Original author: angelilu, Foresight News

Looking back at 2025, Arthur Hayes remains the big winner who is both loved and hated.

As the founder of BitMEX and the KOL in the crypto circle who is best at writing "essays," every "hype call" he made in 2025 could stir up retail trading enthusiasm. But looking back at 2025, you will suddenly realize that if you got on board every time he made a call, the result would be that he made money, and you lost.

He shouted "Bitcoin to one million dollars" and "ETH to $10,000" on Twitter, but on-chain, Arthur Hayes would always inadvertently sell the assets he once favored. If we lay out all his operations from last year, you will find an extremely calm, even冷酷 (cold-blooded), trading record of a top trader.

We can break down his operations into three categories.

VC Coins: "Publicly Hype, Privately Dump"

Hayes' most controversial operations usually occur with projects where he obtained early筹码 (chips/allocations). This is actually a completely asymmetrical game: perhaps he made 10x when selling at $50, while your losses were just beginning when buying at $60.

The most typical script happened with Hyperliquid (HYPE). As an early investor who obtained extremely low-cost筹码 (chips), his operating logic is very simple and crude:

Step one: Use influence to hype at high prices, building grand narratives (e.g., "HYPE 100x in three years");

Step two: Wait until the token unlocks or liquidity is sufficient, then decisively clear the position.

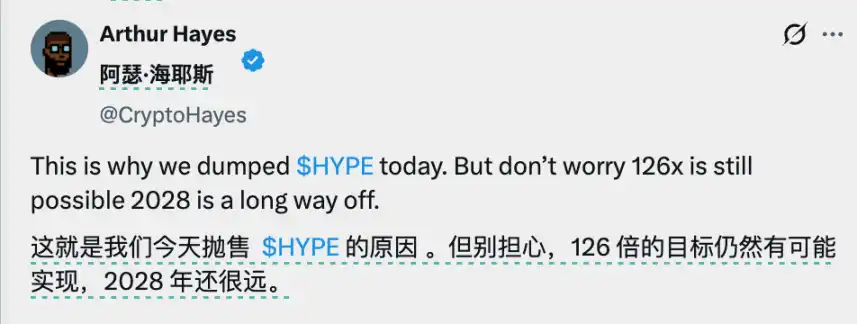

For example, last August, Hayes predicted at a conference in Tokyo that HYPE would have hundred-fold growth and高调 (high-profile) bought in. Just one month later, he cleared his position before HYPE fell and made millions of dollars in profit, giving the reason "to avoid unlocking risks."

But HYPE was not completely abandoned by him. In mid-January 2026, Hayes bought about $499,000 worth of HYPE again after three months.

The same story happened repeatedly, including with ETHFI, ATH, etc., all experiencing similar scripts.

But imagine, if you were Arthur Hayes, what would you do? To achieve profit with large capital, this seems to be the standard playbook: first, put forward market analysis that is足以自圆其说 (sufficient to justify itself),征服 (conquering) the audience with logic; when believers flock in, the market will naturally confirm his prophecy.

And for whales, the only window to quietly exit is when the crowd is bustling and liquidity is most abundant.

The "Old Narratives" That Couldn't Be Hype

After reviewing Hayes' successful hype narratives, we found that Hayes also had times when he failed. Especially when he tried to "revive" some old or niche sectors.

In early 2025, his family fund Maelstrom wrote a long and profound article "Degen DeSci," strongly bullish on the DeSci (Decentralized Science) sector. He listed a bunch of coins, BIO, GROW...

