On April 7, voters in Festus, Missouri, ousted four out of eight city council members in a single recall election. The trigger was the council's approval of a $6 billion AI data center project in late March by a 6-2 vote. The project, led by CRG, the data center development arm of Clayco, spans 360 acres, with the end customer being an undisclosed Fortune 100 company (codenamed Project Cumulus).

The council approved it without holding public hearings. Subsequently, the local resident group Wake Up JeffCo sued the city government and CRG in St. Louis County Court, and a petition to recall the mayor has also been initiated. According to a summary by Tom's Hardware, around the same time, the home of Indianapolis city councilor Ron Gibson was shot at with over a dozen bullets at the end of 2025, with a note left at the doorstep saying, "No Data Centers."

Festus is not an isolated case. Not long ago, Indianapolis city councilor Ron Gibson's home was hit by 13 shots in the middle of the night, waking his 8-year-old son. A handwritten note was left at the door: "No data centers." The FBI has launched an investigation. Jordyn Abrams, a researcher at George Washington University's Program on Extremism, pointed out that data centers are becoming targets for anti-tech, anti-government extremists.

Advocacy group Data Center Watch, in its Q2 2025 report, updated the number of organized opposition groups from 142 (across 24 states) a year ago to 188 (across 40 states). The value of projects halted or delayed increased from $64 billion to $162 billion. On April 1, 2026, Port Washington, Wisconsin, passed the nation's first referendum explicitly targeting data centers, with 66% of voters approving a mandatory referendum threshold for TIF subsidies exceeding $10 million.

These events collectively answer the same question: Could the real bottleneck in AI capacity expansion be stuck at the county and city ballot box?

Widespread Backlash

Plotting events from the past 23 months on a U.S. map reveals two levels of backlash. One is at the state level, where eight states have submitted or passed data center moratorium bills, including Maine (passed the House 82-62, lasting until 2027), Vermont (paused until July 2030), Virginia (submitted by Democratic Representative Irene Shin, paused until 2028), Georgia, Maryland, South Dakota, Wisconsin, and Minnesota. This layer involves legislative action, with the broadest impact but the slowest progress.

The other is at the city and county level, where backlash is denser and more intense. The Chandler, Arizona city council unanimously rejected Active Infrastructure's $2.5 billion project in December 2025 (lobbied by former federal senator Kyrsten Sinema). The Tucson city council is currently reviewing data center zoning restrictions in April 2026, with public comment open until the end of the month. Hays County / San Marcos, Texas, rejected a $1.5 billion project by a 5-2 vote. Oregon's Cascade Locks, Indiana's Chesterton, Virginia's Catlett Station, Missouri's Peculiar, Michigan's Lansing. According to Data Center Watch, at least 10 states have seen direct municipal rejections or developer withdrawals.

More than half of the high-conflict incidents are concentrated in the Midwest and Midsouth. This region has relatively ample grid capacity over the past decade and was a hotspot for the previous wave of data center expansion. The backlash now focused in the same area, from another perspective, is the supply side spreading from "states with power surplus" and hitting the most sensitive layer of local politics.

