Author: David, Shenchao TechFlow

There aren't many projects worth mentioning in this downturn, but Hyperliquid is one of them.

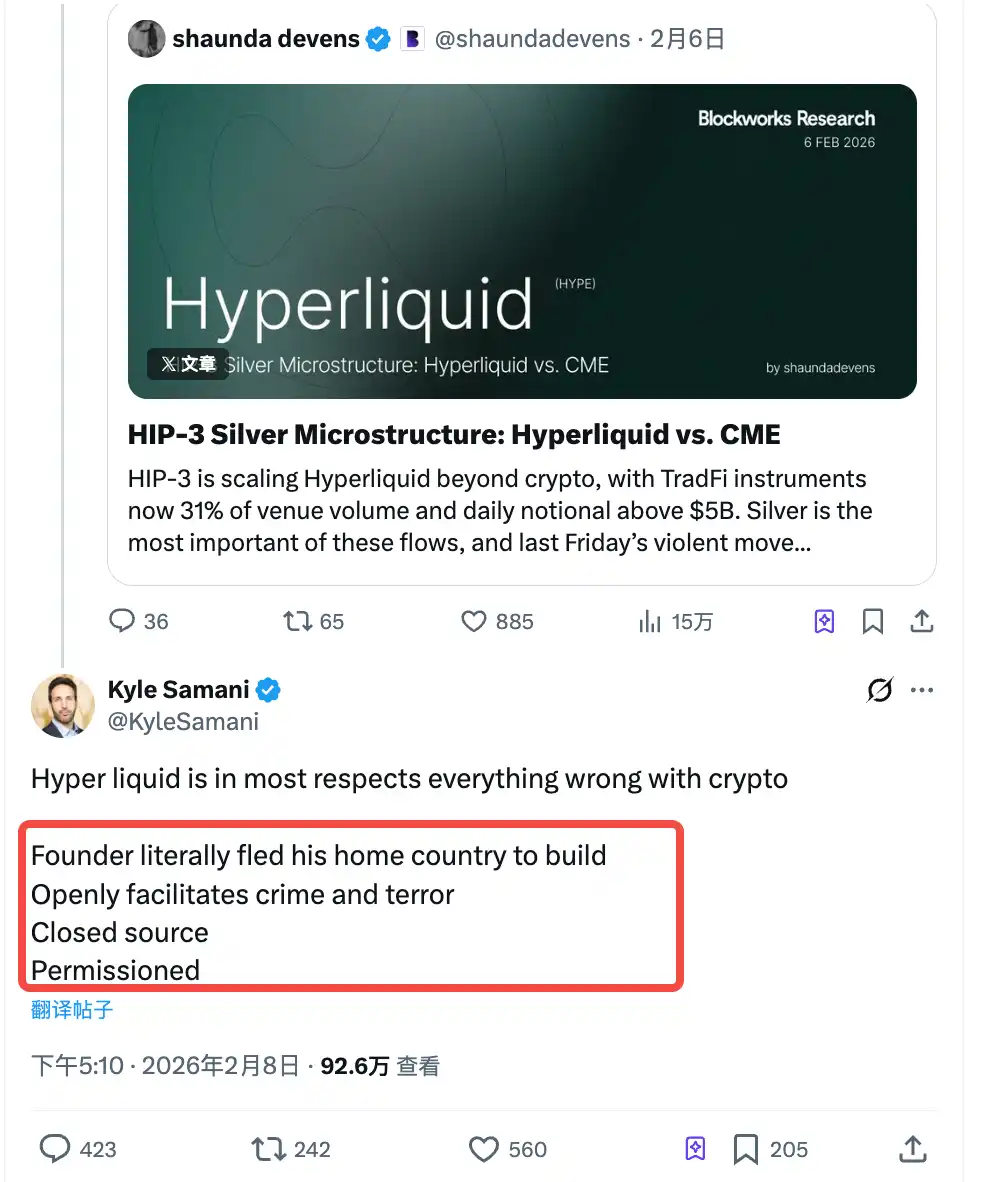

$HYPE has nearly doubled from its January low. No matter how you view this project, the market is voting. But Kyle Samani, the former co-founder of Multicoin, voted against it.

On February 8th, Blockworks Research published a report stating that Hyperliquid's silver contracts have begun competing head-to-head with traditional futures exchanges like CME in terms of spreads and execution.

