Written by: Yash Roy, Bloomberg

Compiled by: Saoirse, Foresight News

This is an advertisement placed by the American prediction market platform Kalshi at a Washington bus stop in March. With the slogan 'We Don't Do Death Markets,' it emphasizes its own federally regulated compliance to attack its competitor Polymarket's unregulated overseas operations and sensitive contracts related to military conflicts. Photographer: Daniel Hoyle / Bloomberg

As competition in the prediction market industry intensifies and this emerging field faces strict regulatory scrutiny in Washington, Kalshi and Polymarket are exchanging heavy accusations in a fierce confrontation.

The two platforms have frequently clashed before, but recent conflicts have escalated completely — Kalshi launched a highly targeted advertising campaign, and its employees have publicly criticized Polymarket, with the rhetoric from both sides becoming increasingly heated.

Benjamin Freeman, who is responsible for political and election markets at Kalshi, posted on social media on Monday, stating: 'Polymarket's irresponsible, dangerous, and allegedly违规的行为 (non-compliant behavior) is threatening the survival of legitimate prediction markets in the United States.'

This accusation quickly sparked a fierce war of words between the two companies.

Polymarket responded in a statement: 'We welcome competition but believe discussions should be based on facts. Misleading the public only harms the entire industry and its participants.'

Kalshi spokesperson Elisabeth Diana directly retorted: 'It's laughable to hear this from a company whose vast majority of trading volume is on an unregulated overseas platform, with rules that even allow for 'death markets'.'

(Note: Death Markets is a general term in the prediction market industry for trading contracts that directly/indirectly bet on events related to death, military conflicts, assassinations, etc., also known as 'assassination markets.')

