A few days ago, I came across a concept in Japanese philosophy: basho. Roughly translated as "place," but the philosopher Kitaro Nishida endowed it with a meaning far beyond a geographical location, more like a situation: a field where all things can become themselves. In other words: people do not appear in a place by accident, but are shaped by where they are. Today, I will use this theory to interpret Base.

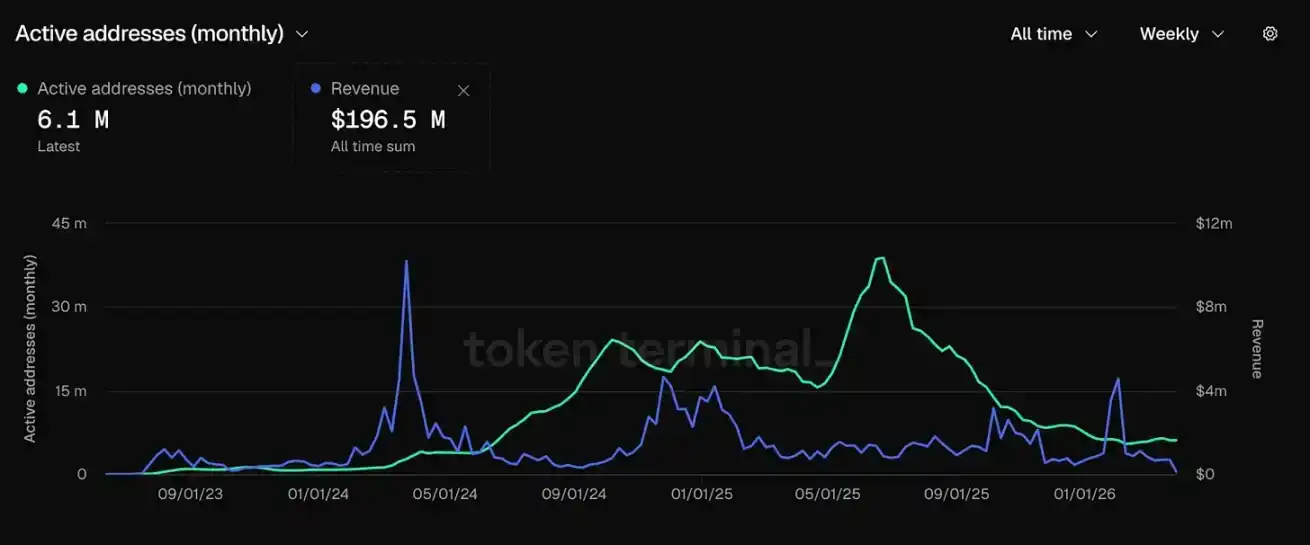

Last month, its number of active addresses fell to an 18-month low. Reflecting on this phenomenon, I realized: Base built only a location, but never created the conditions for things to grow and take shape.

When Coinbase launched Base in 2023, the crypto-native community surprisingly developed a kind of faith. Everyone believed that it could finally solve Ethereum's oldest problem: infrastructure everywhere, but no real users. And Coinbase, with 100 million users and unparalleled distribution capabilities, had a unique advantage. The door opened, and users were already waiting outside.

For a while, this confidence seemed to be validated. Base's growth rate surpassed all previous Layer2s. In October 2025, its Total Value Locked (TVL) reached $5.6 billion, and its fee income was unmatched in the entire L2 field. So, in September 2025, Base confirmed the issuance of a token, seemingly heralding an inevitably successful experiment. Yes, a place was becoming a basho.

Then, the users left.

Look at the data for a clearer picture: Base's active addresses returned to the level of July 2024. The token issuance expectation恰好满足了空投党的需求:拿到最后一笔报酬,然后走人.

