Author: Dovey Wan, Founding Partner of Primitive Ventures

Compiled by: Dayu

In 2025, the cryptocurrency industry achieved almost all its expected goals. Structurally, this should have been a glorious year.

But why does it feel... so lifeless?

It's not just that "prices didn't rise" and it's all over. Bitcoin hit new highs. But the atmosphere, sentiment, internal confirmation, follow-through from other cryptocurrencies, and retail enthusiasm have all changed. Perhaps most worryingly, the former "hot money leading asset" has now lost its appeal in terms of wealth effect and volatility.

Related cryptocurrency assets no longer move in sync with Bitcoin and Ethereum as they did in previous cycles:

1. Memecoins topped the charts from Q4 2024 to Q1 2025, and the launch of Trump tokens pushed this trend to its peak.

2. Crypto stocks peaked around the Circle IPO and began to fall back between May and August 2025.

3. Most altcoins never formed a sustained trend. There was asymmetry on the way up, and the decline was entirely dominated by all participants.

Zooming in, the situation becomes even stranger.

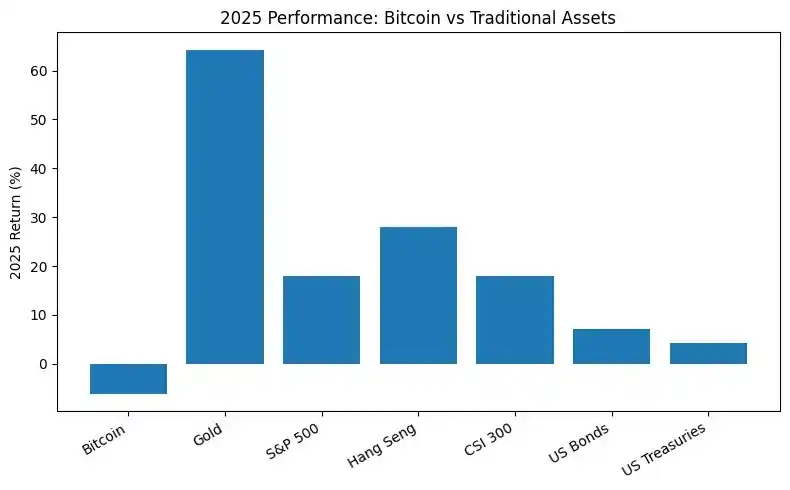

Despite a friendly policy environment, Bitcoin's performance in 2025 lagged behind almost all major traditional financial assets, including gold, U.S. stocks, Hong Kong stocks, A-shares, and even some bond benchmark indices.

(Bitcoin's performance compared poorly to other assets)

This is the first time Bitcoin's performance has decoupled from all other asset classes.

This divergence is crucial: prices hit new highs, but there was no internal confirmation, and other markets performed better. This reveals a simple yet unsettling fact: Bitcoin's liquidity supply chain has undergone significant changes, and its original four-year settlement cycle has been altered by greater forces in other markets.

Therefore, we will delve into who was buying at the highs, who exited the market, and where the price bottom lies.

