Author:Artemis

Compiled by: TechFlow

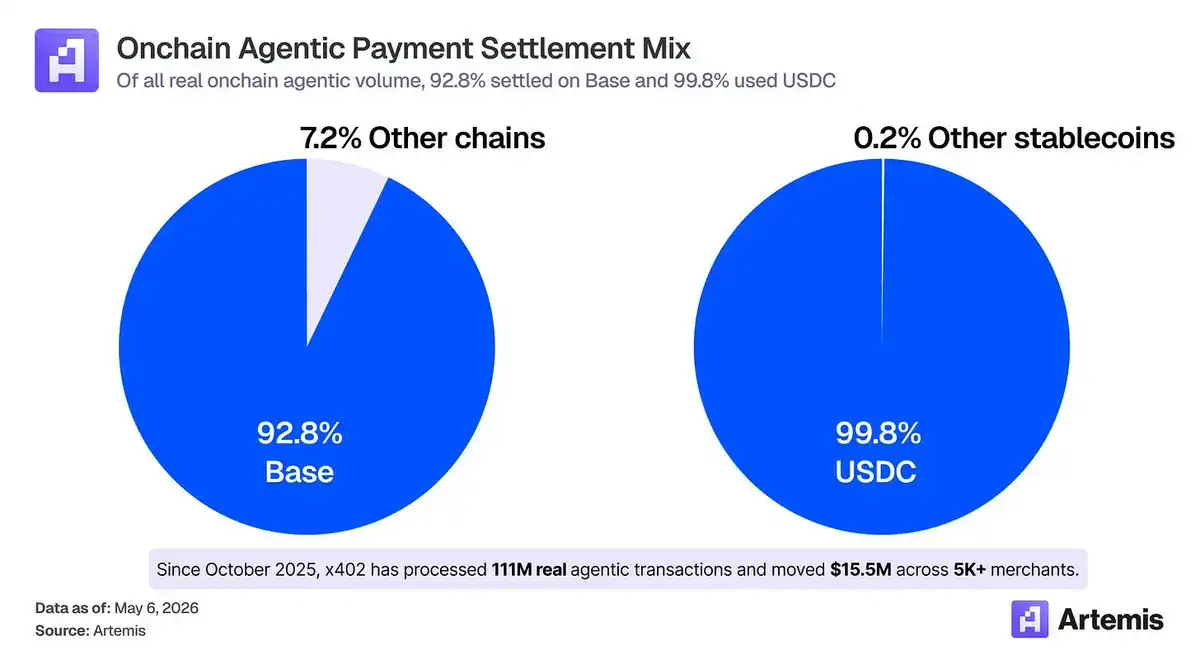

TechFlow Insight: Wall Street treats Coinbase like a brokerage firm that follows Bitcoin's ups and downs, giving it a valuation half that of Circle. But data shows 92.8% of AI agent payments happen on Base, and 99.8% are settled with USDC—Coinbase has become the underlying infrastructure for AI-native finance, not just an exchange. If McKinsey's prediction of a $5 trillion AI agent commerce market by 2030 is even half realized, Coinbase's valuation logic will need a rewrite.

The Bull Case for Coinbase Becoming a $300 Billion Company by 2031

Core Argument: Most people view Coinbase as a crypto brokerage whose fortunes rise and fall with Bitcoin and crypto trading volumes. This narrow perspective overlooks Coinbase's long-term upside potential—in a world where stablecoin supply reaches $3 trillion and AI agent commerce hits $5 trillion by 2031, Coinbase, as the co-creator of USDC (with a favorable revenue-sharing agreement with Circle) and the creator of x402 and Base (the current primary venues for AI agent commerce), will capture immense value.

Introduction

Artemis is a digital finance research firm focused on on-chain data. We have helped McKinsey estimate real stablecoin payment volumes and have written extensively about AI agent commerce and the 2030 digital finance landscape. As crypto and AI converge, Coinbase will evolve beyond just a crypto exchange, becoming the settlement layer, distribution layer, and commerce layer for AI-native finance.

Most people view Coinbase as a cyclical crypto brokerage, moving in sync with crypto trading volumes.

