Last night, Nvidia's price reached $70 during the trading session, soaring 20% after hours because its latest earnings report exceeded everyone's expectations.

Intel disclosed its Q1 2026 fiscal year results on Thursday, with revenue of $13.6 billion, a 7% year-over-year increase, beating Wall Street consensus expectations by 11%. Non-GAAP earnings per share were $0.29, compared to analyst expectations of $0.01, exceeding expectations by 29 times—a rare discrepancy for a large-cap stock. Following the news, Intel's stock rose as much as 20% in after-hours trading.

The Q2 guidance also pointed in a more aggressive direction, with a revenue range of $13.8 billion to $14.8 billion, above the median of consensus expectations. New CEO Lip-Bu Tan used one sentence during the earnings call as a summary of the performance,大意是 the CPU is re-embedding itself into an indispensable foundational position in the AI era.

This has been one of the most discussed propositions for Intel over the past two years, as the company was once thought to have completely missed the first wave of AI.

On one hand, it failed to produce a GPU that could compete with Nvidia's; on the other hand, its advanced manufacturing nodes couldn't keep up with TSMC's. But over the past 12 months, as more and more AI deployments shifted from model training to inference and autonomous "agent" orchestration, the CPU—this once被视为基础款的 "computer brain"—has instead become needed again. Intel's rebound this quarter is the first financial落地 of this technology narrative.