The Great Divide: Onshore vs. Offshore Operations

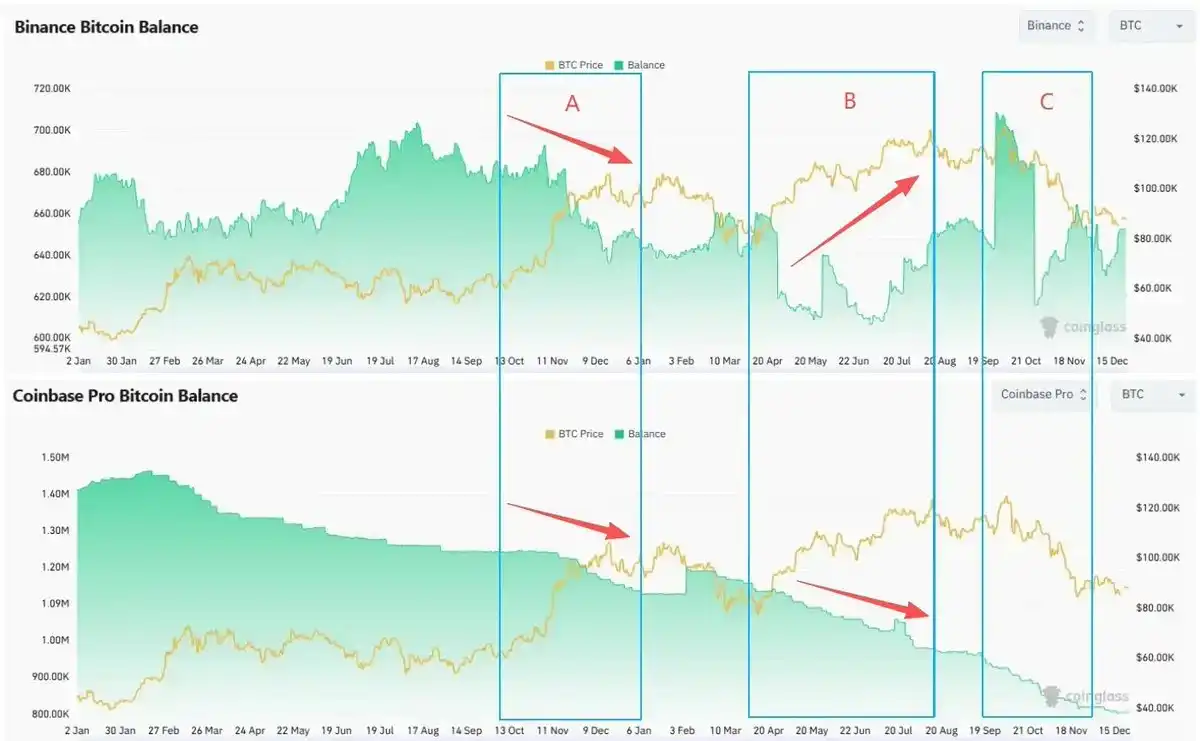

We experienced three distinct phases in this cycle—

-

Phase A (November 2024 to January 2025): Trump's election victory and a more friendly regulatory environment triggered FOMO among both domestic and foreign investors. Bitcoin's price broke through $100,000 for the first time.

-

Phase B (April to mid-August 2025): After deleveraging selling, BTC resumed its upward momentum and broke through $120,000.

-

Phase C (Early October 2025): BTC hit its current local all-time high in early October, then experienced a flash crash on October 10th and entered a correction phase.

In each phase, we saw a significant divergence between U.S. buying and overseas selling—

Spot: Onshore buying on breakouts, offshore selling on strength.

-

Coinbase Premium remained positive in Phases A, B, and C. High levels of buy-side demand primarily came from onshore spot funds.

-

Coinbase BTC balances showed a declining trend throughout the cycle. Sellable inventory on the U.S. side decreased.

-

As prices rebounded in Phases B and C, Binance balances increased significantly. Offshore spot holders replenished inventory, increasing potential selling pressure.

