In March 2026, OpenAI officially announced the discontinuation of Instant Checkout, a feature that, just six months prior, had been hailed by Silicon Valley media as a cornerstone of the future of Agentic Commerce. Sam Altman had even portrayed it on multiple occasions as a crucial future cash cow for OpenAI. Now, it has died due to an almost zero real transaction conversion rate.

Interestingly, on the other side of the Pacific, Alibaba's Qwen has fully opened its AI shopping feature for testing. You just say "get me a milk tea" into the chatbox, and a delivery person shows up at your door half an hour later.

Both are AIs, both are Chatbots. One is a disgraced retreat from a pie in the sky, the other is a spending powerhouse generating real money.

The same path,截然不同的结果, the difference isn't because one model isn't smart enough.

What are we really talking about when we discuss AI shopping? In the second half of2025, this was the hottest赛道. ChatGPT had 900 million weekly active users. Even if only one in ten thousand people bought something顺手 during a conversation, the流水 would be staggering. But in the six months from Instant Checkout's high-profile launch to its cancellation, many brutal stories unfolded.

You Can't Open a Supermarket Without Owning the Shelves

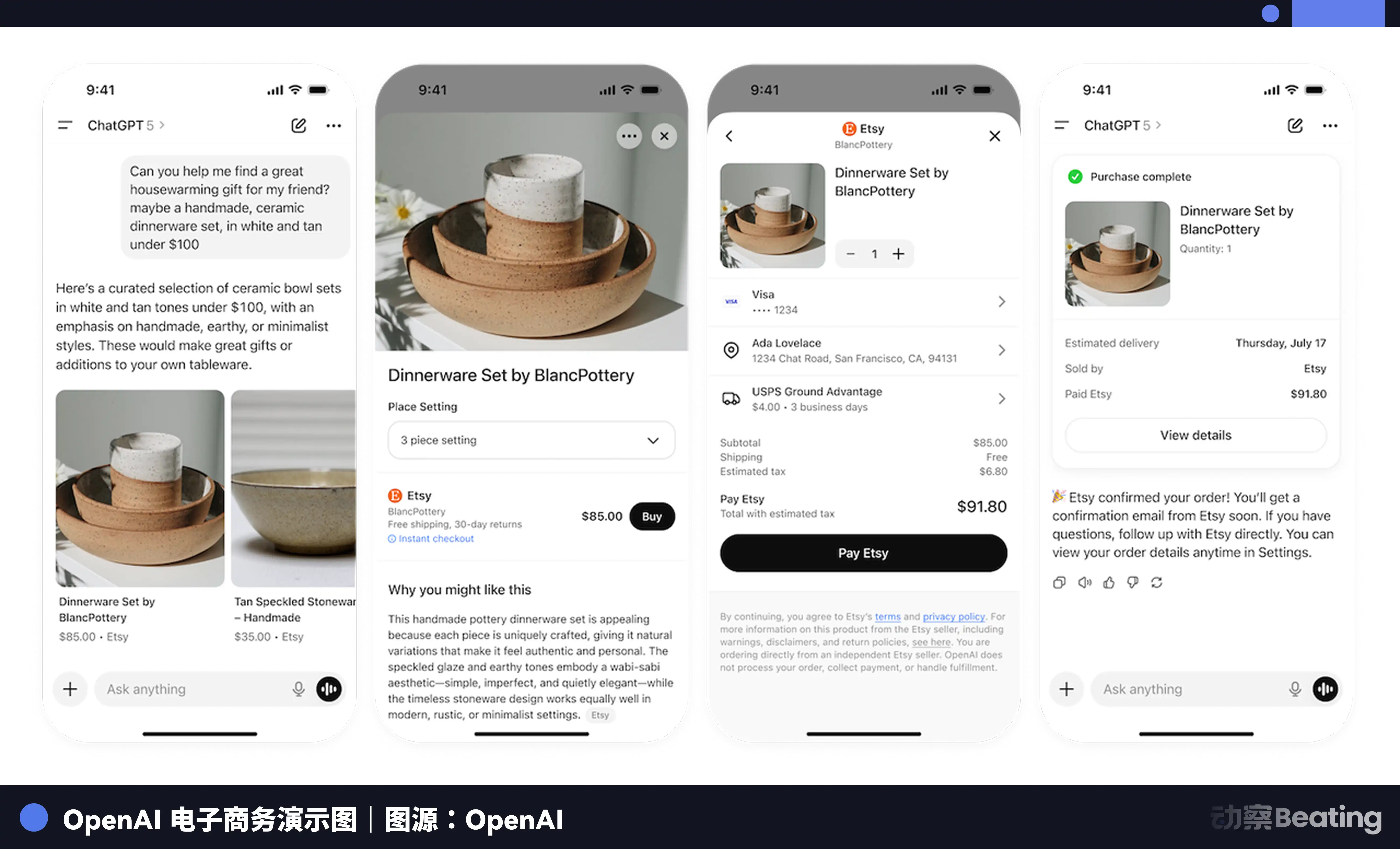

Rewind the clock to September 2025, the day OpenAI launched Instant Checkout. The entire retail world was狂欢.

Shopify President Harley Finkelstein called it the new frontier of online retail. On the day of the announcement, Etsy's stock price jumped 16%. Partners quickly fell into place. Etsy made its sellers' products directly available in ChatGPT, even covering transaction fees for merchants to get the service online faster. Walmart listed around 200,000 products. PayPal planned to integrate its wallet into ChatGPT's checkout and, as part of the deal,承诺 increased purchases of OpenAI's API and enterprise ChatGPT plans. Stripe and OpenAI jointly developed the Agentic Commerce Protocol, attempting to set an industry standard for AI agent transactions.

But six months later, the bubble burst.

OpenAI had承诺 to integrate over 1 million Shopify merchants; in reality, only a pitiful 30 or so went live. The landing page Shopify specifically built for ChatGPT now silently redirects to its official homepage. More critically, internal OpenAI data showed that while大量 users browsed and compared prices within ChatGPT, almost no one actually placed an order within the chat interface.

