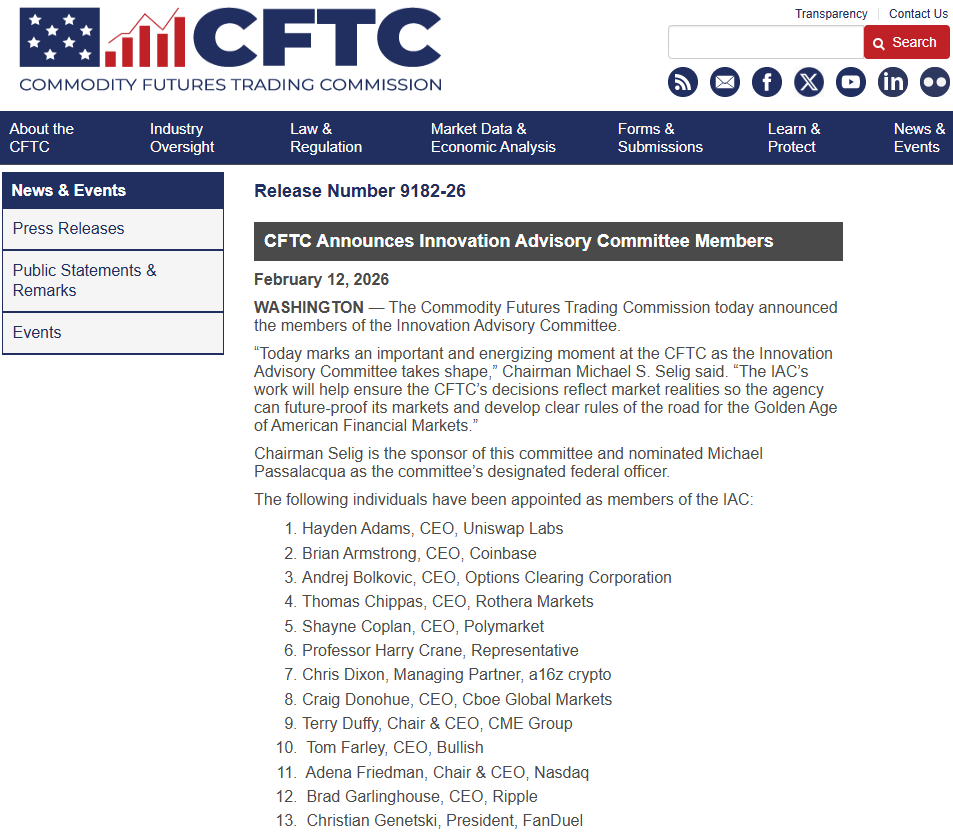

The United States Commodity Futures Trading Commission announced appointments to a new committee that would provide advice on regulatory and industry developments regarding digital assets. Coinbase CEO Brian Armstrong confirmed his position as a member of the committee representing crypto exchange interests. The advisory committee also has Ripple CEO Brad Garlinghouse as a member, offering information from a prominent payments blockchain company. The committee has various members representing companies in digital assets, finance, and blockchain technology. The committee also has members from a company that issues a stablecoin and a derivatives desk manager.

CFTC Chairman Rostin Behnam stated the committee would assist in helping regulators grasp the intricacies of the digital market. The members would contribute their expertise and knowledge from the digital asset marketplace. This advisory committee would meet at least four times in 2026 to discuss the problems regulators face in their work. The CFTC formed the committee through the Digital Commodities Consumer Protection Act’s powers. They would concentrate their focus on market issues such as compliance and risk management.

The committee has executives from companies such as Paxos, Cumberland, Galaxy Digital, among other companies. A representative of the stablecoin issuer has knowledge of liquidity and a framework for redemption. The diversity of the group is evident since there is knowledge on trading platforms, derivatives exchanges, and blockchain operations. The members of the CFTC’s advisory panel are compliance experts and know legal issues. The committee has experts from fintech and blockchain-based think tanks. The experts know derivatives exchanges, clearing operations, and blockchain operations.

Committee Aims and Regulatory Role

The Advisory Group will review options for enhancing digital asset markets under U.S. laws. The members will be able to review the risk issues faced by participants in the digital markets, whether retail or institutional. The members will also give opinions on compliance issues faced and law enforcement. The panel may also discuss transparency issues in digital markets in the U.S. The issue of coordination between U.S. regulatory authorities may also come up.

The committee members may assist the CFTC in oversight roles for new technologies. These could involve data infrastructures and market settlement systems. The contributions from the members to the CFTC may shape the proposals for future rules set forth by the agency.

Highlighted Crypto News:

U.S. Bankers Urge OCC to Slow Crypto Trust Bank Charters