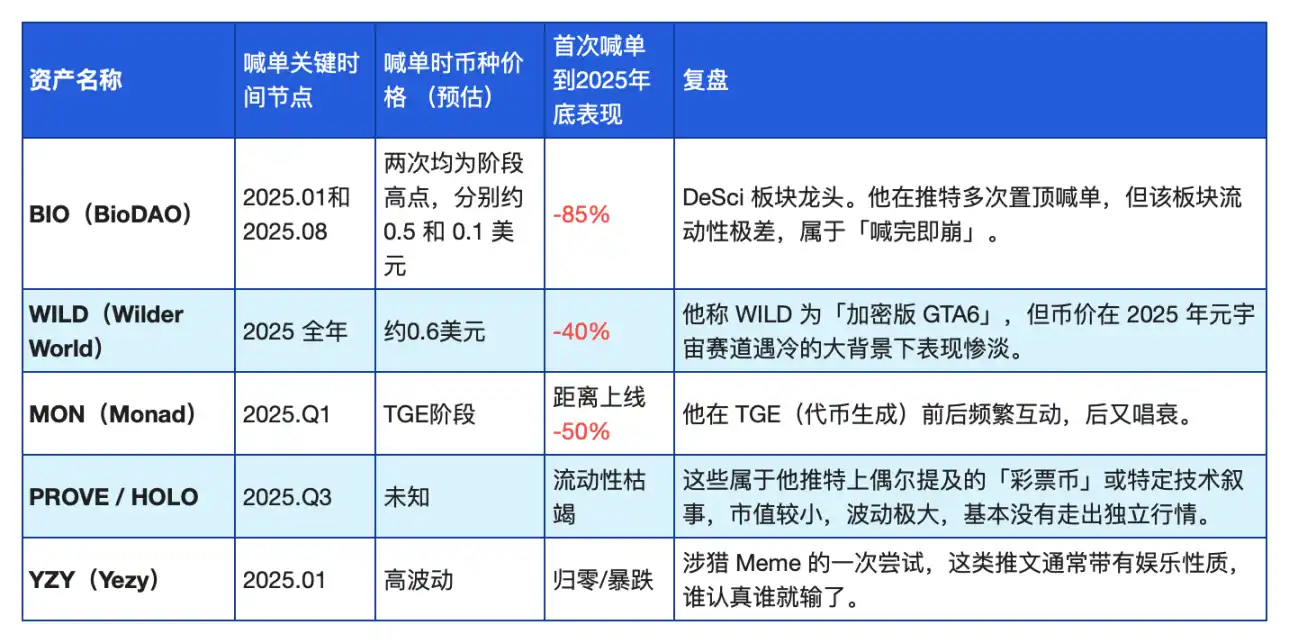

The result is clear for all to see: the DeSci sector almost全军覆没 (was completely wiped out), with many tokens falling more than 85% from their highs. Hayes built a position of $1.1 million worth of BIO again in August and finally deposited 7.66 million BIO into Binance in late November, with a potential loss of $640,000 (-58%).

Then there's Wilder World (WILD), which he called the "Crypto version of GTA6." He hyped it for a whole year, and finally the price sank along with the metaverse concept.

Most of the tokens Hayes hyped had热度 (heat/hype) at specific stages. A summary is shown in the chart:

ZEC's "Smoke Screen"

This might be Hayes' most brilliant and intriguing operation in 2025.

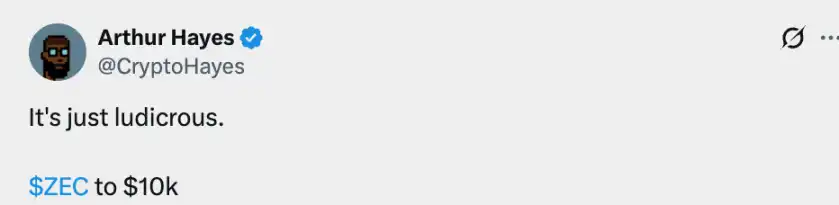

On the surface, Hayes疯狂 (crazily) hyped Zcash (ZEC), stating that he initially bought millions of dollars worth after hearing the suggestion from Silicon Valley big shot Naval at a private dinner during Token 2049. In November last year, he shouted the slogan "target $10,000."

Hayes even initiated a withdrawal movement, calling on everyone to withdraw their coins to the chain to lock up liquidity.

Many people watched his wallet to see if he was secretly selling ZEC. The result: he didn't sell; he was even adding to his position.

Perhaps the real purpose of Hayes creating this ZEC frenzy was: to sell ETH and exchange it for anything that was rising fast at the time.

Hayes had actually already taken a "knife" to ETH several times before this. Although he高喊 (shouted loudly) in 2025 that ETH would rise to $10,000, he experienced several "反复横跳" (back-and-forth jumps). He sold about $13.34 million worth of ETH and other tokens on August 2nd but expressed regret on August 9th for taking profits and had to buy back.

By November 15, 2025, just when he was vigorously hyping ZEC, Lookonchain monitored him transferring millions of dollars worth of ETH and ENA to Binance. On the same day, Hayes publicly declared on Twitter that he had "Aped more ZEC." On-chain analyst EmberCN also分析指出 (analyzed and pointed out) that this selling was极大概率 (most likely) to supply "ammunition" for adding to the ZEC position.

Due to ZEC's privacy features, his transparent ETH was sold and exchanged for opaque assets. On the chain, we can only see him "exiting" (selling ETH) but cannot quantify the scale of his "entering" (buying ZEC).

But in the last two weeks of 2025, Hayes sold another 1,871 ETH (about $5.53 million) and went back to buy the DeFi assets he had abandoned a month earlier.

This is a very冷酷 (cold) signal: in his logic, Ethereum is the "cash reserve" in his investment组合 (portfolio). He sells it when he needs money to buy new narratives (ZEC), and he still sells it when he needs money to bottom-fish old sectors (DeFi).

In the end, you will find that he used ZEC's price increase to attract the attention of the entire market, and then quietly completed his position rotation while everyone was discussing the "privacy renaissance." It wasn't until early 2026, when ZEC plummeted due to internal team strife, that everyone realized that although Hayes's holdings had shrunk, he successfully exited the top of ETH, which performed even worse during that phase.

How to Understand Arthur Hayes?

After reviewing this year, you will find that Hayes,正如 (just as) written in his X background picture, is not a "believer" HODLer but an extremely精明 (shrewd) businessman.

He uses words to build dreams to attract liquidity; he uses on-chain operations to harvest profits to avoid risks; he dares to quickly admit mistakes when he is wrong (e.g., abandoning ETH) to preserve capital.

So, his articles are still worth reading because his macro judgments have been verified. But before you press the "buy" button, please take one more step: don't listen to what he says, go see what his on-chain wallet is doing.

After all, in this残酷 (cruel) market, his loyalty to "volatility" is far higher than his belief in any single project. And volatility is precisely the money transferred from the pockets of retail traders to the pockets of traders.