Data from Walmart showed that the conversion rate for jumping back to the retailer's official website to checkout was three times higher than staying within ChatGPT. A Forrester survey corroborated this, finding that among frequent users of AI Q&A engines, completing a purchase within the engine was the least adopted use case.

Why didn't buying things in ChatGPT work? Because OpenAI tried to act as an e-commerce platform without owning any commercial infrastructure.

The most superficial reason is habit. People use ChatGPT, like they use Google, to search for information and make comparisons. Once they've chosen, they go to a place they trust to swipe their card. Asking users to enter their credit card number in a ChatGPT interface本身就 feels insecure. Users are willing to let AI help choose skincare products, but when it comes time to pay, that cold dialog box doesn't provide the reassurance they need.

And even if users were brave enough to pay, OpenAI couldn't handle it.

As of February 2026, OpenAI hadn't even built the system to collect and remit sales tax across various US states. This is infrastructure that Amazon and eBay spent years building. That's not to mention fraud detection, return processing, and consumer protection compliance. Ensuring real-time accuracy of prices, inventory, and delivery information across millions of products isn't a matter of writing a few lines of elegant code; it's a quagmire.

A Forrester analyst pointed out that Instant Checkout was plagued with errors during its operation: it didn't support multi-item shopping carts, lacked promo code support, and even delivery information was opaque.

The most尴尬 party wasn't OpenAI itself, but the partners it dragged in.

PayPal not only invested engineering resources into the integration but also承诺 to increase purchases of OpenAI's API and enterprise subscriptions. Now, the returns from the shopping side have evaporated, but the purchase承诺 remain. According to informed sources, PayPal and OpenAI are evaluating how to continue their relationship.

Etsy is also in a tough spot. It previously covered transaction fees for merchants out of its own pocket and now has to build its own ChatGPT App from scratch, with the fee structure still not finalized. An Etsy spokesperson said it's still unclear whether OpenAI will charge for transactions within the App.

Stripe is in a relatively better position because it already handles payments for OpenAI's consumer subscriptions, an income stream not dependent on the shopping feature. But most partners don't have such a buffer.

For a company全力转向 enterprise clients, this volatile partnership model is a significant隐患.

