Source: X

Author: Noah

Compiled and Edited by: BitpushNews

Core Summary

-

Product Upgrades: On-chain lending will undergo necessary product improvements to better cater to the needs of scaled capital.

-

Demand Release: As functionalities are released, the current low lending rates will induce strong borrowing demand.

-

Capital Inflow: Lending rates will begin to stabilize above the risk-free rate, thereby driving capital inflows.

-

Valuation Return: The sector's valuation multiples are compressing towards Fintech levels, providing a potential entry opportunity for investment next year.

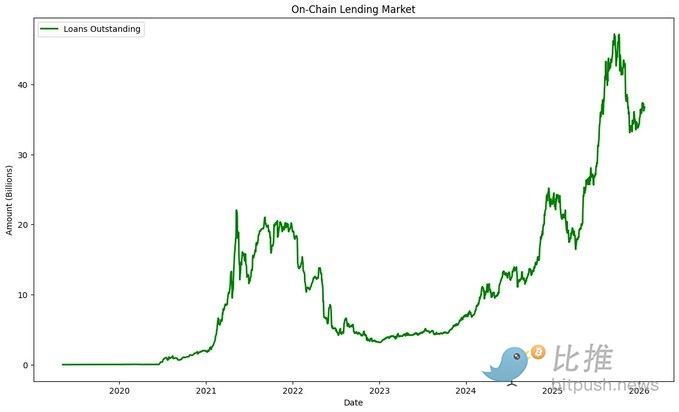

The Cyclical Pattern of On-Chain Lending

Historically, on-chain lending has followed a cyclical behavior with four phases:

-

Low capital in the system, low interest rates.

-

Rising interest rates, capital flows into the system.

-

Due to excess capital, interest rates begin to fall.

-

Due to excessively low rates, capital leaves the system.

Lending protocol token prices tend to follow a similar pattern: prices rise as interest rates increase and capital flows in, and fall as interest rates decrease and capital flows out.

We are currently in the fourth phase. In the past, lending markets could rely on the positive Beta of the crypto market to induce leverage demand, thereby pushing up interest rates; or use token subsidies to stimulate higher yields. Token subsidies worked in highly "reflexive" markets (high price = more subsidies = more platform capital = higher price), but there may no longer be an excess capital base willing to participate in this behavior. I believe most lending protocols are no longer willing to tie their fate to the crypto market's Beta, and subsidies are difficult to scale without increasing costs.

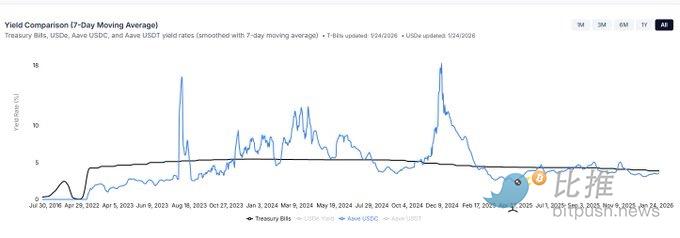

The current issue causing stablecoin lending rates to be below the Secured Overnight Financing Rate (SOFR) is: 1. Insufficient borrowing demand; 2. Capital inefficiencies caused by protocols (such as cash drag from the peer-to-pool model, lack of rehypothecation mechanisms, etc.). Furthermore, on-chain lending rates are significantly lower than most alternative capital sources, a state that is clearly not a long-term equilibrium.

How to Stimulate Lending Demand?

The key to inducing lending demand is to offer a lower price than the alternatives. The current problem is that lending protocols cannot yet provide the collateral asset classes and loan structures that borrowers are accustomed to.

1. Higher Quality Collateral Assets

The security of "monolithic" lending protocols depends on their worst-quality asset, so they tend to be overly conservative when introducing new assets. Currently, almost all protocols are shifting to a modular architecture to allow for higher-risk lending.

