Written by: Jon Ma, Co-founder of Artemis

Compiled by: Saoirse, Foresight News

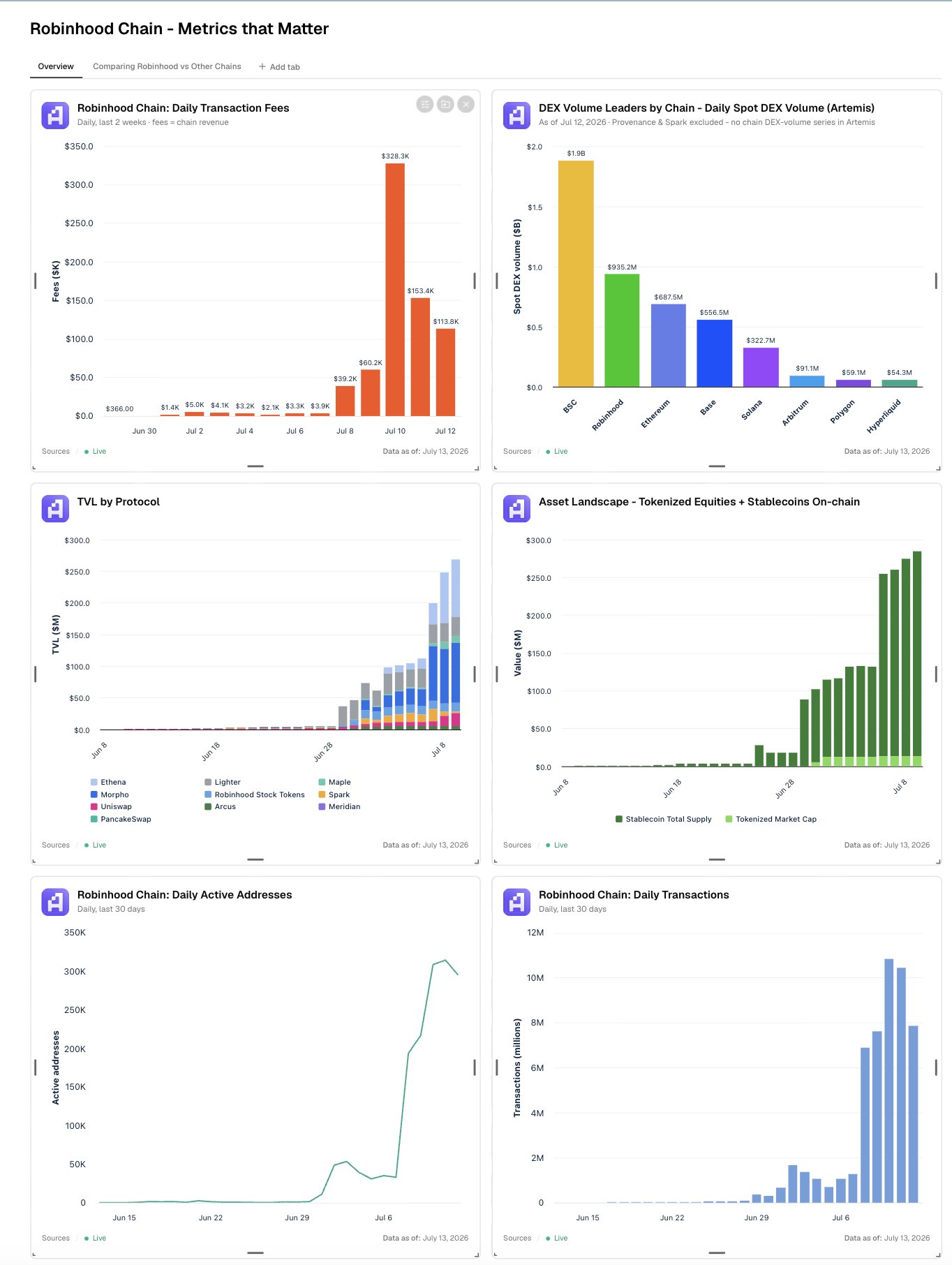

Robinhood Chain has made an impressive start on its path to promoting inclusive finance:

