By Lin Wanwan

Money already lives in the code.

Six months ago, AI payment was just a concept on presentation slides. Now, AI is becoming the "checkout counter".

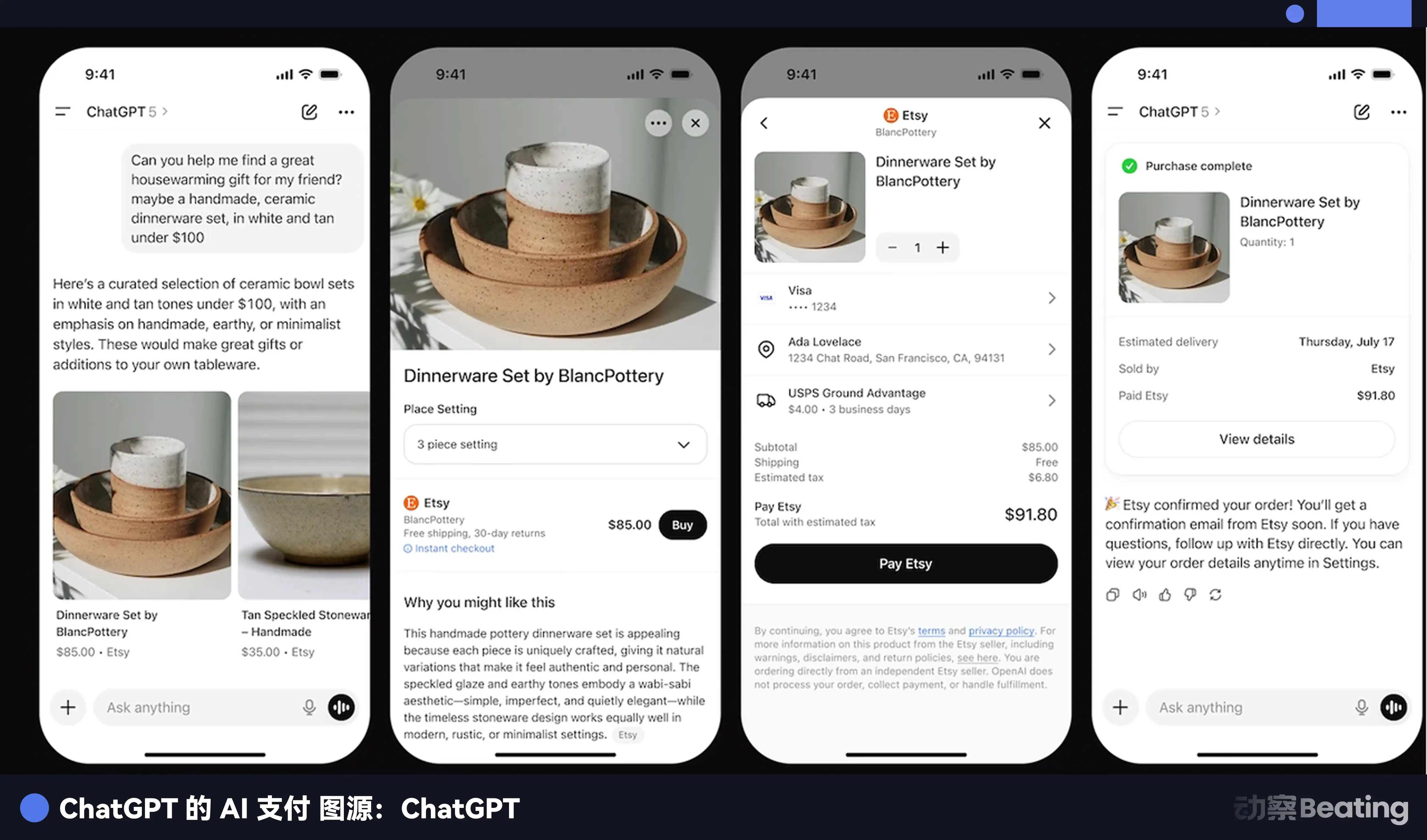

Open ChatGPT today, search for any product, and you'll see a blue Buy button. Enter your address, pay, and it ships. The entire process happens without redirects or opening any web pages.

Last week, Google followed suit, integrating products from Etsy and Wayfair into its Search and Gemini, allowing checkout directly within the conversation. Microsoft's Copilot simultaneously launched its shopping checkout feature. Meta's Zuckerberg just announced a full shift towards AI agent commerce.

But a more covert business battle is also quietly unfolding. The fight over AI payment tolls can be traced back to the two major AI payment camps in the fall of 2025.

On September 16th, Google gathered over 60 companies and released an "AI Agent Payment Protocol".

