Original article from Bitwise

Compiled by|Odaily Planet Daily Qin Xiaofeng(@QinXiaofeng 888 )

Editor's Note: Cryptocurrency asset management company Bitwise recently released its Q2 2026 report.

The report states that the Bitwise 10 Large Cap Crypto Index fell by 15.4%, with 8 out of its 10 constituents recording negative returns; Spot Bitcoin ETFs saw outflows of $4.9 billion, marking the worst quarterly performance on record; On-chain transaction activity, trading volume, and DeFi assets all declined, while the correlation between cryptocurrencies and stocks increased.

Of course, there were bright spots in the market. Prediction market open interest reached a record high of $1.8 billion, with quarterly trading volume hitting $43 billion; The scale of tokenized real-world assets reached $33 billion in Q2, a 45% increase from the beginning of the year; Crypto-related stocks also performed well, with the Bitwise Crypto Innovators 30 Index rising 30.6%, primarily driven by AI-related Bitcoin mining companies.

"Overall, the situation is tough. What's worse, the feeling of difficulty is equally real. While there is no statistical measure for 'vibe,' the current sentiment in the crypto industry is among the worst I've seen in my eight years. One reason is this: this is our third consecutive quarter of negative returns, the longest losing streak since 2022 (which saw four consecutive negative quarters)." wrote Matt Hougan, CIO of Bitwise.

