow banks to issue won-pegged stablecoins has encountered resistance from lawmakers, highlighting the divergence between the ruling party, financial regulators, and the central bank. The Financial Services Commission (FSC) has shifted its stance and now supports the central bank's proposal to restrict stablecoin issuance rights to consortia led and majority-controlled by banks.

According to the revised bill submitted to the National Assembly, stablecoins can be issued by consortia where banks hold a majority stake, but technology companies can be the largest single shareholder as long as the bank maintains overall majority control. The proposal will also impose stricter requirements on cryptocurrency exchanges, such as raising IT stability standards, mandating compensation for losses caused by hacking attacks, and imposing fines of up to 10% of annual revenue. Stablecoin issuers must have at least 5 billion won (approximately $3.7 million) in paid-in capital, and regulators may raise this threshold as the market develops. As the debate continues, lawmakers are expected to form a special task force to propose alternative legislative plans.

Russia Begins Large-Scale Introduction of Digital Ruble into Budget and Banking Systems

According to Cryptopolitan citing RIA Novosti, Russia has begun large-scale introduction of the digital ruble into the budget system and banking sector, preparing for a full rollout in September this year. Since the beginning of the year, the digital ruble has been actively used for state-related transactions and can now be used for transfers to the government budget and payments to federal agencies.

Russia has set a phased timeline and deadlines for the rollout of the digital ruble for banks and businesses, stipulating that by September 1, 2026, Russia's largest banks and their institutional retail clients must allow customers to use the digital ruble for transactions. The Central Bank of Russia also decided that starting last week, when digital ruble accounts of citizens and companies are used for paying taxes, fees, and government-related payments, these transactions will be exempt from handling fees.

Local Dynamics

YTO Express: The Company's Cross-Border Payment and Domestic Supply Chain Service Links Do Not Currently Involve Digital Yuan Payment Scenarios

According to Zhitong Caijing, YTO Express stated on an interactive platform that currently, the company's cross-border payment and domestic supply chain service links do not involve digital yuan payment scenarios. The company will continue to track digital yuan policies and market dynamics, reserve relevant technical adaptation capabilities, and explore its application feasibility in scenarios such as cross-border settlements.

China and Laos Pilot Cross-Border Digital Payment Cooperation, MyBank Completes First Digital Yuan Scan-to-Pay Transaction

According to 21st Century Business Herald, under the guidance of the People's Bank of China, MyBank, by connecting to the cross-border digital payment platform of the digital yuan international operation center, completed the first digital yuan scan-to-pay consumption at a merchant in Laos. This is the latest progress in the bilateral cross-border digital payment cooperation project between the central banks of China and Laos. The opening of this path宣告 the digital yuan has achieved "internal package external use" for the first time, providing a new payment method for Chinese residents consuming overseas, and is another manifestation of the deepening cooperation on central bank digital currencies between China and Laos.

Project Progress

Jupiter Officially Launches JupUSD Stablecoin Built on Ethena Technology

According to an official announcement, Jupiter announced the official launch of the stablecoin JupUSD, a reserve-backed, dollar-pegged stablecoin built on Ethena Labs technology, "designed to power the next chapter of finance." Initially, 90% of its reserves will consist of the compliant, GENIUS-standard stablecoin USDtb, collateralized by BlackRock's BUIDL fund, paired with 10% USDC as a liquidity buffer. While JupUSD does not generate yield, it can be integrated with Jupiter Lend for deposits, loans, or leverage operations, and enjoy exclusive benefits. Depositing funds into Lend's yield vault will earn users jlJupUSD, which offers unique promotional benefits, providing additional liquidity and utility for JupUSD.

MANTRA: All ERC20 Version OM Tokens Will Be Deprecated on January 15, Please Migrate Soon

MANTRA, a Layer1 blockchain focused on RWA assets, reminded on platform X that currently, less than 8% of the total OM token supply is the ERC20 version of OM tokens. On January 15, all ERC20 version OM tokens will be officially deprecated. Please migrate as soon as possible.