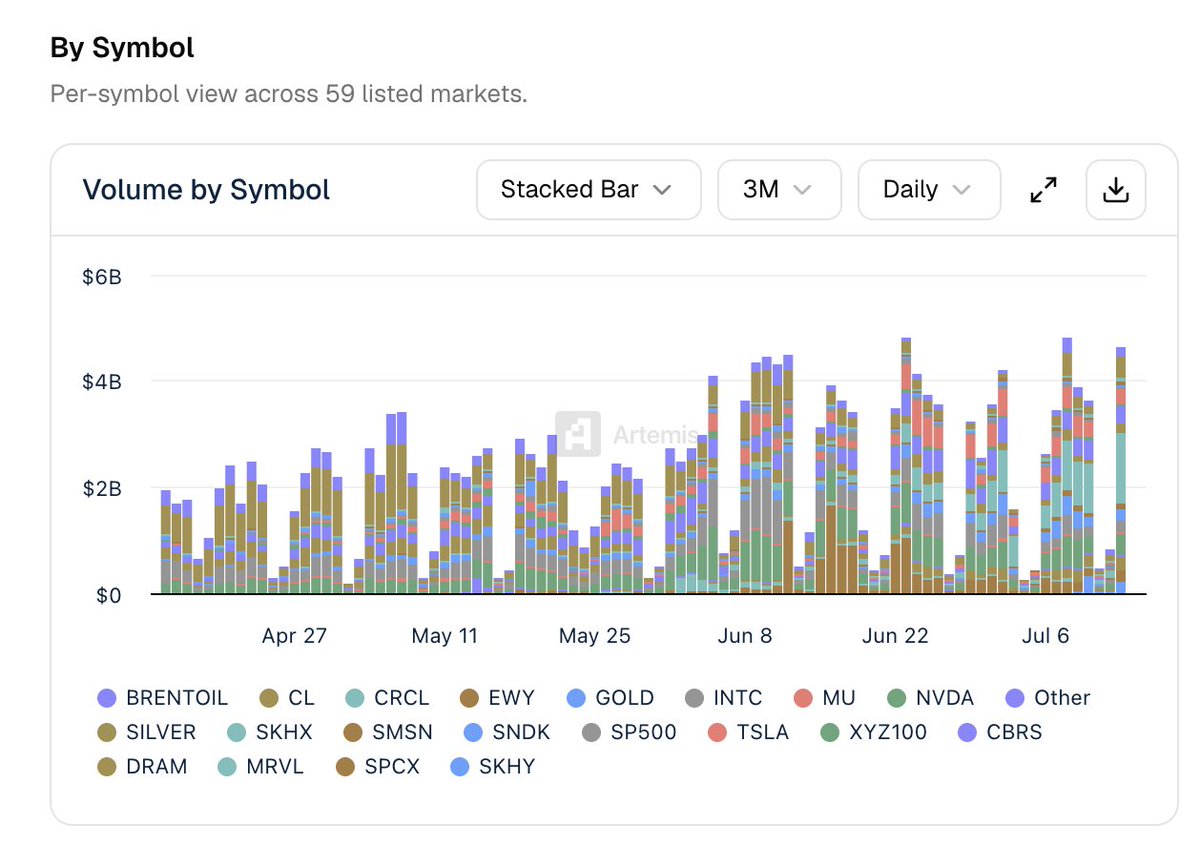

- Over 300,000 daily active addresses;

- Spot decentralized exchange (DEX) daily average trading volume exceeds $1 billion, ranking second among public chains;