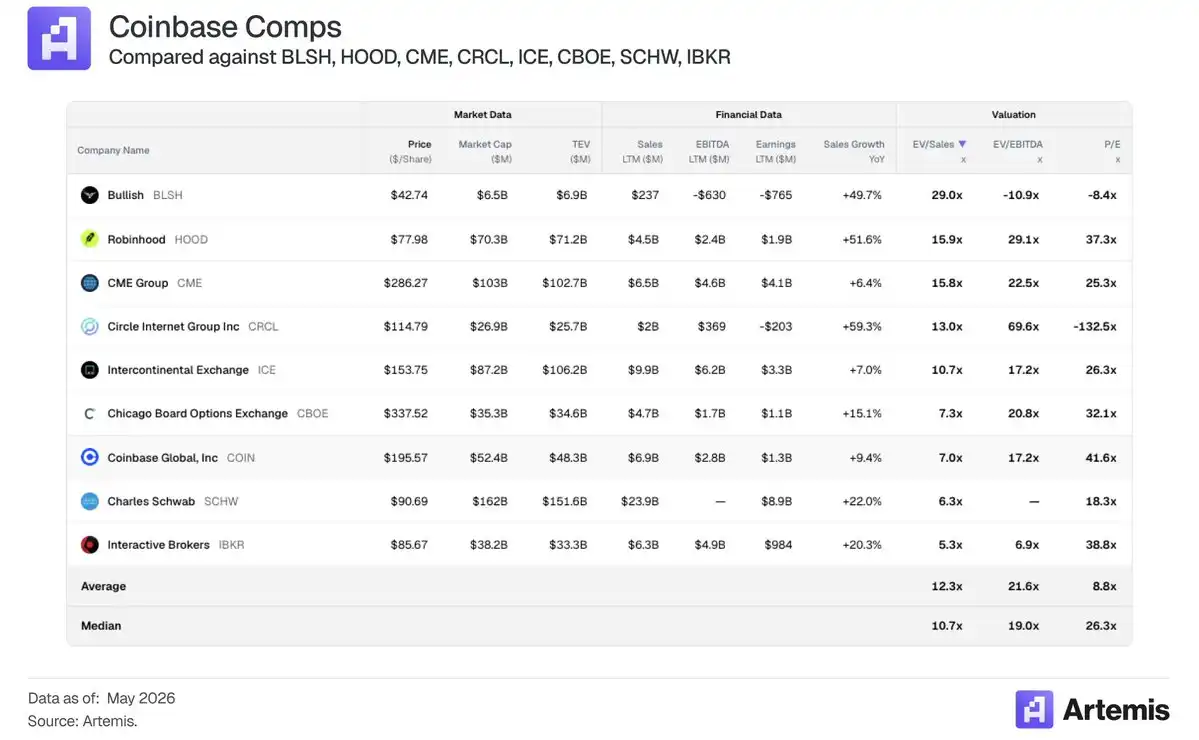

Unsurprisingly, Coinbase's stock trend aligns with other brokerages like IBKR, Robinhood, and Schwab.

Circle, as a pure play on stablecoin growth, receives a much higher valuation multiple (103.9x NTM P/E).

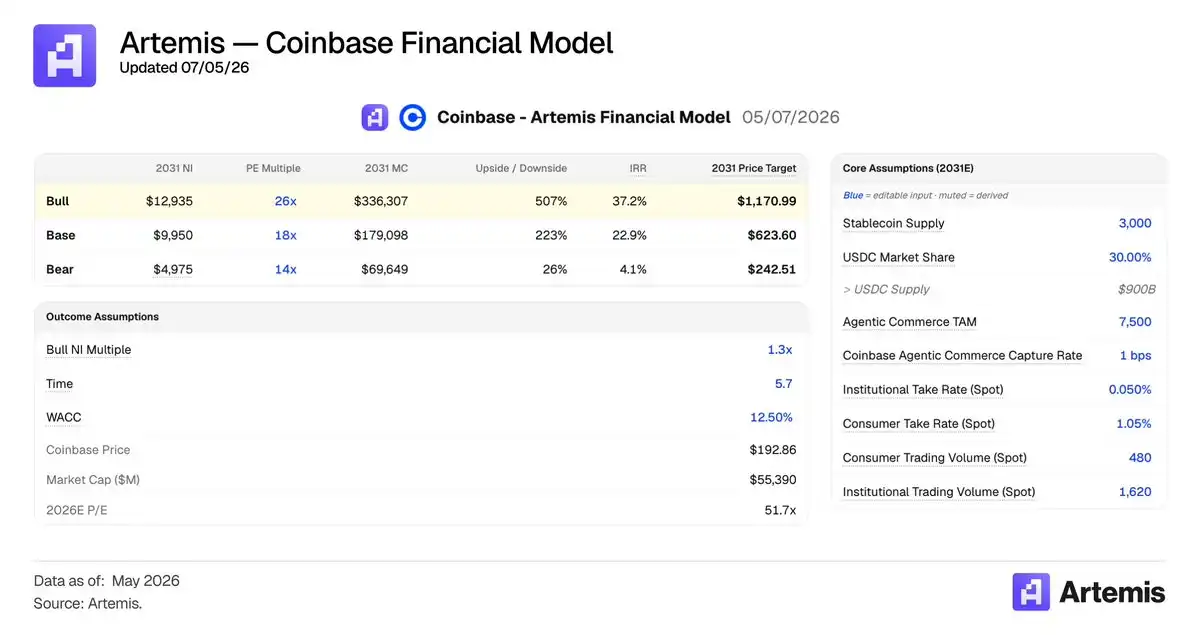

Coinbase can become a $300 billion company by 2031 (a 6x increase from today, representing a 35% CAGR), emerging as a major winner in stablecoins and AI agent payments—not just a crypto exchange. See the full model here.

Our core assumptions:

- Stablecoin supply reaches $3 trillion by 2031

- AI agent commerce volume reaches $7.5 trillion by 2031

- Our assumptions for the core exchange business align with the market—approximately $6 billion in trading revenue by 2028

The market is missing the fact that Coinbase benefits from and is positioned to win in two generational tailwinds:

