Author: Prathik, Thejaswini

Original Title: Built for Humans

Compiled and Edited by: BitpushNews

For thousands of years, human civilization has evolved in countless ways. Our languages, clothing, lifestyles, architectural structures, community forms, methods of obtaining food, and more have constantly changed. However, human civilization has always had one thing in common—the impulse to speculate.

Before the concept of the "church" was born, before the "state" emerged, humans were already gambling. Among all the activities that humans have consistently engaged in across cultures and centuries, betting on uncertain outcomes ranks almost alongside cooking and burying the dead.

The oldest known dice date back more than 5,000 years. They were discovered in a set of backgammon-like game pieces unearthed from a burned city in modern-day Iran, dating to around 2800 BC. In the 6th century BC, chariot racing gambling was widely popular in ancient Rome, attracting all social classes from senators to slaves. The turning point of the Indian mythological war epic "Mahabharata" occurs during a dice game. All four Gospels of the Bible record soldiers "casting lots" to divide Christ's garments after crucifying him.

Every civilization of every era, whether recorded in history or in artificially compiled epics, found ways to wager real wealth on uncertain outcomes. This suggests that the desire to say "I know something the world does not" and be rewarded for that knowledge is inseparable from human nature.

Times change, venues change, but the gambling impulse remains. In fact, it evolves over time.

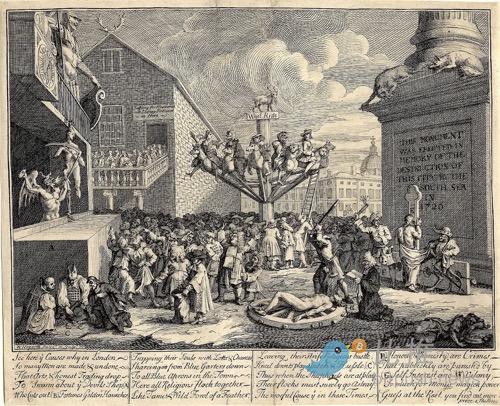

In 1720, the South Sea Company offered the British a tradable future interest. The promise of converting government debt into stock triggered a speculative frenzy, driving the share price from about £100 in 1719 to nearly £1,000 in 1720. The potential trade never materialized, and the speculation ended in the infamous financial collapse—the "South Sea Bubble," equivalent to the 18th century's dot-com bubble burst. Subsequently, the British Parliament banned future speculative ventures.

The craving for speculation remained, just waiting for the next venue.

Throughout the 20th century, traditional finance meticulously built a complex structure of access controls in an attempt to rekindle this impulse—they designed a whole set of checks and balances: accredited investor thresholds, day trader restrictions, markets that close at 4 PM and reopen the next morning. The underlying message to the average person was: "You can speculate, but only if you're already wealthy enough, only on our schedule, and only after filling out all the forms."

These inconveniences annoyed many, but there was no alternative at the time. Until new choices emerged.

Look at what happened in the silver market last month.

This precious metal is one of the oldest traded commodities on Earth. It has its own futures market, institutional infrastructure, and centuries of price history. In January of this year, the decentralized exchange (DEX) Hyperliquid launched a silver contract.

Within a month, it processed 2% of global silver trading volume. Not 2% of crypto silver trading volume, but 2% of *global* silver trading was conducted through a protocol with no headquarters, no CEO, and no brokers.

It's worth exploring where this volume came from. Hyperliquid's existing user base is primarily crypto-native. However, the silver market is not. Considering the risk of over-assumption, the most reasonable explanation for the data I found is that this market attracted traders who had always wanted this risk exposure but were unwilling to bear the friction of traditional infrastructure.

Hyperliquid eliminated most existing barriers, including brokers, high margin and minimum account requirements, interface friction, and offered high leverage and lightning-fast settlement speeds. Want to express your view at 3 AM on a Saturday? No problem, just open the platform, connect your wallet, and express your heart out.

