Author:Shaun Paul Lee

Compiled by: Deep Tide TechFlow

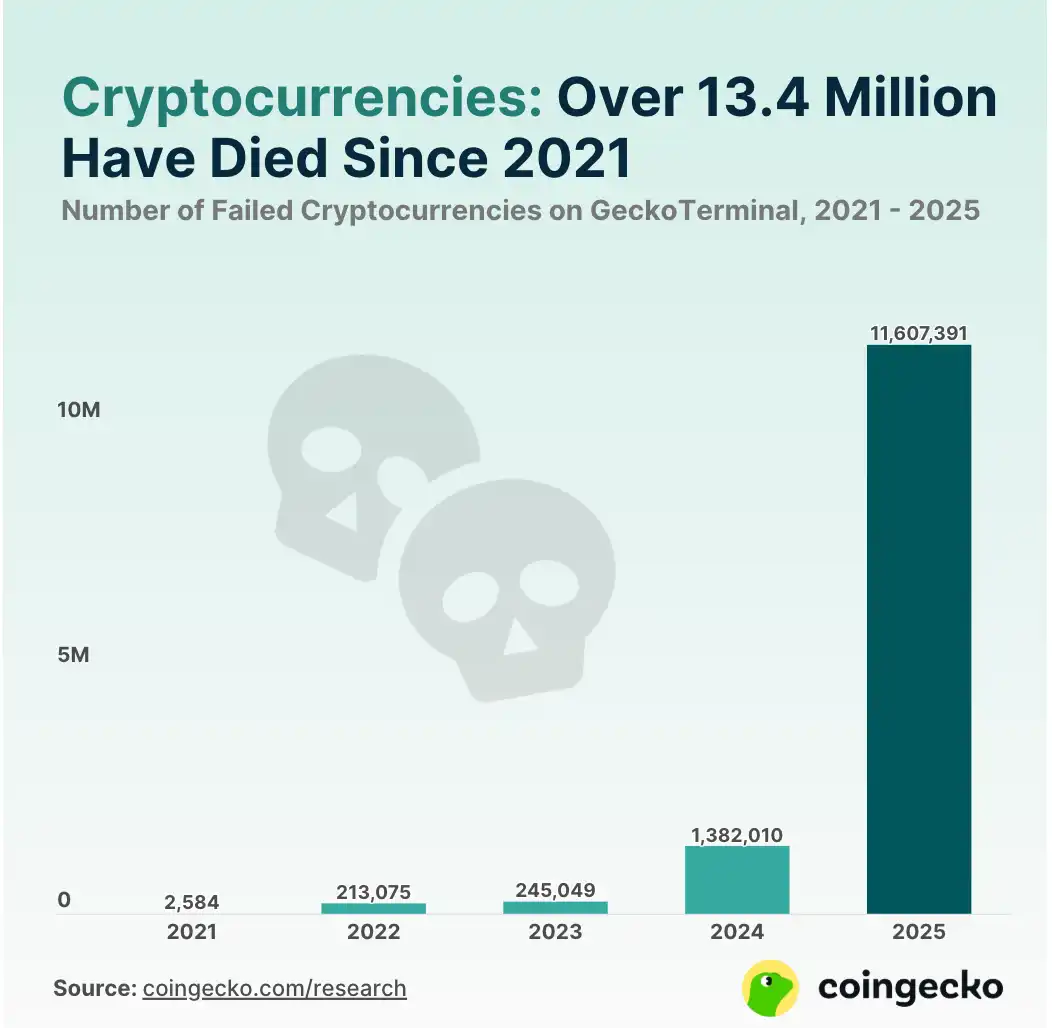

How Many Cryptocurrencies Have "Died"?