Below are some key data charts excerpted from the report, Enjoy~

——————————

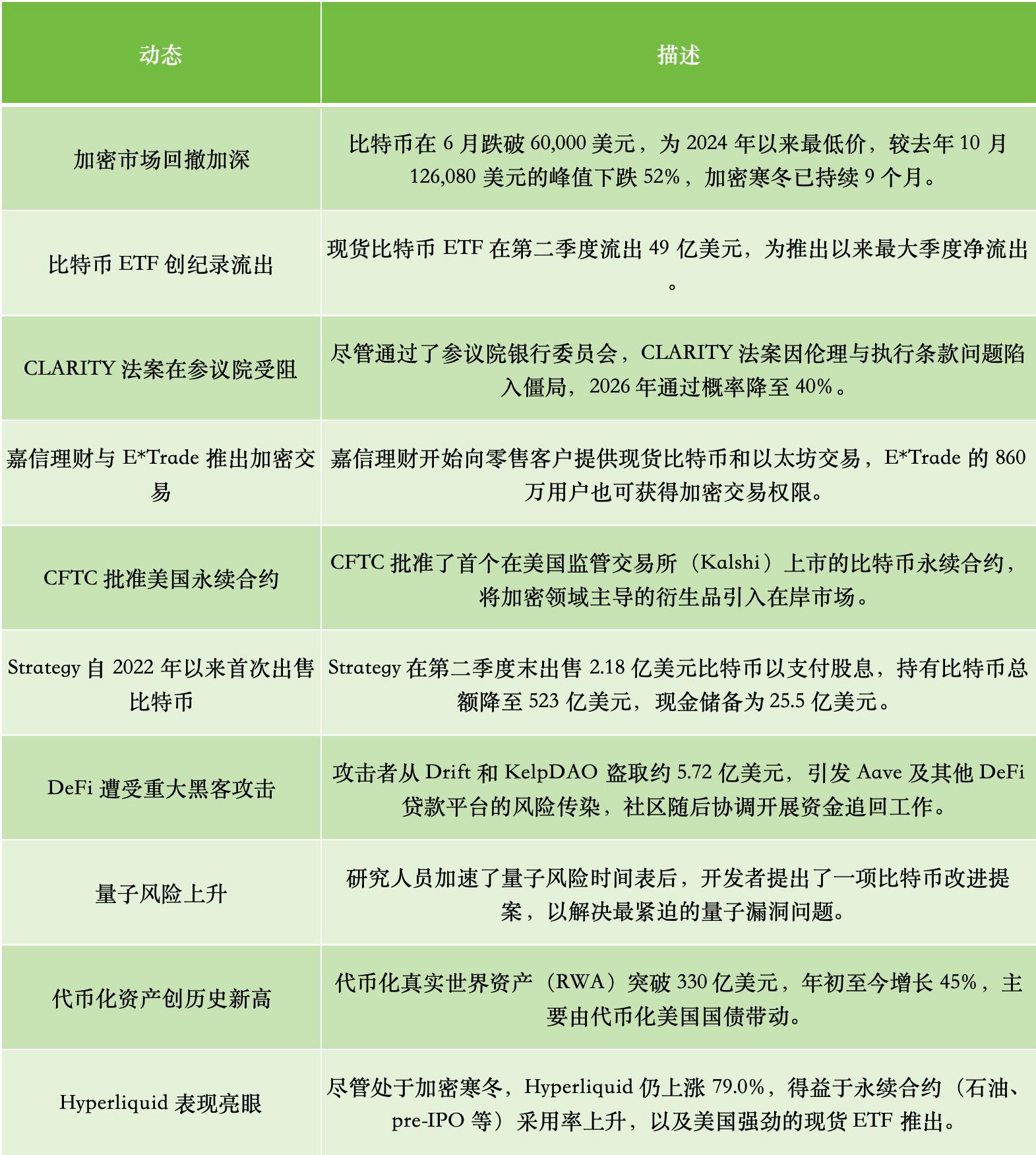

Top 10 Key Events in Q2

In the second quarter, we saw MicroStrategy, which had declared it would "never sell," offload Bitcoin, starting with small tests and culminating in a $218 million sale in late June to pay a dividend.

Influenced by these selling actions, Bitcoin fell below $60,000 in June, hitting its lowest price since 2024, down 52% from its peak of $126,080 (in October last year), marking 9 months of a crypto winter. Meanwhile, spot Bitcoin ETFs saw $4.9 billion in outflows in Q2, the largest quarterly net outflow since their launch.

On the policy front, the long-awaited "CLARITY Act" faced setbacks in the Senate, stalling due to ethical and enforcement clause issues, with prediction markets lowering its 2026 passage probability to 40%.

Below are the top 10 crypto events summarized by Bitwise for Q2:

Q3 Outlook

The third quarter is critical for the fate of the CLARITY Act. This market structure bill passed the Senate Banking Committee in Q2 but stalled over ethics clauses related to the presidential family's crypto interests. Prediction markets show its 2026 passage probability near 40%, down from 75% in mid-May, and we believe passage before the November midterm elections is unlikely. However, bills with such odds often succeed, so we think CLARITY still has a chance. If passed, we believe it could mark the bottom of this bear market; if it fails, we expect short-term volatility followed by a gradual reduction in uncertainty as the industry progresses under a crypto-supportive SEC and CFTC.

