Tonight will bring the most anticipated interest rate cut decision of the year from the Federal Reserve.

The market widely expects a rate cut to be almost a done deal. However, what will truly determine the direction of risk assets in the coming months is not another 25 basis point cut, but a more critical variable: whether the Fed will restart liquidity injections into the market.

This time, Wall Street is not watching interest rates, but the balance sheet.

According to expectations from institutions like Bank of America, Vanguard, and PineBridge, the Fed may announce this week a plan to initiate a $45 billion monthly short-term bond purchase program starting January next year, as a new round of "reserve management operations." In other words, this suggests the Fed might be quietly ushering in an era of "stealth balance sheet expansion," allowing the market to enter a state of liquidity easing even before the rate cut.

But what makes the market nervous is the backdrop against which this is happening—the U.S. is entering an unprecedented period of monetary power restructuring.

Trump is taking over the Fed in a manner far faster, deeper, and more thorough than anyone expected. It's not just about replacing the chair; it's about redrawing the boundaries of power within the monetary system, reclaiming authority over long-term interest rates, liquidity, and the balance sheet from the Fed and handing it back to the Treasury. The independence of the central bank, long considered an "iron law of the system" for decades, is being quietly eroded.

This is also why all seemingly disparate events—from Fed rate cut expectations to ETF fund flows, from MicroStrategy's and Tom Lee's contrarian accumulation, and so on—are actually converging on the same underlying logic: the U.S. is entering a "fiscally dominated monetary era."

And what impact will this have on the crypto market?

MicroStrategy and Others Are Making Their Move

Over the past two weeks, the entire market has been debating the same question: Will MicroStrategy be able to withstand this downturn? Bears have simulated various scenarios of the company's collapse.

But Saylor clearly thinks otherwise.

Last week, MicroStrategy increased its Bitcoin holdings by approximately $963 million, to be precise, 10,624 BTC. This is his largest purchase in recent months, even exceeding the sum of his acquisitions over the past three months.

Consider this: the market had been speculating whether MicroStrategy would be forced to sell coins to avoid systemic risk when its mNAV approached 1. Instead, when the price nearly hit that level, he didn't sell; he doubled down, and on such a large scale.

Meanwhile, a similarly dramatic contrarian move was playing out on the ETH side. Tom Lee's BitMine, despite ETH's price plunge and a 60% drawdown in the company's market cap, managed to continuously tap the ATM (at-the-market offering), raising substantial cash, and last week bought $429 million worth of ETH in one go, pushing its holdings to a $12 billion scale.

Even though BMNR's stock price has fallen more than 60% from its high, the team can still consistently raise money through ATM offerings and keep buying.

CoinDesk analyst James Van Straten put it more bluntly on X: "MSTR can raise $1 billion in a week, while in 2020, it took them four months to do the same. The exponential trend continues."

If we look at market cap impact, Tom Lee's move is even "heavier" than Saylor's. BTC's market cap is five times that of ETH, so Tom Lee's $429 million buy order has the "double impact" in weight equivalent to Saylor buying $1 billion worth of BTC.