The list was full of familiar names from traditional finance: Mastercard, PayPal, American Express, plus a few allies from the tech circle.

On the 29th of the same month, Stripe, jointly with OpenAI, released another protocol, the Agentic Commerce Protocol (ACP). Stripe simultaneously announced it was testing ACP-based agent commerce solutions with AI-native players like Microsoft Copilot, Anthropic, and Perplexity.

The two lists had little overlap. Coinbase appeared in both Google's AP2 ecosystem and is a long-term partner of Stripe.

What these two camps are fighting over is a question that sounds mundane but is worth trillions: When AI spends money on behalf of humans, through whose pipe does the money flow?

You might think this is far from you. But think about it: you now ask ChatGPT to book flights for you, use an AI assistant to compare prices and buy things, or have an Agent automatically purchase office supplies. These scenarios are visibly becoming reality. Every transaction needs a pipe to move money from your pocket to the merchant.

Whoever builds this pipe can charge a toll on every transaction.

This is the essence of this war.

12 Months Changed by a Roundtable

The story starts with a dinner.

In the summer of 2024, Stripe hosted then-U.S. Deputy Treasury Secretary Wally Adeyemo at its San Francisco headquarters for a fintech roundtable.

A group of payment company CEOs sat around chatting. Among them were two people who had never met before: Stripe's CEO Patrick Collison, and a young man named Zach Abrams.

Abrams had significant credentials. He and his partner Sean Yu were serial entrepreneurs who sold their first company, Evenly (a P2P transfer app, similar to the American Venmo) to Square (now called Block) in 2013.

Later, Abrams became the head of consumer products at Coinbase and also served as Chief Product Officer at Brex; Yu worked as an engineer at DoorDash and Airbnb. In 2022, the duo teamed up again to found Bridge, helping businesses integrate stablecoin payments. Clients included Coinbase and SpaceX.

The roundtable discussion was originally broad, but Abrams later recalled being shocked: over 90% of the time was spent talking about stablecoins, even though he represented the only stablecoin company present.

Before that, Bridge had been pursuing Stripe as a client, hoping to integrate its technology into Stripe's payment system. But after that roundtable, the direction changed. Collison started frequently meeting with Abrams, not to discuss cooperation, but acquisition.

In October 2024, Stripe announced the acquisition of Bridge for $1.1 billion. Bridge had just raised a $40 million Series A (its first institutional round) in March 2024, valuing the company at $200 million.

The acquisition price was 5.5 times the valuation, potentially over 100 times revenue multiples. In a post-investment note, Sequoia Capital said they believed Bridge would join the ranks of Instagram, YouTube, PayPal, and WhatsApp as "one of those companies that realized its full potential after being acquired."

In February 2025, the deal officially closed. Bridge's 60-person team moved into Stripe's San Francisco headquarters and participated in Stripe's bi-weekly new employee boot camp.

This was just the first step.

What happened next occurred rapidly. In May 2025, Stripe launched stablecoin financial accounts, allowing businesses in 101 countries to directly hold stablecoin balances and send/receive payments globally using stablecoins.

In the same month, ChatGPT launched a shopping recommendation feature, allowing users to search for products, compare options, and then jump to the merchant's website to place orders.

In June, it acquired the wallet company Privy.

Privy did something simple: allow any app to have a built-in digital wallet, enabling users to complete on-chain payments without downloading additional cryptocurrency wallet software. Over 75 million accounts were already using it.

Patrick Collison tweeted a straightforward statement: "Money has to reside somewhere, and Privy builds the world's best programmable vaults."

In September, it jointly incubated the Tempo chain with crypto investment giant Paradigm, a brand new blockchain specifically designed for payments. Paradigm's co-founder Matt Huang (also a Stripe board member) personally led the team.

The list of companies joining the Tempo design camp read like an all-star game of the payment industry: OpenAI, Anthropic, Deutsche Bank, Visa, Shopify, Standard Chartered Bank, Brazil's largest digital bank Nubank, DoorDash, Revolut, South Korean e-commerce giant Coupang.

Stripe CEO Patrick Collison stated that Tempo could process tens of thousands of transactions per second, with sub-second confirmation, fees of less than 0.1 cents per transaction, and transaction fees denominated in USD stablecoins, eliminating the need to hold highly volatile native tokens.

In the same month, Stripe and OpenAI officially released the ACP protocol, simultaneously launching ChatGPT's Instant Checkout feature—users could see recommended products in the dialog box and directly place orders and pay with one click, without redirecting or swiping cards.

The first to support it were Etsy merchants, followed by Shopify's millions of merchants.