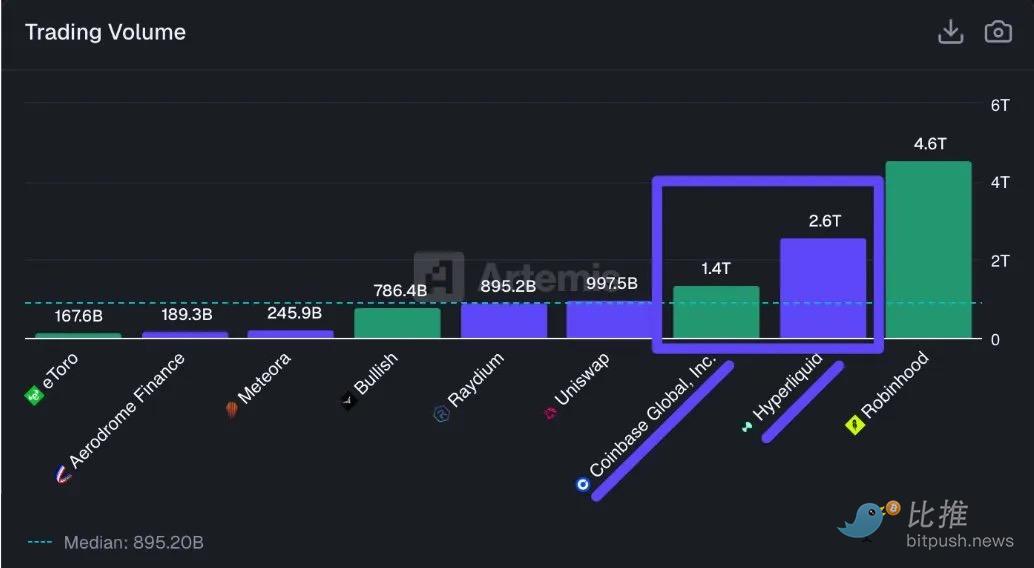

Last month, Hyperliquid processed $2.6 trillion in notional trading volume, nearly double that of Coinbase.

But comparing it to other crypto exchanges is secondary. More importantly, perpetual contract DEXs offer humanity a choice beyond existing traditional financial infrastructure. Do not mistake the elimination of friction for the elimination of risk. This frictionless access at 3 AM also makes it possible to lose your shirt at such an ungodly hour. But isn't that the whole point of speculation? High returns come with high risk. It is this unconstrained risk that completes the adrenaline-pumping experience inherent in any gamble.

But gambling was never just about returns. It's also about "proving oneself right."

Every civilization has had its oracles. The Oracle of Delphi in ancient Greece charged consultation fees for delivering prophecies. Medieval courts often hired astrologers as advisors. The modern version is TV experts being handsomely rewarded for expressing opinions on screen with confidence and charm.

Opinions have always had social and economic value. However, until recently, what they lacked was a common market price.

This is where prediction markets come in. They monetize opinions. When you buy a contract on Polymarket or Kalshi, you are no longer just expressing a view into the void. Your conviction is being continuously priced against a counterparty who disagrees with you. If you're right, you collect; if you're wrong, you pay. This incentive structure and oracle create an accountability mechanism that ancient commentary never had.

What interests me more is not the existence of contemporary prediction markets, but where they are ultimately headed.