$6 Billion Is Not on the Same Scale

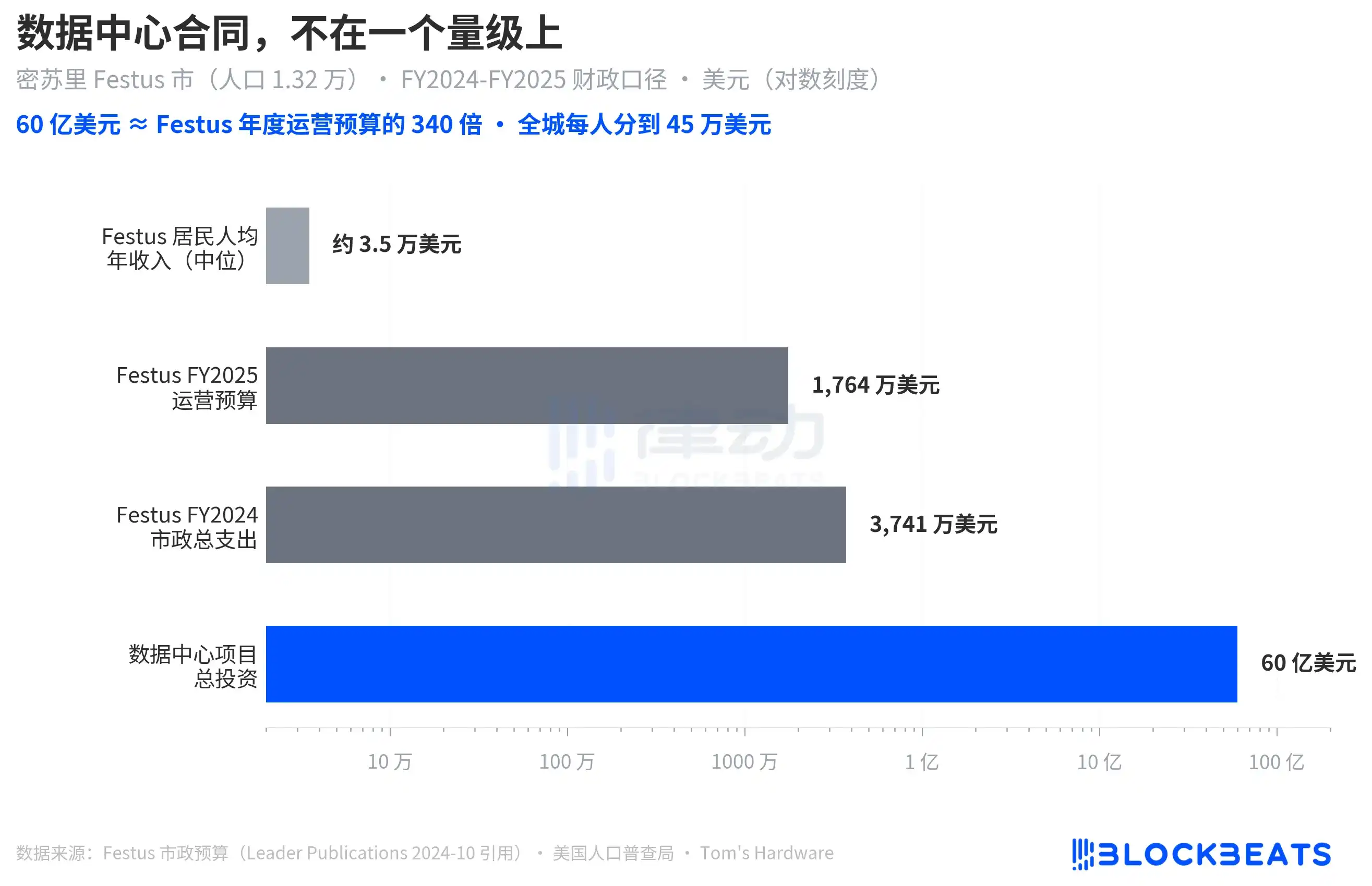

Festus's fiscal scale means the $6 billion figure simply cannot be processed normally by the city council. According to local newspaper myleaderpaper citing municipal budget documents, Festus's FY2025 general fund plus public safety operating budget is $17.64 million, FY2024 total municipal expenditure was $37.41 million, and reserve funds at the end of FY2025 are projected at $28.09 million.

The data center project's $6 billion is about 340 times the annual operating budget, or $450,000 per resident for the city's 13,200 people. In relative terms, this is not a local development project to be discussed, but a small town being plugged into a capital pipeline completely unrelated to itself.

