Original | Odaily Planet Daily (@OdailyChina)

Author | Asher(@Asher_ 0210)

TGE Repeatedly Delayed, Leading to a Continuous Drop in OTC Points Price

Another $20 Million Funding Round in February Made Opinion One of the Most Anticipated Airdrops of 2026

The rising narrative around prediction markets garnered significant attention for Opinion even before its TGE. Combined with top-tier VC backing and deep integration with the Binance ecosystem, the market once regarded it as one of the most anticipated airdrop projects of 2026.

In terms of funding, Opinion completed two rounds, raising over $25 million in total. In March 2024, the project was selected for the 7th season of Yzi Labs' MVB accelerator program, becoming one of 13 early-stage projects. In March 2025, Opinion completed a $5 million seed round led by Yzi Labs, with participation from Echo, Animoca Ventures, Manifold Trading, Amber Group, and others. By February 2026, Opinion announced another $20 million Pre-Series A funding round, co-led by Hack VC and Jump Crypto, with participation from Primitive Ventures, Decasonic, Continue Fund, and others.

Continuous support from several leading institutions led to higher market expectations for the airdrop scale and potential valuation.

TGE Was Originally Scheduled Before Chinese New Year But Repeatedly Postponed Due to Market Conditions

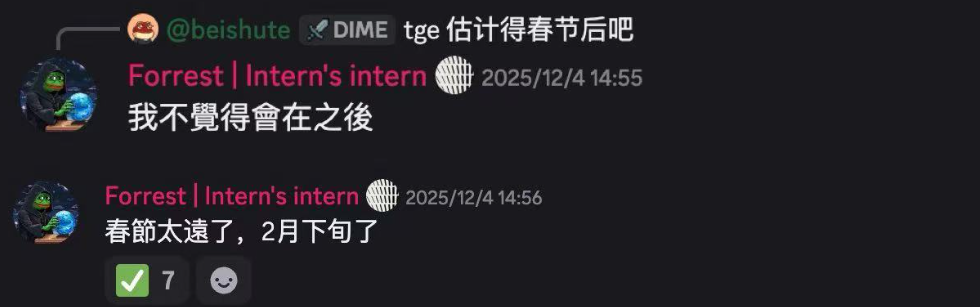

In December 2025, Opinion founder Forrest stated in the official Discord that the project's TGE was expected before the Chinese New Year. This quickly ignited community sentiment, with many users starting to "work overtime" to farm points and frequently participate in various prediction events to boost trading volume. As point farming became more competitive, some users' farming costs even exceeded $20 per point, all to accumulate more points before the TGE, hoping to snag the first "big airdrop" of 2026.

Opinion founder previously stated TGE would occur before Chinese New Year

However, entering February, the overall crypto market experienced a significant correction, and Opinion's TGE timeline became uncertain. The TGE, originally anticipated before the New Year, had no news, causing market expectations for the points to cool. Although Binance launched the Opinion-related Binance Wallet Booster and Alpha airdrop activities on February 4th, the official team still did not announce a clear TGE schedule. As expectations gradually cooled, the OTC price of Opinion points also fell from a high of about $45 per point to around $20 per point.

As the TGE was repeatedly delayed, community sentiment gradually turned negative. Some users began questioning the project's progress in community groups, but in the official Discord, any obvious negative comments often led to the swift removal of the involved members. Some dissatisfied users even went to other prediction market project communities, such as predict.fun, to continue venting their frustrations about Opinion's various issues.

Opinion community members complaining in other prediction market project communities

Repeated TGE delays, continuous point dilution, and arbitrary kicking of members from the official community led to accumulating dissatisfaction within the Opinion community. Points kept increasing, fees kept being paid, but the answers to when the project would TGE and what it would ultimately be worth became increasingly elusive.

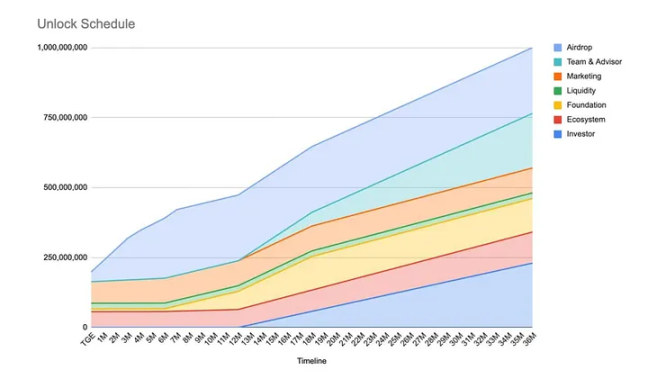

Airdrop Allocation Sparks Controversy: Only 3.5% of TGE Airdrop Unlocked, Marketing Allocation Unlocks a High 7.7%

After Tokenomics Revealed, Point Price Plunged to $6

On the evening of March 2nd, the Opinion Foundation officially announced the tokenomics of its native token OPN. The total supply of OPN is 1 billion tokens, with the airdrop accounting for 23.5% (235 million tokens). At first glance, this proportion is not low compared to current crypto projects.