Data Center Business Emerges from a U-Shaped Reversal

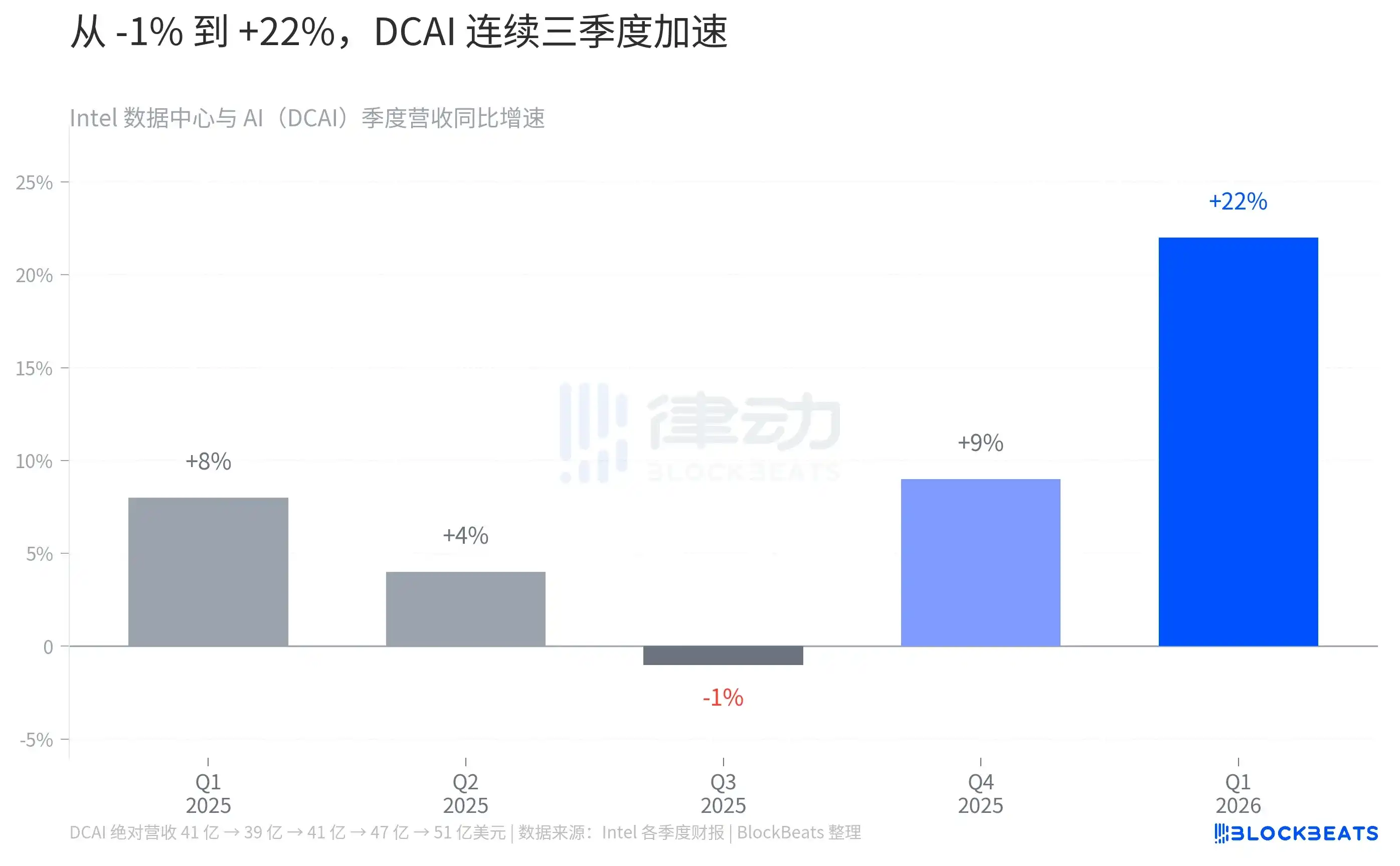

Breaking down the $13.6 billion in Q1, the most critical change came from the Data Center and AI (DCAI) line. According to Intel's earnings report, DCAI's quarterly revenue was $5.1 billion, a 22% year-over-year increase, hitting a record high.

This isn't a one-time爆发. Looking back to 2025, DCAI did $4.1 billion in Q1, dropped to $3.9 billion in Q2, and returned to $4.1 billion in Q3. This横盘 in mid-2025 once made the market doubt whether the so-called "CPU recovery" was just a narrative. Then in Q4, according to the disclosure caliber整理ed by Tom's Hardware, DCAI jumped from $4.1 billion in Q3 to $4.7 billion, a quarter-over-quarter increase of +15%, the fastest quarterly sequential growth rate for the company in a decade.

Entering Q1 2026, the figure of $5.1 billion allows the entire curve to画出了一个清晰的 U-shape, with the谷底 in mid-2025, the拐点 in Q4 2025, and confirmation in Q1 2026. Management's explanation was that the Xeon 6th Gen "Granite Rapids" processor began scaling up volume,叠加 the AI infrastructure refresh cycle. The company even主动牺牲ed part of its client CPU capacity, giving wafer allocation to the data center, raising the entire DCAI segment's profit margin. According to Intel's Q3 2025 earnings report, this segment's operating margin rose from 9.2% in Q3 2024 to 23.4%, almost 2.5 times higher.