Comparing it to Festus residents' median annual income—about $35,000 in Missouri non-metro areas—makes the issue clearer. Any decimal point in the data center contract is larger than the entire community's lifetime per capita disposable income. Local officials lack experience in balancing such numbers procedurally. The Festus council resolution was criticized for "not holding public hearings" technically because such projects typically operate under commercial confidentiality clauses (developer and end customer identities undisclosed), making normal council procedures unable to review confidential contracts. This is a structural loophole, not negligence by individual council members.

Precisely because of the scale gap, breaking down the data center contract into manageable pieces for local councils is inherently unworkable. This is why, over the past 12 months, the backlash path hasn't been internal resolution but external weapons: recall, litigation, and referendum. Festus's recall of four council members, simultaneous lawsuit by residents in St. Louis County Court, and initiation of a mayor recall petition are a rare case of all three paths triggering at once.

One Data Center, Consuming a Small Town

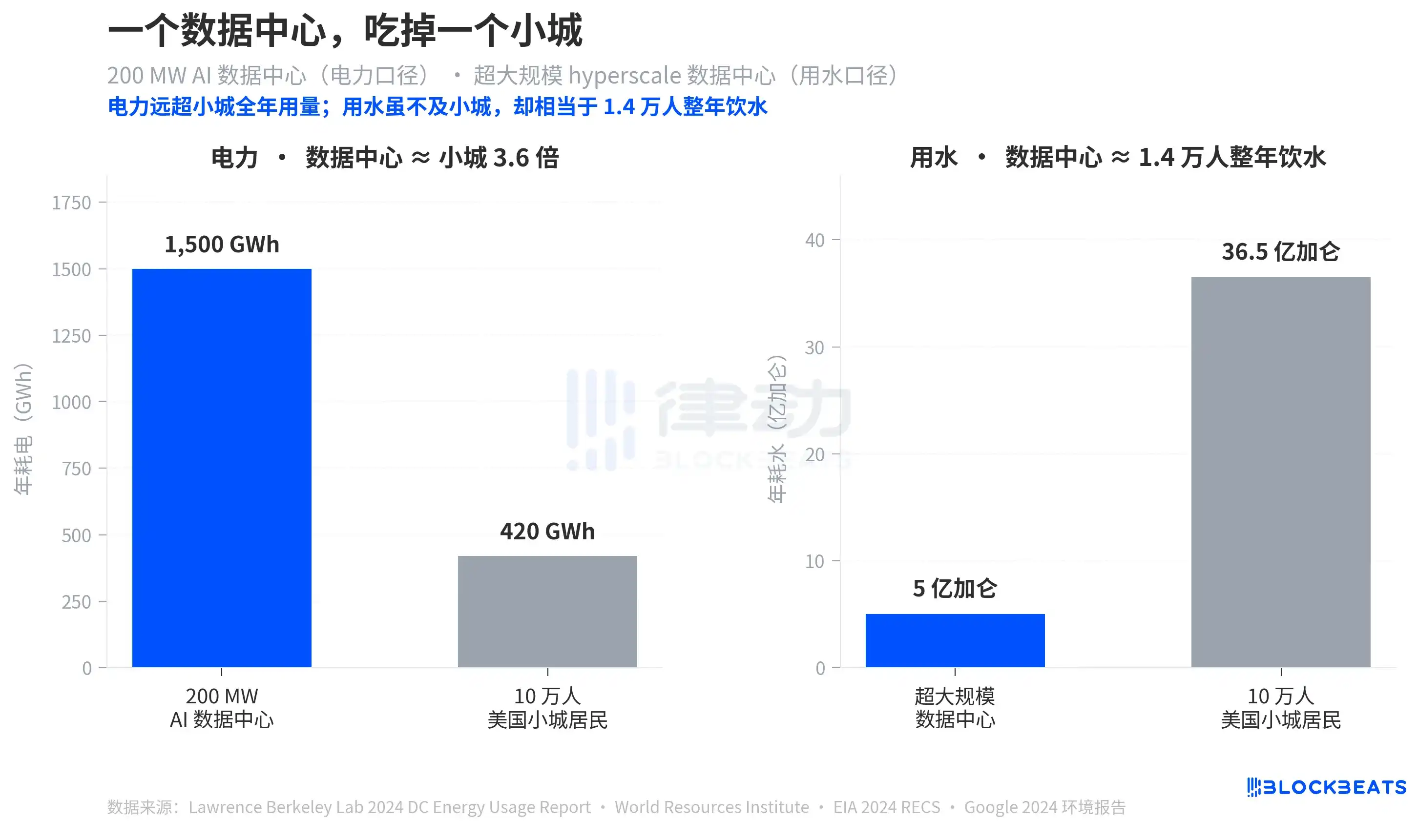

The power consumption of an AI data center is best felt using a small U.S. town for comparison. A fully loaded 200 MW AI data center, at 86% load factor, consumes about 1,500 GWh annually. A 100,000-person small U.S. town's residential electricity consumption is about 420 GWh per year (based on EIA's average residential electricity use of 10.5 MWh per household, 2.5 persons per household). The data center uses 3.6 times the electricity of the town's residents. And this is just electricity, not counting cooling and ancillary water use.

The water comparison is reversed but even more直观. According to USGS typical residential water use (100 gallons per person per day), a 100,000-person town uses about 3.65 billion gallons annually. A hyperscale AI data center, per Google's Council Bluffs (the largest Google data center in the U.S.), uses 500 million gallons per year. In absolute terms, the data center uses 13.7% of the town's water, but on another scale, it's equivalent to the annual drinking water for 14,000 people. For a town with 10,000 to 50,000 residents, it means ceding a substantial portion of the city's water supply to one user. According to Lawrence Berkeley Lab's 2024 data center energy report, U.S. data centers used 17 billion gallons directly for cooling in 2023, and 211 billion gallons indirectly (for power generation), with direct water use expected to double or quadruple by 2028.

The most common protest cry is "our wells will run dry." Numerically, this is not an emotional expression. In Loudoun County, Virginia (the most data center-dense county in the U.S.), potential data center water use in 2023 was 899 million gallons, about 10% of the county's total water use, according to local water data cited by Sierra Club and Grist. If this is the case at the county level, the numbers for towns will only be more extreme.