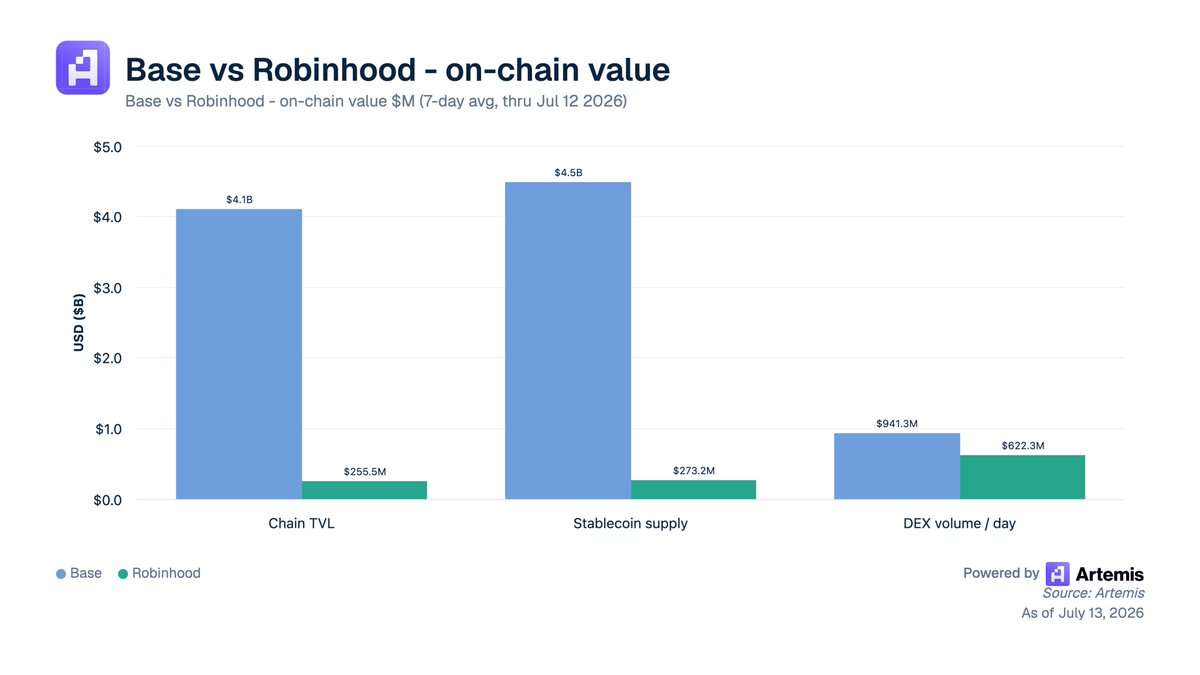

- Stablecoin circulation scale of approximately $300 million;

- On-chain annualized fee revenue over $40 million;

- Projects like Morpho, Ethena, and Uniswap have driven the total value locked (TVL) on-chain to surpass $300 million.

Related data dashboard: https://www.artemis.ai/jon/dashboard/334077439341928255

I participated in Robinhood's pre-IPO funding round in 2019 via @whalerock and followed Coinbase's IPO roadshow coverage in 2020. My original intention was to guide people to invest in quality assets with long-term value in the crypto and stock markets, not to speculate on Meme coins.

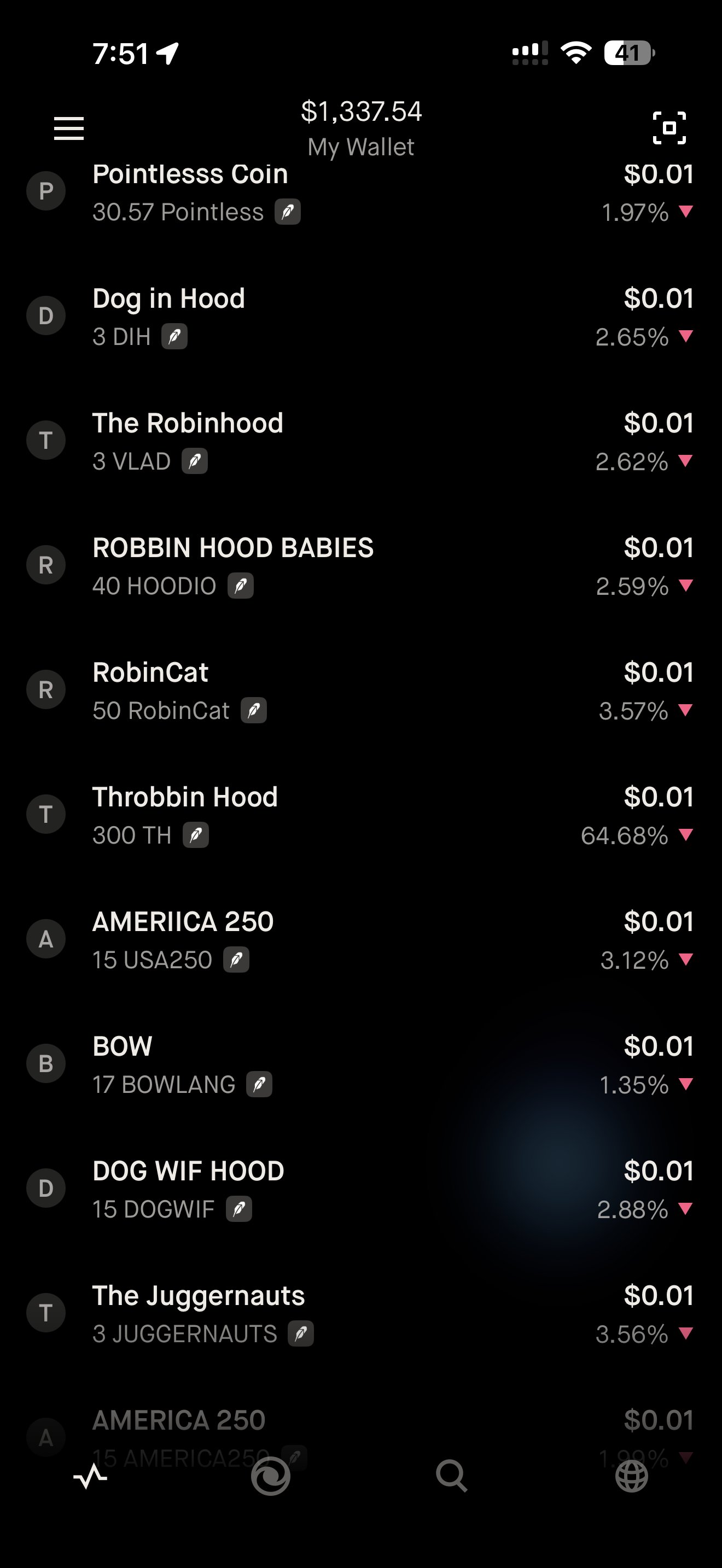

Last week, I opened the Robinhood wallet and was genuinely shocked and disappointed: the platform's available trading options were almost exclusively various Meme coins. After purchasing a small amount of CASCHAT, my wallet received a flood of random, worthless token airdrops within just three days, including one even named "Pointless Coin."

