Author: Chloe, ChainCatcher

On February 26, 2026, on-chain detective ZachXBT officially unveiled the truth behind the Axiom Exchange insider trading case: a senior business development employee had abused backend permissions for ten months, tracking KOLs' private wallets to front-run trades, illegally profiting over $400,000. This report not only concluded the case but also settled the high-stakes prediction market on Polymarket, which had held the entire market in suspense with a betting pool of $40 million.

However, beyond the truth, ripples remain. Before the investigation's results were revealed, the market had unanimously pointed fingers at Meteora, whose implied probability once soared to 43%. This was not baseless speculation. According to crypto asset data platform RootData, Meteora is backed by a Singaporean-Malaysian founding team core of Meow and Ben Chow. They rose from the ashes of Mercurial Finance and built a full-stack matrix within the Solana ecosystem encompassing traffic entry points, trading aggregation, and liquidity infrastructure.

From past controversies like the LIBRA dispute, the MET airdrop scandal, to the Upbit listing rumors, Meteora's development history has always lingered in the gray area of "information asymmetry arbitrage." Although ZachXBT ultimately targeted Axiom, the various clouds of suspicion surrounding Meteora seem never to have been truly answered.

From Mercurial to the "Jupiter System," the Foundational Connection Remains

The starting point of everything traces back to 2021, when the pseudonymous Meow and Ben Chow founded Mercurial Finance on Solana, positioning it as a stablecoin asset management protocol aiming to be the Solana version of Curve. In that liquidity-surged bull market cycle, Mercurial not only received support from Alameda Research but also completed an IEO (Initial Exchange Offering) on the FTX platform with SBF's personal endorsement. Its TVL once accounted for 10% of the Solana ecosystem, a truly glorious time.

The collapse of the FTX empire in 2022 severely wounded Mercurial. However, the two founders did not choose to liquidate and leave but embarked on a rebuilding path called the "Phoenix Plan": splitting the business in two. Meow led Jupiter, aiming to solve Solana's liquidity fragmentation by defining optimal prices through routing algorithms; Ben Chow took the helm at Meteora, focusing on developing a highly capital-efficient Dynamic Liquidity Market Maker (DLMM) model. This split,表面上 (superficially) was about business focus, but in reality, it formed two independent brands with complementary flywheels, yet they were always connected in terms of shareholder structure and underlying logic.

On the traffic front, Jupiter pursued an aggressive strategy. According to crypto asset data platform RootData, in January 2025, Jupiter acquired Moonshot, successfully creating the shortest path for retail users to directly purchase meme coins via Apple Pay or credit cards, flattening the consistently high barrier to entry in the crypto industry to a consumer-grade level.

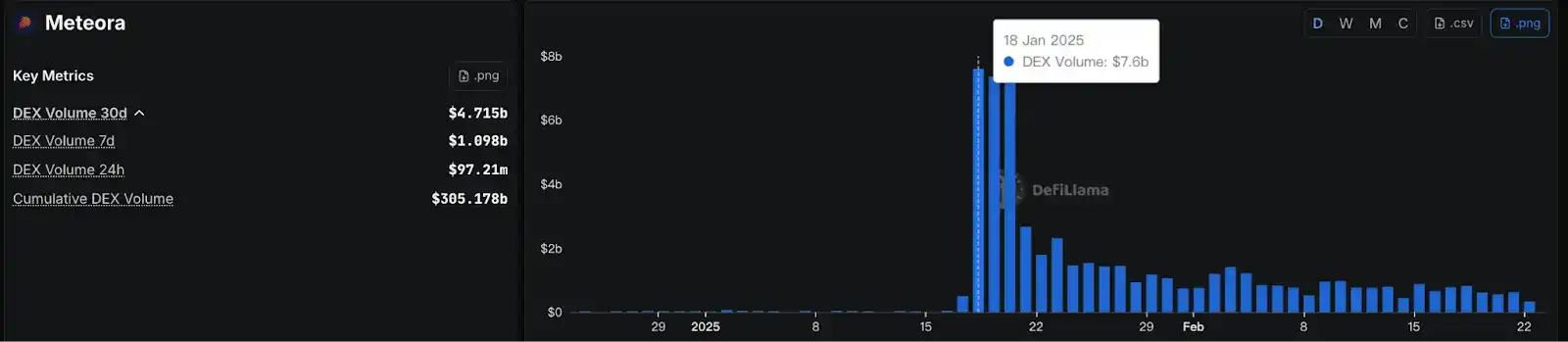

This布局 (layout) was successfully monetized during the TRUMP token frenzy: when a massive flow of retail traffic poured in through Moonshot, these buy orders precisely hit the initial liquidity the TRUMP team had established on Meteora. This closed loop of "front-end capturing traffic, back-end executing trades" enabled Meteora to achieve a single-day trading volume of $7.6 billion, capturing 20% of the DEX trading share on the entire Solana chain.