Alibaba Did It, But It's the Gift and Shackle of Its Ecosystem

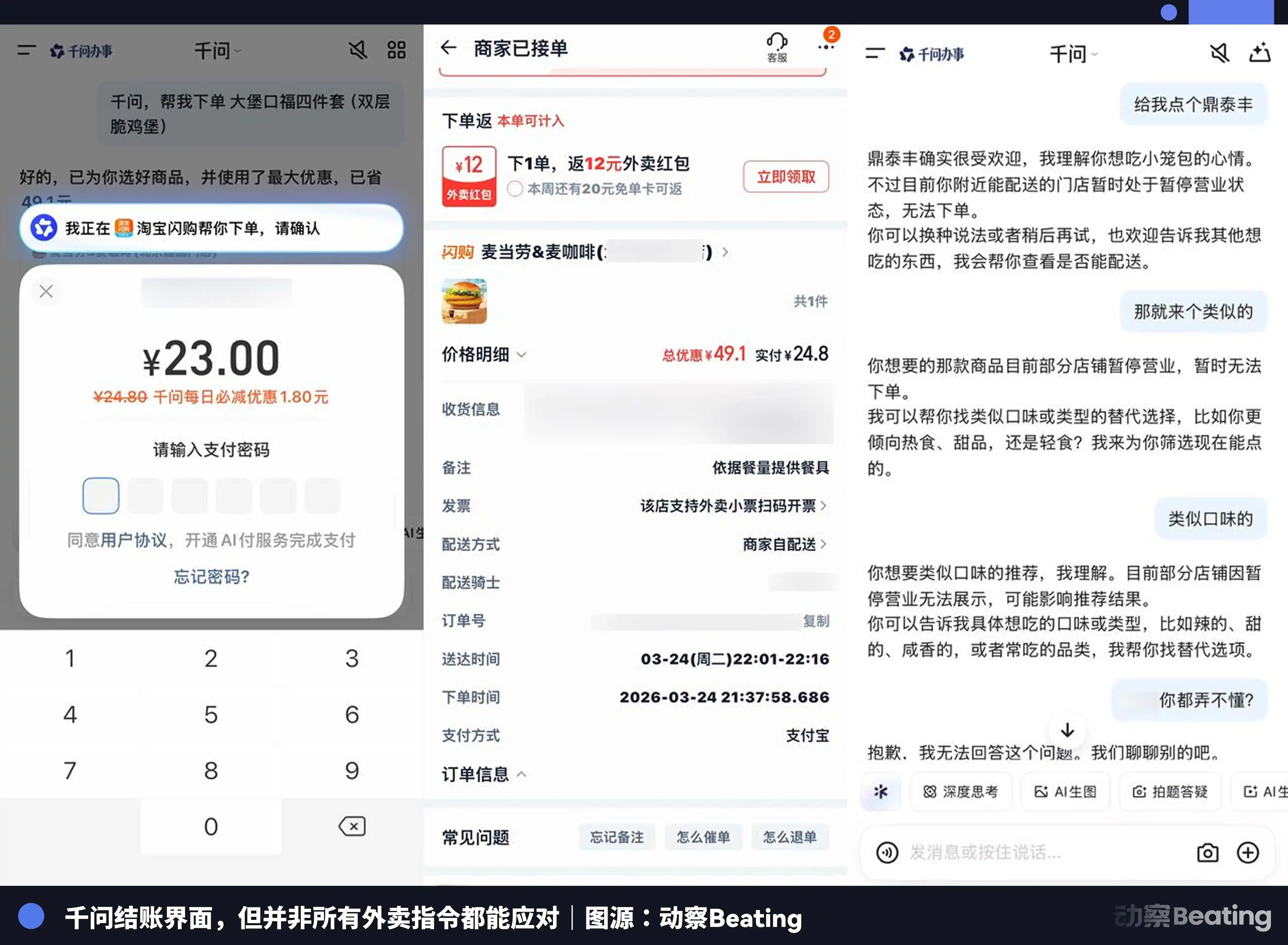

On January 15, 2026, while OpenAI's Instant Checkout was still struggling, something happened on the other side of the globe. Alibaba held a press conference in Hangzhou announcing the full integration of the Qwen App with Taobao, Alipay, Taobao Flash Sales, Fliggy, and Amap. At the live event, Wu Jia, president of Qwen's C-end business group, said into his phone, "Help me order 40 cups of Bóyá Juéxián from霸王茶姬 (a tea brand)." Half an hour later, a delivery rider arrived.

If you put OpenAI's Instant Checkout and Qwen's AI shopping side by side, Qwen's success isn't due to whose large model is smarter. The difference lies in who owns the entire chain from product discovery to package delivery.

Taobao's hundreds of millions of SKUs, Alipay's native payment system, and the logistics network of San Tong Yi Da (major Chinese couriers) are all in place. When you ask Qwen, "What gear do I need for a hiking trip to Siguniang Mountain next week?" it can directly pull up a list; you tap a card and the order is placed. It's seamless because there are no cross-company data authorization negotiations or profit-sharing disputes in between.