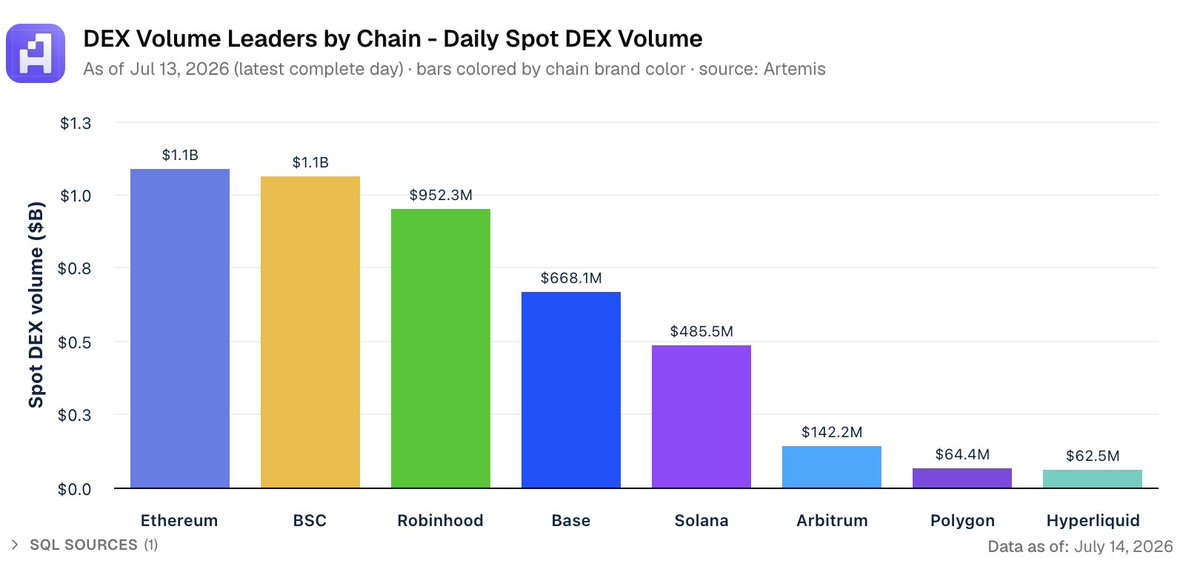

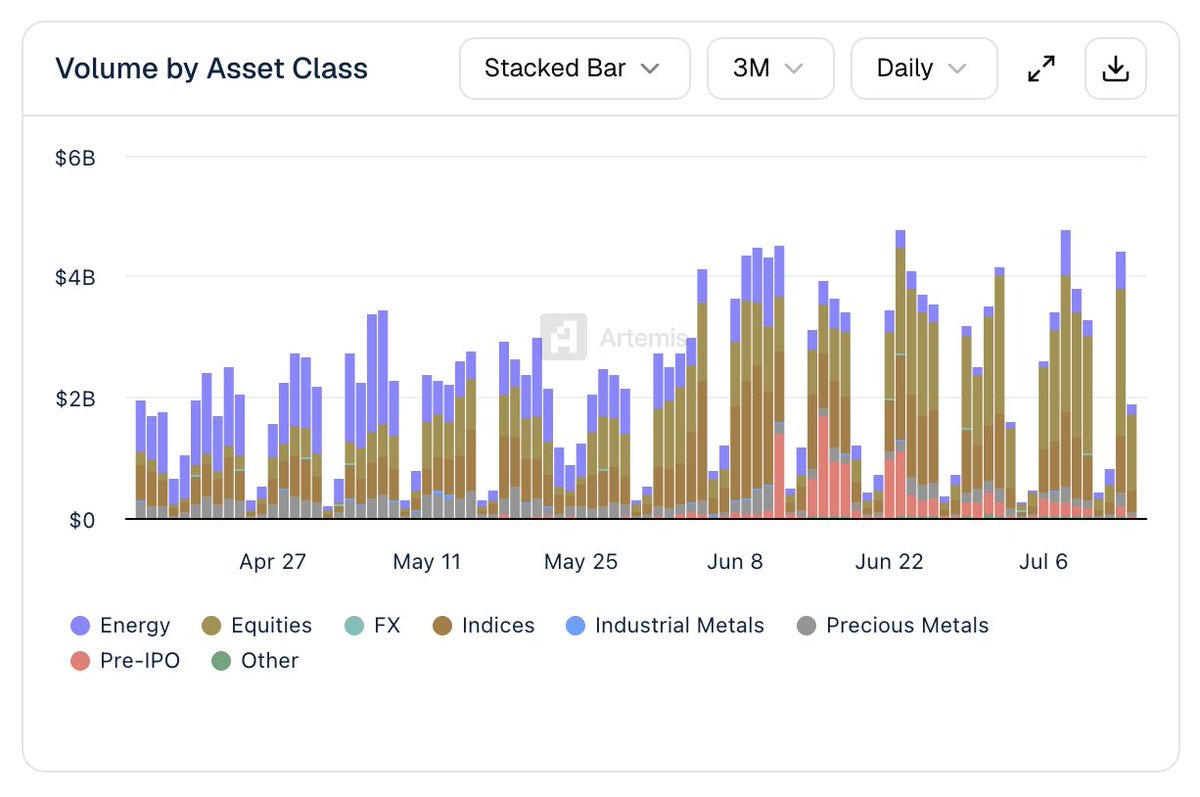

It's undeniable that Robinhood currently ranks third in spot DEX trading volume across all networks.

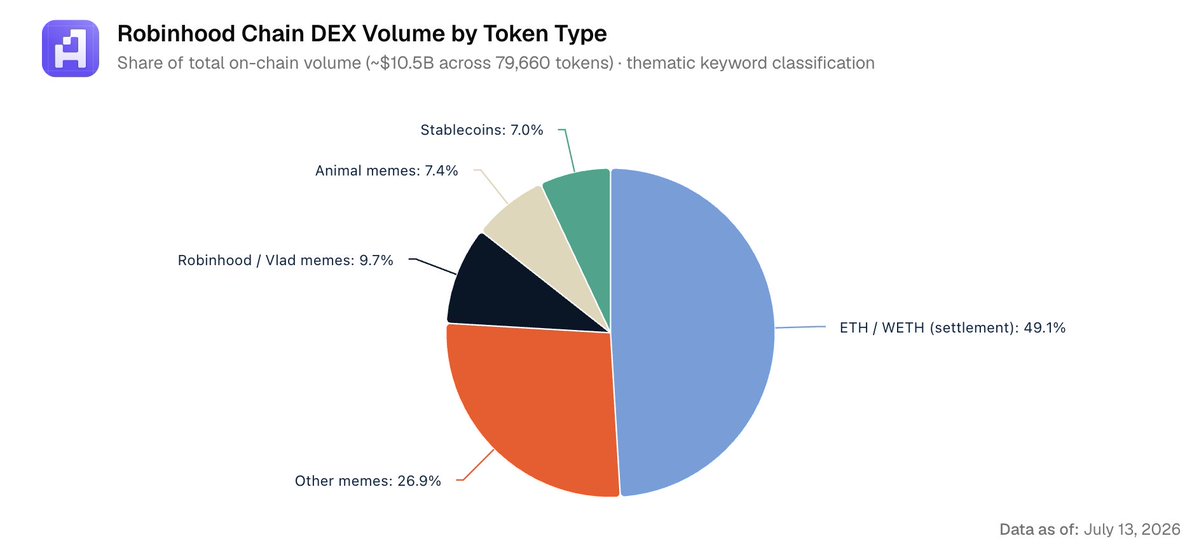

However, the vast majority of this trading volume currently comes from various Meme coins — animal-themed Memes, Memes derived around Vlad (Vlad Tenev, Robinhood Co-founder and CEO) and Robinhood, and a myriad of generic Meme tokens. I sincerely urge Robinhood: please do not turn this public chain into a dedicated Meme coin chain.

Coinbase's Base chain developed earlier and has a larger scale. There is a wealth of experience in Robinhood's crypto business worth learning from.

