Michael Barr, a member of the Federal Reserve Board of Governors, has called for caution and strict stablecoin oversight.

During a recent discussion on stablecoin law, the GENIUS Act, Barr singled out major uses of the products, including crypto trading, cheaper remittances, and savings overseas.

However, he raised concerns about stablecoins’ facilitation of terrorist financing and risk to financial stability.

Well, Chainalysis data estimates that stablecoins now account for 84% of illicit crypto activity. This is a massive spike from only 15% in 2020. Hackers are now embracing stablecoins and P2P transactions to evade sanctions.

To curb this, Barr recommended,

Both regulatory and technological solutions will need to be deployed to limit these risks.

Despite the surge, the overall illicit activity only accounts for less than 1% of total crypto transactions.

On financial stability risk, Barr cited the ‘long and painful history’ of competing private money (bank notes) in the 1800s that led to bank runs and financial panics because they traded below par.

The cause? Low-quality reserve assets and weak safeguards. Barr added,

Tight control over reserve assets, coupled with supervision, capital and liquidity requirements, and other measures, could enhance the stability of stablecoins and make them more viable payment instruments.

This is part of the rulemaking process as regulators race to meet the July 2026 deadline for implementing the GENIUS Act. So far, the OCC and NCUA have issued proposed rules for the same. The Fed and other regulators are expected to follow suit and finalize guidelines by early Q3.

Stablecoins: USD-based vs. others

For issuers, the GENIUS Act offers clear rules. But for the U.S. government, it’s an increasingly important demand line for Treasury Bills to finance its debt.

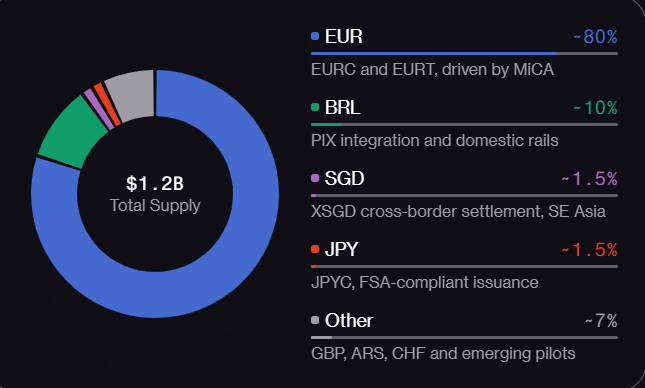

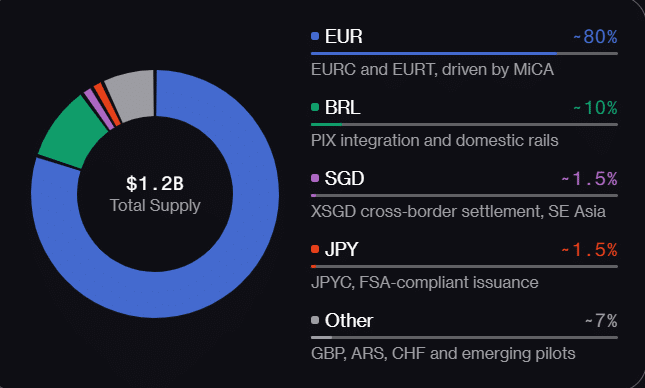

Although USD-based versions (USDT, USDC) dominate the current $315 billion stablecoin market, non-USD alternatives have seen record growth. Since 2023, non-USD stablecoins have surged from $350 million to $1.2 billion. That’s a 3x expansion outpacing USD stablecoin growth, mostly dominated by Euro-based alternatives.

Beyond currency-based measures, Asia accounts for over 60% of global stablecoin activity, driven primarily by the Singapore–Japan–Hong Kong–China corridor. Interestingly, these jurisdictions are pushing for stablecoin rules that could restrict USD-based options. It’s unclear how these shifts will impact current stablecoin market dynamics in the upcoming months.

Final Summary

- Fed’s Barr called for strong stablecoin oversight to avoid repeating the ‘painful’ bank runs of the 1800s due to private money.

- The stablecoin market could be headed for major shifts as key global adoption jurisdictions mull restricting USD-based alternatives.