Original | Odaily Planet Daily (@OdailyChina)

Author|jk

May 24th, Haiphong Road in Tsim Sha Tsui, Hong Kong, was eerily quiet.

A week ago, this was the "Account Opening Street" for mainland investors, with temporary brokerage booths and mobile vans lined up, bustling with crowds. Zero-commission Hong Kong stock account openings, free stock gifts, support for IPO subscriptions, relaxed proof-of-address requirements... To attract mainland clients, brokerages had practically lowered the barriers to the floor.

Yet, just seven days later, the door slammed shut. Nowadays, mainland clients wanting to open a Hong Kong stock account not only have to sign a written declaration promising that their funds come from outside mainland China and that they have never forged documents, but even after signing, they might still face a "rejection."

The turning point began on May 22nd. Regulators from both sides simultaneously launched a coordinated crackdown, directly affecting millions of mainland investors trading overseas markets through Hong Kong brokers.

Just how intense is this regulatory storm? What is the real experience for mainland residents trying to open accounts in Hong Kong now? What other compliant channels remain for investing in overseas assets? Odaily Planet Daily breaks it down for our readers.

I. Joint Action from Both Sides Ends the "Gray Channel" for Hong Kong and US Stock Investment

On May 22nd, regulators in Hong Kong and mainland China acted almost simultaneously, clamping down from the south and the north in a pincer movement.

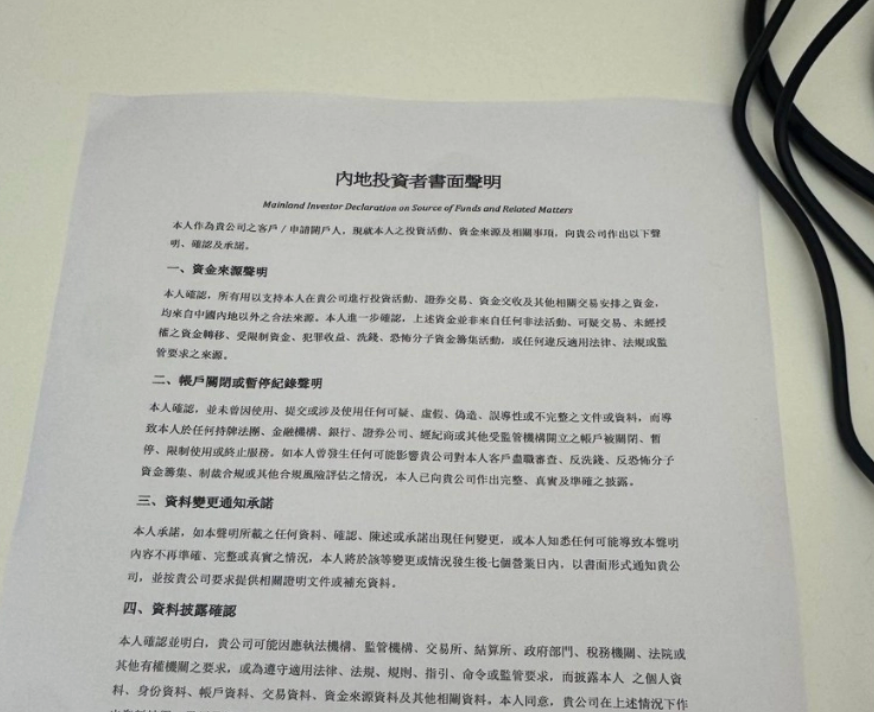

The Hong Kong Securities and Futures Commission (SFC), after reviewing the account opening practices of 12 securities brokers, issued a circular with unusually stern wording. The document pointed out numerous significant deficiencies: insufficient due diligence on account opening documents, acceptance of suspicious or forged documents during the process, and clear weaknesses in managing cross-border agency relationships with overseas intermediaries. The SFC explicitly stated that these accounts might be used for illegal activities, with non-negligible money laundering risks.

Regarding mainland investors, the SFC listed additional "three requirements" in the circular's annex: new accounts must submit a written declaration; deposits, withdrawals, and settlements can only be made through qualified bank accounts opened in the client's own name. The core content of the written declaration includes: confirming that all investment funds originate from legal sources outside mainland China; that the account has never been closed due to the use of suspicious documents; that the broker must be notified within 7 business days if circumstances change; and agreeing to disclose relevant information to law enforcement and regulatory authorities.

The SFC required all licensed institutions to conduct immediate self-inspections, closing accounts opened with suspicious or forged documents, as well as "dormant accounts" with zero balance or no transactions for 12 months. Senior management was also explicitly named, potentially facing regulatory and enforcement actions for serious compliance failures.