Planned Capacity Entering the Backlash Window

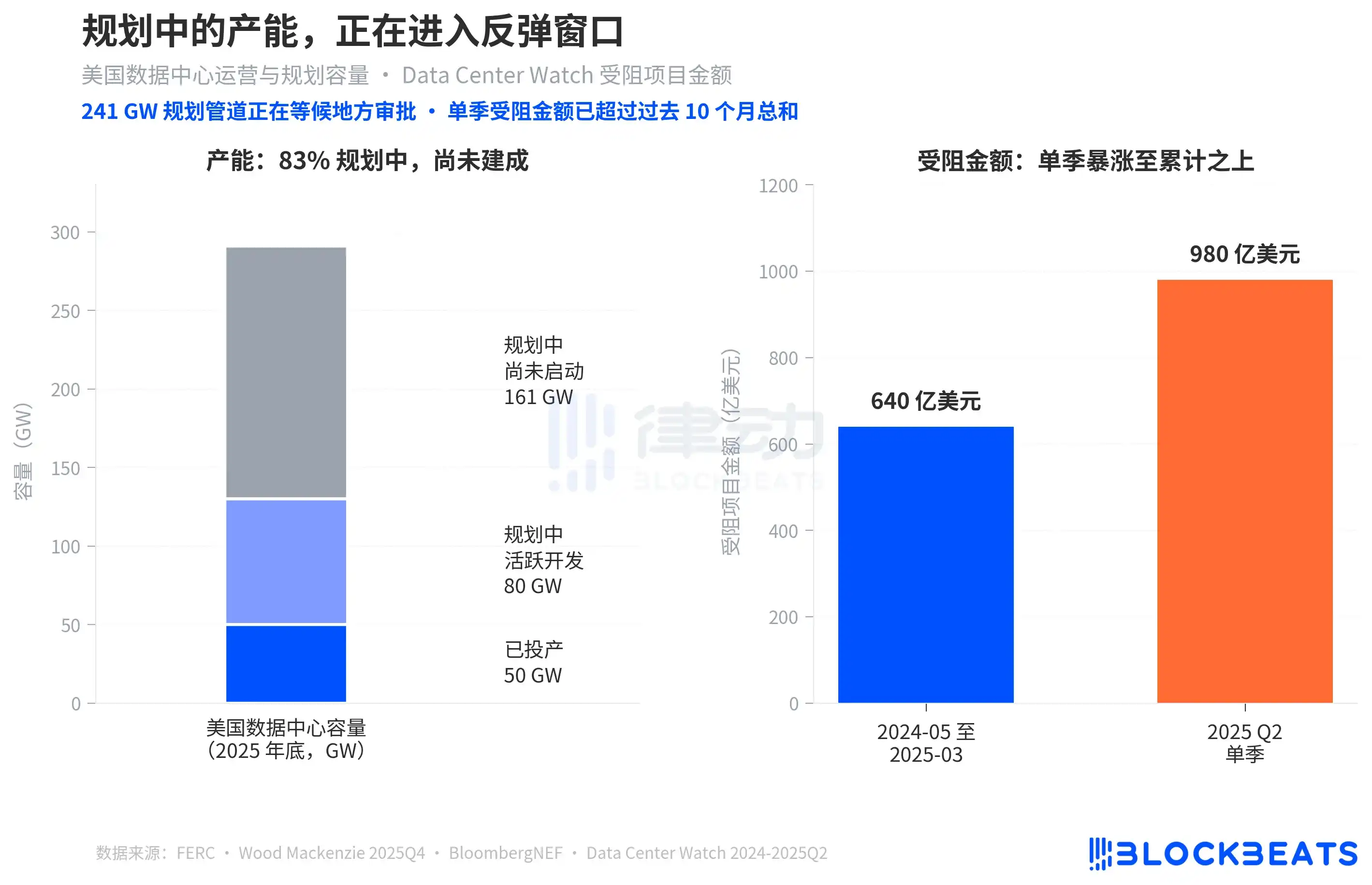

Actually operational U.S. data center capacity, per FERC and Wood Mackenzie Q4 2025 data, is about 50 GW. The planned pipeline totals 241 GW, with 33% (about 80 GW) in active development and the remaining 67% (about 161 GW) not yet started. BloombergNEF predicts the U.S. will add 97 GW from 2025 to 2030, with data center electricity peak reaching 106 GW by 2035. All these numbers point to one fact: the vast majority of capacity is still on drawing boards, not yet落地.

According to data disclosed by Sightline Climate via TechRadar, 30% to 50% of the 16 GW originally planned for 2026 commissioning is expected to be canceled or delayed. Meanwhile, Data Center Watch data shows that from May 2024 to March 2025, organized opposition blocked or delayed $64 billion in data center projects. In Q2 2025 alone, this figure was $98 billion, corresponding to 20 projects. The quarterly受阻 amount already exceeds the cumulative total of the previous 10 months.

This creates a timing mismatch. Capital has committed to multiplying U.S. data center capacity several times over the next five years, but新增 capacity must pass through county and city approvals one by one. The more planned capacity, the larger the surface area vulnerable to backlash. Cases like Festus escalating from council vote to recall and lawsuit in a month are not because it's special, but because the number of opposition groups increased by 46 in a year (per Data Center Watch Q2 2025 report), and they share templated legal tools跨州, including TIF subsidy referendums, zoning lawsuits, and councilor recall petitions. Whether the long-term power contracts signed by frontier labs will be fulfilled depends on which counties they land in and what kind of residents are watching those counties' councils.

The bottleneck in AI capacity expansion has, for the first time, jumped outside the power contract negotiation table and appeared on the recall ballots of 13,200 people.