Stablecoin expansion post-GENIUS Act. July marks the final sprint before the GENIUS Act takes effect in January 2027, with regulators needing to finalize rules in Q3. We expect a wave of large companies announcing stablecoin projects ahead of the official launch, such as the recent announcement of OpenUSD backed by Stripe, BlackRock, Visa, Coinbase, and about 140 other companies. Stablecoin supply has remained near $3 trillion since last fall, showing resilience during the crypto sell-off. We believe accelerating stablecoin growth will be a catalyst for blockchains like Ethereum and Solana in Q3 as the January effective date approaches.

The Warsh-led Fed. The Federal Reserve has a new chair, Kevin Warsh, whose style is largely unknown to the market. The third quarter will bring the first signals: the July FOMC meeting and the Fed's annual Jackson Hole symposium in late August. So far, Warsh has held rates steady and hinted at no rush to cut. By the end of the quarter, we should have a clearer picture of the Fed's direction than we do now. It's too early to call the direction of rates, but the Fed sets the tone for all risk assets, and any outcome will be quickly digested by the market.

The quiet re-rating of DeFi. Over the past month, Bitcoin fell about 22%, while Bitwise's DeFi Index fell only 4%. DeFi is typically far more volatile than Bitcoin, making such resilience rare and largely unnoticed. We believe DeFi is quietly being re-rated: token economics are improving, the gap between usage and token value is narrowing, real institutions are building on protocols like Morpho and Jupiter, and Aave alone generated about $900 million in revenue over the past year. We expect DeFi's outperformance to continue into Q3, a shift often realized with a lag by the market.