The Same AI Narrative, Three Companies Paint Three Different Trends

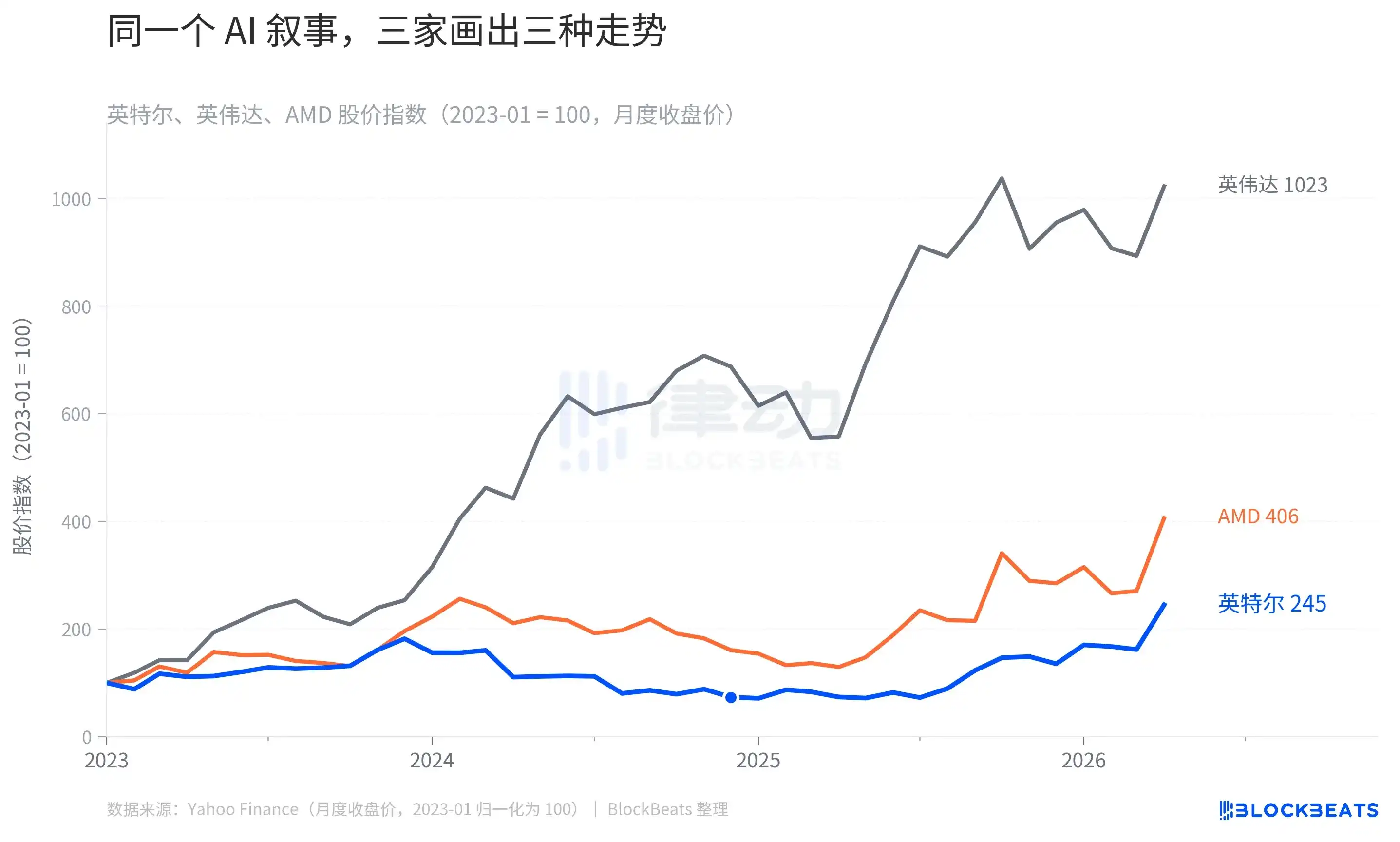

Placing Intel's rebound within a peer comparison reveals a chart more interesting than just the gains and losses.

Using January 2023 as a baseline, by April 2026, Nvidia's stock index had surged to 1023, AMD rose to 406, and Intel was at 245. The three lines started from the same point, but the endpoints differed by nearly five times. But what's more worth looking at is the shape of Intel's blue line. It didn't slowly climb; it first探ed down to 64 in September 2024 (equivalent to a 36% drop from the starting point), then画出一道 V-shaped rebound, only catching up to 245 in early 2026.

This chart actually tells the story of the market's two pricings of "who really makes money in the AI capital cycle." From 2023 to 2024, money flowed to Nvidia because training requires GPUs. AMD啃下 the second piece of the cake with its MI300 series, and its stock price followed. Intel, however, was系统性地划掉ed from the AI交易名单 because Gaudi accelerator sales fell short of expectations and advanced process mass production lagged. According to third-party estimates cited by《Fortune》in January 2025, Nvidia's share of the AI chip market rose from 25% in 2021 to 86% in 2024, while Intel's fell from 68% to 6%.