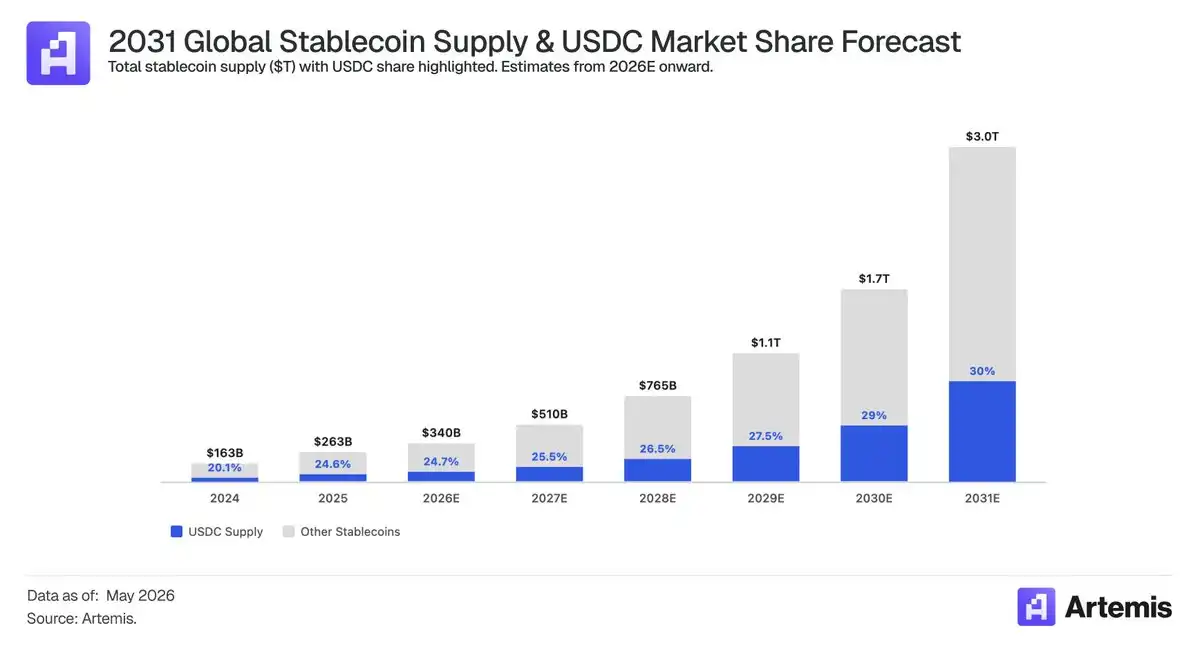

1. The rise of stablecoins and global demand for digital dollars. US Treasury Secretary Scott Bessent predicts stablecoin supply will reach $3 trillion by 2030 (a 10x increase from today). Bain & Company believes supply will grow 12x, or to $3.8 trillion, by 2030.

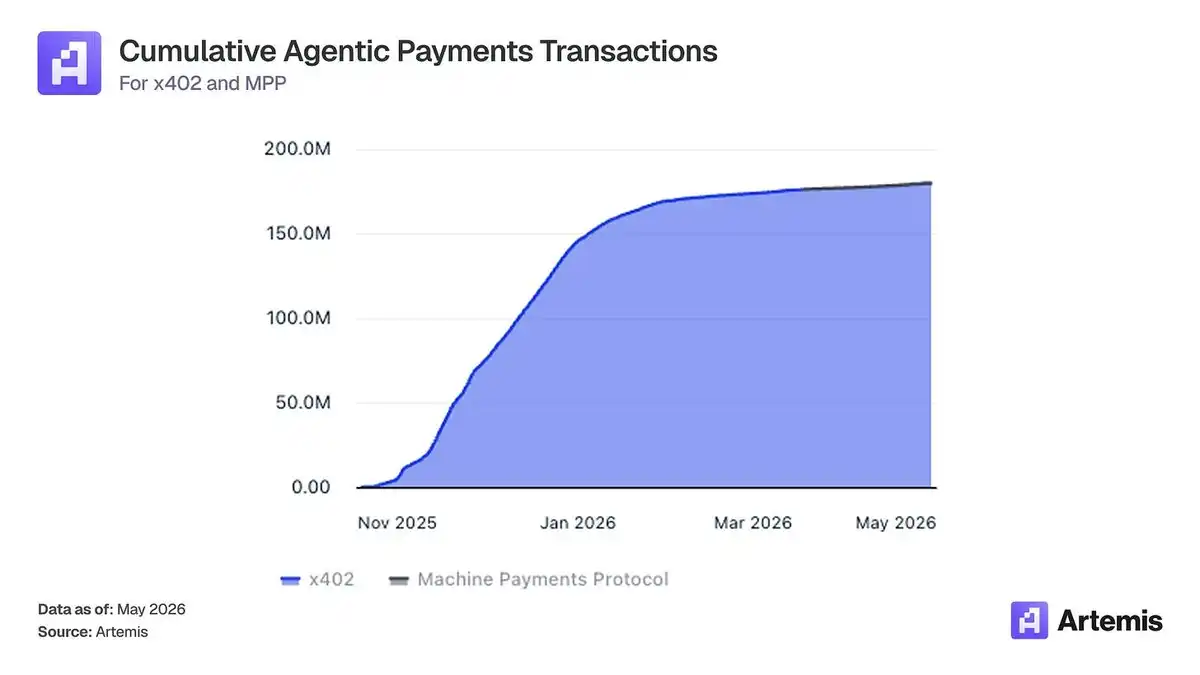

2. The rise of AI agent commerce. McKinsey predicts global AI agent commerce will be $3-5 trillion by 2030. We predict one-third of that commerce will be settled on-chain using AI agent payment protocols like x402 and MPP. We are currently seeing rapid growth in AI agent payments on-chain:

Coinbase clearly benefits from these two tailwinds, capturing value as the largest and most regulated distributor of USDC and as the network with the leading position in AI agent payments.

Coinbase will still win even if institutions are skeptical of DeFi and believe crypto is "dead"—not because of crypto and trading volume, but by becoming the most trusted and dominant stablecoin platform and AI agent payment infrastructure.