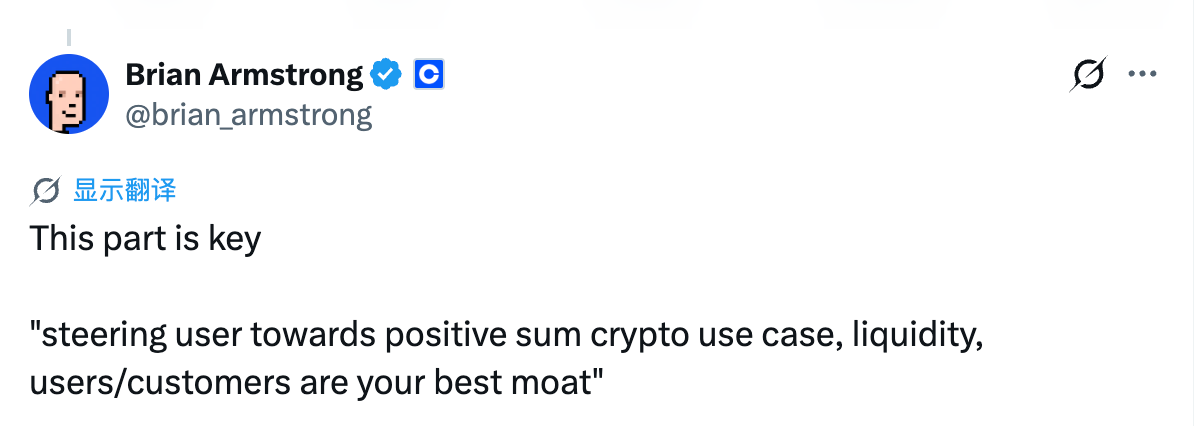

Brian Armstrong (Coinbase Co-founder and CEO) has repeatedly emphasized in public responses the need to guide users towards real, sustainable, and value-driven applications:

Source: https://x.com/brian_armstrong/status/2076506839953629445?s=20

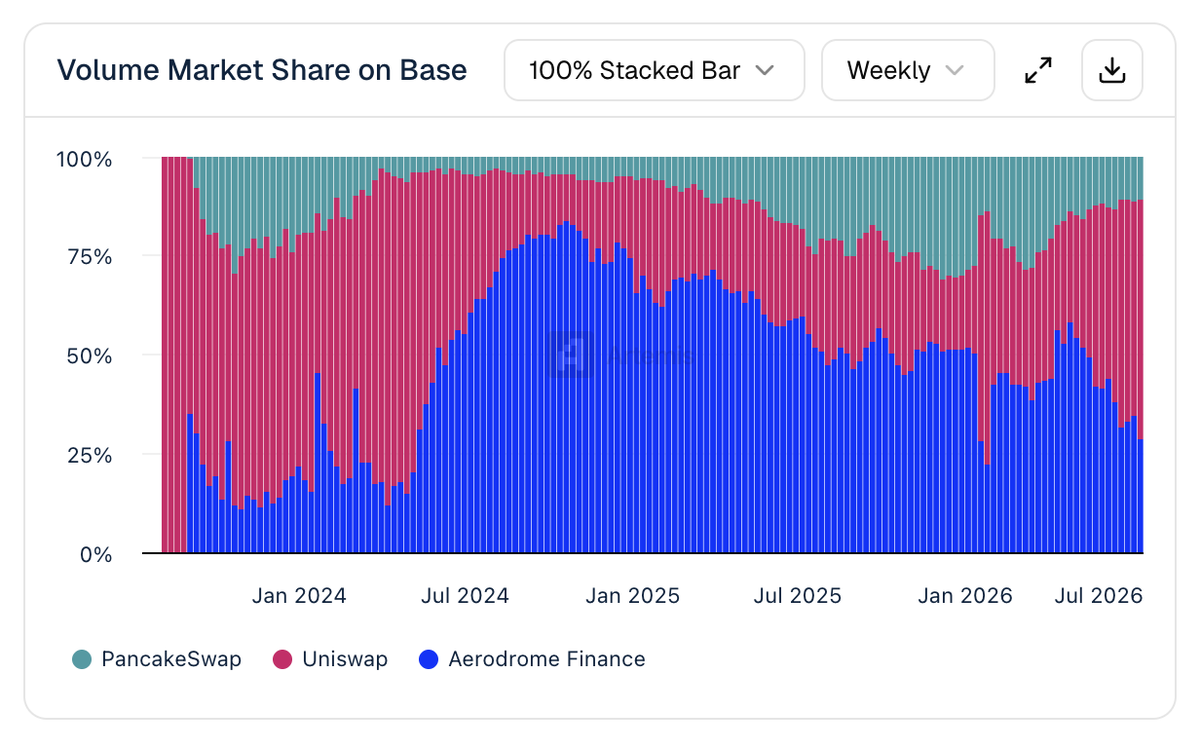

I understand the platform's difficulty in resisting the allure of Meme coins: such tokens are a shortcut to acquiring early users, attracting market makers, and boosting liquidity and trading volume. Many believe in "come for the Meme, stay for the real application." Just like Aerodrome on Base chain, which dominates the chain's trading volume and has built a sustainable business model.