The second pricing occurred from the second half of 2025 to early 2026, when the market began重新讨论一个问题: if AI moves from training to inference and the Agent stage, will the demand structure for computing power change? The answer to this question directly determines how far Intel's blue line can go.

The Closer the Scenario is to Agent, the More CPUs Return to Center Stage

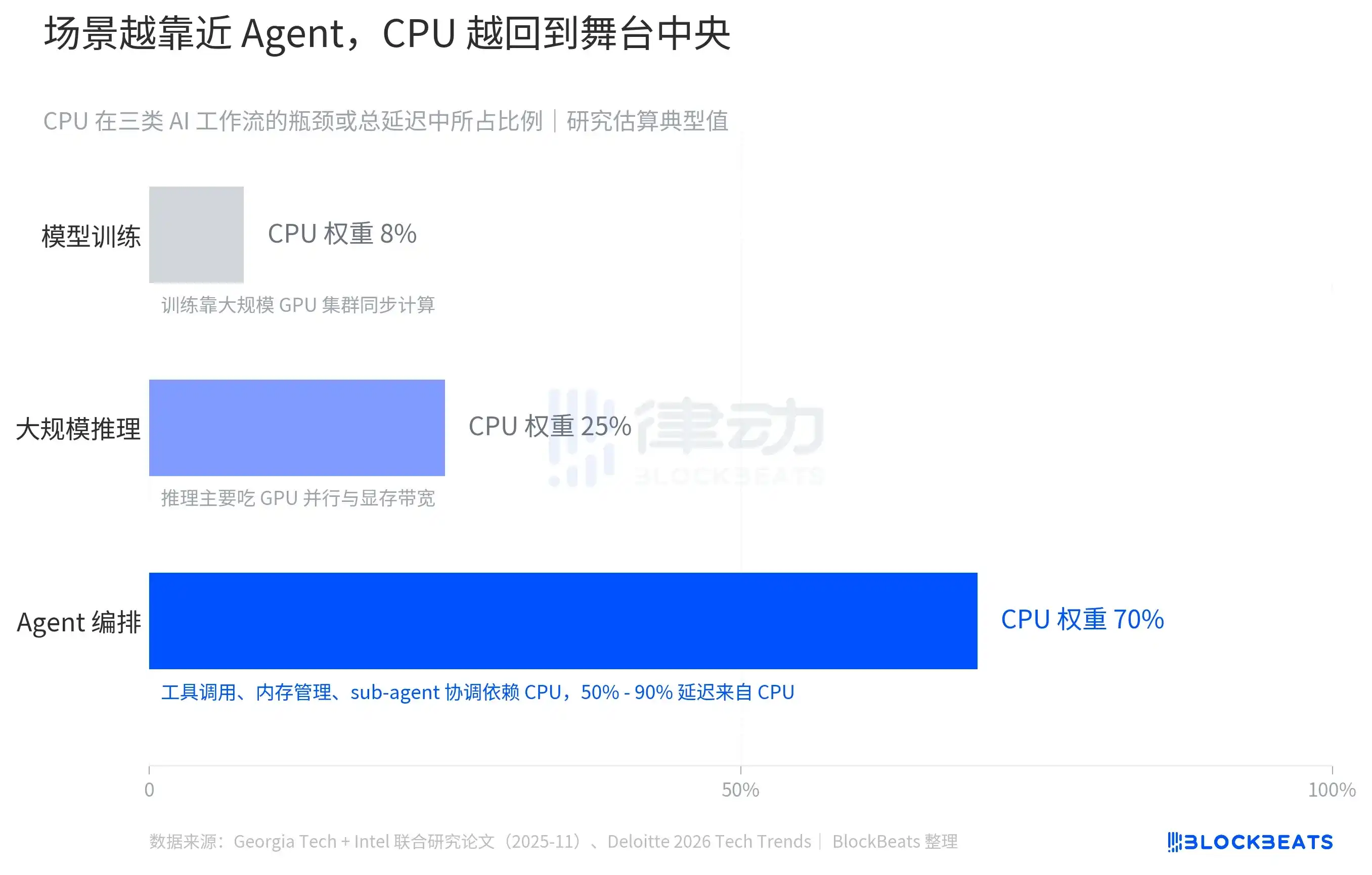

Breaking down the AI workflow into three types of scenarios, the weight of the CPU varies greatly among them. According to estimates from Deloitte's 2026 Technology Trends report, in the large model training phase, the CPU only accounts for about 8% of the workflow bottleneck, with the remaining 92% of the computing pressure on the parallel synchronization of GPU clusters—this is Nvidia's主场. Entering the large-scale inference phase, the CPU's weight rises to 25%, but GPU parallel throughput and memory bandwidth remain the bottlenecks.

The real change happens in Agent orchestration scenarios. According to a study jointly published by Georgia Tech and Intel in November 2025, CPU processing for tool calls in Agent workflows accounts for 50% to 90% of the total latency of the entire process, with the specific proportion depending on the tool type and orchestration complexity. In other words, when an AI Agent is doing things like "calling APIs, pulling data, coordinating subtasks, managing contextual memory," the bottleneck is not the GPU, but the CPU.

This trend has quantifiable magnitude for reference. According to Deloitte estimates, the proportion of inference workload in total AI computing power was about 1/3 in 2023, about 1/2 in 2025, and is expected to reach 2/3 by 2026. According to Futurum Group calculations, the server CPU market size will grow from $26 billion in 2025 to $60 billion in 2030, with growth exceeding the historical long-term average. A more specific signal is OpenAI's disclosed computing power roadmap; the company plans to acquire "hundreds of thousands of the most advanced Nvidia GPUs, as well as computing power scalable to tens of millions of CPUs to support Agent workloads." GPUs are still the boss, but the magnitude of CPUs is publicly placed on the same line for the first time.