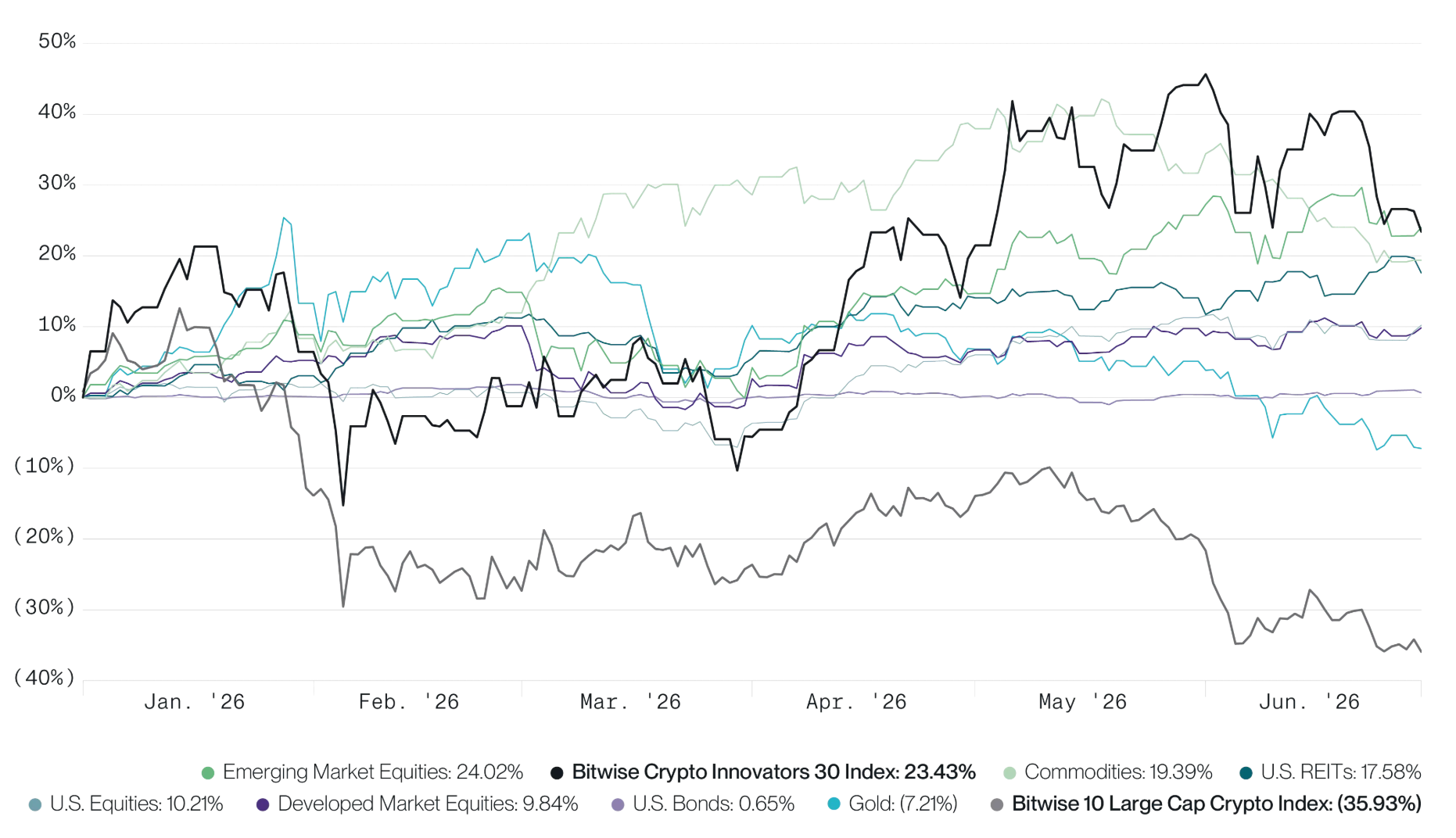

Crypto Stocks and Crypto Assets Diverge Significantly

Halfway through 2026, crypto asset prices are down 36%. The only other major asset class with a negative return is gold, down 7%, with all others in positive territory. This is precisely why this crypto winter feels particularly harsh—it's a lonely winter.

