Breaking News! China Telecom, China Mobile, and China Unicom All Enter the Fray

From May 16th to 17th, the three major telecom operators successively launched nationwide Token plans within two days.

Starting as low as 9.9 yuan/month for 10 million Tokens.

Direct payment via phone bill is supported.

AI has evolved from a tech circle concern into a line item on your phone bill.

What does this mean—Tokens are becoming the new generation of "data packages."

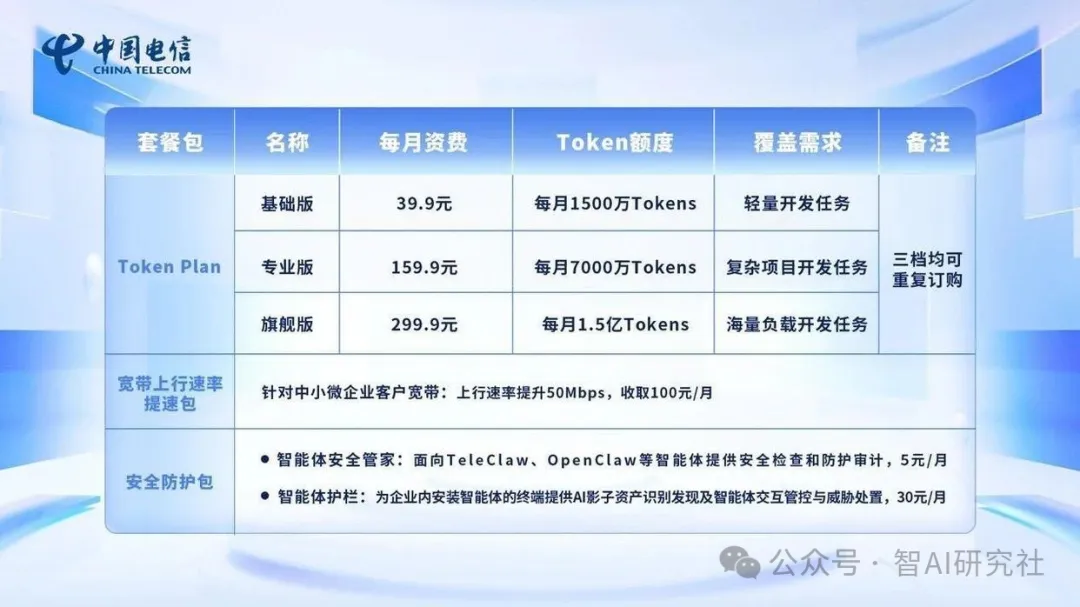

First, look at China Telecom's offering.

Individual plan: Minimum 9.9 yuan/month, includes 10 million Tokens.

Higher tiers include 29.9 yuan and 49.9 yuan, corresponding to 40 million and 80 million Tokens respectively.

For developers and enterprises: Basic version at 39.9 yuan for 15 million Tokens, Professional version at 159.9 yuan, and Flagship version at 299.9 yuan.

China Telecom's selling point is a bundled package of "Tokens + Connectivity + Security," offering broadband uplink speed boost and security protection along with Tokens.

Shanghai Mobile, in collaboration with Tencent, launched an AI-native workbench, with 1 yuan buying 400k Tokens. Beijing Mobile was even earlier—minimum 5.99 yuan for a computing resource sub-package, and 24.99 yuan for 10 million Tokens.

The most notable move is that China Mobile integrated Tokens into its cloud computer service.

Users without a cloud computer can directly purchase a bundled cloud computer plan with built-in OpenClaw, ready to use upon startup.

China Unicom's approach is also different.

Shanghai Unicom is giving them away—OPC customers can receive a 30 million Token testing quota for free.

Personal version: 15 yuan/month for 6 million Tokens. Team version: 198 yuan/month, also including a one-month free trial of AI cloud desktop.

The prices of the three operators are similar, with each having its own strategic focus.

But the core logic is exactly the same—selling Tokens like phone credit packages.

The 9.9 yuan Token plan itself is not cheaper than offerings from major tech giants.

Some market commentators note that compared to API pricing from major model providers, the operators do not have a clear price advantage.

But the key point here is not the price; it's the distribution channel.

Major tech companies sell Tokens to developers and power users—there's a ceiling there.

Telecom operators sell Tokens to everyone who has a mobile phone.

China Mobile has nearly 1 billion subscribers, China Telecom has nearly 400 million, and China Unicom also has over 300 million.

This user pool is on a completely different scale.

And most importantly, this represents the collective entry of state-owned enterprises.

It is a synchronous pivot by the three major operators.

The data from the National Data Administration is also on the table—the daily Token consumption volume in China surged from 100 billion in early 2024 to over 140 trillion by March 2026.

An increase of over a thousand times in two years.

Tokens are no longer a niche unit in the AI circle; they are becoming a basic telecom commodity alongside data and call credit.

Some telecommunications industry experts judge that if all three operators follow through,

the distribution market for large model APIs might partially shift from cloud providers to the operator system.

In the future, you won't need to understand what an API or a model is to buy Tokens.

You could just go to a service center and say, "Top up 100 yuan worth of Tokens for me," and another line would appear on your phone bill.