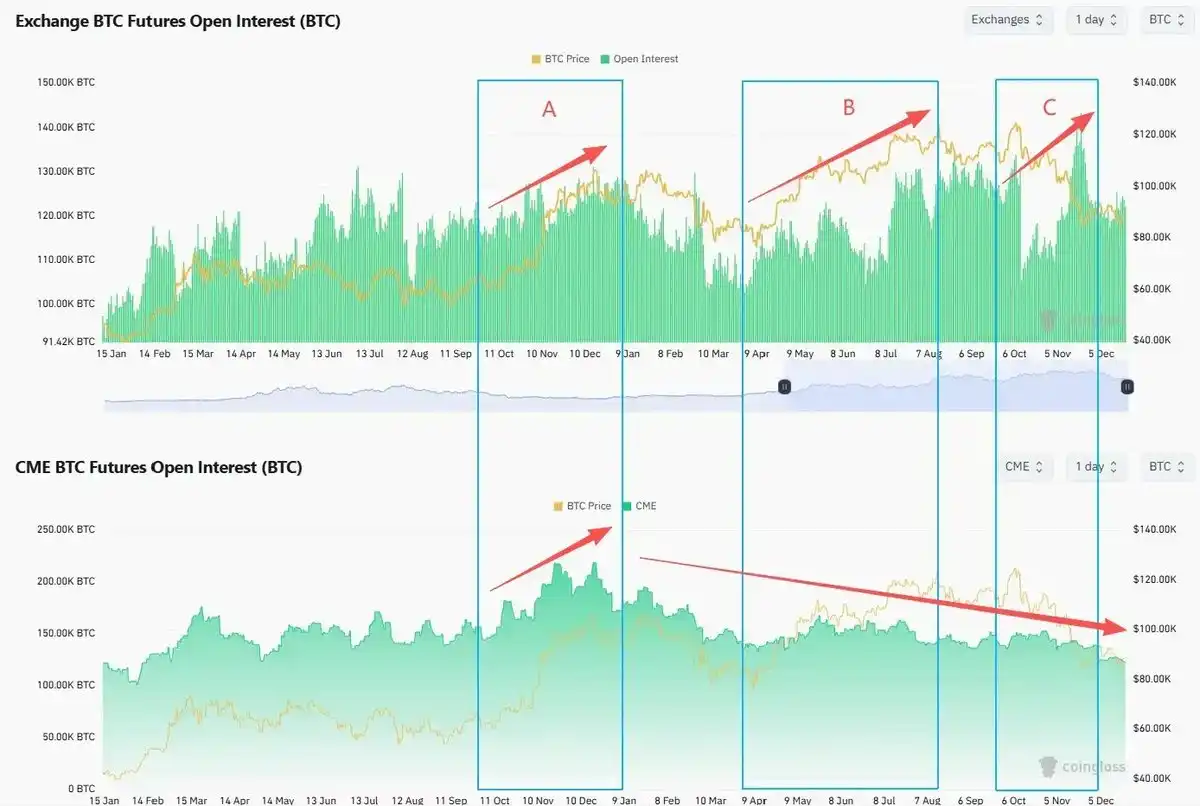

Futures: Offshore leverage rises, onshore positions decline

Offshore open interest (Binance and other offshore exchanges) climbed during Phases B and C. Leverage increased. Even after October 10th, leverage quickly recovered and returned to or exceeded previous peaks.

Onshore open interest (CME) has been on a downward trend since early 2025. Institutional investors did not increase their risk exposure as contracts hit new highs.

Meanwhile, Bitcoin volatility diverged from price action.

In August 2025, when Bitcoin's price first surpassed $120,000, DVOL was near a local low. The options market did not adequately compensate for continued risk.

Each "top" seemed to reflect a divergence between onshore and offshore traders. When onshore spot funds pushed prices to break out, offshore spot traders sold into strength. When offshore leveraged capital chased the rally, onshore futures and options traders reduced positions and stayed on the sidelines.

Where are the marginal buyers? Who is left to buy?

Glassnode estimates that the number of Bitcoins held by corporate and DAT-like tools increased from about 197,000 in early 2023 to about 1.08 million by the end of 2025, a net increase of about 890,000 over two years. DATs have become one of the largest structural investment vehicles in the Bitcoin system.