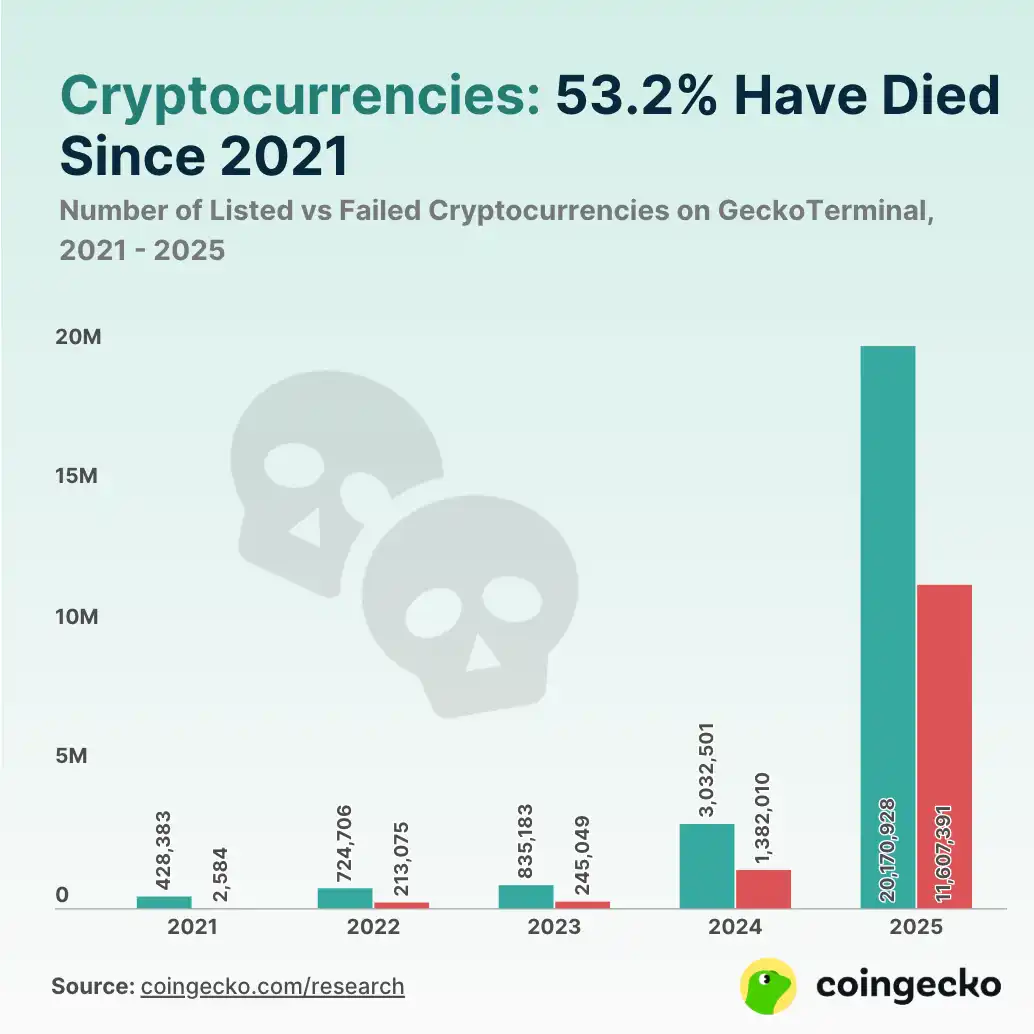

According to data from GeckoTerminal, 53.2% of cryptocurrency projects have failed, with the majority of these failures concentrated in 2025. In 2025 alone, 11.6 million token projects came to an end, accounting for 86.3% of all failed projects. This phenomenon is closely related to the severe market turbulence throughout the year, particularly the impact on the memecoin sector.

This sharp decline in token viability may be related to the market turmoil throughout the year, especially affecting the meme coin sector.

Shockingly, the fourth quarter of 2025 alone saw 7.7 million token projects collapse, accounting for 34.9% of all failed projects. This sharp decline is closely linked to the "liquidation chain reaction" that occurred on October 10. In this record-breaking event, a staggering $19 billion in leveraged positions were liquidated within 24 hours, making it the single largest day of deleveraging in cryptocurrency history.

Despite the extreme volatility in the cryptocurrency market in 2025, the total number of cryptocurrency projects grew dramatically. From 428,383 projects on GeckoTerminal in 2021, this number had surged to nearly 20.2 million projects by 2025. This growth is largely attributed to the rise of various token issuance platforms, which made creating low-quality memecoins and projects exceptionally easy.

86.3% of Cryptocurrencies Died in 2025

As of December 31, 2025, a total of 11.6 million cryptocurrency projects had failed, setting a new historical record for the number of failed projects in a single year. These failed projects account for 86.3% of all failure cases between 2021 and 2025.

This was followed by 2024, which saw approximately 1.4 million project failures, accounting for 10.3% of the total failures over the past five years. 2024 was also the second-highest peak for the growth in the number of cryptocurrency projects, with over 3 million new projects entering the market. However, before the launch of the pump.fun platform in 2024, the number of cryptocurrency failures remained at a relatively low six-figure level. In contrast, the total number of failed projects between 2021 and 2023 accounts for only 3.4% of the total failures over the past five years.

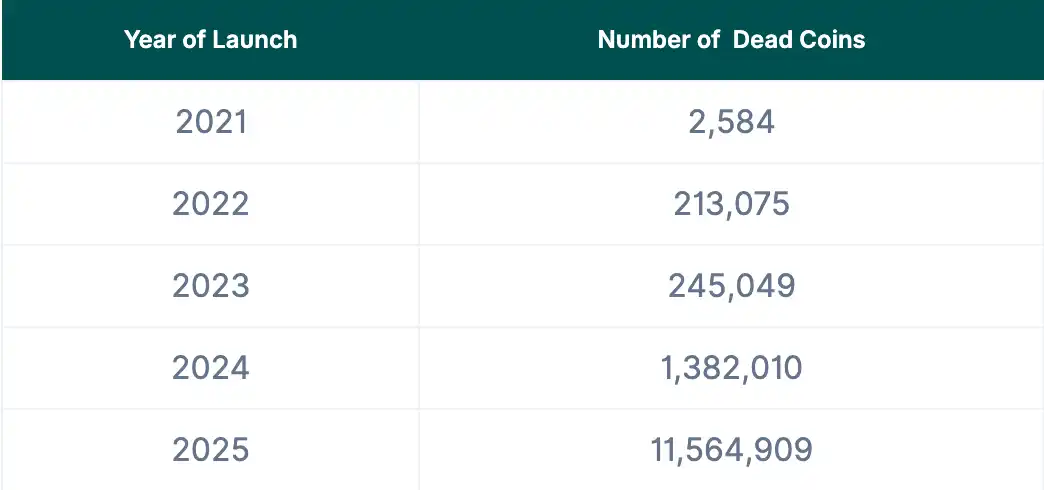

Year-by-Year Statistics: Cryptocurrency Failure Data

The following statistics show the number of failed cryptocurrency projects each year from 2021 to 2025:

Research Methodology

This study analyzed tokens and cryptocurrency projects (collectively referred to as "cryptocurrencies") that were once listed on GeckoTerminal between July 1, 2021, and December 31, 2025, but are no longer actively traded. These projects are classified as "failed" or "dead" and are grouped according to the year of their last active trade.

- Only tokens that had at least one trade before failing are counted.

- Additionally, only token projects that had "graduated" within the pump.fun platform were included.