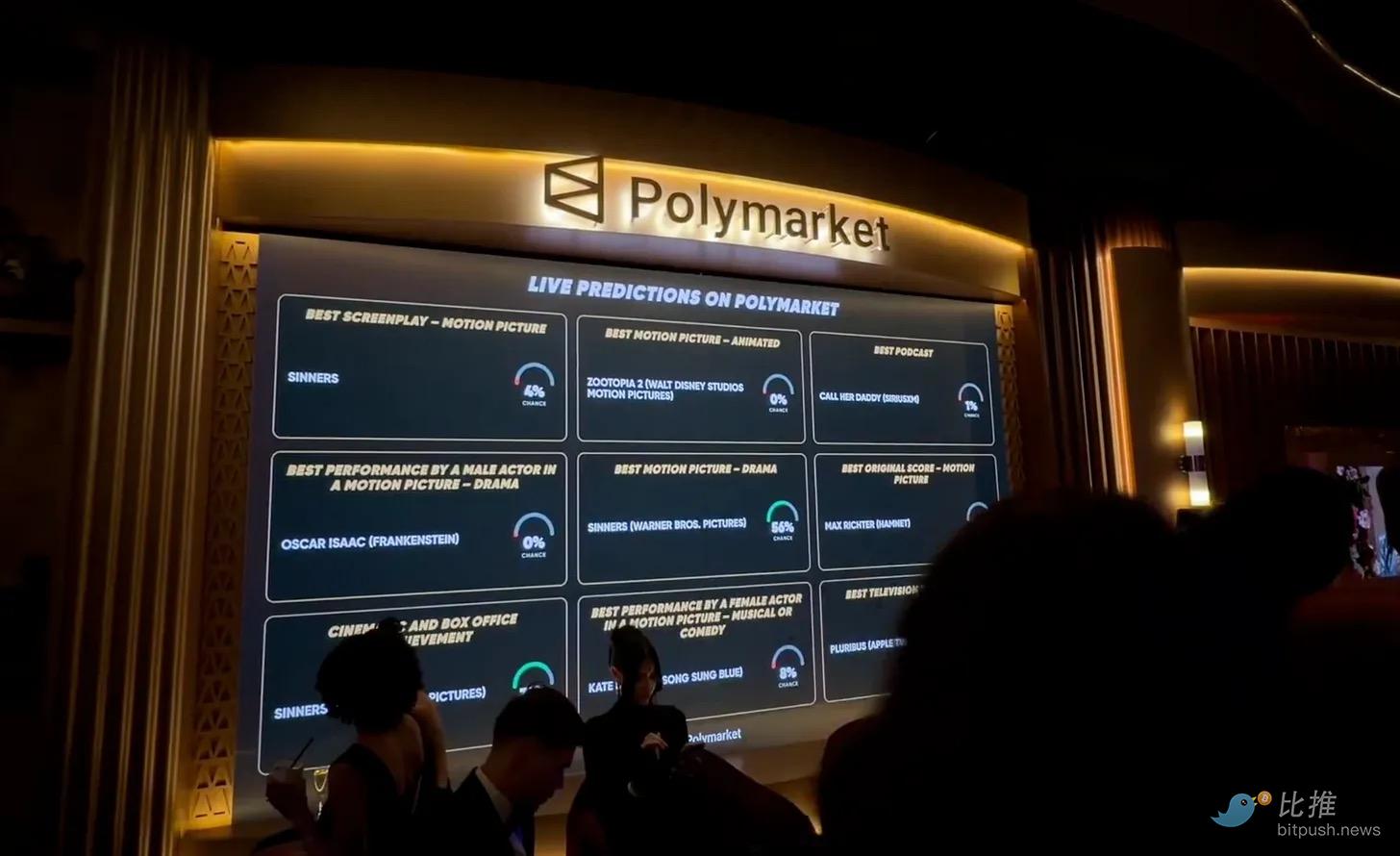

This year's Golden Globes broadcast partnered with Polymarket to read out odds before every commercial break. CNN and CNBC have both signed data deals with Kalshi. Robinhood launched prediction markets, which became its fastest-growing revenue line, with an annualized run rate of about $300 million. On Super Bowl Sunday this month, prediction markets saw over $1 billion in daily volume. Kalshi even partnered with Venmo for payment integration.

These developments are not targeting crypto-first individuals. They are aimed at sports bettors and political enthusiasts seeking to turn what they believe they know, but the market does not, into money.

While some see prediction markets as the future of news, their limitations cannot be ignored. The issue of insider trading is always present. But what excites me most is how these markets open up a new set of primitives for solving everyday problems. Think hedging and insurance.

Not every speculative venue is built on such solid foundations.

In January 2024, pump.fun launched, allowing anyone to create a tradable token in seconds. The world evolved from having fewer than 10 meme coins launched over years, to over 70,000 tokens launched in a single day at peak. This frenzy was supported by broad participation, with people betting on tokens built around jokes, collective sentiment, and even political figures. It even extended all the way to US President Donald Trump.

The TRUMP token, launched just days before the presidential inauguration, attracted people from all over the world to buy. It was a reminder of how, throughout ancient history, people have always put money on cultural movements. Cryptocurrency simply made the whole process programmable, frictionless, and instantaneous.

This is where I find cryptocurrency humbling. It doesn't get bogged down in moral right or wrong. Yet, the same system that helped Hyperliquid generate roughly $1 billion in revenue also enabled the token issuance platform pump.fun to earn over $900 million.

Cryptocurrency never offered a perfect system from the start. It often introduced flawed systems as alternatives to traditional incumbents. But interestingly, over time and through multiple iterations, some of these systems evolved into frictionless, more efficient, permissionless venues, exhibiting both sophistication and recklessness.

We saw this pattern in the evolution of capital formation systems. The Initial Coin Offerings (ICOs) of 2017 made a radical promise: anyone could bypass venture capital thresholds to fund and invest in projects. In reality, most of them failed or were fraudulent. But what followed was iteration and honest reflection on why they failed. Each generation of crypto financing solved one problem while introducing a new one. The result is that the frameworks we see now do a better job of addressing these challenges than the early primitives.

The fact that many projects today generate auditable revenue before issuing tokens is a testament to the maturation of the capital formation industry. I don't see any idealism in this. If anything, the industry has become more practical about which markets can be sustained.