However, the actual unlock ratio at TGE sparked controversy. Of the total airdrop allocation, only 3.5% (35 million tokens) were released on TGE day, with the remaining portion to be linearly released over 7 months. This means that for the vast majority of users who farmed points for the airdrop, the number of tokens actually received on TGE day was far lower than previous market expectations.

What further displeased the community was the unlock ratio of other allocation parts. According to the official token distribution, the Marketing portion accounts for 8.9%, but 7.7% is released at TGE, significantly higher than the airdrop release ratio. In comparison, users who participated in early interactions and contributed trading volume only received 3.5% at TGE.

This comparison quickly sparked controversy within the community—early interactive users contributing trading volume received a minimal share at TGE, while the related marketing share received a higher proportion of unlocks at launch. Simultaneously, Binance Launchpool directly received 2% of the token supply, further intensifying community dissatisfaction.

At the same time, the internal holding比例 further exacerbated community discontent. According to the token distribution, investors account for 23%, the team and advisors account for 19.5%, and the foundation accounts for 12%, totaling over 54%.

OPN Token Unlock Schedule

After the tokenomics were announced, market expectations quickly changed. Prior to this, OPN points were once quoted at $45 per point on the secondary market. With only 3.5% being airdropped at TGE, the OTC price of Opinion points plummeted, with pre-market quotes quickly falling to $6 per point.

Furthermore, many "airdrop farming whales" spent real money on fees to farm points, only to be flagged as Sybils. According to feedback data from community members, 1 point ultimately corresponded to $6, but many users with high point rankings received an airdrop value even lower than this. KOL Daidaidai Bitcoin posted his loss details on platform X: invested $200,000 to farm points,最终 received 2000 OPN, worth about $1000 at current prices. "200k USD for 2000 tokens. Yes, you read that right." This phrase quickly went viral in the Chinese crypto community.

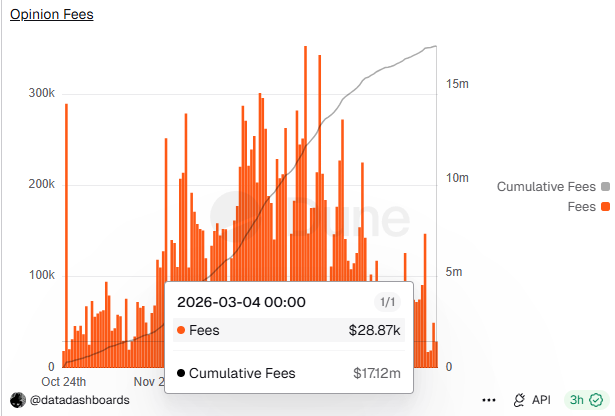

What the community found even more ironic was that according to Dune data, Opinion's cumulative revenue from trading fees over the past months has exceeded $17 million. Calculated at current market prices, the TGE airdrop value is even lower than this figure.

Opinion's cumulative fee revenue exceeds $17 million

Summary

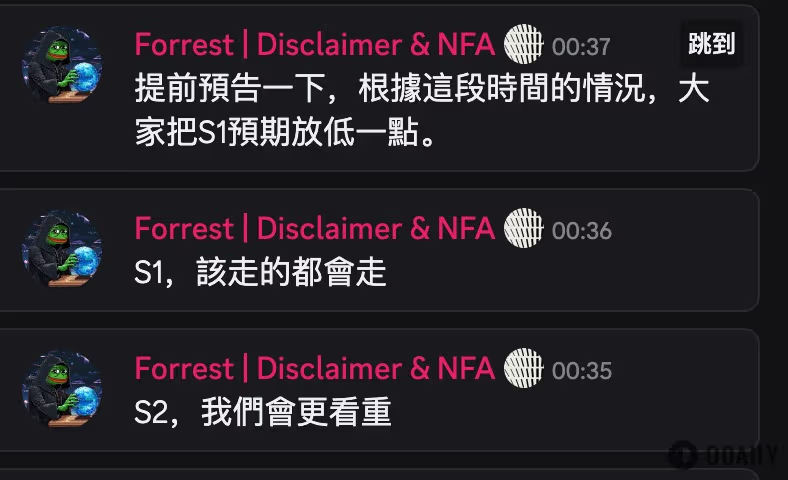

From "the most anticipated airdrop of 2026" to being joked about by the community as "almost entirely flipped," Opinion's plot twist took only a few months. Although Opinion founder Forrest recently stated that more emphasis would be placed on Season 2 rewards, for many early participants, the Season 1 airdrop result has severely透支 trust.

Opinion founder emphasizes greater focus on S2 rewards

This sentiment was quickly reflected in user behavior. More and more participants chose to reduce or even stop trading on the platform, and on-chain data showed a significant subsequent decline. Platform TVL plummeted from about $150 million to $36 million, and trading volume dropped from $150 million to about $15 million, indicating a clear cooling off in user activity.

Against this backdrop, the controversy surrounding Opinion is more than just an airdrop incident. As one of the most watched prediction market projects in the BNB Chain ecosystem, this event has also had a significant impact on the entire sector.

After this storm, can the BNB Chain ecosystem still produce new prediction market platforms?