Author: Grayscale

Compiled by: Deep Tide TechFlow

As a leading crypto asset management company, introducing a diverse range of investable digital assets to investors is a crucial part of our mission.

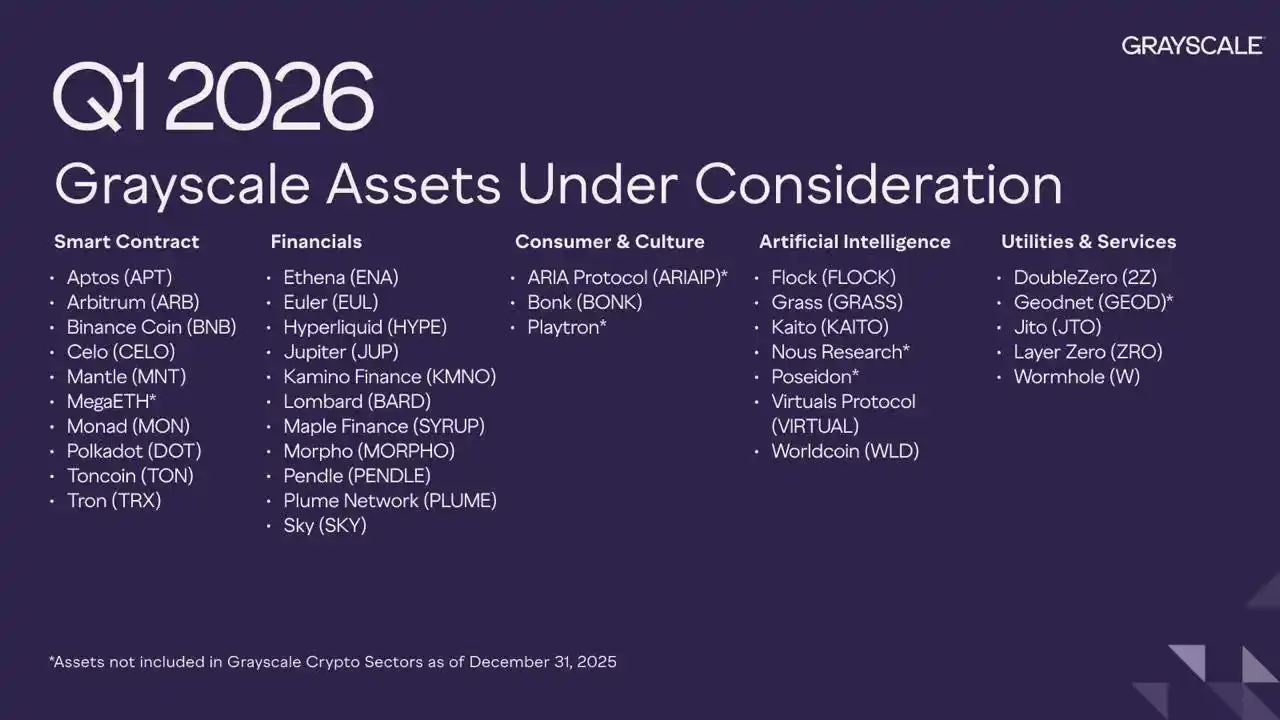

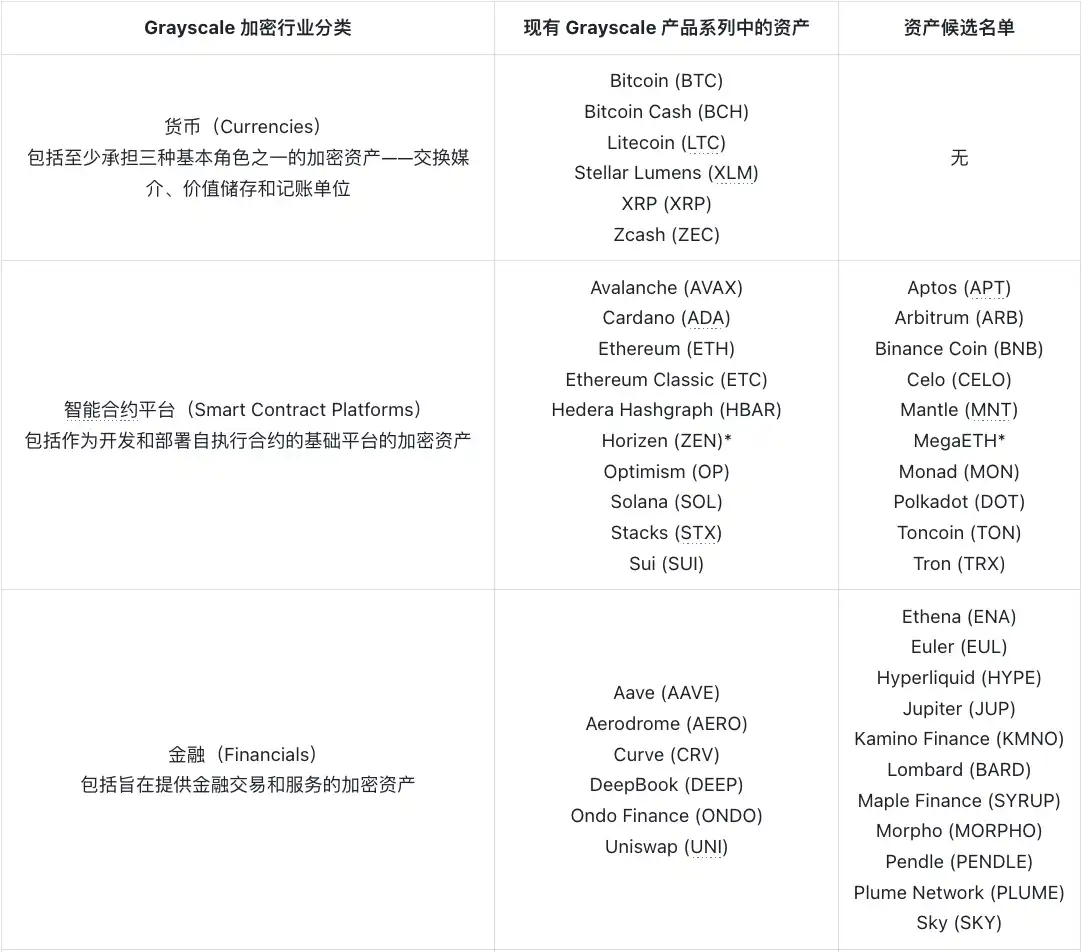

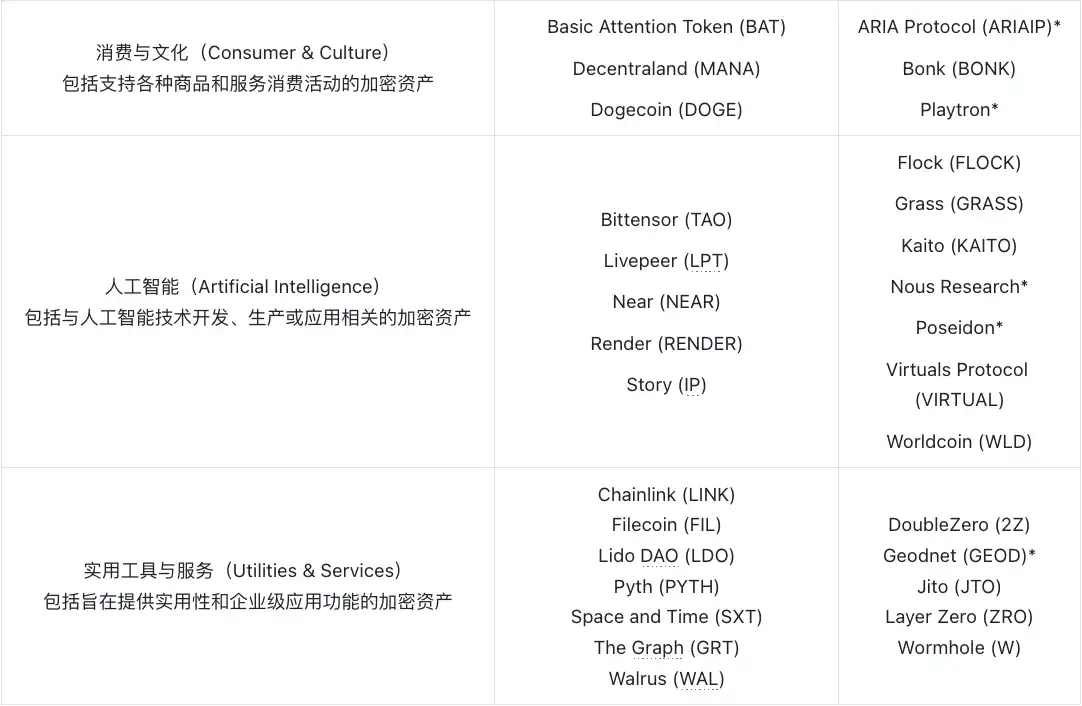

Therefore, we are pleased to share this candidate list of assets that may potentially be included in Grayscale investment products in the future, along with an updated list of assets currently in our existing product lineup. Both lists are categorized according to the Grayscale Crypto Sector Classification Framework we designed, which aims to set the standard for organizing crypto asset categories.

The "Asset Candidate List" includes digital assets that are not currently part of Grayscale investment products but have been identified by our team as potential candidates for future products.

The "Assets in Existing Grayscale Product Lineup" lists the digital assets held by Grayscale products as of January 12, 2026, which may be part of either single-asset products or multi-asset products.

As the crypto ecosystem expands and the Grayscale team reviews or re-evaluates additional assets, we plan to update this list as frequently as possible within 15 days after the end of each quarter. The following lists are as of January 12, 2026, and may change during the quarter as some multi-asset funds rebalance their compositions and we launch new single-asset products.

*As of December 31, 2025, assets not included in the Grayscale Crypto Sector Classification.

1 Assets may be directly included in the Grayscale product lineup without first being listed in this table, for example, if a decision is made to include an asset in a Grayscale product during the quarter.

The process of creating investment products similar to our existing ones is complex and multifaceted. It requires in-depth review and consideration and is influenced by various factors such as internal controls, custody arrangements, and regulatory requirements. It is important to note that this table is for informational purposes only, and not all candidate assets will be converted into our investment products. Grayscale may also explore other assets not listed in the table for inclusion in its product lineup. Similarly, assets may be directly included in the Grayscale product lineup without first being listed in this table.

Grayscale may attempt to have shares of new products quoted on secondary markets. Although shares of certain Grayscale products are approved for trading on secondary markets (such as OTCQX), for investors in new products, it cannot be assumed that such shares will receive similar approval due to potential concerns from the U.S. Securities and Exchange Commission (SEC) and/or the Financial Industry Regulatory Authority (FINRA) regarding the status of the underlying digital assets under federal securities laws.

This article does not constitute an offer to sell or a solicitation to buy any securities in any jurisdiction, nor should it be considered as legal to make such an offer, solicitation, or sale without registration or qualification under the securities laws of that jurisdiction. Grayscale, its affiliates, and clients may hold positions in the digital assets or securities discussed herein.