Simultaneously, Jupiter's flagship DEX aggregator evolved into a cornerstone of the Solana ecosystem. It is no longer limited to token swaps but has continuously iterated products, introducing perpetual contracts, lending markets, prediction markets, and more. Thus, Moonshot, Jupiter, and Meteora constructed a full closed-loop ecosystem spanning fiat on-ramps, front-end traffic, trading routing, multi-functional products, and automated market making, completing the transition from "project party" to "ecosystem controller."

Meteora's Airdrop Controversy and Upbit Listing Suspicions

Although vertical monopoly brought efficiency, the ensuing information asymmetry and suspicions of power abuse have always loomed over the Jupiter system. Among these, the airdrop distribution of Meteora (MET) and the Upbit listing风波 (incident) led outsiders to question whether this was truly "community first."

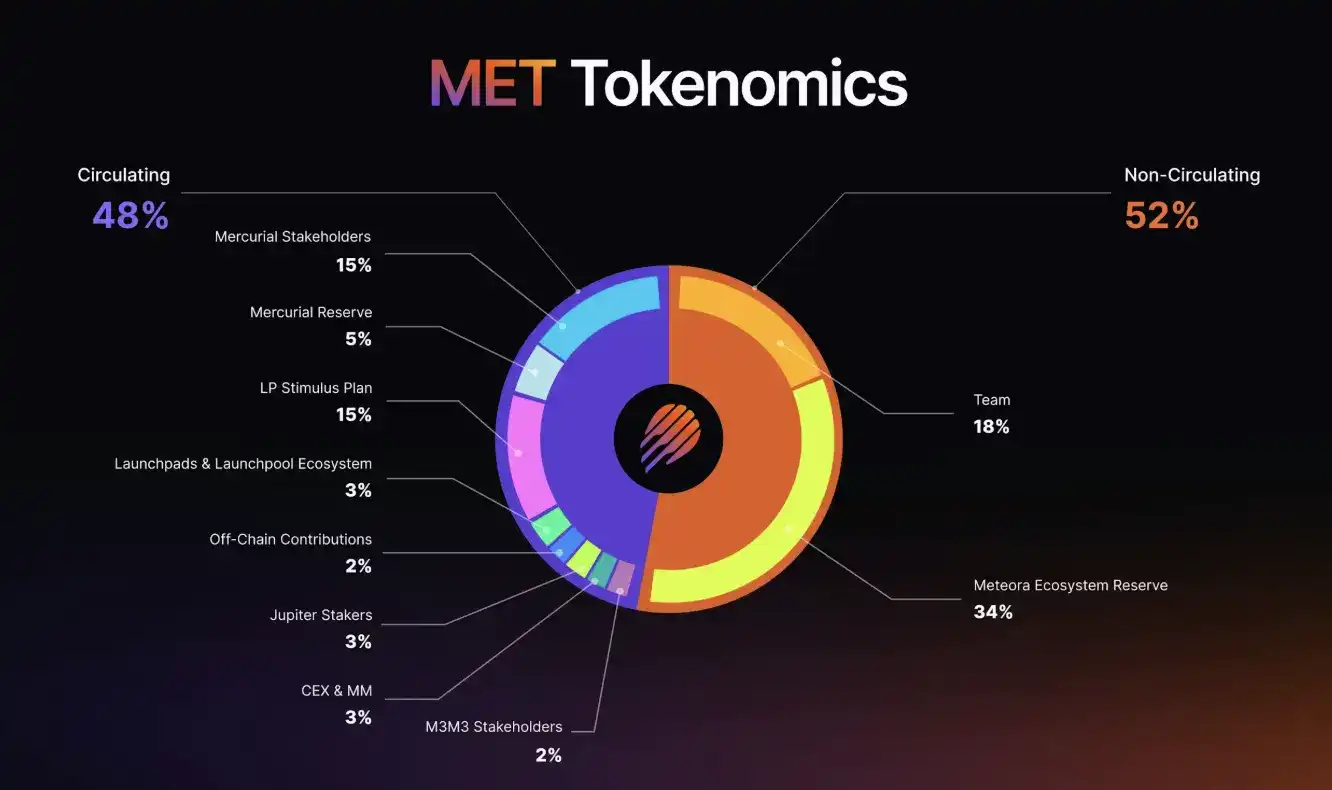

On October 23, 2025, Meteora had its TGE (Token Generation Event). At that time, 48% of the total token supply (i.e., 480 million tokens) was fully unlocked and entered circulation at once. The team claimed this was intentional to achieve "true price discovery," but the market's answer was brutally negative. MET plummeted from $0.90 to $0.51 within hours of opening, a single-day drop of over 55%.

According to on-chain data from the initial TGE period, there were significant flaws in the fairness of the airdrop distribution. The top 4 claiming addresses took approximately 45.94 million tokens, accounting for 28.5% of the total claimed. The behavioral patterns of these addresses were anomalous:

-

Suspicious Address 1 (3vAau...ae): Claimed 12.15 million MET (worth $6.31 million at the time). This address had not only previously claimed the Mercurial (MER) airdrop but had also sold over 30 million JUP to exchanges in the past, employing the same dumping strategy now transferred to MET.

