21Shares is set to launch its Dogecoin ETF after gaining approval from the U.S. Securities and Exchange Commission (SEC) and Nasdaq. This is expected to provide some bullish momentum for the meme coin even as DOGE funds see muted interest from institutional investors.

21Shares To Launch Dogecoin ETF After Filing Final Prospectus

Crypto ETF issuer 21Shares has filed the prospectus for its Dogecoin ETF, signaling plans to launch this fund this week. However, the asset manager has yet to announce a specific launch date. This will be the third spot DOGE fund to launch after Grayscale and Bitwise’s DOGE ETF, which launched last year.

21Shares Dogecoin ETF will launch on the Nasdaq under the ticker ‘TDOG.’ Crypto exchange Coinbase is listed among the Trust’s custodians alongside BitGo and Anchorage. Meanwhile, the fund will offer in-kind creations and redemptions, similar to other existing spot crypto ETFs. 21shares will charge a 0.50% management fee for the fund.

The Dogecoin ETF will be 21Shares’ fifth spot U.S. crypto ETF, as the asset manager already offers Bitcoin, Ethereum, Solana, and XRP ETFs. The DOGE fund’s launch is bullish for the foremost meme coin as it could attract more institutional flows into its ecosystem. However, it is worth noting that the other existing spot U.S. DOGE funds have only seen moderate demand so far.

SoSoValue data shows that the inflows into these Dogecoin ETFs have been minimal, with these funds currently boasting net assets of just under $10 million, which is less than 1% of the meme coin’s market cap. They have also mostly recorded zero-flow days since launching, with most inflow days below $1 million. However, it is worth noting that these funds saw greater demand at the start of the year, when DOGE rose to around $0.15. As such, they could attract more inflows as the market recovers.

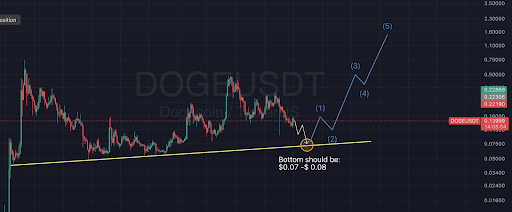

A Generational Buying Opportunity

Crypto analyst Hokage described the current DOGE price level as a generational buying opportunity amid the imminent launch of the Dogecoin ETF. This came as the analyst remarked that while the short-term is extremely hard to figure out, the long-term support will eventually get hit. His accompanying chart showed that the leading meme coin could rally to as high as $1.6 in the long term.

The crypto analyst highlighted the potential integration of Dogecoin into Elon Musk’s X as one catalyst that could spark this run. He opined that the meme coin will eventually get integrated into X as a payment and tips feature. Hokage added that it is just a matter of time and not if.

Related Reading: Dogecoin Is Breakout Ready: Analyst Shows Major Target For The Meme Coin King

At the time of writing, the Dogecoin price is trading at around $0.137, down over 2% in the last 24 hours, according to data from CoinMarketCap.