But notably, crypto stocks returned 23% in the first half, outperforming all major asset classes except emerging market equities. In fact, the Bitwise Crypto Innovators 30 Index, which tracks the 30 largest listed crypto-economy companies, more than doubled the return of U.S. stocks.

This illustrates that even in a bear market, investment opportunities within the crypto space continue to emerge. Bitcoin miners benefit from the AI tailwind; stablecoin issuers and tokenization platforms are riding the wave of Wall Street adoption; the link between traditional finance and crypto is strengthening. While I expect crypto assets to rebound in the second half of the year, the first half reinforced an important insight: crypto is not a single thing, but a diverse, dynamic field that should be viewed with a broader lens.

The performance of cryptocurrencies versus major asset classes is as follows:

Data from Bloomberg. Data as of June 30, 2026.

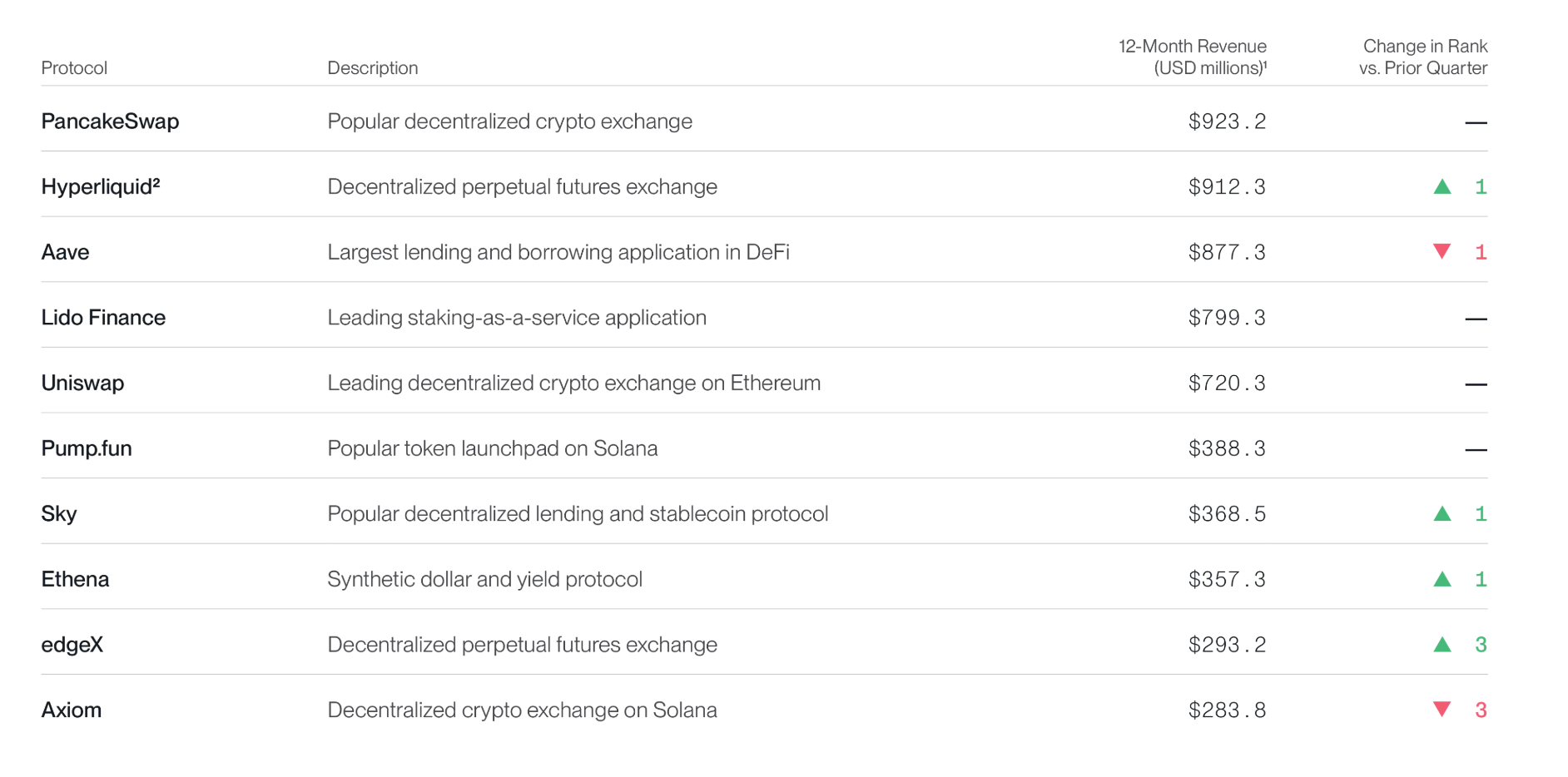

Crypto Applications Generate Significant Revenue

Over the past 12 months, the top 10 crypto applications collectively generated $5.9 billion in revenue. The top three (PancakeSwap, Hyperliquid, and Aave) each approached nearly $1 billion in revenue. These are real businesses, earning fees from trading, lending, and staking—even in a bear market.

The top 10 crypto applications by revenue are shown below:

Data from Token Terminal, covering the period from January 1, 2025, to June 30, 2026.

(1) Revenue consists of total fees paid by users; (2) Hyperliquid revenue excludes HyperEVM fees.