Why Coinbase Wins from Stablecoins

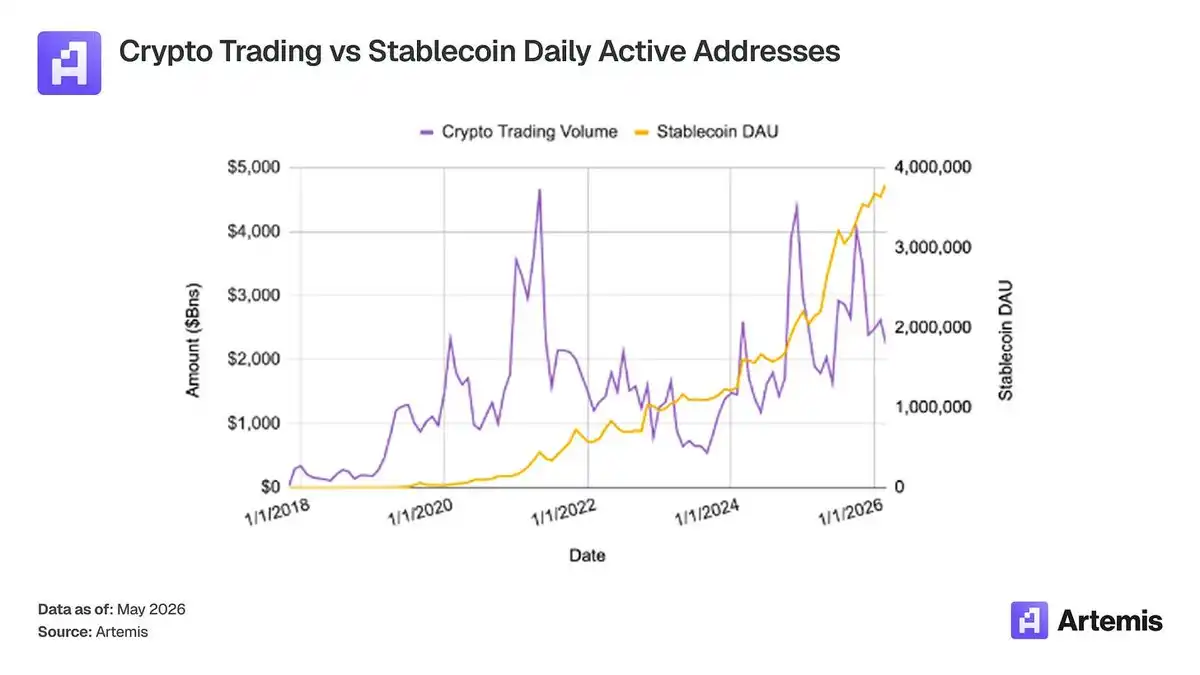

The market doesn't understand that Coinbase is a clear winner from stablecoin growth—even as crypto trading volumes decline, stablecoin usage has trended consistently upward historically.

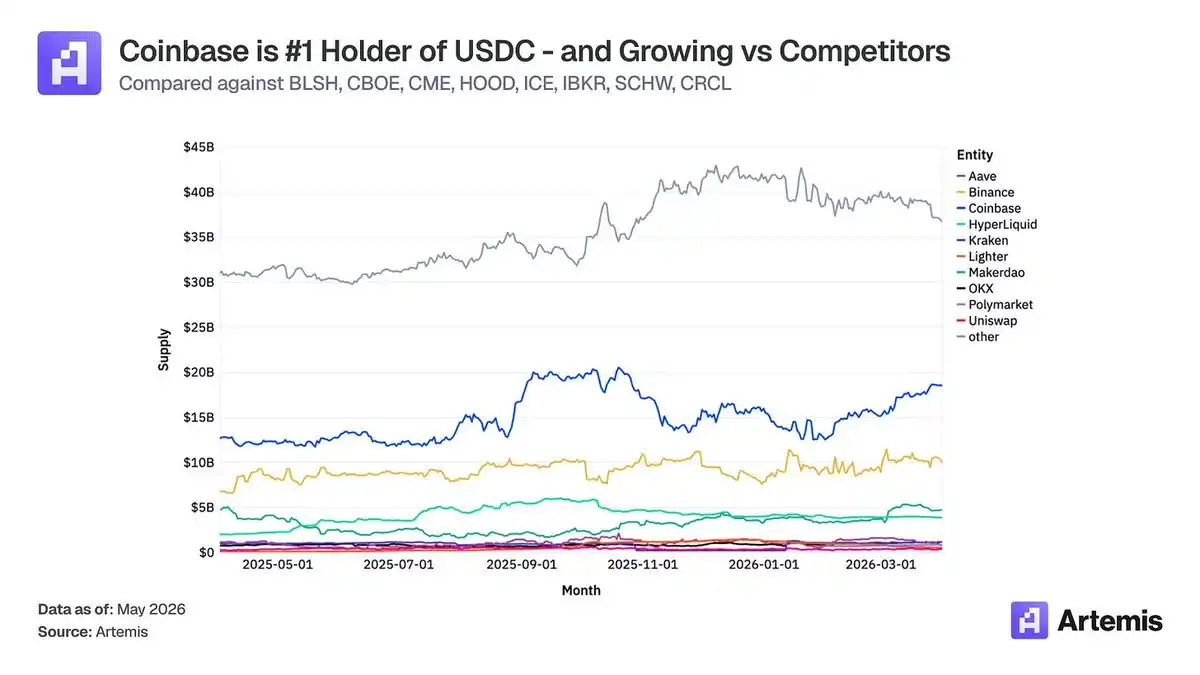

The USDC distribution agreement is an asset for Coinbase, not Circle. The revenue share Circle pays to Coinbase has climbed from 32% in 2022 to roughly 50% over the past two years. The structural reason is straightforward: Coinbase earns close to 100% yield on USDC held in its products and gains a material share from off-platform balances under the Payment Base waterfall mechanism. As Coinbase's distribution scale grows (average USDC held in Coinbase products reached a record $17.8 billion in Q4 2025), its waterfall share grows accordingly.

From an investor perspective, the agreement resembles Coinbase outsourcing regulatory and reserve management work to Circle, rather than Circle paying Coinbase for distribution. The cooperation agreement is for 3-year terms with automatic renewal, contingent on meeting three thresholds (Product, Company, and Dealer). Public filings indicate, "the Circle agreement cannot be terminated" if these thresholds are met. The renewal mechanism is not a cliff for renegotiation—it's a locked-in continuation. For Circle, leaving would mean severing its single largest distribution channel for USDC. For Coinbase, the upside scenario (regulatory clarity driving stablecoin payments to scale, USDC market cap expanding significantly) would flow directly through the same contractual share. The structure of the contract is designed to solidify Coinbase's position regardless of who operates Circle.