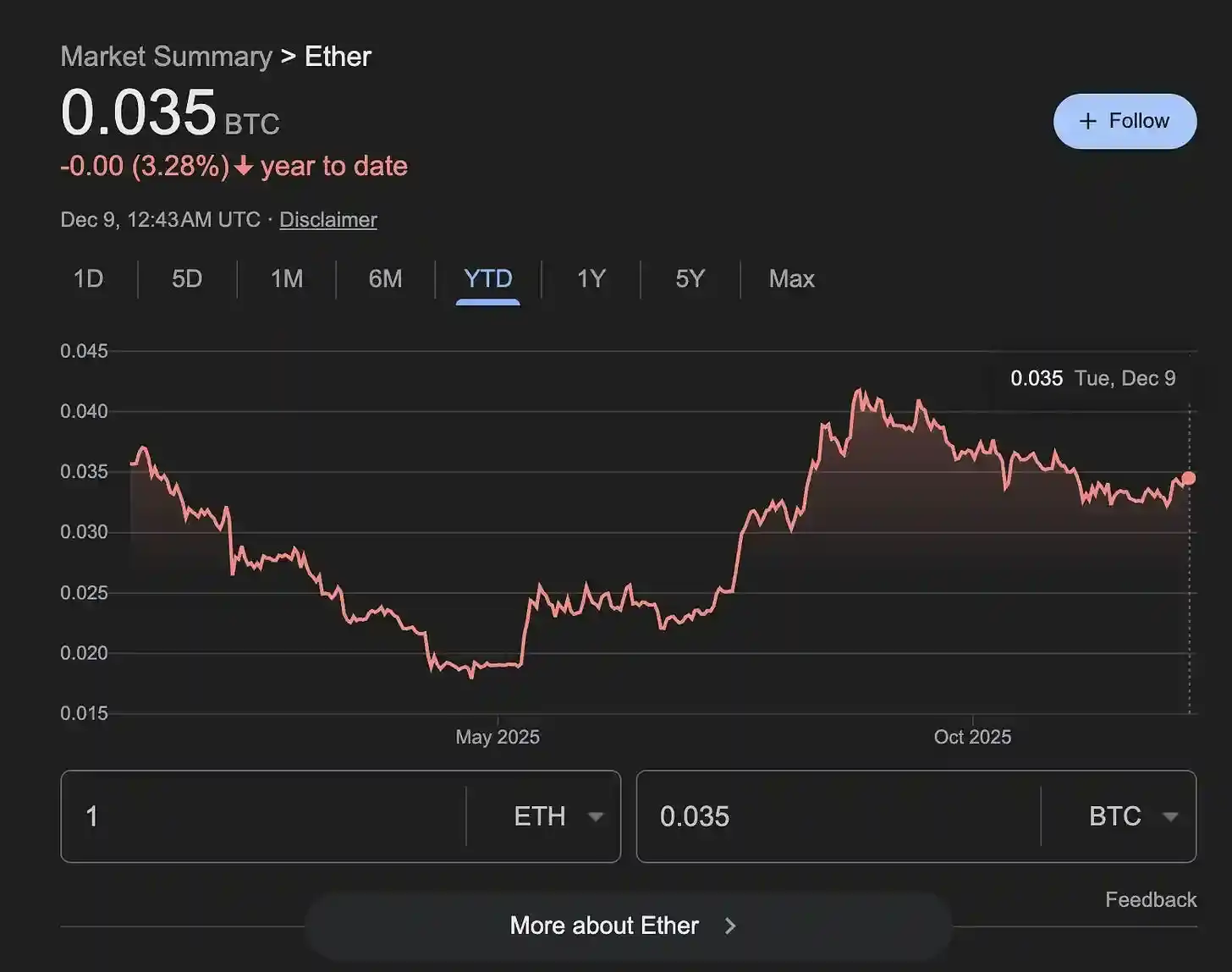

No wonder the ETH/BTC ratio has started to rebound, breaking a three-month downtrend. History has repeated this countless times: whenever ETH leads the recovery, the market enters a brief but fierce "altcoin rebound window."

BitMine now holds $1 billion in cash, and ETH's pullback zone happens to be the perfect place to significantly lower its average cost. In a market where funding is generally tight, institutions that can keep firing are themselves part of the price structure.

ETF Outflows Are Not Flight, But Temporary Withdrawal of Arbitrage Capital

On the surface, Bitcoin ETFs have seen nearly $4 billion in outflows over the past two months, with the price dropping from $125,000 to $80,000, leading the market to quickly draw a crude conclusion: institutions are retreating, ETF investors are panicking, the bull market structure is broken.

But Amberdata offers a completely different explanation.

These outflows are not "value investors fleeing" but "leveraged arbitrage funds being forced to unwind." The primary source is the collapse of a structured arbitrage strategy called the "basis trade." Funds were originally earning a stable spread by "buying spot/shorting futures," but starting in October, the annualized basis fell from 6.6% to 4.4%, spending 93% of the time below the breakeven point, turning arbitrage into losses and forcing the strategy to be dismantled.

This triggered a "two-way action" of ETF selling + futures buybacks.