Latin American Digital Bank Kontigo Promises to Compensate Customers After Theft of Approximately $340,000 in Stablecoins

According to Bloomberg, Latin America-focused digital bank Kontigo stated in a declaration on platform X on Monday that a hack caused losses of stablecoins worth approximately $340,905 for some customers, and the company plans to compensate over 1,000 customers. Kontigo said in an earlier post: "We detected unauthorized access, and some users' funds were affected. User funds are protected, and any affected will be compensated by Kontigo."

Kontigo is headquartered in San Francisco but focuses on cryptocurrency and payment services in Latin America. Since its establishment in 2023, the company has grown rapidly and attracted many well-known partners. According to its website, Kontigo currently has over 1 million monthly active users, with total platform payments exceeding $1 billion. The company recently raised $20 million in a seed round from investors including Y Combinator.

Tempo Releases TIP-20 Token Standard Designed for Stablecoins and Payment Scenarios

According to an official Tempo announcement, it launched the new TIP-20 token standard, designed for stablecoins and payment applications, extended from ERC-20, and compatible with the existing EVM ecosystem. TIP-20 integrates transfer memos, a compliance policy registry, a yield distribution mechanism, and stablecoin payment for gas, making it suitable for diverse scenarios such as corporate finance, cross-border settlements, and interest-bearing stablecoins.

TIP-20 has received support from infrastructure partners including AllUnity, Bridge, and LayerZero, aiming to build a unified on-chain payment standard, improve the compliance, efficiency, and interoperability of stablecoins, and accelerate the on-chain process of real-world payment scenarios. Tempo will provide developers with SDK, test funds, and documentation support to facilitate the rapid deployment and implementation of TIP-20.

RAKBank Receives In-Principle Approval from UAE Central Bank to Issue Dirham-Pegged Stablecoin

According to Cointelegraph, on Wednesday, RAKBank is preparing to join the UAE stablecoin ecosystem after receiving in-principle approval from the UAE Central Bank (CBUAE) to issue a UAE dirham-pegged payment token. The bank stated in a press release on Wednesday that the upcoming stablecoin will be fully backed 1:1 by dirhams held in a separately regulated account, managed by audited smart contracts, and具备 real-time proof of reserves. The launch of this stablecoin marks a new phase in RAKBank's digital asset strategy, following the bank's move in 2025 to allow retail customers to trade cryptocurrencies through regulated brokerage partners.

Barclays Bank Invests in Stablecoin Clearing Platform Ubyx

According to Cointelegraph, Barclays Bank made its first investment in a stablecoin-related company—U.S. stablecoin clearing platform Ubyx—though the specific scale of the investment was not disclosed. Ryan Hayward, Head of Digital Assets and Strategic Investments at Barclays, said: "As the token, blockchain, and wallet space continues to evolve, specialized technology will play a key role in providing connectivity and infrastructure, helping regulated financial institutions interact seamlessly. This investment aligns with Barclays' approach to exploring opportunities based on new types of digital currency, such as stablecoins."

Lloyds Bank Completes UK's First Purchase of Government Bonds Using Tokenized Deposits

According to CoinDesk, UK lender Lloyds Banking Group claimed to have completed the UK's first purchase of UK government bonds using tokenized deposits. Lloyds Bank is the UK's third-largest bank by market capitalization. The bank stated that it completed the purchase of the UK government bonds with the help of crypto trading platform Archax and the privacy-focused Canton network. This purchase demonstrates that tokenization technology can transform traditional banking by converting real-world assets into digital forms, enabling instant buying, selling, or transfer.

In this transaction, Lloyds Bank plc, a subsidiary of Lloyds Banking Group, issued tokenized deposits on the Canton network. Subsequently, Lloyds Bank Corporate Markets used these deposits to purchase tokenized government bonds from Archax. Finally, Archax transferred the underlying funds back to its regular account at Lloyds Bank.

J.P. Morgan Deploys JPM Coin to Canton Network

According to The Block, J.P. Morgan's blockchain and digital payments division, Kinexys, announced the deployment of JPMCoin (JPMD) to the Canton network. This is the second expansion following its launch on the Coinbase-backed Ethereum Layer2 network Base in November 2025.