USDC's Future Growth

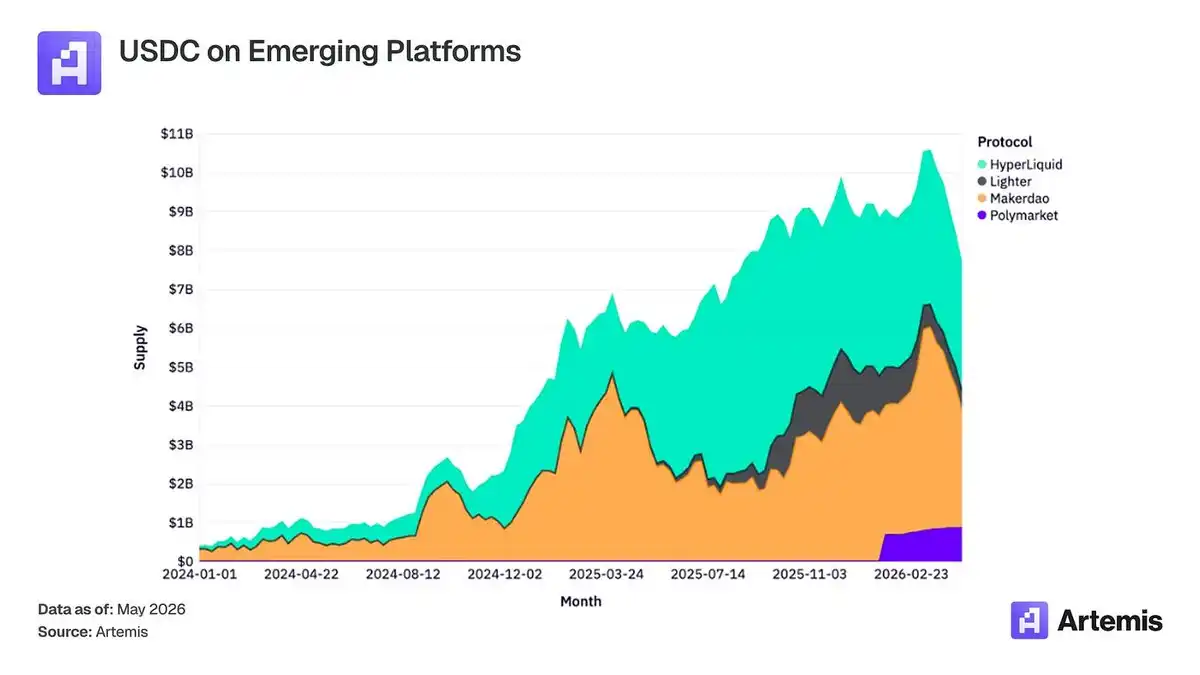

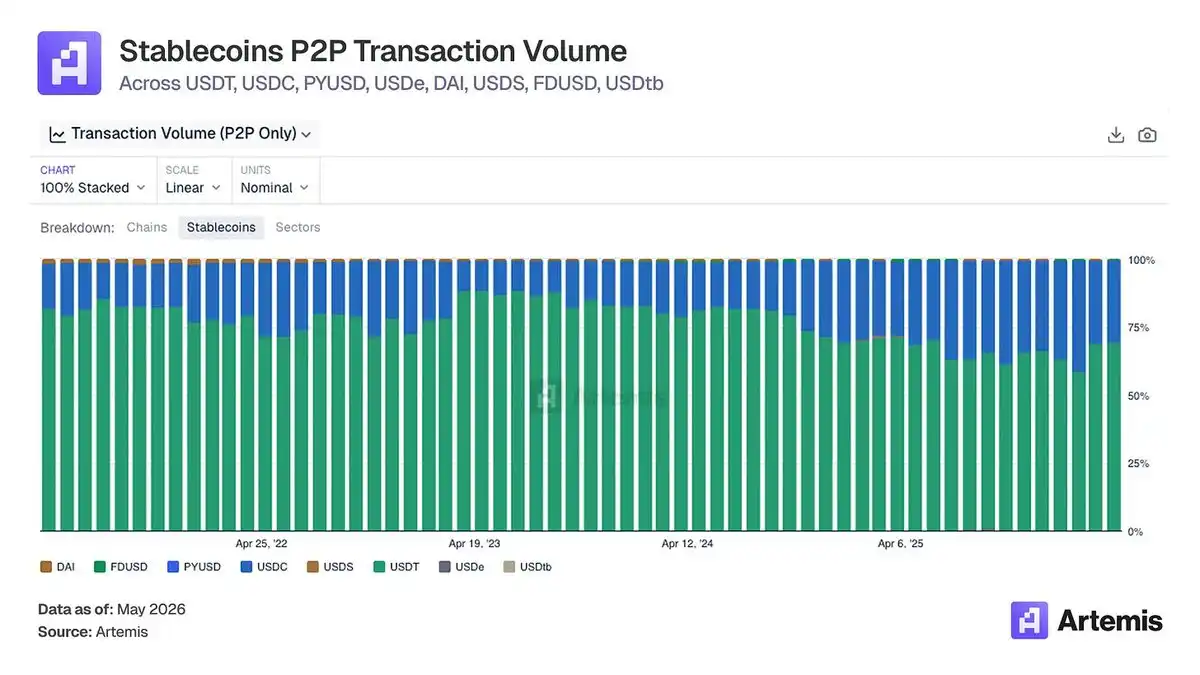

Beyond Coinbase, we also see many interesting use cases for USDC, especially in emerging protocols. We've seen the growth of USDC supply in protocols like Polymarket, Hyperliquid, and MakerDAO increase substantially over the past two years. As new financial use cases emerge on blockchain platforms, we see USDC continuing to be used within these protocols.