This shows how the speculative layer has matured over time to meet the same human impulse that has spanned millennia: the desire to gamble.

Beyond speculation, cryptocurrency has also enabled infrastructure to meet another pressing human need: the transfer of money.

Although stablecoin settlement data is still debated, the place where they see their deepest application is not the trading desk. They are adopted in countries like Argentina, Nigeria, and Venezuela, where inflation, fragile economies, and weak currencies prompt residents to use these digital dollar equivalents for daily commerce.

Stablecoins found their product-market fit where traditional institutions, such as banks and governments, stopped serving local citizens.

Then there is an impulse even older than speculation: ownership.

Long before humans gambled, they asserted sovereignty. Territory, livestock, and granaries. The concept of "this is mine" is arguably our species' most fundamental economic act. From the Code of Hammurabi to British common law, most of the energy of every legal system ever devised has been spent defining and protecting "who owns what."

Traditional finance built complex systems to serve this impulse. Deeds, titles, stock certificates, custodians, transfer agents, and clearinghouses—an entire industry of intermediaries whose purpose is to record and verify that you indeed own what you say you do. But we have a problem: this infrastructure is slow, expensive, and exclusive. Settling a stock trade still takes a full business day. Transferring property can take months. For billions of people globally, many of these asset classes remain completely out of reach.

Tokenization attempts to compress this entire stack of intermediaries into code. A tokenized US Treasury is still a US Treasury. A tokenized ounce of gold is still an ounce of gold sitting in a vault. What changes is how ownership is recorded, transferred, and used. Settlement becomes instantaneous. Access becomes global. And assets that once sat idle in custodianship become programmable and composable.