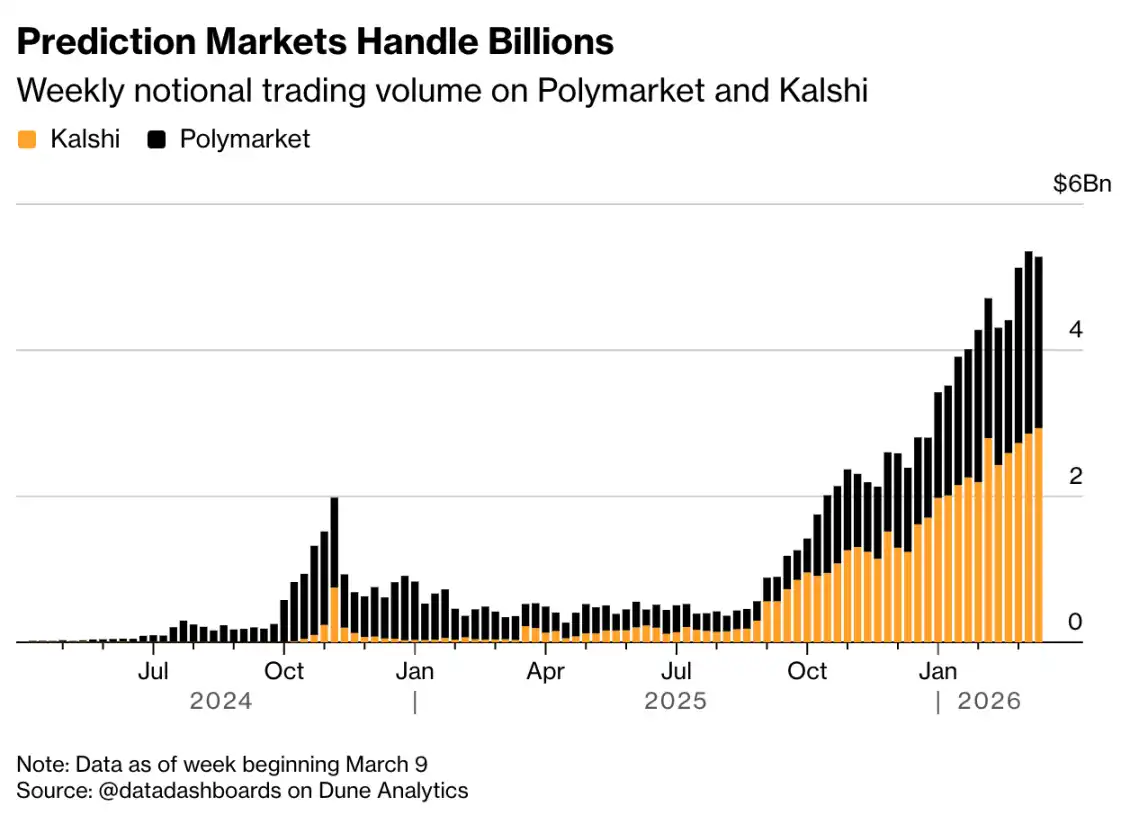

This internal strife erupts at a critical time when Polymarket and Kalshi are vying for the leading position in the rapidly growing prediction market industry. This industry provides Americans with a new way to bet on various events, from sports games to election outcomes. According to data compiled by a user on Dune Analytics, the two startups have recently set new records in weekly trading volume, with their combined nominal trading volume recently approaching $6 billion.

Prediction Market Trading Volume Reaches Billions

Weekly nominal trading volume of Polymarket and Kalshi. Note: Data is for the week ending March 9th. Source: @datadashboards on Dune Analytics

The core of the dispute lies in the fundamental differences in the establishment models and operating rules of the trading platforms. The Kalshi platform is headquartered in the United States and is regulated by the U.S. Commodity Futures Trading Commission (CFTC); Polymarket's main trading platform is based overseas.

Polymarket leverages its overseas operational advantage to list contracts related to military conflicts, including those involving Iran. Kalshi directly states that such products are both unethical and illegal.

One of Kalshi's advertisements bluntly states: 'We Don't Do Death Markets.'

Earlier this week, this set of marketing ads from Kalshi, in the form of a 'platform rules list,' began appearing at bus stops and subway stations in Washington.

One of them reads: 'Rule 1: We ban insider trading because Kalshi is a federally regulated U.S. exchange.' In the eyes of industry observers, the subtext of this statement is obvious: Polymarket's main platform is not under the jurisdiction of U.S. regulators.

'BETS OFF Act' signage, Representative Greg Casar and Senator Chris Murphy speak at a press conference regarding the 'Betting on Events with Security and Federal Functions Off-Limits (BETS OFF) Act'. Photographer: Stephanie Reynolds / Bloomberg

Following allegations that insider information was used to improperly bet on U.S. military actions in Iran and Venezuela, Congress has turned its focus to the issue of insider trading in prediction markets. In response, Kalshi has taken a tougher stance, imposing fines, suspending trading, and other penalties on users it deems to have violated rules; Polymarket has been relatively permissive, though with increased regulatory attention, the platform recently announced its own insider trading rules.

Kalshi spokesperson Diana said: 'We want to make these significant differences clear. Many people in the market currently conflate Kalshi and Polymarket and confuse the different paths we have taken regarding regulatory compliance.'

In addition to its overseas main platform, Polymarket also has a U.S.-regulated platform, which is still in the testing phase. The company stated in a declaration that both platforms enforce 'the same strict market integrity standards, including prohibitions on insider trading and market manipulation, active monitoring of trading, and ongoing communication and cooperation with regulators and law enforcement agencies.'

A trade on the Polymarket website regarding whether the Houthis will attack Israeli territory. Photographer: Gabby Jones / Bloomberg

Just a few months ago, Kalshi co-founder Luana Lopes Lara was still trying to ease tensions between the two rivals. In a social media post last October, she expressed hope that the industry could move beyond 'destructive infighting' and develop together.

Now, that vision seems largely shattered.

The conflict became even more difficult to reconcile after Kalshi advisor and former U.S. Commodity Futures Trading Commissioner Brian Quintenz joined the fray. In response to reports that prosecutors are investigating insider trading, Brian Quintenz publicly hinted on social media this week that the investigation should focus on Polymarket. When contacted by Bloomberg News, he declined to comment further.