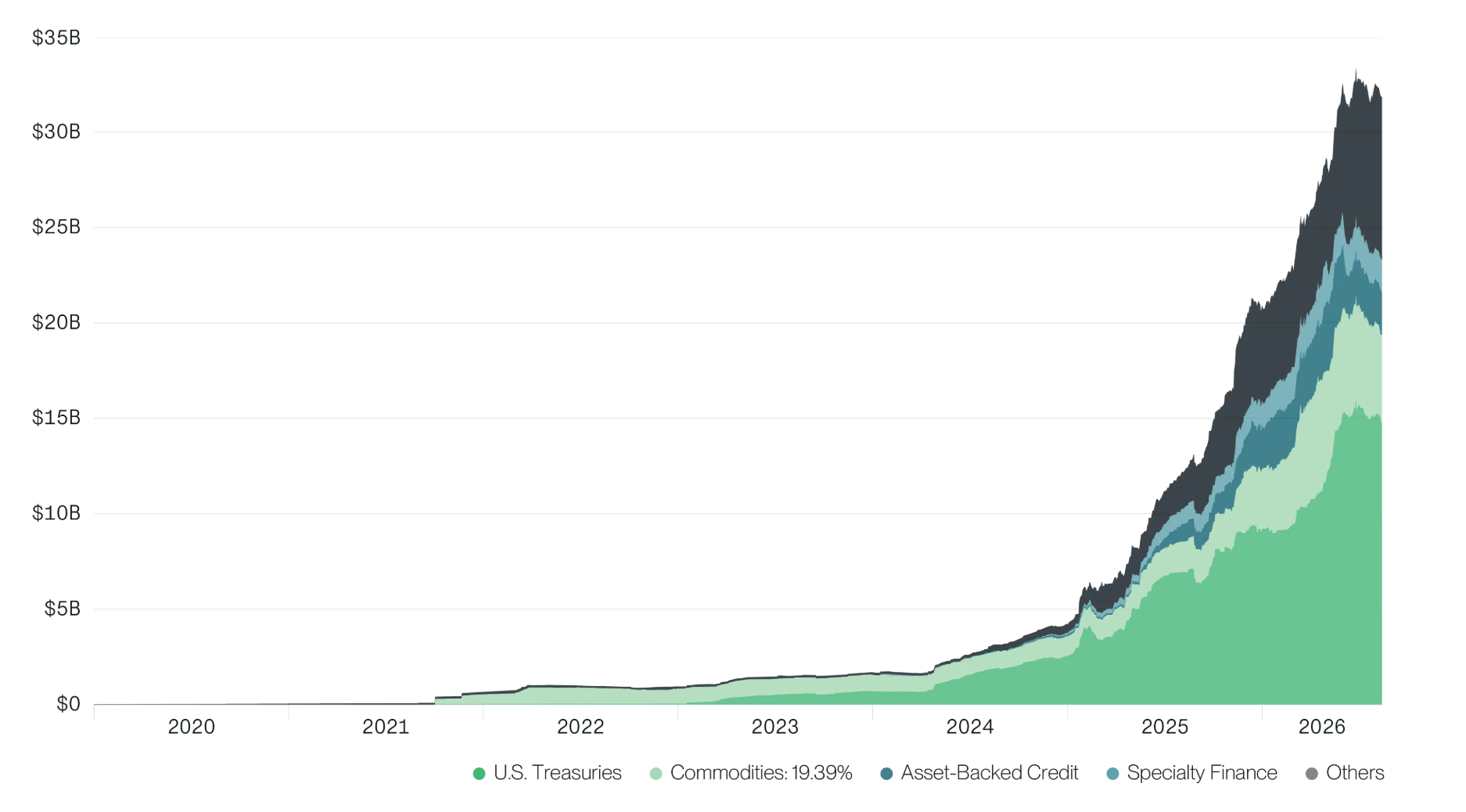

The Bull Market for Real-World Assets (RWA)

U.S. Treasury Secretary Scott Bessent himself stated just weeks ago: "Digital assets, stablecoins, tokenization, and new payment systems will help shape the future of money."

In a sense, the future he described is already here. Tokenized real-world assets (RWAs) reached a record $33 billion in Q2, growing 12% quarter-over-quarter and 45% year-to-date, with tokenized U.S. Treasuries, corporate credit, equities, and venture capital seeing particularly rapid growth.

When I look at this chart, I see the world's largest asset managers moving assets on-chain at full scale and massive speed. It's worth paying attention to.

The scale of tokenized real-world assets (RWA) is shown below:

Data from RWA.xyz, covering the period from January 1, 2020, to June 30, 2026.

Note: The chart above omits stablecoin issuers like Circle and Tether.