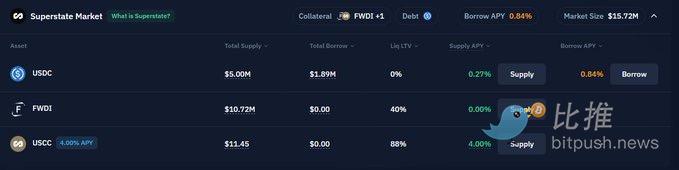

Many traditional collateral assets are currently difficult to obtain on-chain. Securities lending is a multi-trillion dollar market, with settlement rates typically at $SOFR + 75-250$ basis points. Although still in its early stages, we are seeing the beginnings of securities lending, such as Kamino's Superstate market, Aave's Horizon market, and Morpho's curated markets.

2. Protocol Design Improvements

Historically, lending protocols primarily offered floating-rate margin loans for highly liquid crypto assets using a "peer-to-pool" model. This only suits a narrow group of borrowers and imposes a substantial cash drag on lenders due to utilization-based interest rate models.

Kamino, Aave, and Morpho are all releasing upgrades this year to significantly expand loan types. As protocols add features like term loans, address whitelisting, tri-party agreements with compliant custodians, and direct matching, lenders will see spread compression (more of what the borrower pays flows to the lender), and borrowers will gain more flexible loan options.

This will induce borrowing demand, push up interest rates, and subsequently attract capital supply, moving us into "Phase Two" of the lending cycle.

Creating High-Yield Opportunities

High-yield opportunities are crucial for the survival of crypto yield funds. While the market might survive without them, it's better not to take that risk. Historically, on-chain yield funds needed 12-15% returns to justify their existence and raise capital.

Due to the tokenization of basis trades and the increased capital efficiency of CME basis trades, basis yields have been compressed for the foreseeable future. Achieving lending demand above 10% would require an (unpredictable) crypto bull market.

This means funds will be forced to seek opportunities with slightly higher risk but good risk-adjusted returns. The most likely opportunities lie in the entry of tokenized yield products. For example, Figure has already launched tokenized Home Equity Line of Credit (HELOC) with an 8% yield, and yield funds can use revolving leverage on Kamino to achieve returns exceeding their target rate.

2026 may see more equivalents of credit funds being tokenized, offering 8-15% yields. A word of caution: revolving leverage carries risks that are difficult to quantify, and the legal structures of tokenized credit products must be sound.

Conclusion

I believe there is a plausible logic: even if token prices continue to fall, on-chain lending demand can still grow sustainably. While I refrain from commenting on the Beta valuation of the crypto market, if the above logic holds, protocol valuations will become very reasonable at some point in 2026.

Data Calculation:

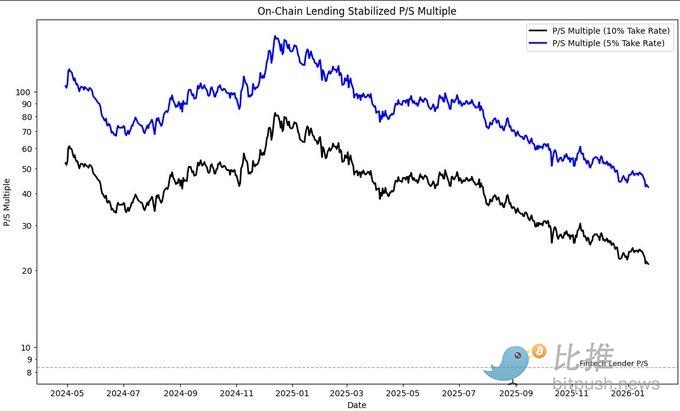

Assuming on-chain lending companies extract 5-10% of interest as revenue, with an average interest rate of 6.5%. The current Price/Sales (P/S) multiple for the sector is 21x to 42x, while listed Fintech lending companies are around 8.4x.

While the nuances between the two are not worth debating, you must be optimistic about on-chain lending over the next two years for the current valuation multiples to seem reasonable. Even so, these multiples are compressing rapidly due to falling token prices and growth in Key Performance Indicators (KPIs).

I believe 2026 will be an opportunity to "swing big" in this sector. Although short-term growth may be slow due to falling crypto asset prices, the upcoming fundamental catalysts could provide another inflection point for on-chain lending activity, with greater sustainability.