In traditional terms, capitulation selling typically occurs in extreme emotional environments after continuous declines, where panic peaks, and investors stop trying to cut losses and instead abandon all holdings entirely. Its typical characteristics include: large-scale redemptions across almost all issuers, surging trading volume, cost-indifferent selling pressure, and accompanying extreme sentiment indicators. But this ETF outflow clearly doesn't fit this pattern. Although there were net outflows overall, the direction of funds was inconsistent: for example, Fidelity's FBTC maintained continuous inflows throughout the period, and BlackRock's IBIT even absorbed some incremental funds during the worst phases of net outflows. This shows that the real exodus was only from a minority of issuers, not the entire institutional cohort.

More crucial evidence comes from the distribution of outflows. From October 1 to November 26 (53 days), funds from Grayscale contributed over $900 million in redemptions, accounting for 53% of the total outflow; 21Shares and Grayscale Mini followed closely, together making up nearly ninety percent of the redemption volume. In contrast, BlackRock and Fidelity—the most typical channels for institutional allocation—were net inflows overall. This is completely inconsistent with a true "panic-driven institutional retreat" and looks more like a "localized event."

So, which type of institution was selling? The answer: large funds engaged in basis arbitrage.

The basis trade is essentially a directionally neutral arbitrage structure: funds buy spot Bitcoin (or ETF shares) while shorting futures, profiting from the contango yield. It's a low-risk, low-volatility strategy that attracts significant institutional capital when futures are in contango and funding costs are manageable. However, this model relies on one premise: futures prices must consistently be higher than spot prices, with a stable spread. And starting in October, this premise suddenly disappeared.

According to Amberdata's statistics, the 30-day annualized basis compressed from 6.63% down to 4.46%, with 93% of trading days below the 5% breakeven point required for arbitrage. This meant these trades were no longer profitable, even starting to lose money, forcing funds to exit. The rapid collapse of the basis led to a "systematic unwinding" of arbitrage positions: they had to sell their ETF holdings and simultaneously buy back the futures they had previously shorted to close the arbitrage trade.

This process is clearly visible in market data. The open interest in Bitcoin perpetual contracts fell 37.7% over the same period, a cumulative decrease of over $4.2 billion, with a correlation coefficient of 0.878 to the basis change—almost a synchronous move. This combination of "ETF selling + short covering" is the classic path for basis trade exit; the sudden amplification of ETF outflow规模 was not driven by price panic but was the inevitable result of the arbitrage mechanism collapsing.

In other words, the ETF outflows of the past two months were more like a "liquidation of leveraged arbitrage positions" rather than a "retreat by long-term institutions." It was the unwinding of a highly specialized, structured trade, not panic selling pressure caused by a market sentiment crash.

What's more noteworthy is: after these arbitrage positions are cleared out, the remaining capital structure becomes healthier. Current ETF holdings remain at a high level of approximately 1.43 million Bitcoin, with most shares coming from allocation-oriented institutions, not short-term funds chasing yields. As the leveraged hedging from arbitrageurs is removed, the overall market leverage decreases, there are fewer sources of volatility, and price action will be driven more by "genuine buying and selling forces," not hijacked by forced technical operations.

Amberdata's head of research, Marshall, describes this as a "market reset": after the arbitrage capital retreats, new ETF inflows will be more directional and long-term, structural noise in the market will decrease, and subsequent price movements will more accurately reflect real demand. This means that although it looks like $4 billion flowed out on the surface, it might not be a bad thing for the market itself. On the contrary, it could lay the foundation for the next wave of healthier gains.

If Saylor, Tom Lee, and ETF flows show the attitude of micro-level capital, then the changes happening at the macro level are deeper and more intense. Will the Santa Claus rally come? To find the answer, we might need to look further at the macro picture.

Trump's "Takeover" of the Monetary System

For decades, the Fed's independence has been seen as an "iron law of the system." Monetary power belongs to the central bank, not the White House.

But Trump clearly doesn't agree with this.

Increasing signs show that the Trump team is taking over the Fed in a manner far faster and more thorough than the market expected. It's not just symbolically "replacing the chair with a hawk," but comprehensively rewriting the power distribution between the Fed and the Treasury, changing the balance sheet mechanism, and redefining how the yield curve is priced.

Trump is attempting to restructure the entire monetary system.

Former New York Fed trading desk head Joseph Wang (a long-time researcher of Fed operations) also clearly warned: "The market is clearly underestimating Trump's determination to control the Fed. This change could push the market into a phase of higher risk and higher volatility."