JPMCoin is a U.S. dollar deposit token issued by J.P. Morgan, providing institutional clients with an alternative to stablecoins and supporting 24/7 instant peer-to-peer transactions.

Former Brazilian Central Bank Official Launches BRD Stablecoin Pegged to Real Exchange Rate with Yield Sharing

According to CoinDesk, former Brazilian central bank director Tony Volpon launched a yield-sharing stablecoin pegged to the Brazilian currency and backed by Brazilian government debt—BRD. Volpon stated on the "Cripto na Real" program on Brazilian CNN that the token will be supported by national treasury bonds, linking its value to sovereign debt, aiming to allow holders to enjoy the benefits of local interest rates. The Brazilian central bank's benchmark interest rate is 15%, while the Federal Reserve's target rate is 3.5% to 3.75%.

Volpon stated that this move aims to make it easier for foreign investors to enter Brazil's high-yield environment. Although Brazil's interest rates have long attracted international attention, access to these yields has often been limited due to regulatory restrictions, currency friction, and domestic infrastructure. BRD could increase demand for the country's debt and potentially lower borrowing costs by expanding the investor base.

Wyoming's Official Stablecoin FRNT Officially Launched to the Public via Kraken, Deployed on Solana

According to an announcement from the Wyoming Stable Token Commission, the U.S. state of Wyoming officially launched its government-backed, fully reserve-backed stablecoin "FRNT" to the public through the Kraken exchange, becoming the first U.S. public institution to issue a fully reserve-backed stablecoin. FRNT is deployed on the Solana blockchain and can be bridged to multiple networks such as Ethereum and Arbitrum via Stargate. The coin is available to individuals and institutions, supports second-level settlements, and has transaction fees as low as $0.01. The interest on its reserves will be used to support education within the state.

OSL Global Lists Four Trading Pairs Including Gold-Backed Stablecoin PAXG

OSL Global, the global exchange under OSL Group, announced that it officially listed the U.S. dollar trading pair for the gold-backed stablecoin PAX Gold (PAXG) today. Users can trade PAXG/USD, and deposit and withdrawal functions via the Ethereum network have been enabled.

Simultaneously, OSL Global has also listed three U.S. dollar trading pairs for Worldcoin (WLD), Pump.Fun (PUMP), and Curve Dao Token (CRV). Users can trade WLD/USD, PUMP/USD, and CRV/USD. Among them, deposit and withdrawal functions for WLD and CRV have been enabled via the Ethereum network, while for PUMP, they can be completed via the Solana network.

Morgan Stanley Plans to Launch Digital Wallet This Year to Support Tokenized Assets

According to market news: Morgan Stanley plans to launch a digital wallet later this year to support tokenized assets.

RWA Trading Platform MSX Lists Spot and Contract Targets Across Multiple Sectors

According to official news, MSX has newly listed spot and contract trading for U.S. aircraft carrier and strategic nuclear submarine manufacturer $HII.M, NASA technology and engineering solutions provider $KBR.M, the largest U.S. independent oil and gas producer $COP.M, global oilfield services technology leader $SLB.M, as well as Vietnam ETF $VNM.M, Japan ETF $EWJ.M, and South Korea ETF $EWY.M.

Insight Collection

BlackRock: Stablecoins Are No Longer Niche, Will Challenge Fiat Dominance and Reshape Bank Deposit Landscape

According to DL News, BlackRock stated in its "2026 Global Outlook" that stablecoins will challenge governments' control over fiat currency. As stablecoin adoption surges, there is a risk of shrinking scale in the use of fiat currencies in emerging market countries. Samara Cohen, Global Head of Market Development at BlackRock, said: "Stablecoins are no longer a niche product; they are becoming a bridge between traditional finance and digital liquidity."

It is reported that UK's Standard Chartered Bank warned in October that the popularity of stablecoins could lead to a loss of over $1 trillion in deposits from emerging market bank accounts. Similar challenges also exist in the U.S. banking industry. The landmark stablecoin bill "GENIUS Act," signed into law in July of this year, allows crypto companies to offer yield-like products that traditional banks are prohibited from offering, posing a threat to traditional financial institutions.