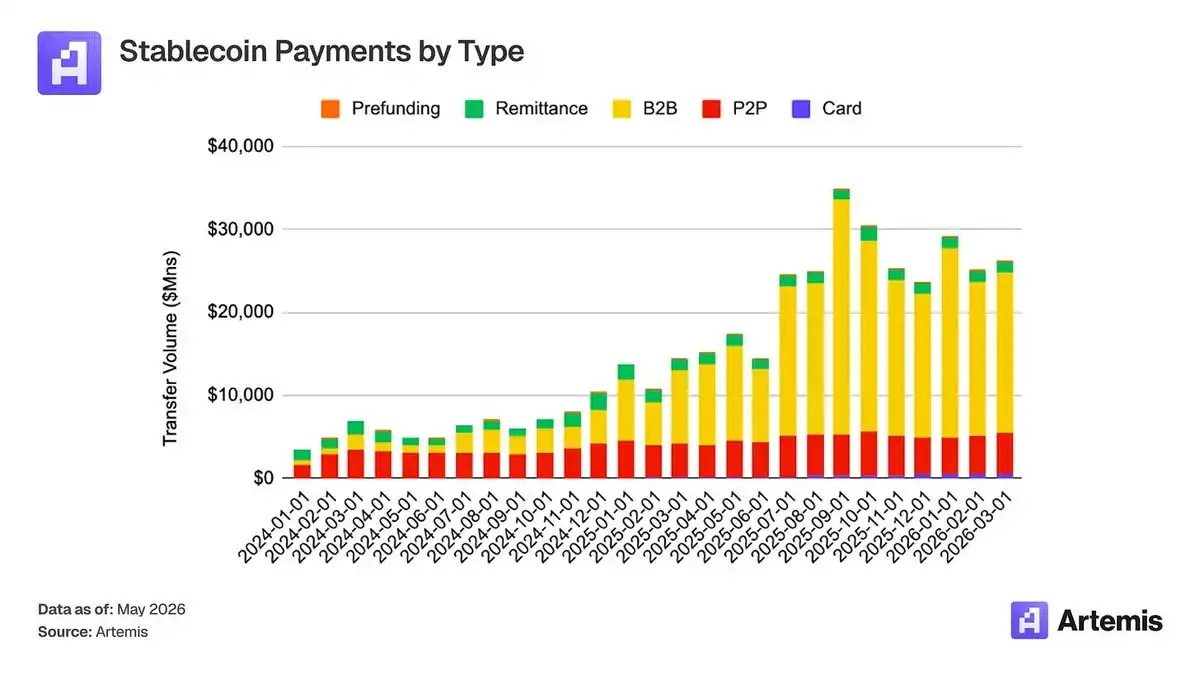

Coinbase is well-positioned to capture the next wave of stablecoin use cases—payments. Payment types (B2B, B2C) on card rails have increased significantly over the past year, and USDC continues to gain share in these transactions.

Looking at USDC address-to-address transfers (a proxy for this type of transaction), we see USDC gaining share relative to USDT.

Is the Market Misreading the CLARITY Act?

The Digital Asset Market Certainty Act of 2025 (H.R. 3633), commonly referred to as the "CLARITY Act," passed the U.S. House of Representatives on July 17, 2025, by a bipartisan vote of 294-134. The bill would establish a comprehensive regulatory framework for digital assets other than payment stablecoins. For Coinbase, the CLARITY Act represents the most significant pending U.S. legislation in the company's regulatory environment, establishing a largely complete federal regulatory architecture for the digital asset ecosystem in which Coinbase operates.

The relevance of the CLARITY Act to Coinbase's stablecoin economics is also greater than commonly understood. The revenue streams generated from Coinbase's distribution and reserve share arrangement with Circle are, under current rate assumptions, comparable to Circle's own economics at the issuer level, and Coinbase's USDC rewards program contributes another line whose ultimate scale depends on the final drafting of the Tillis-Alsobrooks compromise. The market underappreciates the size and durability of these stablecoin-related revenue lines, viewing them as ancillary to the exchange business rather than core infrastructure economics in their own right. The CLARITY Act reinforces this argument by formalizing the broader regulatory architecture for stablecoin clearing, settlement, and circulation—and clarifying the registered intermediaries through which stablecoin institutional flows pass. It repositions Coinbase's stablecoin business as the application layer of a regulated and rapidly institutionalizing system, rather than a consumer product line whose value ebbs and flows with retail token trading volume.

Why Coinbase Wins in AI Agent Payments

Most investors view Stripe (valued at $159 billion as of February 2026) and Tempo as clear winners in AI agent commerce, but on-chain data suggests otherwise: 92.8% of real AI agent payment volume occurs on Base, and 99.8% is settled in USDC.

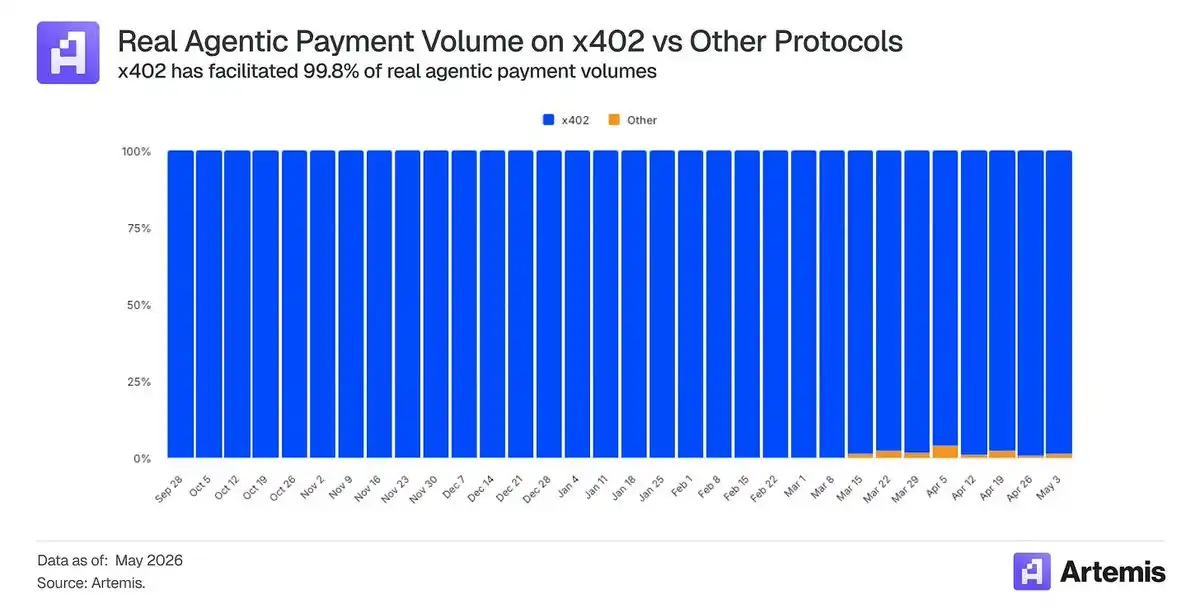

Of all AI agent payment volume, over 99.8% occurs on x402—the open payment protocol pioneered by Coinbase.