From personnel appointments, policy direction, to technical details, we can see very clear traces.

The most direct evidence comes from personnel arrangements. The Trump camp has placed several key figures in core positions, including Kevin Hassett (former White House economic advisor), James Bessent (key Treasury decision-maker), Dino Miran (fiscal policy智库), and Kevin Warsh (former Fed governor). These individuals share a common trait: they are not traditional "central bank school" and do not insist on central bank independence. Their goal is very clear: to weaken the Fed's monopoly on interest rates, long-term funding costs, and system liquidity, and return more monetary power to the Treasury.

The most symbolic point: it is widely believed that Bessent, considered the most suitable candidate for Fed chair, ultimately chose to remain at the Treasury. The reason is simple: in the new power structure, the Treasury's position can determine the rules of the game more than the Fed chair.

Another important clue comes from changes in term premium.

For the average investor, this indicator might be somewhat unfamiliar, but it is actually the most direct signal for the market to judge "who controls long-term interest rates." Recently, the spread between 12-month and 10-year Treasury yields has approached phase highs again, and this round of increase is not due to an improving economy or rising inflation, but because the market is reassessing: in the future, what determines long-term rates might not be the Fed, but the Treasury.

Yields on the 10-year and 12-month Treasury notes are continuing to fall, meaning the market is strongly betting that the Fed will cut rates, and the pace will be faster and more aggressive than previously expected

SOFR (Secured Overnight Financing Rate) experienced a cliff-like drop in September, meaning U.S. money market rates suddenly collapsed, signaling a significant loosening in the Fed's policy rate system

The initial spread widening was because the market thought Trump would overheat the economy upon taking office; later, when tariffs and large-scale fiscal stimulus were absorbed by the market, the spread quickly retreated. Now the spread is widening again, reflecting not growth expectations, but uncertainty about the Hassett-Bessent system: if in the future the Treasury controls the yield curve by adjusting debt duration, issuing more short-term debt, compressing long-term debt, etc., then traditional methods of judging long-end rates will become completely obsolete.

More subtle but crucial evidence lies in the balance sheet system. The Trump team frequently criticizes the current "ample reserves system" (where the Fed provides reserves to the banking system by expanding its balance sheet, making the financial system highly dependent on the central bank). But at the same time, they clearly know: current reserves are noticeably tight, and the system actually needs balance sheet expansion to maintain stability.

This contradiction of "opposing balance sheet expansion, yet having to expand" is actually a strategy. They use it as a reason to question the Fed's institutional framework and push for transferring more monetary power back to the Treasury. In other words, they don't want to shrink the balance sheet immediately; they want to use the "balance sheet controversy" as a breakthrough to weaken the Fed's institutional standing.

If we piece these actions together, we see a very clear direction: term premium is compressed, U.S. debt duration is shortened, long-end rates gradually lose independence; banks may be required to hold more U.S. debt; government-sponsored agencies may be encouraged to leverage up and buy mortgage bonds; the Treasury may influence the entire yield structure by increasing short-end debt issuance. Key prices once determined by the Fed will gradually be replaced by fiscal tools.

The result of this might be: gold enters a long-term uptrend, stocks maintain a slow grind higher after volatility, and liquidity gradually improves due to fiscal expansion and repo mechanisms. The market will appear chaotic in the short term, but this is only because the power boundaries of the monetary system are being redrawn.

As for Bitcoin, which the crypto market cares about most, it sits on the periphery of this structural change—not the most direct beneficiary, nor will it be the main battlefield. On the positive side, improved liquidity will put a floor under Bitcoin's price; but looking further out 1-2 years, it will still need to go through a period of re-accumulation, waiting for the framework of the new monetary system to truly become clear.

The U.S. is moving from a "central bank-dominated era" to a "fiscally dominated era."

In this new framework, long-term interest rates may no longer be set by the Fed, liquidity will come more from the Treasury, the central bank's independence will be weakened, market volatility will be greater, and risk assets will face a completely different pricing system.

When the foundation of a system is being rewritten, all prices will behave more "illogically" than usual. But this is a necessary phase as the old order loosens and the new order arrives.

The行情 of the coming months will likely be born from this chaos.