Almost simultaneously, the China Securities Regulatory Commission (CSRC), jointly with eight other ministries (Ministry of Industry and Information Technology, Ministry of Public Security, People's Bank of China, State Administration for Market Regulation, National Financial Regulatory Administration, Cyberspace Administration of China, State Administration of Foreign Exchange), officially issued the "Implementation Plan for Comprehensive Regulation of Illegal Cross-border Securities, Futures, and Fund Business Activities." The plan sets a 2-year intensive rectification period, during which existing accounts can only sell and withdraw funds unidirectionally, with no new additions allowed. Administrative penalty notices were also issued to Tiger Brokers, Futu Securities, and Longbridge Securities and their related entities for illegal securities business activities. The scope, intensity, and determination of this crackdown are rare in recent financial regulatory history.

Two documents, from different regulatory systems, point to the same issue: The model where a large number of mainland investors traded Hong Kong and US stocks through Hong Kong brokers, long operating in a legal gray area, has officially come to an end. This time, the regulators mean business.

To understand why this crackdown is so decisive, we must look back at how "wide" this channel has been over the past two to three years.

From 2023 to early 2025, the Hong Kong and US stock markets took off in succession, and numerous IPO opportunities emerged in Hong Kong, driving a surge in demand for account openings among mainland investors. At that time, internet brokers like Futu, Tiger, and Longbridge, leveraging their smooth Chinese app experience, low or even zero commissions, and support for direct RMB deposits, aggressively penetrated the mainland user base. Some Hong Kong broker platforms did not require proof of address, or performed no substantive address verification, and even allowed deposits using stablecoins (USDT). Opening an account was practically just a click away.

As early as July 2016, the CSRC issued a risk warning, specifically naming Tiger Brokers, Futu Securities, and others for providing trading services for overseas securities like Hong Kong and US stocks. At the end of 2022, the CSRC launched a special rectification campaign targeting overseas brokers like Tiger and Futu. However, the rectification had limited effect, with existing accounts still functioning normally. Some platforms even continued to accept new mainland clients through various workarounds after the rectification.

This time, the authorities are not holding back. The policy focus has shifted from restricting new inflows to rectifying existing accounts. All previous loopholes have been explicitly locked down by regulation.

II. "Written Declaration" in Hand, Account Opening Still Fails

As soon as the new rules were announced, the fastest-acting individuals bought tickets and flew to Hong Kong, but opening an account was not smooth. Over the past week, photos titled "Written Declaration for Mainland Investors" have circulated on social media, all from mainlanders who personally visited Hong Kong broker branches to try to open accounts.

Blogger AB Kuai.Dong described a friend's personal experience: they specially traveled to Hong Kong to apply for a US/Hong Kong stock account at the Yuanta Securities branch, were asked to sign the "Written Declaration for Mainland Investors," filled out all materials, waited over an hour, but were still told "account opening review failed." Blogger Simon also recorded a similar experience; a friend tried walk-in account opening, signed the declaration, waited over an hour, and ultimately also did not pass.

Judging from the declaration texts shared by multiple accounts, the content closely matches the requirements in the SFC circular annex. Brokers clearly moved swiftly to implement the new rules after they were issued.

It's noteworthy that signing may not guarantee account opening, but refusing to sign certainly prevents it. Blogger Li Zhi gave a straightforward interpretation: by having clients sign this declaration, brokers are essentially doing two things: first, shifting compliance responsibility—if something goes wrong, they can say "the client declared the funds were legal themselves"; second, screening clients—because most mainlanders trading Hong Kong/US stocks through Hong Kong brokers were already in a legal gray zone. This declaration requires them to confirm in black and white that funds come from overseas, acting as a filter in itself.

A May 27th report by Cailian Press also confirmed this phenomenon across almost all brokers in Hong Kong: starting May 26th, opening investment accounts through bank channels in Hong Kong required new documentation from clients, including signing a declaration on the legal source of funds. A Hong Kong foreign bank representative also confirmed to Cailian Press that the new requirement to sign such a declaration indeed exists.

Reportedly, the newly added document is titled "Cross-Border Disclosure Statement (Applicable to Investment Account Opening Applications)." According to documents shown by clients, the core content is: The applicant must confirm that "all funds used to support investment activities and related settlements originate from legal sources outside mainland China"; it also reminds mainland residents that investment account services are only for investors physically present in Hong Kong (e.g., living or working there) and that they should ensure the legality and compliance of fund sources.

The document clearly states that, to comply with relevant regulatory requirements in Hong Kong, banks may request clients to provide supporting documents. Failure to provide them may result in refusal of service, and existing services may also be terminated. Notably, not only new accounts are affected. An official customer service representative from a Chinese bank confirmed to Cailian Press that mainland investors who opened investment accounts between May 23rd and 25th, 2026, also need to sign the new version of the cross-border declaration, with no transition period granted by the policy.

III. Who Can Still Open an Account? Overview of Remaining Compliant Channels

This tightening directly shuts the mainland entry point for major internet brokers, but not all channels are closed.