Many in the circle shared it, seeing it as a sign that on-chain finance is finally starting to bite into traditional finance's turf.

But Kyle poured cold water on it.

He believes that Hyperliquid represents almost all the classic problems of the crypto industry:

- The founders fled their home country to build this project

- The platform openly facilitates crime and terrorist activities

- The code is closed-source

- The product operates with permissions, not fully open

In the past, this kind of statement would have been a common project attack on Crypto Twitter.

But don't forget, just four days ago, Kyle announced his departure from Multicoin Capital (Reference reading: Kyle Left the Crypto Industry, I'm a Bit Sad), and before the departure announcement, he posted a since-deleted tweet:

"Crypto isn't as fun as many people (including myself) once thought."

Old acquaintance Arthur Hayes clearly disagreed with this assessment, and he directly expressed his confidence in HYPE after Kyle's comments:

"Since you think HYPE is so bad, let's make a bet. From February 10th to July 31st, HYPE outperforms any coin with a market cap over $1 billion that you choose. The loser donates $100,000 to the winner's chosen charity. You pick the coin, I'm only betting HYPE wins."

Criticism, Leaving the Table

As of publication, Kyle has not accepted Arthur's bet and likely won't.

Someone who just said "crypto isn't as fun anymore" is unlikely to sit back down at the table to compare whose coin pumps more.

But Kyle's accusations against Hyperliquid are worth discussing.

For example, "the founders fled their home country." Hyperliquid founder Jeff Yan grew up in Palo Alto, California, graduated from Harvard, and previously worked as a quant at the high-frequency trading firm Hudson River Trading.

The team is based in Singapore, the company is registered in the Cayman Islands, and the platform blocks US users.

This structure is used by everyone from Binance to dYdX. Having been in this industry for nearly a decade, Kyle must know this is standard practice for offshore compliance.

Calling it "fleeing his homeland" seems a bit deliberate for someone who grew up in Palo Alto.

The points about being closed-source, permissioned, and facilitating crime aren't without merit, but in the past, Kyle might not have publicly stated such criticism. When he was at Multicoin, his job was to find, invest in, and promote projects; these gray areas were an unspoken cost everyone in the industry understood.

The change is that Kyle is no longer in that position.

What one sees after leaving the table is different from what one sees while sitting at it.

Pumping, No Need for Words

On the other hand, note that Arthur Hayes did not refute any of Kyle's accusations. He didn't defend Hyperliquid's closed-source nature, nor did he explain why Jeff Yan moved to Singapore.

His response was simply a price bet.

This is familiar crypto logic: pumping equals a good product. Choosing to respond with price is because, for those still working in this industry full-time, price is the only language that matters.

You say Hyperliquid has moral flaws, he says HYPE will outperform any large-cap altcoin in five months.

These two statements seem to be about the same thing but are actually on completely different planes.

Kyle is talking about "should or shouldn't," Hayes is talking about "will it pump or not."

This kind of talking past each other happens every cycle in the crypto space. Every time the market reaches its mid-to-late stages or a bear market, a group of people stands up and says the industry has problems, and those still at the table always respond with the same phrase:

Then look at the price.

Token price is the most convenient weapon for players still in the game because, as long as it's rising, all criticism can be temporarily set aside.

The problem is, Kyle might not be entirely an insider anymore. For a fund's co-founder to publicly express disillusionment with the entire industry just before formally resigning isn't quite appropriate in any circle.

The post was deleted, but the sentiment remains.

His current criticism of Hyperliquid, with its tone of leaving no room for doubt, seems less like criticizing a project and more like cutting ties with certain aspects of his past eight years.

However, while he personally can cut ties, Multicoin itself is still in the game.