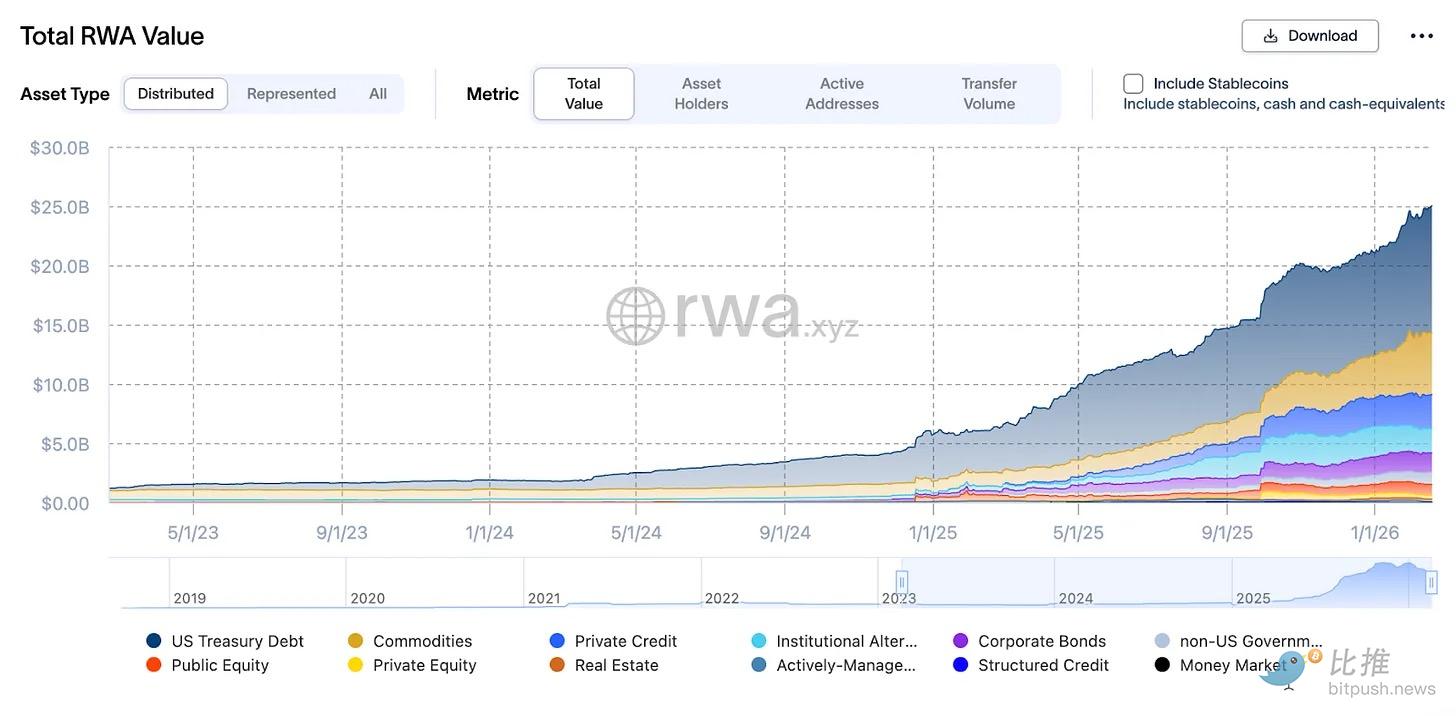

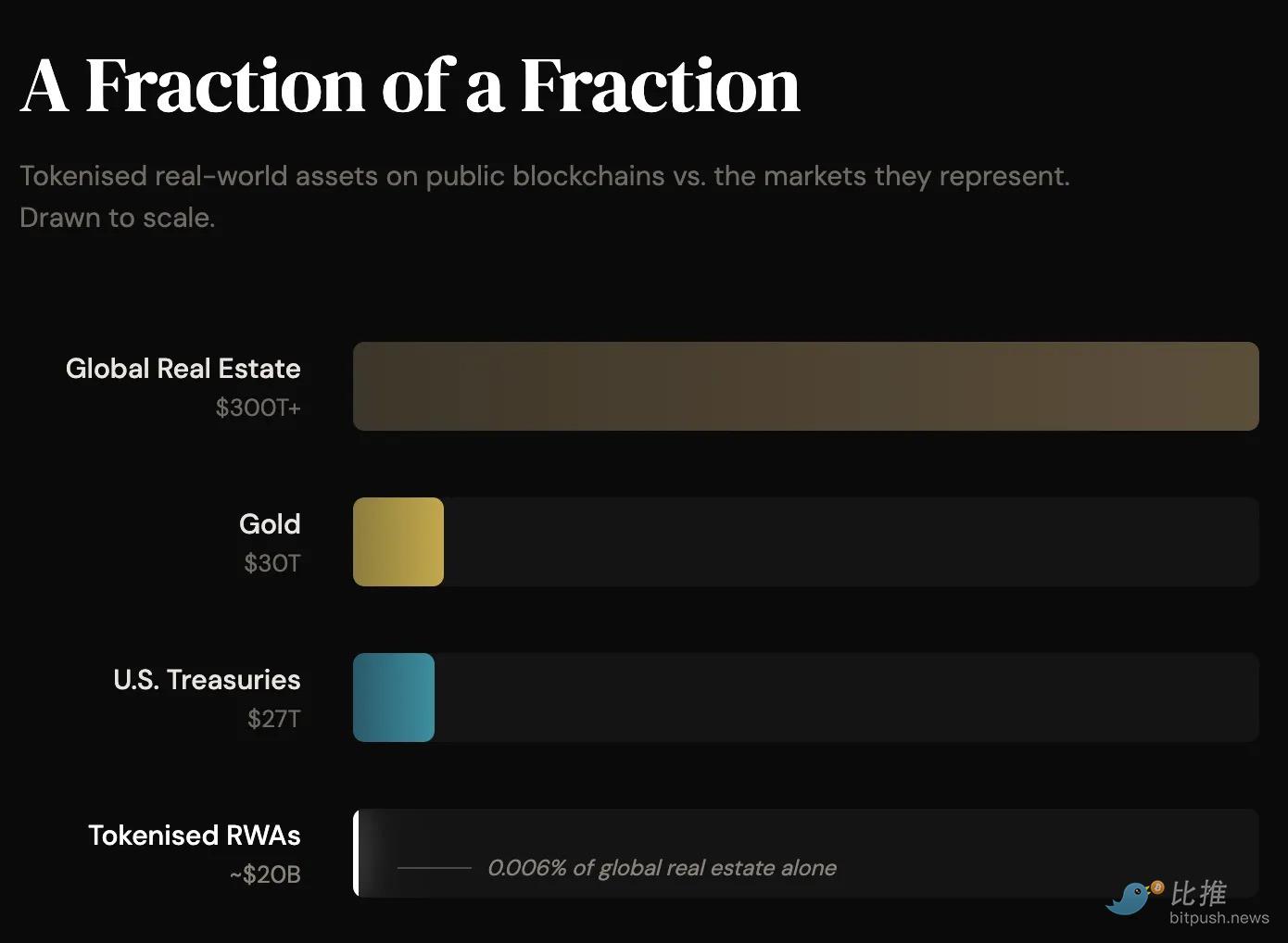

Tokenized real-world assets (RWAs) on public blockchains are approaching $20 billion. Tokenized US Treasuries alone surpassed $10 billion in January this year, a tenfold increase in less than two years; tokenized gold has exceeded $6 billion.