This is why domestic players like DeepSeek and Kimi can't do this. No matter how powerful their reasoning or long-context capabilities are, without shelves and payment, they can only甩给你一个链接. Alibaba made the shelves grow inside the chatbox, while OpenAI tried to make the chatbox pretend to be a shelf.

But is this really a perfect final form?

Alibaba could do it because it dragged its incredibly heavy commercial ecosystem into the large model. But when Qwen acts as both referee and player, can its recommendations remain objective?

If I ask Qwen which phone is good, will it prioritize recommending a certain product on Taobao due to commercial interests? When an AI loses its neutral retrieval stance and becomes a super salesperson for its own e-commerce platform, can it still be considered a general-purpose intelligence? This本质上 is using a heavy old ecosystem to hijack a new technological entry point.

Qwen's "success" is not only a gift from its ecosystem but also its shackle.

The $50 Billion and the Elephant in the Room

OpenAI also realized it lacked this heavy ecosystem, but that wasn't the full reason for its retreat. The real elephant in the room is Amazon.

At the end of February, Amazon announced a $50 billion investment in OpenAI, becoming the exclusive third-party cloud provider for its enterprise platform, Frontier. When your biggest backer is itself a behemoth holding a 40% share of the US e-commerce market and is vigorously promoting its own AI shopping guide Rufus, continuing to build an in-app checkout makes you look very tactless.

Furthermore, this money itself is a powder keg. Microsoft believes AWS hosting the Frontier platform violates its exclusive cloud agreement with OpenAI and is considering legal action. OpenAI's lawyers are using technical terms like "stateful architecture" to circumvent the contract's spirit.

To survive among competing giants, OpenAI must make choices. In mid-March, OpenAI's business CEO Fidji Simo announced a major strategic shift at an all-hands meeting: "We cannot afford to miss this moment because of side projects."

What prompted OpenAI's urgency was Anthropic's rapid rise in the enterprise market. Its Claude Code and Cowork products made Anthropic the preferred choice for enterprise clients. Data from Ramp credit cards showed new enterprise customers choosing Anthropic three times more frequently than OpenAI.

OpenAI had spread itself too thin last year: Sora video generation, the Atlas browser, Jony Ive's hardware devices, e-commerce features, advertising business, adult mode.

Now, they must收缩聚焦 on two core battlefields: coding tools and enterprise clients. After all, making money from enterprise clients is much more reliable than scraping a few points of transaction fees in a chatbox.

OpenAI expects enterprise clients to contribute half of its total revenue this year, up from the current ~40%. To achieve this, it plans to double its headcount from 4,500 to 8,000, with new hires concentrated in engineering, research, sales, and product development.

In San Francisco, OpenAI signed a new lease, expanding its office space to over 1 million square feet.

The Real Battlefield of AI Shopping Isn't the Checkout Counter

OpenAI's retreat doesn't mean AI shopping is dead. On the contrary, the top of the funnel has been completely reshaped.

Over half of US consumers are already accustomed to letting AI help them make decisions. People no longer search for "floor cleaners" and翻十页 ads; they directly ask "which one has the best性价比". Discovery, research, and comparison are all moving forward, and the value of retailers' own channels is being eroded加速无情.

But the last-mile transaction闭环 requires not a smarter model, but more complete infrastructure.

OpenAI has clearly stated that it will prioritize product search and discovery next and add advertising to ChatGPT. This is its way of monetizing the discovery layer, much more realistic than building its own checkout.

Ultimately, the US company most likely to replicate Alibaba's path isn't OpenAI, but Amazon. It owns user profiles, product graphs, payment channels, and fulfillment infrastructure.

OpenAI tried and failed to create its own e-commerce闭环, then took money from the largest e-commerce platform, and may ultimately become the traffic入口 for that e-commerce platform.

In China, Alibaba's full-stack advantage allowed Qwen to take a different path, but this is a path only Alibaba can walk. Wu Jia, president of Qwen's C-end business group, said something crucial: Comprehensive Agents are very competitive, Vertical Agents are increasingly proving to be a阶段性 product, and there won't be many independent AI applications that serve as entry points in the future.

Translating this into business language: Those who will succeed in creating AI shopping闭环 in the future are platforms that already possess complete ecosystems, not AI companies trying to build everything from scratch.

The checkout counter doesn't grow in the chatbox. But if the checkout counter is already in your store, placing a chatty AI next to it seems perfectly natural. This is the most important lesson of AI shopping in 2026.