Moody's 2026 Outlook: Stablecoins to Become Core Market Infrastructure

According to Cointelegraph, Moody's latest cross-industry outlook report indicates that stablecoins are transitioning from crypto-native tools to the core of institutional market infrastructure. Its report released on Monday shows that based on industry estimates for on-chain transactions (not merely interbank fund flows), stablecoin settlement volume in 2025 grew by approximately 87% compared to the previous year, reaching about $9 trillion. Moody's believes that fiat-collateralized stablecoins and tokenized deposits are becoming "digital cash" for liquidity management, collateral transfer, and settlement in an increasingly tokenized financial system.

Moody's lists stablecoins alongside tokenized bonds, funds, and credit products as part of the integration of traditional and digital finance. In 2025, banks, asset management companies, and market infrastructure providers launched pilot programs for blockchain settlement networks, tokenization platforms, and digital custody to simplify issuance, post-trade processes, and intraday liquidity management. As companies build large-scale tokenization and programmable settlement infrastructure, the report estimates that these initiatives will attract over $300 billion in investment in digital finance and infrastructure by 2030. In this landscape, stablecoins and tokenized deposits are increasingly becoming settlement assets for cross-border payments, repos, and collateral transfers. Moody's emphasizes that if stablecoins are to become reliable institutional settlement assets rather than a new source of systemic fragility, security, interoperability, and governance and regulatory clarity are equally important.

Venezuela's On-Chain Phantom: USDT Becomes Hard Currency, Possibly Secretly Building a Hundred-Billion Dollar Bitcoin "Shadow Reserve"

PANews Summary: Due to hyperinflation, the national currency, the bolivar, has lost credibility. USDT (dollar stablecoin) has become the default "hard currency" in daily life, used for shopping, payments, and even 80% of oil sales settlements. Simultaneously, to evade U.S. sanctions, it is rumored that the government is secretly converting gold and oil revenues into Bitcoin, possibly accumulating a "shadow reserve" of Bitcoin worth hundreds of billions of dollars. This case extremely demonstrates the dual role of cryptocurrency: for the people, it is a safe-haven tool and medium of exchange for livelihood; for sanctioned countries, it may become a secret weapon to bypass traditional financial blockades and store national wealth,预示 a new global financial game is taking place.

Trend Research: In 2026, Tech and AI Companies Will Accelerate Their Layout in Stablecoins, WLFI and USD1 to Become the Biggest Beneficiaries

PANews Summary: The stablecoin market will experience explosive growth in 2026, driven by three core factors: large-scale布局 by tech and AI companies, clear U.S. regulatory legislation (the "Genius Act"), and the trend of financial assets "going on-chain" promoted by Wall Street. In this wave, the compliant stablecoin USD1, issued by World Liberty Financial (WLFI), will become the biggest beneficiary due to its strong compliance (in line with the new U.S. act), transparent and reliable reserve custody, and backing by a strong background. It is expected to rapidly expand from the crypto market to traditional finance, internet payments, and offline scenarios, with the ultimate goal of building a panoramic financial ecosystem serving global users.

Mankun Research | Is Dubai the Global Optimal Compliance Solution for RWA?

PANews Summary: In the global RWA (Real World Asset tokenization) field, traditional financial centers (such as the U.S., Singapore, Hong Kong, the EU) face challenges of poor liquidity and high compliance costs because most yield-bearing RWA projects are classified as "securities," limiting them to professional investors. Dubai, with its VARA (Virtual Assets Regulatory Authority) framework, provides a unique "optimal solution": it is not about lax regulation but innovatively regulates RWA as an independent category of "virtual assets" rather than强行 applying traditional securities laws. This allows qualified RWA projects to legally target retail investors, conduct public offerings, and list on compliant exchanges, thereby truly achieving asset liquidity and commercialization. Therefore, Dubai is becoming a key hub attracting global RWA projects to land. Its core value lies in providing a new regulatory paradigm for RWA that is implementable, supports public offerings, and allows global business expansion.