AI agents are evolving from assistants that answer questions to systems that transact on behalf of users, buying APIs, data endpoints, compute, inference, and services with sub-penny economics and at machine speeds.

Existing card rails aren't designed for this. A typical card transaction has fixed costs of ~$0.03 to $0.04 before interchange fees, making a $0.003 API call economically infeasible—off by two orders of magnitude. Stablecoins settled on high-throughput L2s clear in seconds for fractions of a penny and require no human intervention to establish a billing relationship.

McKinsey projects $3-5 trillion in global AI agent commerce sales by 2030. Gartner estimates AI agents will intermediate over $15 trillion in B2B procurement by 2028. Both numbers are directional and should be treated as such; however, what is not speculative is that if either materializes, it structurally favors stablecoin rails, and USDC is already the default choice, from which Coinbase benefits directly.

Data Scorecard

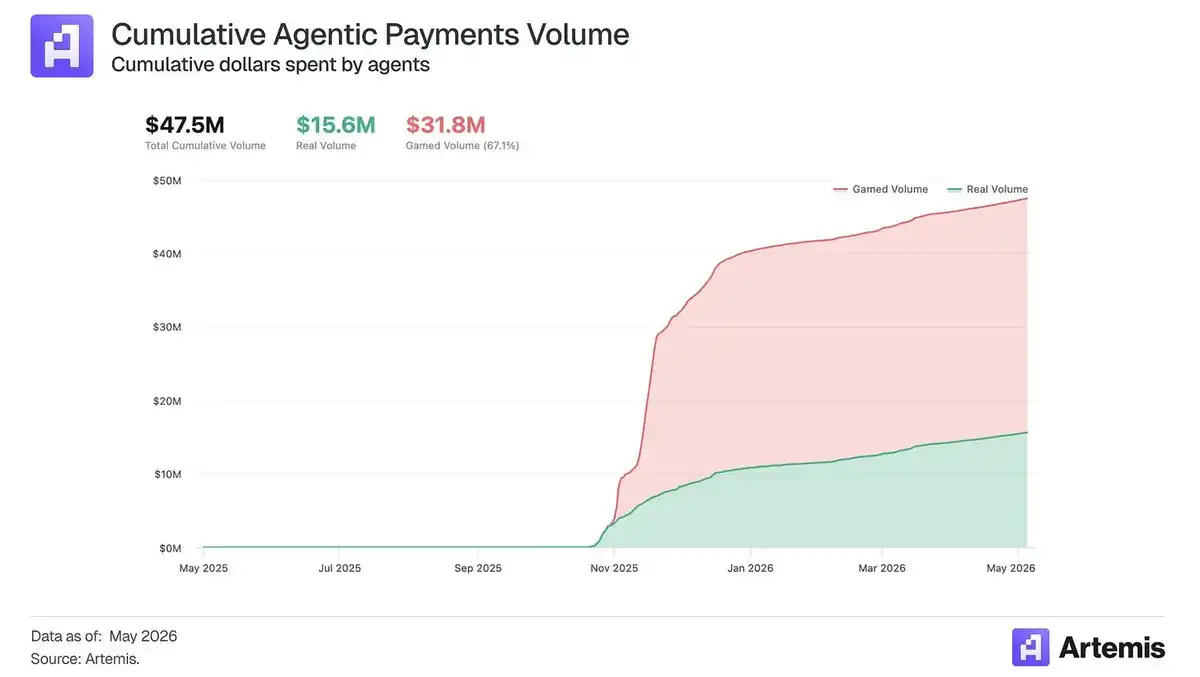

The x402 standard, an HTTP-native micropayments protocol co-developed by Coinbase (now managed by the Linux Foundation), has become the leading open protocol for payments initiated by AI agents. Since October 2025, x402 has processed over 180 million AI agent payments, moving $47.5 million in AI agent spend across over 5,000 merchants selling to AI agents.

When merchants make their services consumable by AI agents, Coinbase's L2 and USDC are already the default payment rail. Furthermore, Agentic.Market gives Coinbase a path to own resource discovery. If AI agents use it to find, evaluate, and route to x402-enabled services, value accrues not only through Base settlement and USDC volume but also through Coinbase's position as a marketplace coordinating AI agent-to-service transactions.

How Coinbase Monetizes

Coinbase captures the economics of AI agent payments through four compounding lines around its stablecoin pillar: USDC float, Base settlement, CDP/AgentKit monetization, and Agentic.Market distribution.

USDC Reserve Yield. The revenue line with Coinbase's highest upside potential is not trading fees, but float. AI agent wallets need prefunded balances to authorize autonomous spending, pay for APIs, cover usage-based services, and settle machine-to-machine commerce in real time. As AI agents become economic actors, USDC balances held in wallets under Coinbase's control become recurring, yield-generating deposits. Every dollar of USDC held by an AI agent generates reserve revenue, regardless of how fast that dollar turns over.

Base Sequencer Economics. Every x402 or MPP-style transaction settled on Base becomes a sequenced transaction that can generate priority fees. This line scales with the number of transactions, not just payment value, which is important because AI agent commerce may be higher-frequency and lower-ticket than human commerce. That said, sequencer fees are likely the smallest component of upside potential, as transaction costs trend lower over time.

CDP, AgentKit, and Enabler Monetization. Coinbase can monetize the developer layers that let AI agents hold wallets, manage permissions, sponsor gas, settle x402 payments, and interface with paid services. This includes enabler fees for x402 transactions, wallet infrastructure, gasless transactions, key management, policy controls, and enterprise-grade developer tooling. If the CDP becomes the default infrastructure stack for AI agent payments, Coinbase earns platform revenue even if end-payment values are low.

Scaled Upside Potential

We assume AI agent commerce reaches $5 trillion annually by 2030. Most of this will still be routed through card, ACH, bank payment, and account-to-account rails, especially for large consumer and enterprise purchases. But machine-native, high-frequency, cross-border, API-based commerce will disproportionately use stablecoins and payment standards like x402 and MPP.