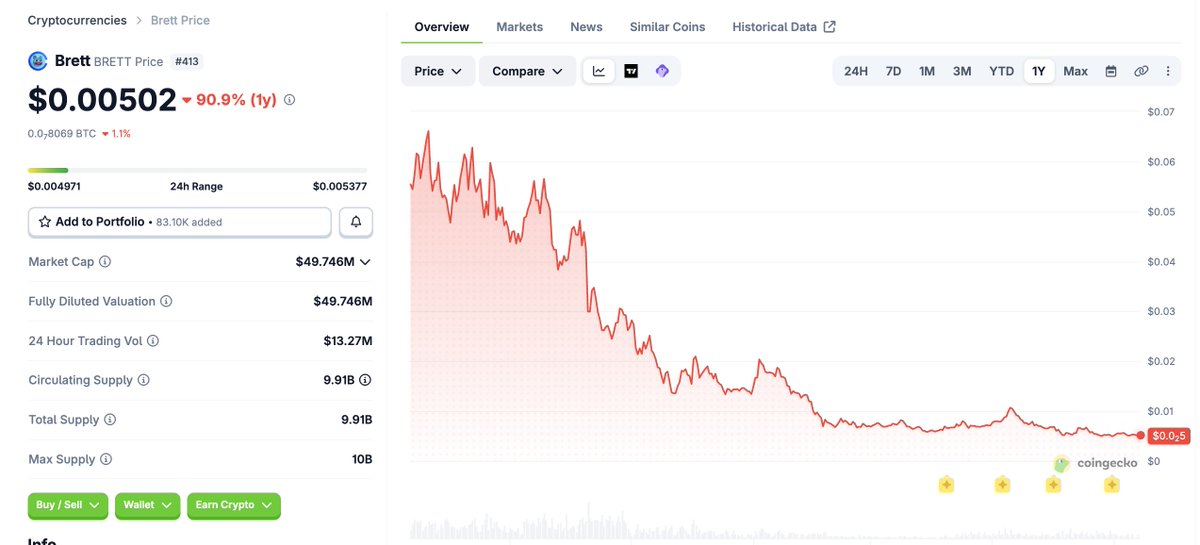

However, Meme coins can cause significant losses for many users, eroding trust in the industry. Look at the Meme coins launched on Base chain in early 2024 as a cautionary tale: their prices plummeted another 90% this year, with a maximum drop of up to 99% from their peaks.

Meme coins lack long-term vitality. They not only harm ordinary investors but also make retail investors increasingly averse to blockchain. Furthermore, if Robinhood Chain continues to be flooded with Meme coins, it will reinforce the existing perception on Wall Street and among major hedge funds: Robinhood is merely a speculative trading app that rose to prominence on the back of the 2021 GME (GameStop stock ticker, the famous Meme stock) and Meme stock frenzy.

Source: https://x.com/vladtenev/status/2074695821896065360?s=20

Wall Street already struggles to view Robinhood objectively. Do not repeat the mistakes of 2021 that damaged the brand's reputation.

On the contrary, Robinhood Wallet and its ecosystem should direct liquidity and resources towards Arcus (built by the former dYdX team, a veteran top-tier perpetual contracts DEX) and the tokenized stock sector. I am very optimistic about Arcus's vision: enabling anyone globally to trade spot tokenized stocks.

These types of stocks have only emerged in the past decade.

Please have Robinhood Chain genuinely focus on the real-world asset tokenization (RWA) sector, broaden the boundaries of financial services, and allow more investors to trade stocks and shares of pre-IPO companies.