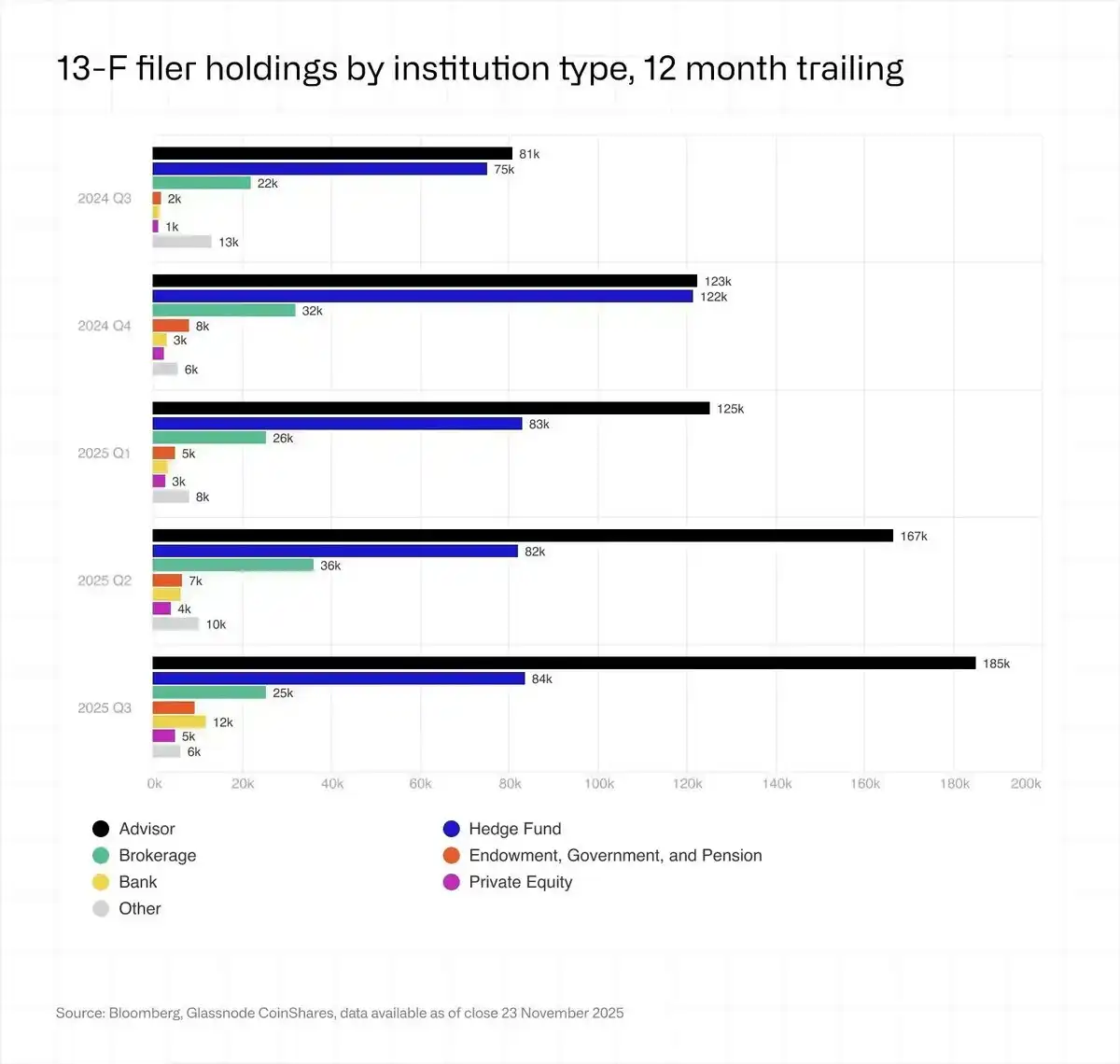

Another often misunderstood area is ETFs. By the end of 2025, U.S. spot Bitcoin ETFs held approximately 1.36 million, a year-on-year increase of about 23%, accounting for about 6.8% of the circulating supply.

Institutional investors (13F filers) hold less than a quarter of the total ETF amount, and most of these are hedge funds and investment advisors, clearly not the "diamond hand" families we know.