In October, Tempo completed a $500 million first round of financing, led by Greenoaks and Thrive Capital, with participation from Sequoia, Ribbit Capital, and SV Angel, valuing it at $5 billion. A blockchain project less than two months old, valued at $5 billion. Stripe and Paradigm themselves did not participate in this round.

In December, Tempo opened for public testing. UBS Group AG, Mastercard, and European buy-now-pay-later giant Klarna joined the partner list.

Bridge's Zach Abrams simultaneously announced that Bridge had applied for a national bank trust charter in the U.S. to comply with the requirements of the stablecoin regulatory act signed into effect in July 2025, the GENIUS Act.

String these events together: $1.1B for coin issuance capability, creating stablecoin financial accounts, acquiring a wallet company, incubating a dedicated blockchain, applying for a banking license.

From issuing coins to building chains to making wallets to setting protocols to obtaining licenses, Stripe did every layer itself.

In contrast, Google: over 60 alliance members, one open protocol, one code repository. Google has everything, except its own chain, its own stablecoin, its own wallet.

An alliance is the product of people sitting down for meetings. What Stripe built is a system that can be launched by one person's decision.

The month Google released AP2, Tempo was already in testing.

Whoever Wins, Circle Wins

There is one player in this war smarter than Stripe.

It doesn't pick sides, doesn't fight, and barely speaks. But no matter who wins, it wins steadily.

This player is called Circle.

Circle issues a stablecoin called USDC, currently the most compliant digital dollar globally.

Another company, Tether, issues USDT which has a larger scale, but regulators have argued for years over whether its reserves are sufficient and its reliability audited. Retail investors might not care, but in the AI world, where there might be hundreds of thousands of automatic transactions daily, each one needs to be auditable. No serious company would dare build its AI transactions on a stablecoin with questionable compliance.

Circle? A company listed on the NYSE. The U.S. SEC has seen its books, it discloses quarterly financial reports, and the whole world can see how much of its reserves are U.S. Treasuries and how much is cash.

So you see an interesting situation: Stripe's stablecoin financial accounts support USDC. OpenAI uses USDC through Stripe. Coinbase in Google's camp also connects to USDC.

The two camps are fighting bloody battles over the "entrance"—who controls the interface and protocol for AI spending. But no matter who controls the entrance, the money ultimately needs to be converted into stablecoins to run on the chain. And in the compliant stablecoin market, USDC has almost no rivals.

The two camps fight over the entrance; Circle gets the settlement volume.

Look at some data. In 2024, the global stablecoin transfer volume reached $15.6 trillion. To put that number in perspective: it's roughly equivalent to Visa's annual transaction volume.

A thing born less than a decade ago has already caught up with the network Visa built over sixty years.

And AI transactions are just beginning. Consulting firm Edgar Dunn & Co. predicts that by 2030, AI-driven transactions will reach $1.7 trillion. Every single one of these $1.7 trillion transactions will most likely go through the stablecoin pipe.

U.S. Treasury Secretary Scott Bessent said publicly during a Senate hearing in June 2025 that a stablecoin market capitalization reaching $2 trillion was a "very reasonable expectation".

Patrick Collison himself said: The average interest rate on U.S. bank deposits is only 0.40%, and $4 trillion in bank deposits even earn zero interest.

He believes this consumer-unfriendly approach is a "loser strategy," and young people will eventually move their money to higher-yielding stablecoins.

He was talking about the trend. And Circle happens to be standing right in the middle of that trend.

Epilogue

Finally, let's zoom out the lens.

On the surface, this battle over AI payment standards is about two commercial camps fighting for territory. But what it reflects is a deeper question: when AI starts participating in economic activities independently, is the financial system we designed for humans still sufficient?

Patrick Collison sees one future, where AI Agents are the main participants in economic activity. They compare prices, procure, pay, settle—the entire process doesn't require a human to press any button. This is the ultimate efficiency, but also the boundary of risk.

The alliance of Google and traditional finance sees another future: AI should be grafted onto the existing human financial infrastructure, constrained by existing human regulatory rules, and operate within the existing human trust framework.

Two futures, two logics, two camps.

But no matter which future arrives, one thing is certain: AI needs to spend money, money needs to run on the chain, and on-chain settlement requires stablecoins.

So Circle keeps winning. Stripe and Google keep fighting. Regulators keep chasing. Merchants keep integrating. Consumers continue not knowing which pipe their money actually flowed through.

Until one day, something goes wrong with what the AI bought for you, and you find that no one, not even the AI, knows who to ask for a refund.

On that day, everyone will suddenly remember the questions no one answered today.

But by that day, the pipes will already be built, and the tolls will already be collected.

History is always like this: get on the bus first, then buy the ticket.

Only this time, the bus is moving too fast.