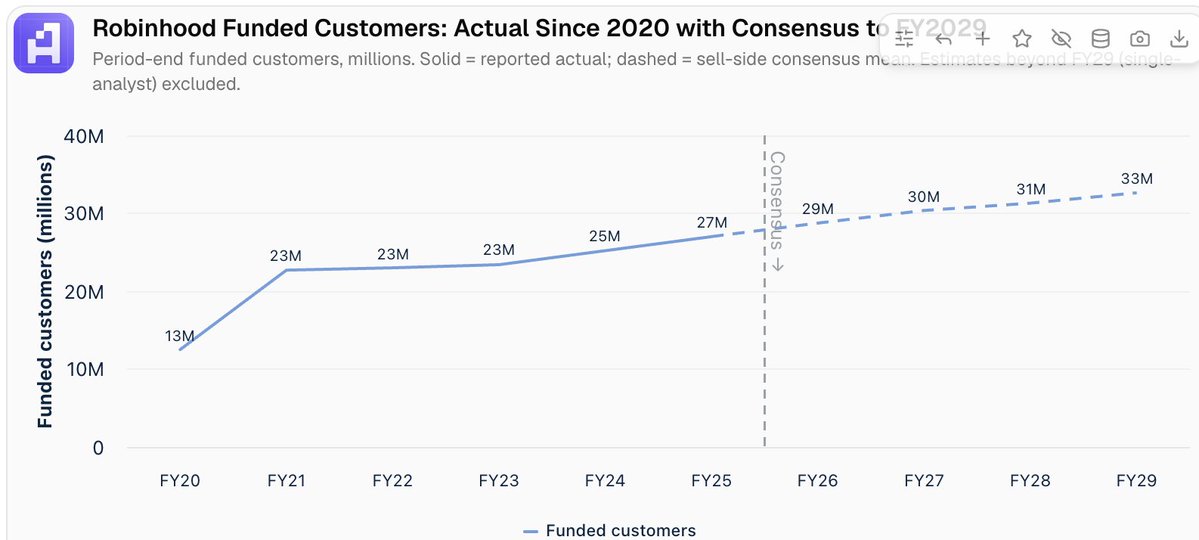

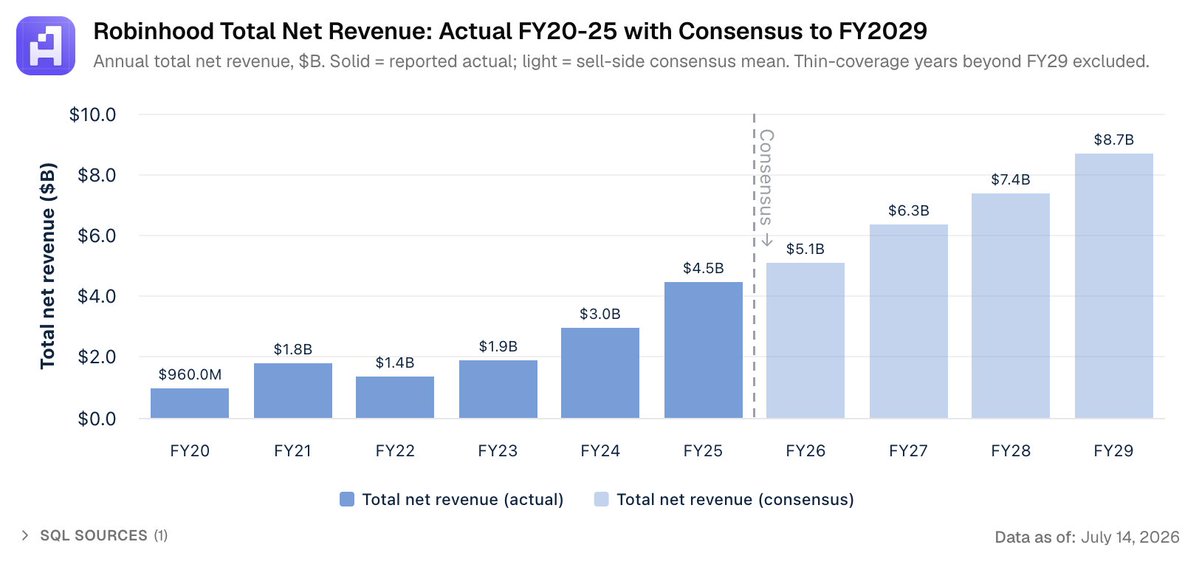

Robinhood faces its biggest potential downside risk: the US domestic market is nearing saturation. The platform currently has 27 million funded accounts, with institutional forecasts predicting account growth to only 31-32 million by fiscal year 2028, indicating limited room for expansion.

The core logic of my bullish view on Robinhood is: leveraging Robinhood Chain to reach over 100 million new overseas investors. Users can participate in RWA, prediction markets, stablecoins, and investments in listed and Pre-IPO assets via the public chain, while continuously feeding upstream traffic to the public chain App.

Tokenized stocks, traded around the clock, have genuine market demand. Referring to the trade.xyz platform, users primarily trade assets corresponding to real-world enterprises like SKHY, which has annual real revenue as high as $68 billion.

Here's a projection: leveraging Robinhood Chain, assuming the company reaches 100 million monthly active users by 2030. The current platform ARPU (Average Revenue Per User) is about $171; overseas users are more likely to pay on-chain transaction fees rather than trade via the App with higher commission rates. Conservatively assuming an ARPU of $100 for overseas users, just the C-side business could generate $10 billion in revenue by 2030, surpassing Wall Street's forecast of $8.78 billion for fiscal year 2029.

Vlad Tenev (Robinhood Co-founder and CEO), Johann Kerbrat (Robinhood SVP, Head of Crypto and International Business), you have an exceptional opportunity: leverage asset tokenization to fulfill crypto's original promise — providing equal access to financial services for everyone worldwide.

Do not squander this opportunity by turning Robinhood's public chain into a Meme coin chain. If you choose the right direction, Wall Street, hundreds of millions of users, and the whole world will recognize you for it.