The Rebound Didn't Start in Q1 2026

Overlaying Intel's stock price over the past five years with six key events, the 20% after-hours jump in Q1 is actually the尾声 of a series of earlier decisions.

In February 2021, Pat Gelsinger returned as CEO, presenting the "IDM 2.0" strategy to make Intel both a chip designer and an open foundry. When Gaudi 3 was released in April 2024, Intel set its 2024 AI accelerator sales target at $500 million.

On August 2, 2024, the Q2 2024 earnings report爆雷ed, with revenue of $12.8 billion down year-over-year, GAAP EPS of -$0.38, announcing 15% layoffs and a dividend suspension. The stock fell 26% in a single day, its worst single day since 1974. According to Intel's disclosure at the time, management subsequently admitted that Gaudi 3 would not achieve the full-year $500 million target and took a $300 million inventory write-down.

According to Intel's official announcement, Gelsinger left on December 1, 2024, and the company entered an interim co-CEO phase. In February 2025, the new management decided to cancel the independent GPU project "Falcon Shores," which aimed to compete with Nvidia, admitting that its self-developed AI accelerator roadmap could not outrun Nvidia's ecosystem lock-in. On March 18, 2025, former Cadence CEO and semiconductor veteran Lip-Bu Tan officially became Intel's CEO. This time point corresponded to an Intel stock price around $22, only up a little over 20% from the September 2024 low of $18.

From Lip-Bu Tan's appointment to this Q1 earnings report, Intel's stock price rose from $22 to $65 before the report. Coupled with the 20% after-hours jump, it意味着 just touched around $78. If the period from August 2024 to December 2024 was the company's至暗时期, then the true starting point of the rebound was not Q1 2026, but the moment when Falcon Shores was canceled and Tan was selected as CEO. The company abandoned its fantasy of competing with Nvidia and returned to its true strength—the CPU主场.

The 29x EPS beat is a financial signal, but behind it, two things happened simultaneously. The market began重新定价 the position of the CPU in the AI architecture, and Intel恰好 completed its management change and product line取舍. Neither of these things happened in Q1.