Base's bet on the creator economy in 2025 also did not work. Its core was the Zora protocol, which tokenizes content by default. By the end of the year, 6.52 million creator and content tokens were issued on Base through Zora, of which only 17,800 remained consistently active throughout the year, accounting for 0.3%. The remaining 99.7% were already neglected.

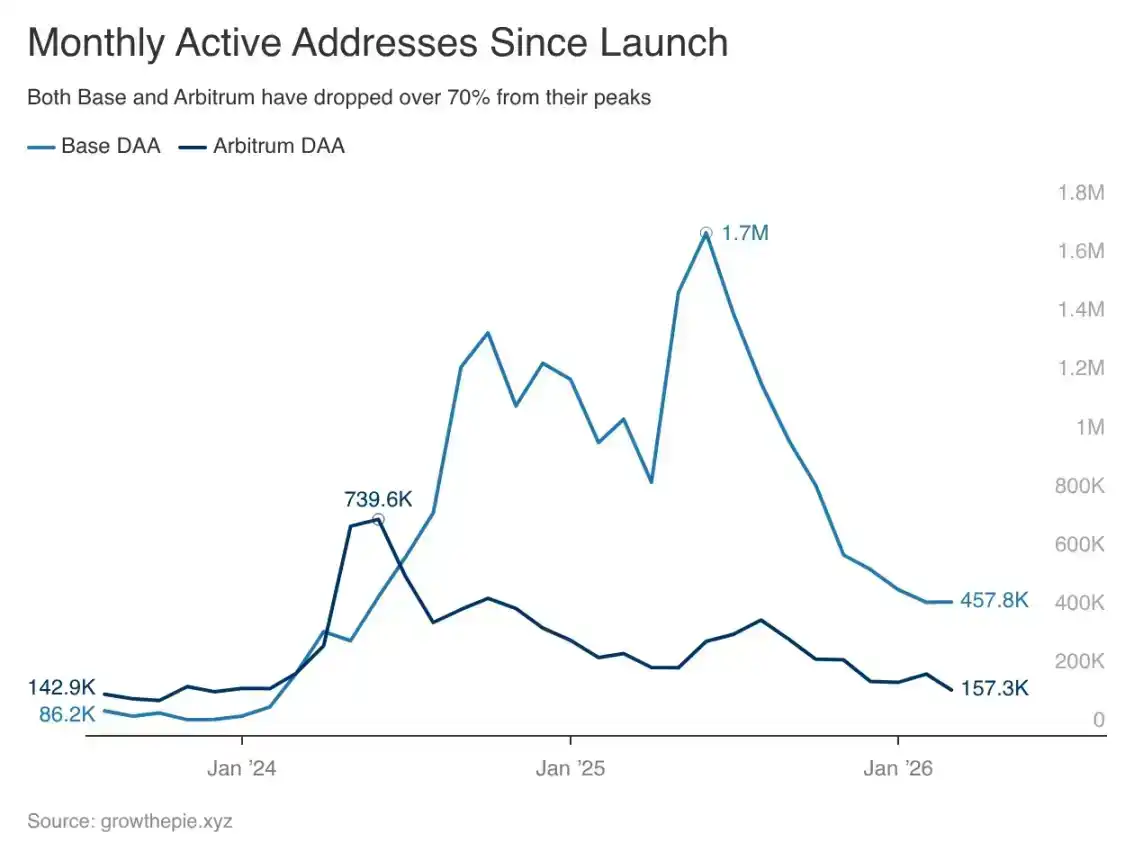

Base's daily active addresses peaked at 1.72 million in June 2025. By March 2026, only 458,000 remained, a sharp drop of 73% from the peak. After Armstrong announced in September 2025 that Base was considering issuing a token, active addresses decreased by 54% in just six months, meaning speculative capital has completely left the market.

Sociologist Ray Oldenburg once studied: what makes people return to a place repeatedly without compensation. He called it the third place, such as bars, barbershops, city squares. They are not efficient production spaces, but they give people a reason to return unrelated to incentives. The core is: the desire to come back cannot be artificially manufactured; it can only grow naturally from the possibilities provided by the place over time. The cryptocurrency industry designs places for the purpose of extracting value from users, and then wonders why no one stays.