The Death of Retail

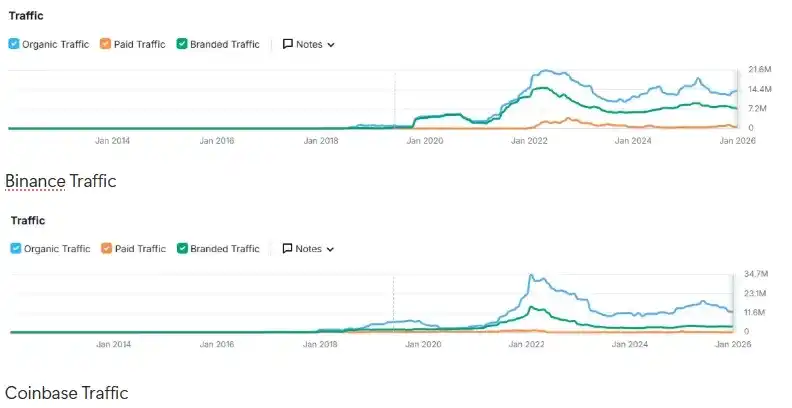

Since early 2025, flow data from Binance, Coinbase, and other top exchanges clearly shows that retail investor weakness has continued since Trump sold his "memecoins".

Furthermore, overall social sentiment among retail investors has actually been bearish since early 2024.

Overall website traffic has been on a downward trend since peaking in 2021.

Bitcoin's price hitting new highs did not bring traffic back to previous levels.

You can read more on this topic in our article from last year. "Who is the marginal buyer?"

Exchange strategies have also adjusted. Facing high customer acquisition costs and low activity from existing users, exchanges have shifted from "striving for growth" to "retaining existing capital through yield products and multi-asset trading (actively listing U.S. stocks, gold, and forex)".

Everywhere Else, It's a Bull Market

The real "wealth effect" in 2025 was not in crypto: the S&P 500 (+18%), Nasdaq (+22%), Nikkei (+27%), Hang Seng Index (+30%), KOSPI (+75%), and even A-shares rose 19%, all posting strong gains. Gold (+70%) and silver (+144%) also surged, making "digital gold" seem somewhat ridiculous by comparison.

AI stocks, 0DTE (zero-day to expiration) options, and commodities like gold and silver further eroded its appeal.

Speculative money did not rotate into alternative investments. Many exited altogether, returning to equity volatility markets, while new speculators happily profited in U.S. stocks or their domestic equity markets.

Even Korean retail investors sold off Upbit to bet on the KOSPI index and U.S. stocks: Upbit's average daily trading volume in 2025 fell about 80% compared to 2024. During the same period, the KOSPI rose over 75%. Korean retail investors net bought about $31 billion in U.S. stocks.

Who Are the Biggest Sellers?

Every cycle has whales selling at local highs, but interestingly, the timing of seller distribution this cycle coincided perfectly with the RSI divergence points.

Bitcoin had previously moved closely in line with U.S. tech stocks until around August 2025, when Bitcoin began to significantly lag ARKK and Nvidia, followed by the October 10th flash crash, and it has yet to close the gap since.

Just before this divergence appeared, in late July, Galaxy disclosed in its earnings report and media briefings that it had executed a sell order of over 80,000 Bitcoins on behalf of an established holder. This transaction brought the phenomenon of "Satoshi-era whale profit-taking" into public view.

Miners Selling for AI Capex

From the 2024 Bitcoin halving to the end of 2025, miner reserves experienced their most sustained decline since 2021. By year-end, reserves were around 1.806 million Bitcoins. Hash rate fell about 15% year-on-year.

-

Under the "AI Diversion Plan," miners transferred approximately $5.6 billion worth of Bitcoin to exchanges to fund the construction of AI data centers.

-

Bitfarms, Hut 8, Cipher, Iren, and others are converting sites into AI and high-performance computing campuses, signing 10 to 15-year compute contracts, treating power and land as "gold in the AI era."

-

Riot, a representative HODLer, announced in April 2025 that it would begin selling all coins mined monthly.

It is estimated that by the end of 2027, about 20% of mining power capacity could be redeployed to AI workloads.

China took more severe measures. In December 2025, Xinjiang again became a target for the People's Bank of China and various ministries. About 400,000 ASIC miners were forced offline, causing global hash rate to drop 8% to 10% in a few days.