Brokers that have completely stopped accepting new mainland clients: Futu Securities, Tiger Brokers, Longbridge Securities, Huasheng Securities. All four have closed new account opening channels. Some existing accounts can still trade normally for now, but by regulation, they can only sell unidirectionally, awaiting complete closure after the 2-year transition period.

Hong Kong licensed brokers that still maintain limited channels for mainland residents (as of article publication, the situation is still dynamically changing):

Yuanta Securities is currently one of the few Hong Kong brokers still supporting direct account opening for mainland users. It holds Hong Kong SFC Type 1, 4, and 9 licenses, and its US subsidiary is registered with the SEC and regulated by FINRA, boasting a relatively complete compliance system. However, according to the latest feedback on social media, after the new rules, Yuanta has significantly tightened its account opening review for mainland residents. Cases of walk-in opening failures have increased substantially. Whether one passes largely depends on whether the applicant genuinely meets the condition of "funds from outside mainland China."

Fosun Wealth and Chifu Securities are two other options still retaining channels for mainland users.

A blogger claimed that according to the latest official news from Fosun, their adjusted account opening policy is: no longer requiring proof of address, but applicants must use a VPN or personally go to Hong Kong for on-site application; users with Hong Kong virtual bank cards from ZA Bank, Tianxing Bank, HSBC, etc., must show a Hong Kong location during account opening. Odaily has verified with Fosun's official sources; this account opening policy is a rumor. Account opening still requires compliance with the aforementioned regulatory policies.

For users with overseas status (international students, work visa holders, overseas permanent residents, etc.), conditions are relatively more relaxed, but they also must be able to provide proof that funds originate from overseas.

Opening an account is just the first step. How to transfer money in is also a core constraint under the new rules.

The SFC circular clearly states that for mainland investor accounts, deposits, withdrawals, and settlements can only be conducted through accounts opened in the client's own name at licensed banks in Hong Kong or other qualified jurisdictions. Channels like transferring funds through third parties or unknown sources have been explicitly blocked. This means that previous methods to bypass foreign exchange controls, such as using money changers, transfers through friends, or USDT deposits, are no longer viable on a compliance level.

In practice, the prerequisite for smooth deposits is holding a real-name Hong Kong bank card. Hong Kong virtual banks like ZA Bank and Tianxing Bank support FPS (Faster Payment System) for normal deposits into brokerage accounts. Some brokers (like Yuanta Securities) also support eDDA fast deposit functions linked to ZA Bank. Therefore, for users without a Hong Kong bank account, securing a Hong Kong card before opening a securities account has become an essential step in the complete process.

Overall, after May 2026, compliant paths for ordinary mainland investors to trade Hong Kong and US stocks have narrowed significantly but are not completely closed. Based on the current situation, several paths are still viable.

Most Stable Path: Compliant Status, Compliant Fund Channel, and Hong Kong Bank Account. International students, overseas work visa holders, Hong Kong/Macau residents, with overseas documentation, can still open accounts at licensed brokers like Yuanta, Chifu, and Fosun, provided they meet the "funds from outside mainland China" condition. Tourists face a certain possibility of failure, especially regarding the source of funds.

Policy-Compliant Channels: Stock Connect, QDII, Cross-border Wealth Management Connect. These are the directions regulators explicitly hope to guide funds towards. Although product choices are limited and there are quota ceilings, they are fully compliant. Funds from affected mainland investors are expected to gradually shift to these channels.

On-Chain Paths: Platforms like Hyperliquid and xStocks offer technical alternatives for users who meet their account opening requirements. However, it must be noted that such on-chain products operate within clear compliance boundaries. Recently, many projects offering Hong Kong stock crypto products have explicitly announced in response to Hong Kong's new regulations that they will no longer provide such products. Additionally, most of these products do not accept registrations from mainland Chinese users, making them more suitable for users residing overseas.

Conclusion: Significant Tightening, But Opportunities Still Exist

This tightening is a concentrated release of long-simmering contradictions. The unchecked expansion of Hong Kong brokers into the mainland client base over the past few years undoubtedly brought substantial user growth but also left significant compliance hazards, including document forgery, unclear fund sources, and misuse of dormant accounts. The synchronized strike from regulators on both sides sends a clear signal to the market: The gravy train of this gray channel is over.

For mainland investors who still wish to allocate funds to Hong Kong and US stocks, the path ahead will not be easier, but compliant options still exist. Which path to take depends on one's personal status, risk tolerance, and self-assessment of compliance boundaries. Regardless, before signing any written declaration, one should be clear: once you sign, legal responsibility falls on you.

(Odaily Note: This article synthesizes official SFC circulars, CSRC announcements, reports from Cailian Press, Yicai, and other media, as well as first-hand social media information. For informational reference only, not investment advice.)