This is a location without basho: people pass by, take what they need, and leave, because leaving costs nothing. No identity is formed here, no capabilities that cannot be replicated elsewhere within three weeks, nothing that makes leaving a loss. Do unique relationships exist on this chain? We have never built things with this mindset, have we?

You cannot build basho with financial incentives. Incentives can certainly pull people in the door, but they cannot make people *want* to stay. The desire to stay must come from the possibilities nurtured by the place over the long term. Kitaro Nishida called this "basho logic," referring to how the relational field shapes the things that emerge within it. The crypto industry designed fields for extraction, and was finally surprised to find that only extraction was born.

Brian Armstrong has publicly stated that the Base App now focuses on becoming a self-custody, trading version of Coinbase.

The former social and creator vision aimed at building social stickiness and allowing users to establish identities worth protecting on-chain has disappeared. Judging from the data, this is a rational decision, but it also admits: this vision never truly formed. Base has a location, and it now only focuses on serving past users, because that is all it can provide.

One Chain, One Track

Base is the most visible epitome of the entire L2 model.

Since June 2025, the usage of small and medium-sized L2s has overall declined by 61%. Most chains outside the top three have become zombie chains: active enough not to shut down, but deserted enough to be insignificant. The ratio of L2 to L1 daily active users has dropped from 15 times in mid-2024 to 10-11 times today. Most new L2s see usage collapse directly after the incentive cycle ends. The entire L2 ecosystem is cooling down, not just Base.

The Rollup-centric roadmap was once a theory about user adoption: reduce participation costs → users flood in → ecosystem forms → compound growth. The Ethereum Foundation released a 38-page vision document this year outlining Ethereum's future direction. The largest L2 by scale hit bottom in activity and left the OP Stack, while the second largest L2 has stagnant growth.

Reducing the cost of entry is not equal to creating the conditions for things to take shape. The industry solved the "entry" problem, but took it for granted that a "sense of belonging" would follow. It doesn't appear automatically, because a sense of belonging is not a feature that can be launched.

Farcaster is the product closest to building a basho in the crypto world. Because a specific group of people built a specific culture on it: developers sharing work, discussing Ethereum, forming opinions about each other over months. This takes time, and competitors cannot replicate it with higher rewards. Friend.tech tried to do the same thing with incentive mechanisms, topped the charts in a week, and died in a month. The same mechanism, but no culture was formed. The difference is not in the product, but in whether people stay long enough for something to truly take shape.

What Can Make People Stay?

The chains that retain users in the winter do not rely on more generous incentives.

Arbitrum's daily active addresses peaked at 740,000 in June 2024, and now stand at 157,000, also a sharp drop of 79%. Both chains are declining, but the underlying logic is completely different.