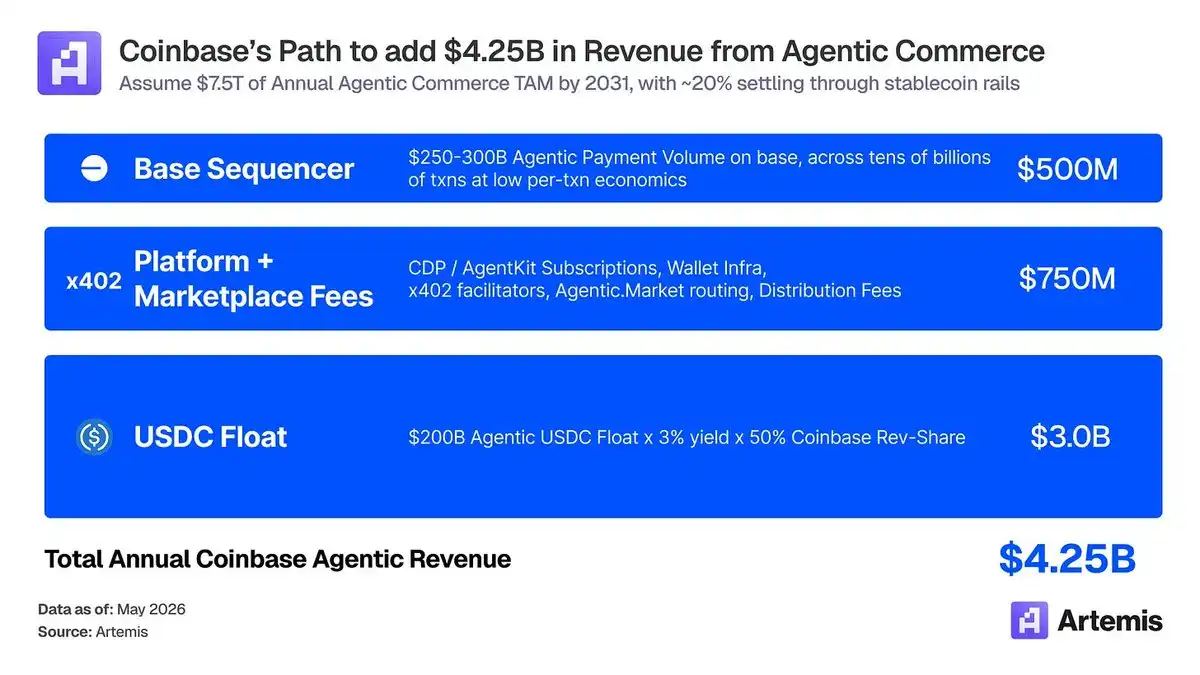

In the bull case, roughly 20% of AI agent commerce settles over stablecoin rails, implying $1.0–1.5 trillion in annual stablecoin-based AI agent payment volume. An illustrative bull case revenue calculation is as follows:

- USDC Float: $200 billion average AI agent USDC balance × 4% reserve yield × 50% Coinbase-attributable economics = $4 billion

- CDP/AgentKit/Enabler/Agentic.Market: Developer subscriptions, wallet infrastructure, x402 enabling, marketplace routing, provider analytics, and distribution fees = $750 million

- Base Sequencer: $250-300 billion in AI agent payment volume on Base, tens of billions of transactions, with low per-transaction economics = $250 million

This points to roughly $4.25 billion in annual Coinbase-attributable AI agent revenue. The important takeaway is that real value accrues if Coinbase becomes the operating account, developer platform, discovery layer, and settlement rail for autonomous commerce, and they have made significant progress on this front over the past few months.

Why Coinbase and USDC Win

Coinbase's advantage lies in its control over four mutually reinforcing layers of the AI agent payments stack: USDC float, Base settlement, CDP/AgentKit infrastructure, and Agentic.Market discovery.

USDC is already the default settlement asset, meaning builders integrate it first because it has the deepest tooling, liquidity, and developer support. Base then benefits as the natural settlement chain for USDC-native AI agent payments, with low developer friction and growing enabler coverage. The CDP and AgentKit sit a layer above, providing developers the wallets, key management, gas sponsorship, and payment infrastructure needed to make AI agents economically active. Finally, Agentic.Market can become the discovery and routing layer where AI agents find, compare, and consume x402-enabled services. Competitors entering this market need to replicate liquidity, settlement, developer infrastructure, and distribution simultaneously—and each new AI agent, merchant, and service makes the existing Coinbase stack harder to displace.

Conclusion

The market views Coinbase as a crypto exchange, missing the AI-native finance platform they are building. Global leaders predict $3 trillion in stablecoin supply and $5 trillion in AI agent commerce by 2030, and stablecoins have already decoupled from crypto prices. Coinbase has positioned itself to be a winner in that world and is showing early leadership. x402, USDC, and Base have become the de facto standard stack for AI agent commerce, with over 90% share across each layer versus competitors. Coinbase is uniquely positioned, having developed Base, incubated x402, and secured a favorable share of USDC economics. The mispricing has three legs. The Circle agreement structure is a perpetually locked contract, not a renewable one, meaning stablecoin revenue lines are durable, not at risk. The CLARITY Act formalizes the regulated infrastructure layer Coinbase already operates, repricing the business from a consumer product to core market plumbing. And the four-layer AI agent stack (USDC, Base, CDP, Agentic.Market) reflexively compounds, making the moat harder to attack with each new AI agent and merchant. Coinbase should trade closer to infrastructure comps than brokerage comps. We believe Coinbase will become a $300 billion company powered by these generational tailwinds, with the majority of revenue coming from subscription and service lines like stablecoins and AI agent commerce.

Disclosure: This material is for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other form of recommendation. The views expressed are those of the author and should not be taken as advice to buy, sell, or hold any asset. The author or related entities may hold positions in the assets discussed. You should conduct your own research and consult appropriate financial professionals before making any investment decisions.