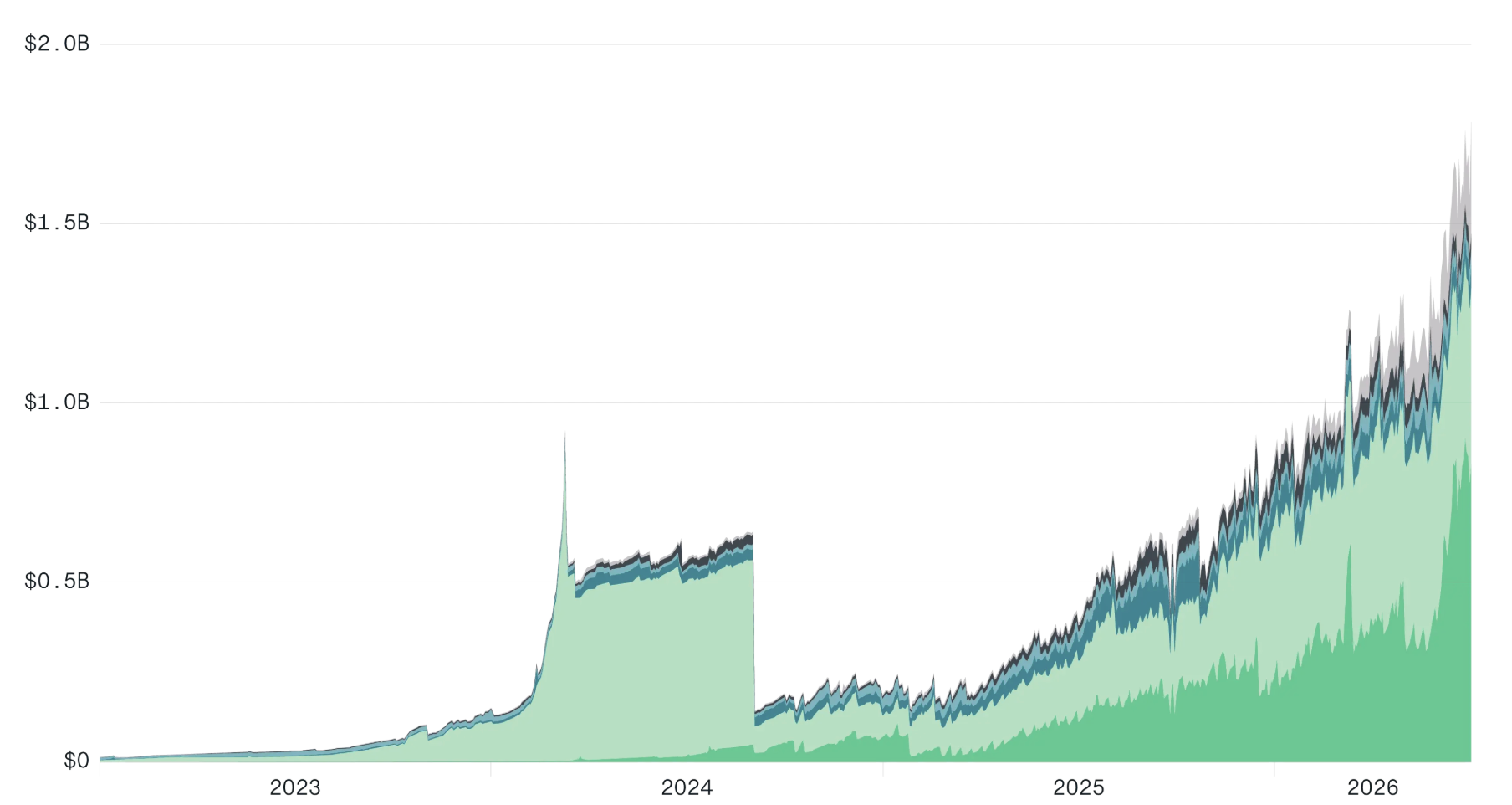

Prediction Markets Continue to Expand

Prediction market open interest reached a record high of $1.8 billion in Q2, with the sports category becoming the largest segment by weight. Quarterly trading volume also hit a record of $43 billion.

Applications like Polymarket embody the stealth nature of retail adoption of cryptocurrency: millions are using crypto infrastructure to trade on real-world event outcomes, but most don't know or care that crypto provides the underlying technology.

As the U.S. midterm elections approach, trading volume and open interest in prediction markets will repeatedly set new records this year. After all, politics was the category that brought prediction markets to the mainstream in 2024, and the market size has tripled since then.

Prediction market open interest is shown below:

Data from Blockworks Research, covering the period from January 1, 2023, to June 30, 2026.