Gray Whales: Bitcoin's Black Hangover

Similar to the significant impact of the PlusToken scam in the 2021 cycle, several large-scale fraud and gambling cases in 2025, including Qian Zhimin's Ponzi scheme/cult network and the Cambodia Prince Group/Chen Zhi case, were likely major behind-the-scenes drivers of Bitcoin's price action.

Both cases involved the seizure of tens of thousands of Bitcoins, totaling at or above the level of 100,000 black coins.

This may also add potential selling pressure from governments, while significantly inhibiting large gray market long-term holders of Bitcoin, which could create selling pressure in the medium term but is overall positive in the long run.

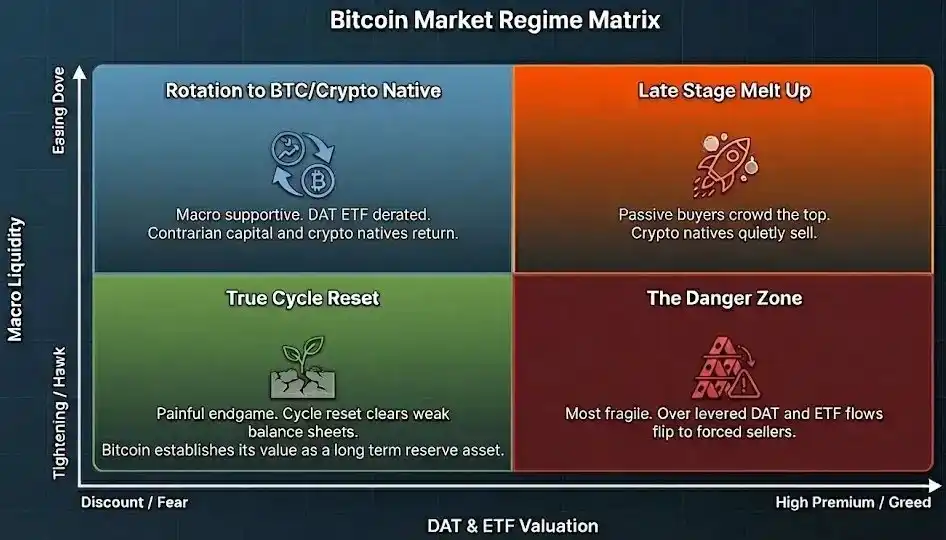

2026 Outlook

Under this new structure, the original "four-year halving cycle" is no longer a feasible self-fulfilling path.

The next phase of the regime is primarily driven by two axes.

-

Vertical: Macro liquidity and credit conditions, interest rates, fiscal stance, AI investment cycle.

-

Horizontal: Valuation and premium levels of DATs, ETFs, and other Bitcoin alternative assets.

Early Bitcoin winners, including OGs, miners, and Asian gray whales, are distributing tokens to passive ETF holders, DAT structures, and long-term national capital.

Bitcoin's trajectory seems similar to that of FAANG between 2013 and 2020: the market is slowly shifting from a high-beta strategy dominated by early retail and growth funds to a passive allocation strategy dominated by index funds, pension funds, and sovereign wealth funds.

Bitcoin is now the crypto asset you can own easily without touching crypto. You can buy it through a brokerage account, custody it like an ETF, account for it clearly, and explain it to a trader investment committee in five sentences.

Whereas the valuation of most other crypto assets does not stem from their actual utility or legitimacy in the physical market and Wall Street.

We always look forward to the next bull market, but it would be great if this bull market wasn't just about price increases, but also about utility increases, translating the legitimacy of the ETF era into on-chain demand, converting passive holding into active use, and bringing real yield returns, not just constantly shifting narratives.

If that happens, today's "bag holders" won't look like fools trapped at the cycle's peak, but rather like the first investors of the new cycle.

Bitcoin finally becomes national reserve currency

Code is eating the bank

Crypto still needs to evolve into a new tool of civilization.