These are meaningful milestones for cryptocurrency, but the share occupied by tokenization is still a tiny fraction of global assets. The global gold market is over $30 trillion. The US Treasury market is $27 trillion. The global real estate market is over $300 trillion. Honestly assessed, it is still early days.

What has shifted recently is not the market size, but the identity of the participants.

On February 11 this year, BlackRock placed its tokenized US Treasury fund, BUIDL, for trading on Uniswap, one of the largest decentralized exchanges in crypto. The world's largest asset manager, overseeing $10 trillion, chose to use public DeFi infrastructure to settle tokenized government bonds. Subsequently, it also purchased the protocol's governance token.

This deal was a year and a half in the making, partly facilitated by Uniswap's former COO, who previously founded BlackRock's digital assets division. Meetings alternated between BlackRock's offices in Hudson Yards and Uniswap's headquarters in SoHo. It's hard to imagine two more symbolically different offices.

US Treasuries are the foundational collateral of the global financial system. They underpin the $5 trillion repo market, the overnight "plumbing" that maintains bank liquidity. Leverage is created based on them. Structured products are anchored to them. Stablecoins are backed by them. When this collateral moves on-chain, the instruments built on top of it follow. Lending protocols gain high-quality collateral. Derivatives infrastructure gets connected. Stablecoins become pegged to verifiable on-chain reserves, not off-chain attestations.

BlackRock's BUIDL is increasingly becoming the cornerstone for other on-chain products. Ethena's USDtb and Ondo's OUSG both use it as a core reserve asset. It has been accepted as collateral by centralized exchanges. It has expanded to multiple blockchains. What started as one tokenized fund is quietly becoming the infrastructure upon which other products are built.

This follows the same pattern. Hyperliquid didn't invent commodity trading; it just removed friction. Stablecoins didn't invent the dollar; they just made it flow to places banks wouldn't touch.

Tokenization didn't invent ownership. It made ownership programmable, portable, and globally accessible—features the existing intermediary stack was never designed to support.

JPMorgan already runs tokenized payments through its Onyx platform. Goldman Sachs operates digital asset infrastructure for institutional clients. The Canton Network, backed by BNY Mellon and Deutsche Börse, is building permissioned DeFi infrastructure. And now, BlackRock sits at Uniswap's table, holding the governance token of a protocol built by anonymous developers.

This mirrors the path stablecoins once walked. First skepticism, then cautious experimentation, and finally a quiet admission: for certain use cases, this infrastructure simply works better. Tokenization is still in the second phase. On-chain assets are still a drop in the bucket compared to what they represent. But the direction of travel is no longer in question; the suspense lies only in the pace.

Those technologies that have changed human life in the most profound ways share a common characteristic: they become "invisible." Their value is only realized when they fail.

Before the COVID-19 pandemic brought supply chain issues into the mainstream, no one thought about shipping containers when ordering new electronics online. People don't care about the submarine cables that transmit 99% of international data. These technologies are so embedded in daily life that their presence is often overlooked, and their absence becomes unimaginable.

Perpetual contract DEXs returned the right to express financial views and act on them to ordinary people, a right that accredited investor rules had taken away;

Prediction markets allow people to put their money where their mouth is;

Tokenization gives global investors access to assets that were previously locked away due to geographical restrictions;

All these primitives address the same appeal: the existing system was built for insiders, while restricting access for outsiders.

The circulating supply of stablecoins has skyrocketed more than sixfold in the past five years, from a mere $4.5 billion $307 billion. Although cryptocurrency has existed for over fifteen years, the focus on developing institutional-grade privacy protections in recent years has led more institutions to evaluate alternatives to traditional infrastructure for cost-effectiveness.

After enduring failures, frauds, the casino-era frenzy, and countless iterations, cryptocurrency has finally built an alternative system—one that requires no permission, yet allows people to satisfy that timeless need: to express their views.

Today, crypto is often viewed negatively due to long sideways price movements, criticized as a castle in the air. But what is overlooked is its seemingly dull underlying layer—precisely the layer that satisfies one of humanity's oldest impulses: whether it's speculation or the transfer of value. It is at this point that crypto's domain has quietly evolved into an indispensable existence, silently embedded into the crevices of daily life.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush