Author:David Hoffman

Translation:Jiahuan, ChainCatcher

If you missed the news last week, I sold my ETH.

For someone who has built a career, community, identity, and business around Ethereum, making this decision was not easy.

The reason behind the sale requires a more thorough explanation than fragmented tweets on Twitter.

The 'ETH is Money' thesis did not fail... it has simply been realized. Ethereum has earned the ETH price it deserves, and I believe ETH as an asset will not be revalued, either upwards or downwards.

'ETH is Money' is the core narrative proposed by author David Hoffman in 2019 and long promoted through Bankless, advocating that ETH should become a global store of value. It was once one of Ethereum's most mainstream bullish logics.

Note: I am extremely bullish on Ethereum. I expect the Ethereum network to perform exceptionally well from here on out. However, I believe that only a tiny fraction of this success will be reflected in ETH.

The article text is as follows:

'ETH is Money' Has Always Been an Aspiration

Money is a coordination game, and coordination is very difficult.

The Ethereum project itself is a series of coordination challenges stacked upon multiple levels, and the 'ETH is Money' thesis demands that all these levels succeed, and succeed unequivocally.

ETH can only become money if and only if every layer of Ethereum's techno-social stack performs better than its competitors.

Given the ambition of the Ethereum project, achieving its most successful version was always a monumental challenge. Despite shortcomings, the Ethereum project has performed admirably, fully deserving its current market capitalization.

Nevertheless, the window of opportunity for $ETH to be 'revalued' by the market seems to be closing.

In a sense, ETH is money. But it is not the most successful version we collectively aspired to.

Ethereum is a Coordination Game

A Turing-complete blockchain is such a powerful idea that Ethereum's maximum potential is the entire crypto world. Everything.

The only obstacle to Ethereum achieving 100% absolute domination over everything is coordination.

Ethereum's leadership needs to be sufficiently decentralized; governance needs 'rough consensus' to create credible neutrality, maximizing Ethereum's adoption at the highest level.

Ethereum's leadership needs to respond quickly to market dynamics, operating like a startup facing an existential threat of marginalization.

Ethereum L2s need to be able to operate and make their own market choices independently from the base layer, but they also need to be economically bound and constrained by the broader Ethereum economy and brand.

Ethereum's roadmap needs to be executed in a specific order to maximize and maintain Ethereum's momentum and market dominance, thereby fully subduing competition and maximizing confidence in Ethereum and ETH.

Key technology R&D and engineering implementation need to be fast enough so that Ethereum can both prove its utility to the outside world and stay ahead of competitors.

The 'ETH is Money' thesis is about creating an extremely revolutionary and powerful financial asset that, by virtue of its unique properties as the premier global store of value, attracts individuals who would otherwise be indifferent.

Ethereum's brand and ETH's strength need to be so powerful that traditional large capital not only feels safe but actively includes ETH as a significant position in retirement portfolios due to the dominance of the Ethereum project.

For 'ETH is Money' to happen, everything upstream of ETH needs to function in an extremely perfect manner.

Ethereum is not Bitcoin; it chose the hard path. Bitcoin chose to strip everything from its blockchain to elevate BTC.

Ethereum chose to add everything to its blockchain to maximize the utility of its block space. Only by doing this in the best possible way before competitors can ETH attain its status as global money.

We've come a long way, and Ethereum has already achieved the maximum potential market share it deserves.

I fear the window to play this game has closed.

The Macro Environment May Never Allow It to Happen

Looking back over the past few years, I see that Ethereum needed to overcome numerous macro-environmental challenges.

1. L1 Asset Valuation is Inextricably Linked to Revenue

Say what you will about how hard it is to value smart contract chains based on fees and revenue, but fees and revenue are clearly how smart contract L1 assets increase their pricing power.

By 2026, we have ample data showing that all these factors are closely correlated: L1 activity, L1 fees, and the price appreciation of the L1 native asset.

In 2021, when ETH had the highest L1 revenue market share, it dominated.

In 2024, when SOL's L1 revenue market share surged across the industry, it dominated.

In 2026, NEAR is experiencing price revaluation alongside fundamental growth in its L1 revenue and NEAR burn.

You can also look at assets like BNB and TRX, perhaps the highest cumulative revenue projects ever. Their price charts look the way I once expected ETH's should—provided ETH could maintain its L1 fee dominance for longer than just that stretch in 2022.

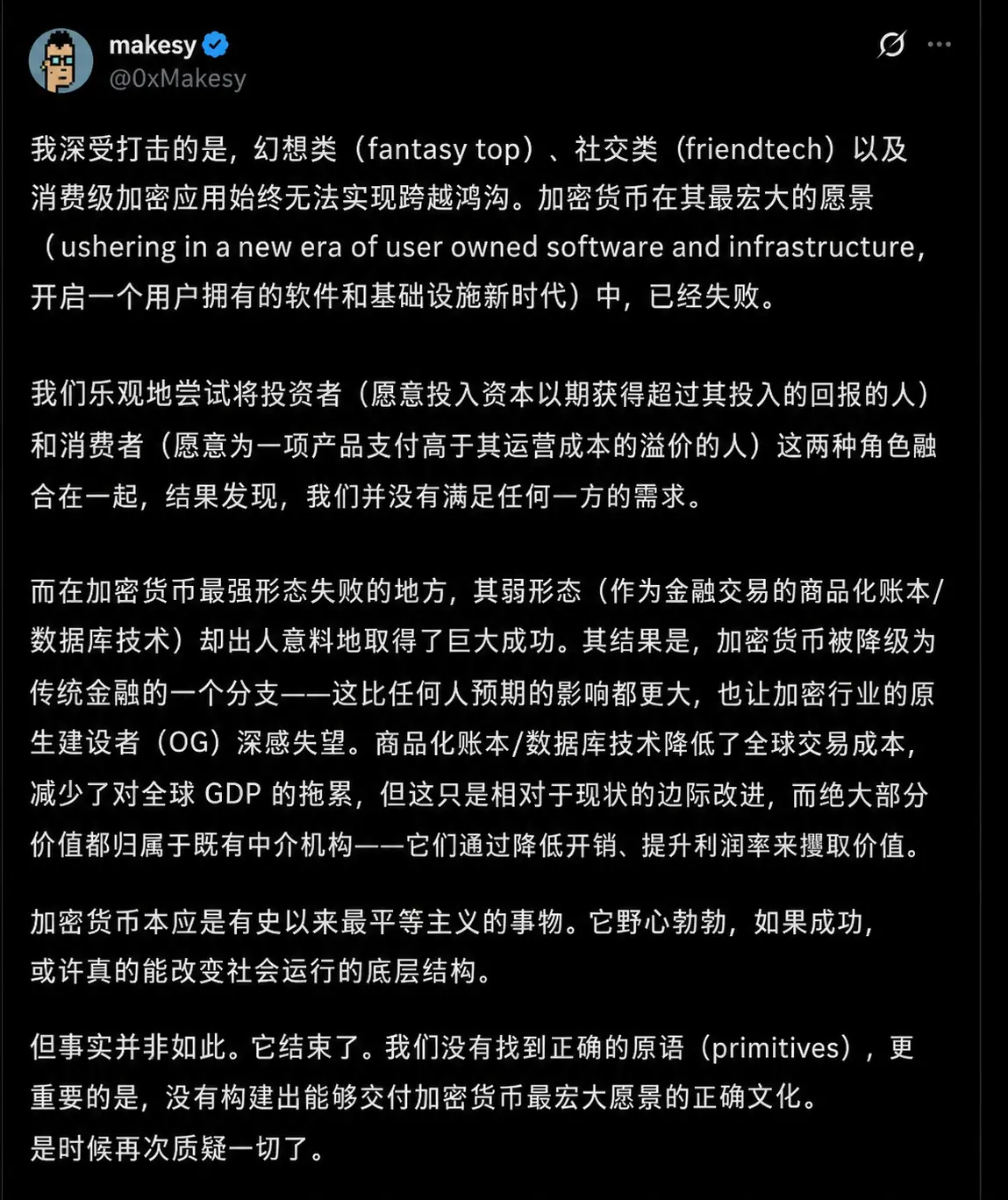

2. The Strong Version of Crypto Didn't Work

@0xMakesy put it well:

Ethereum represents the strong version of crypto, crypto for crypto's sake, self-sustaining and self-perpetuating. DeFi, NFTs, DAOs—we were rebels, building an alternative financial system of, by, and for the people, plugging imagination into the money system.

Simultaneously, there exists the weak version: efficient ledger infrastructure for financial institutions' backends. The weak version would fuel the strong version, converting demand for internet ledgers into inward-flowing capital streams toward crypto, toward Ethereum, ultimately converging on ETH.

Perhaps if Ethereum executed better, faster, stronger, and if crypto hadn't attracted such a massive cohort of speculative charlatans and value extractors, the industry could have won the influence and respect I always thought it deserved.

But the only period where crypto maintained a positive brand image with the general public was from late 2020 to early 2022. Outside this narrow window, crypto's reputation has been one of fraud, scams, get-rich-quick schemes, and uselessness to the average person.

'ETH is Money' Relies on 'Strong Crypto'

Right at the moment when everyone was forced online, ETH emerged as the internet's money. The world discovered crypto for the first time, and for that brief window, it was very cool.

Money is a coordination game, and a currency's Schelling Point (consensus focal point) is held together by belief. In 2021, the broader public believed in ETH: it was cool, disruptive, and populist. Bitcoin possessed the same properties and has retained them better than ETH post-2021.

This raises a disquieting possibility: the strong version of crypto may never have been a stable equilibrium point. COVID was an extremely distorted time for money, and perhaps 'ETH as Money' was only propped up by that distortion.

If that's the case, ETH becoming money always depended on the strong version of crypto working better than it has in reality.

3. Ethereum's Utility Also Benefits Other Monies

Is Bitcoin money? Is the Dollar money? Is Gold money? It doesn't matter—whatever is money will be tokenized on Ethereum.

In 2020, Nic Carter posited on Bankless that stablecoins would likely be parasitic to ETH as Ethereum's native unit. Back then, Ethereum had $3B in stablecoins. Today, that number is $163B, a 54x increase.

The utility Ethereum provides is helping to expand the monetary network of any asset that truly is money, which is why the US is so bullish on crypto for stablecoin adoption. Ethereum is helping the US maintain dollar hegemony, and leveraging this fact is explicit government policy.

Clearly, the positive spillover effects garnered by $ETH as money are far less potent than those seen by the US government in Ethereum's stablecoin ecosystem.

Ethereum is a Giver, Not a Taker

At its core, Ethereum is a giver, not a taker.

It provides the world's most secure block space to L2s at cost.

It tokenizes the world's assets at cost.

It secures billions in DeFi at cost.

Ethereum takes no markup on anything it does.

This is the nature of open-source software and the power of Ethereum. Ethereum provides its full suite of immensely valuable goods to the world at cost.

Ethereum is noble. Ethereum is good.

Ethereum is the world's most successful non-profit organization.

Naturally, incredible mass adoption will occur on Ethereum. It has been and will continue to be one of the most impactful open-source software projects ever built by humanity, and being a 'non-profit protocol' is one of its core features.

This is why ETH's path to becoming money depended on maintaining sustained and extremely high market dominance.

Ultimately, as block space becomes commoditized, fees will trend towards zero. So long as it's Ethereum that gets commoditized and not its competitors, Ethereum can maintain its margins and dominance.

Ultimately, the fat protocol theory (referring to the idea that the majority of economic value will be captured and monopolized by the foundational protocol (like Ethereum), not by the application layer built on top, as in traditional internet models) will give way to the fat application theory, and applications will swallow the remaining profits.

So long as they are Ethereum's applications and not a competitor's, that's fine for ETH.

It's hard to square 'ETH is Money' with 'Ethereum is a giver, not a taker.' Ethereum's architecture is intentionally designed to give everything back to its ecosystem and only take the minimum required to keep the network running.

Architecturally, ETH is not prioritized within Ethereum; this is a feature, not a bug. ETH could only become money if Ethereum won a battle it was architecturally refusing to fight.

This could have worked if Ethereum could have maintained incredible market dominance.

This Thesis Asks Too Much of Ethereum

'ETH is Money' requires everything about Ethereum to go right. The margin for error is much smaller than I originally thought. Ethereum's momentum in 2021 and 2022 made 'ETH is Money' seem like the default path.

In hindsight, Solana's rise in 2021 alongside rising anti-Ethereum sentiment was the first major sign that Ethereum and ETH's coordination game wasn't going as planned.

The Ethereum Foundation needed to decentralize and allow alternative power structures to emerge. But it also needed to respond to market forces with the urgency and drive of a startup facing an existential elimination threat.

L2 teams needed the freedom for self-determination, but also needed to operate under the larger protective brand of Ethereum and ETH. The technical synchronicity integration between Ethereum and its L2s needed to be executed much faster.

Smart contract chains are valued via fees; to break out of this mold, Ethereum needed to rewrite the rules with overwhelming success.

My Reason for Selling

It just didn't reach its maximum potential either.

Ethereum did a noble thing, choosing for itself the hardest, most ambitious, most ideologically pure path for its future.

It secured some incredible wins and failed to win others.

Ethereum has earned the market cap it deserves.

I am very bullish on the Ethereum network and its ecosystem—Ethereum is architected to maximize the success of its apps, L2s, and ecosystem. The fat application theory means Ethereum's apps take all the fees, and the rollup-centric roadmap means L2s take 97% of the profits.

As for ETH the asset, I have a hard time seeing it being structurally revalued, either up or down.

Therefore, my reason for selling ETH is not bearishness on ETH; it's that I believe the 'ETH is Money' thesis has been realized, and I wish to allocate capital to other opportunities in the market that I'm bullish on.