-

Associated Addresses 2 & 3: These two addresses exhibited extremely high synchronicity. Their JUP transfer amounts were repeatedly locked at the specific figure of 2,622,632.41, and their activity times were completely identical, likely belonging to a group controlled by the same entity.

-

Address 4: Claimed 10 million MET. Bizarrely, this address was created *after* the snapshot time and had never participated in any liquidity provision or staking activities. This "out-of-thin-air" claim completely defied the logic of the points mechanism.

If the airdrop distribution was a display of power corruption and abuse, then the information leak regarding the exchange listing touched the industry's gray area. On November 18, 2025, Meteora officially listed on Upbit, but well before the official announcement, insiders claimed to have known this information and profited from the leaked insider information. Although there is no direct evidence pointing to the Jupiter or Meteora core teams, combined with the MET airdrop controversy, it has already led the community to label them with distrust.

The LIBRA Scandal: Ben Chow's Resignation and the Responsibility Enigma

Rewinding to February 2025, the LIBRA token, endorsed by Argentine President Javier Milei, exploded onto the scene, its market cap soaring to $4.6 billion within hours before nearly crashing to zero, resulting in over $280 million in losses for tens of thousands of investors. The舆论炮火 (barrage of public criticism) quickly targeted the Meteora and Jupiter teams, with外界指控 (external accusations) that the team, knowing the token launch involved scientist front-running and wash trading, still provided a "Verified" label and liquidity support for LIBRA. Although the team insisted the verification was only to prevent fake tokens, not an endorsement, the public clearly didn't buy it.

Under public pressure, Meteora's core leader Ben Chow announced his resignation and hired the law firm Fenwick & West to conduct an independent investigation. However, this move instead triggered a secondary crisis: Fenwick & West was itself deeply embroiled in class-action lawsuits stemming from the FTX collapse, with外界指控 (external accusations) that the firm had assisted SBF in blurring the financial boundaries between FTX and Alameda Research.

The community's reaction was almost uniformly sarcastic. Using a former FTX legal advisor, itself entangled in lawsuits, to "independently investigate" the ethical issues of a former FTX-affiliated project—this method of "using controversy to handle controversy" made outsiders even more suspicious about whether the Jupiter system was truly willing to move towards transparency. Although Meow eventually stated under public pressure that they would reassess the choice of legal counsel, there was no subsequent follow-up explanation.

The Double-Edged Sword Impact of Vertical Monopoly on the DeFi Ecosystem

For the average user, vertical monopoly means extreme efficiency. When you use Moonshot for on-ramping, find a route through Jupiter, and finally complete the trade in Meteora's pool, the entire pathway is optimized by the same team, reducing transaction failure rates and experience friction to a minimum. Furthermore, because the team controls both traffic and liquidity, they can quickly foster tokens with phenomenal potential like TRUMP, thereby maintaining Solana's popularity and on-chain activity.

However, for the entire ecosystem, this high degree of concentration is almost synonymous with high risk. When a single team simultaneously controls front-end traffic, trading routing weight, lending markets, and liquidity pools, once its core private keys face security issues, or core members are forced to halt operations due to legal disputes, liquidity could suffer a severe blow in a short period.

More noteworthy is the issue of "innovation monopoly." Jupiter controls most of the order flow routing on Solana. Emerging DEXs, if not integrated into Jupiter's ecosystem, almost lose the basic condition for acquiring traffic. This oligopolistic pattern at the routing level essentially constitutes an invisible market barrier—success is determined not by product superiority but by proximity to Jupiter. More worryingly, Jupiter itself participates in the liquidity business through Meteora, creating a clear conflict of interest between "directing traffic flow" and "being a beneficiary of that traffic."

Conclusion: The Shadow of the Jupiter System, and the Market's Unanswered Questions

ZachXBT ultimately exposed Axiom, but this does not mean Meteora, or the entire Jupiter system, is清白 (innocent). It may only mean that the scope of ZachXBT's investigation did not cover them this time, or that direct evidence was lacking.

The controversy surrounding Meteora has never been a black-and-white legal issue; it is a superposition of a series of gray areas: the utilization of information asymmetry, airdrop disputes, the choice of legal counsel, and even the repetitive excuse of 'we only provide infrastructure' after every high-profile token collapse.

This founding team from Singapore and Malaysia has indeed demonstrated its product execution capability to the market over the past three years, but they have also fully arbitraged every regulatory gray area with their business logic. Trust in the crypto industry has never been this easy. When the traffic entry points, trade execution, and liquidity of an ecosystem are controlled by the same community of interest, the cost is ultimately borne by retail investors.

The Polymarket bet is over, but regarding Jupiter and Meteora, the market still hasn't gotten its answers.