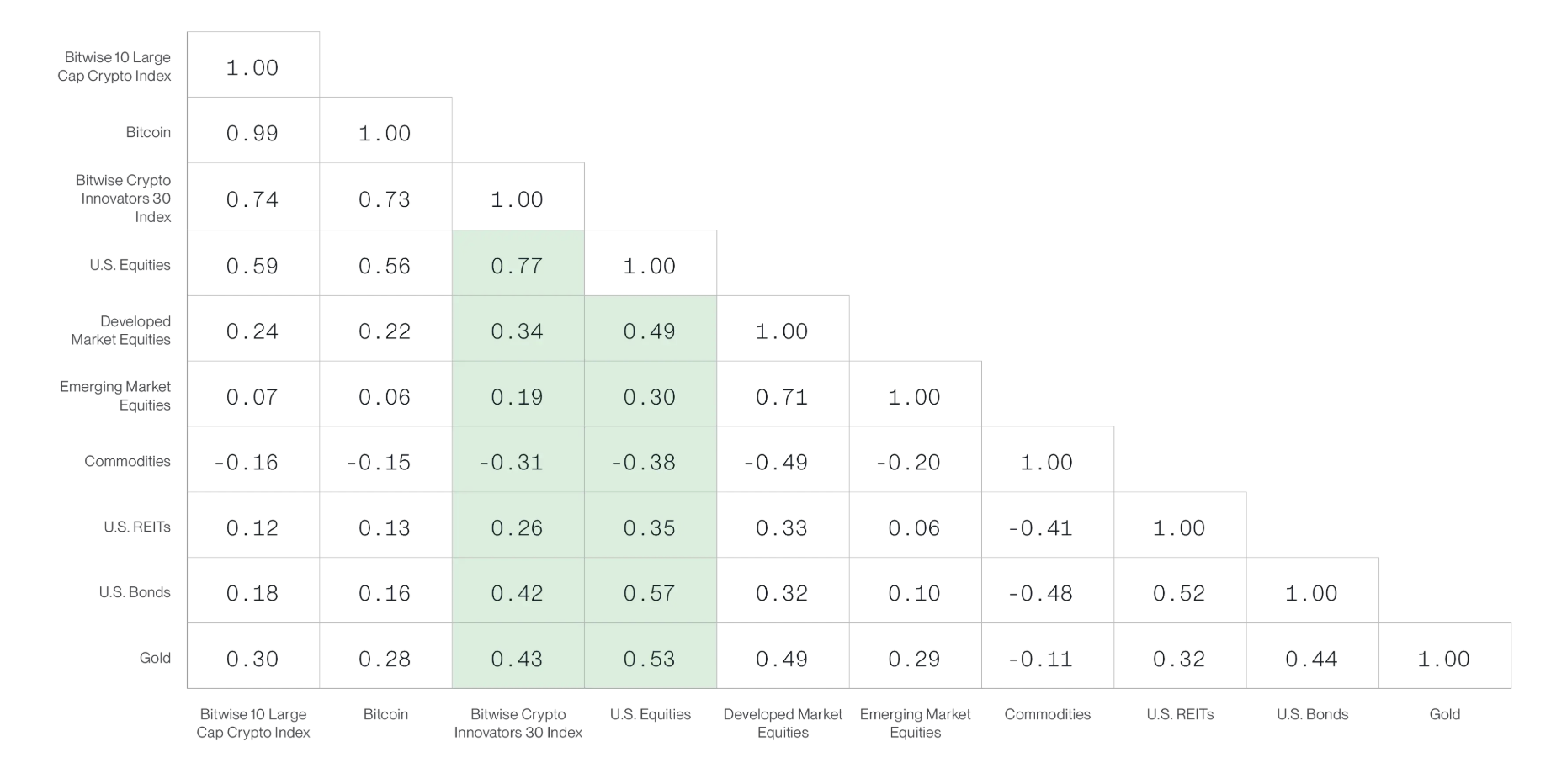

Crypto Stocks Have Low Correlation with Major Assets

Returning to crypto stocks, one of the most interesting charts is the 90-day rolling correlation of the Bitwise Crypto Innovators 30 Index with other major asset classes. Particularly striking is its lower correlation compared to U.S. stocks with nearly every other category: developed market stocks, emerging market stocks, U.S. REITs, U.S. bonds, and gold. (The sole exception is commodities, where correlation is negative for both.)

In other words: in the first half of 2026, crypto stocks returned more than double that of U.S. stocks while having lower correlation with almost every other asset in a portfolio. That combination of return and diversification is enough to get investors excited.

Correlation of select assets and asset classes (90-day rolling) is shown below:

Data from Bloomberg, as of June 30, 2026.

Conclusion

As you page through these charts, look closely. Almost every metric—price, on-chain activity, volume—is far from its all-time highs. Given that prices are down more than 50% from the October peak, this is unsurprising.

But compare the same data to the last bear market bottom—2022—on a cycle-over-cycle basis, and the picture is starkly different. Ethereum transaction activity is up about 13x compared to Q2 2022. DeFi TVL is up over 60%. Stablecoin size has roughly doubled. The only thing not keeping pace seems to be price.

I think this reflects exactly where we are: the market is pricing an industry that's twice the size it was at the last cycle bottom, with deeper liquidity and stronger fundamentals, as Wall Street finally moves on-chain—at bear market prices.

This kind of foundation can't stop a winter, but it does determine what will grow in the spring.

That's my take on the quarter. Of course, none of these 50+ charts can answer the question we've been asked most lately: "Have crypto prices bottomed?" But they do point to the resilient fundamentals of the crypto space—an area where usage, revenue, and adoption continue to grow even in a bear market.

To me, that's exactly what makes for an interesting area—and the foundation on which the next cycle will be built.