The Federal Reserve announced on April 24, 2025, that it is pulling back previous rules for banks handling crypto and dollar tokens. From now on, banks will be supervised the usual way, instead of through separate crypto-focused requirements.

Banks Can Now Move Faster With Crypto

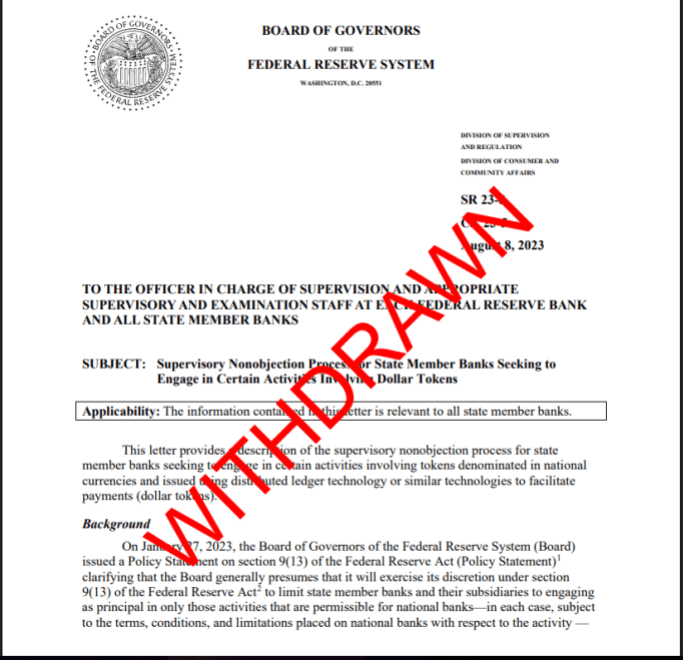

The rules being withdrawn included a 2022 letter that told state member banks to notify the Fed before dealing with crypto, and a 2023 letter that required approval before handling dollar tokens. These rules had kept some smaller banks, especially uninsured crypto-focused ones, from accessing Fed accounts or payment systems.

Other regulators moved at the same time. The FDIC and the OCC also withdrew two 2023 statements about crypto risks. Those statements had flagged issues like liquidity and governance risks in crypto banking. By pulling them back, banks now face fewer formal roadblocks when offering crypto services.

🚨🚨🚨WOWZERS–the Fed rescinded guidance it enacted in Jan 2023 simultaneously with the @custodiabank denials + the Biden White House anti-crypto statement. Thank you, VCS Bowman & Gov Waller!🙏 The Fed broke the law by citing this very guidance in the Custodia denial, even tho...

— Caitlin Long 🔑⚡️🟠 (@CaitlinLong_) December 17, 2025

Fed’s New Guidance

On Dec. 17, 2025, the Fed introduced new guidance to give both insured and uninsured state member banks a clear path to explore activities like cryptocurrencies, as long as they meet the Fed’s risk-management standards, the central bank said.

@federalreserve withdraws 2023 policy statement and issues new policy statement regarding the treatment of certain Board-supervised banks that facilitates responsible innovation: https://t.co/5s1I9LO9EF

— Federal Reserve (@federalreserve) December 17, 2025

Supervision Now Part Of Normal Oversight

The Fed said it will continue watching banks’ crypto work, but through regular supervisory processes. Banks don’t need to send extra notifications or get prior approval for crypto activities anymore. That includes things like custody, trading, or settlement of digital assets. There aren’t new rules being added — it’s just now part of normal oversight.

Key Dates And Actions

The important date is April 24, 2025. On this day, the Fed withdrew letters from 2022 and 2023, along with the two joint interagency statements from 2023. These had previously told banks how to report and get approval for crypto work. The withdrawal simply moves crypto activities into regular bank supervision.

The US Federal Reserve. Image: TuftsNow

What This Means For Banks And Markets

Banks have more leeway to provide crypto services because they no longer have to follow the old regulations. They’ve gained the ability to quickly develop, test, and manage digital assets. However, the Fed continues to keep an eye on how banks manage their risks.

While this change does not eliminate all regulatory requirements, it eliminates much of the extra duplication of paperwork and approvals that acted as barriers and impeded progress in the past.

Featured image from Unsplash, chart from TradingView