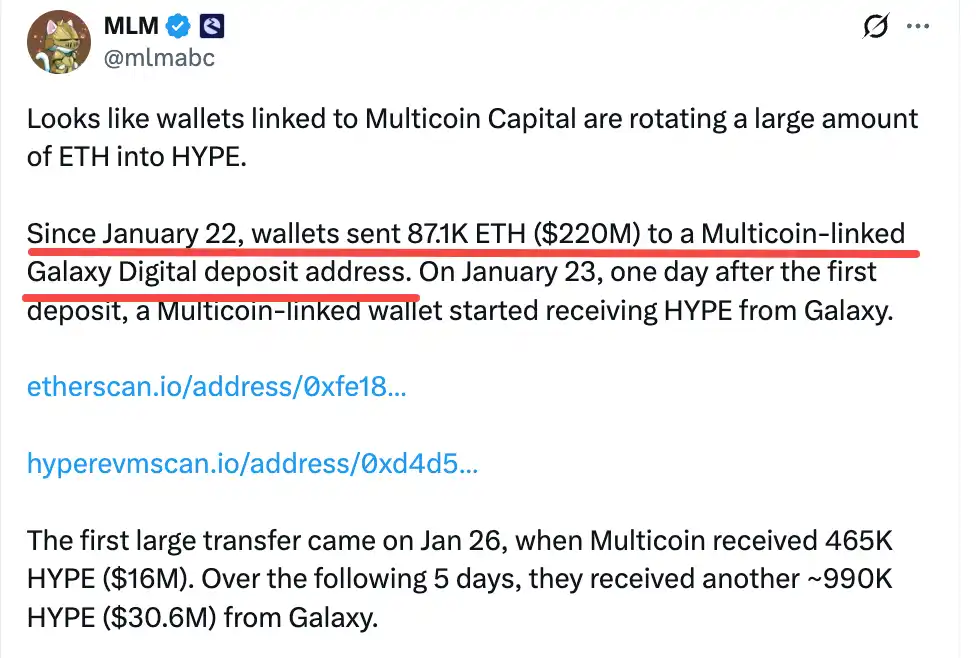

Starting November 22nd of this year, on-chain analysts discovered that a wallet疑似 associated with Multicoin deposited approximately 87,000 ETH to Galaxy Digital, and began buying HYPE in 17 transactions the next day, totaling about $46 million.

This means that around the time Kyle was leaving Multicoin, his former fund was making large investments in the project he just harshly criticized.

17 separate purchase transactions most likely mean someone within Multicoin made a judgment call and took action.

Kyle thinks Hyperliquid represents all the problems of the crypto industry, but at least someone at Multicoin thinks it's worth voting for with real money. Holding it is an attitude in itself.

Kyle left, but his old employer's money might have sat down. And it sat down at the very table Kyle despises the most.

Beyond the Arthur and Kyle showdown, the reactions in the comments are also interesting.

A Hyperliquid community user named Max dug up an old post he made in September 2024. The background of that post was that people were questioning Multicoin's operations in the circle. Max criticized Kyle back then, roughly saying:

"You're always trying to use LPs' money to chase the beta returns of your heavily invested assets, while also helping to pump your own investment portfolio."

A year and a half later, with Kyle now criticizing Hyperliquid, Max believes the套路 hasn't really changed:

Kyle is still the same Kyle, always criticizing others through the lens of his own portfolio. Defending Solana back then, sour on Hyperliquid now—the root lies in Multicoin's ecosystem interests and competitive anxiety.

Kyle couldn't help himself and directly replied with a characteristically crypto "wealth flex":The money I've directly invested in crypto is at least 10 times the total sum of your entire life.

And Max's follow-up jab hit the mark perfectly,In September last year, your assets might have been 30 times mine...

From September 2025 to February 2026, the market experienced several fluctuations. Multicoin, which Kyle previously represented, clearly saw its crypto assets shrink significantly; meanwhile, Hyperliquid has remained relatively resilient.

Position never exists separately from portfolio.

When a project begins to threaten the traffic and valuation of an existing ecosystem, criticism is quickly labeled as "conflict of interest"; conversely, defenders retaliate with "you're just jealous."

In this wave, Kyle wanted to attack Hyperliquid from the high ground of morality and decentralization purity, but was easily pulled back into the jungle law of "whoever makes money is right" by his opponent.

In the end, rational discussion is drowned out by tribal狂欢, leaving only screenshots and memes.

Every cycle is like this. Some people sit down, some people stand up. Those sitting down talk about price, those standing up talk about morality.

But whether one sees the problems first and then becomes disillusioned with the industry, or becomes disillusioned first and then sees the problems, the order is actually unclear.

Regardless of whether HYPE rises or falls five months from now, Kyle probably won't care. He's already looking at other things.