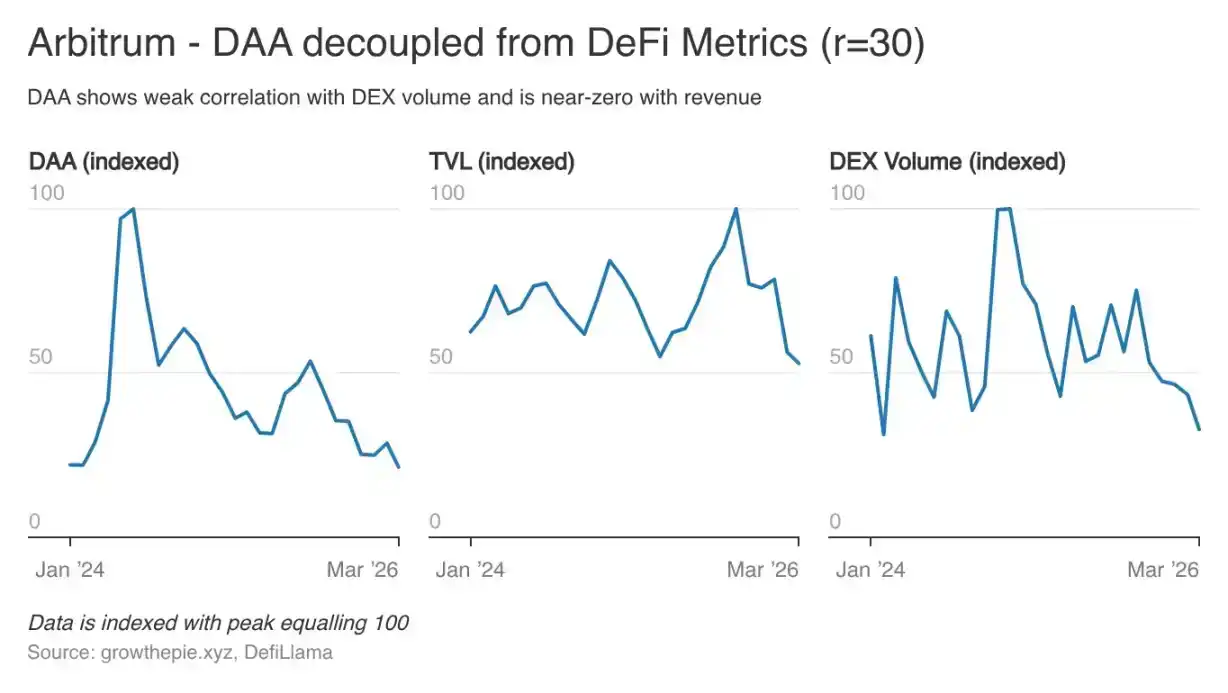

Base's users go online to trade, and they leave when trading volume decreases. Arbitrum's users, however, are unaffected by the level of transaction fees; the correlation between user numbers and fee income is almost zero. Base attracts tourists, while Arbitrum has somehow retained users.

Hyperliquid can stand firm because its trading experience is unique, and the community has formed an identity found nowhere else. Token incentives are almost irrelevant; being part of it has become part of their behavior and identity. Things shape users, and users in turn shape things.

The crypto industry is still optimizing "how to get people to come," while the question of "how to create a situation" is only remembered after the data crashes, never considered at the beginning of chain design.

I believe that Base, with the strongest distribution capability in history, could have solved this problem better than any other chain.

Now it is a trading app. This is a reasonable product direction, but it is also something that over 40 products are already doing. Trading apps cannot generate basho; they can only generate sessions: users come in when they have a trading need and leave when finished.

To truly become a successful application, a continuous connection needs to be established. Users need to build a relationship between each visit, making the next visit feel like a return, not just an arrival.

Armstrong's pivot is largely based on the lessons Base learned from the data. The social layer, creator economy, on-chain identity—these things that should have turned Base from "being used" to "being inhabited"—require patience, and the system does not reward patience.

The Ethereum ecosystem needs Base to be more than just a trading venue. The foundation of the entire L2 narrative is that chains can become infrastructure around which people build their lives. If the L2 with the strongest distribution capability in crypto history ultimately settles for being a faster Coinbase, then this narrative itself is untenable.

Kitaro Nishida believed that the deepest basho is where the boundary between the self and the place begins to dissolve. You cannot completely separate "who you are" from "where you are shaped." This sounds abstract, but applied to a public chain it means: a user cannot imagine their financial life after leaving a certain chain; a developer's entire toolkit is based on a certain ecosystem; their identity can hardly exist elsewhere.

As far as I know, such a thing has never been built on any L2. It might not be possible to build it under an incentive program at all.

Even if you have 100 million potential users, as long as there is nothing worth staying for, you will eventually end up with an empty building. Base understands this now.