Editor's Note: The AI boom is entering a phase of financial scrutiny, moving beyond the technical narrative.

Over the past year, market discussions on AI have focused more on model capabilities, compute shortages, and application prospects. However, this article reminds us that what truly needs to be calculated is the return on capital behind this wave of prosperity. Hyperscale cloud providers like Microsoft, Alphabet, Amazon, Meta, and Oracle are investing hundreds of billions of dollars into AI data centers. Based on current analyst expectations for revenue and capital expenditure, the implied return on investment for most of these companies, except Amazon, is likely negative.

This means the similarity between the AI bubble and the previous internet bubble lies not only in market sentiment but also in the high degree to which capital expenditure is bound to macroeconomic growth and stock price expectations. The author points out that over the past four quarters, 93% of U.S. GDP growth can be explained by tech investment. If cloud providers cut back on data center, chip, and infrastructure spending, not only will companies along the supply chain like Nvidia, TSMC, and ASML be impacted, but the U.S. economy itself could quickly face pressure.

More importantly, if AI companies like OpenAI and Anthropic push for IPOs during a peak in market sentiment, it might not be just a fundraising event but a risk transfer: early capital and existing shareholders could be passing on the uncertainties within the AI narrative to retail investors, pension funds, and other investors willing to keep buying into the growth story.

The core question of this article is not whether AI has a future, but rather who will foot the bill for this expensive infrastructure race once the marketing hype subsides.

The following is the original text:

In December 1996, then Federal Reserve Chairman Alan Greenspan described the boom in technology, media, and telecom stocks as showing signs of 'irrational exuberance.' Nearly 30 years later, we can make the same judgment about today's AI boom.

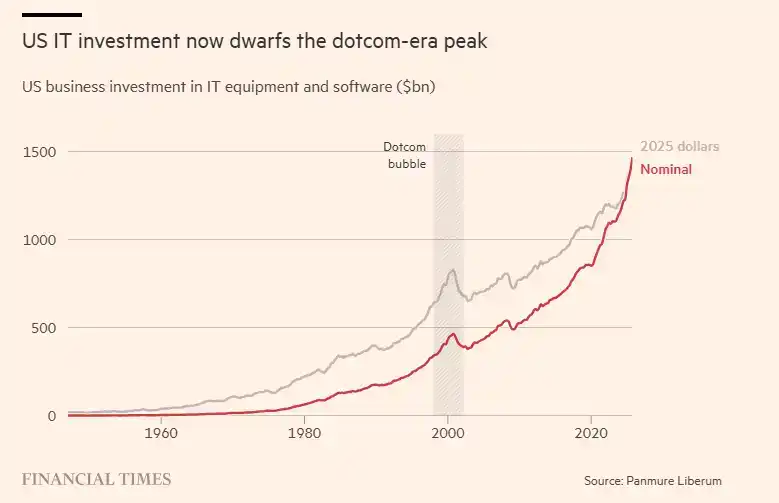

However, while the current tech boom shares similarities with the internet bubble of the previous generation, there is a crucial difference: a certain segment of today's boom has already far surpassed the scale of the TMT bubble. In 2025, U.S. corporate investment in IT equipment and software is nearing $1.5 trillion. At the peak of the TMT bubble, this figure was $466 billion, or just $829 billion after adjusting for inflation.

In fact, the U.S. economy is almost entirely growing on the back of the tech boom. According to my calculations, over the past four quarters, 93% of U.S. GDP growth can be explained by tech investment. Even at the absolute peak of the TMT bubble, this ratio barely reached 60%.

Large language model developers like OpenAI and Anthropic are preparing for high-profile IPOs later this year to capitalize on investors' optimism about their growth prospects. Meanwhile, hyperscale cloud providers like Microsoft, Alphabet, Amazon, Meta, and Oracle plan to invest hundreds of billions of dollars into data centers over the next five years to provide the compute power needed to run these models.

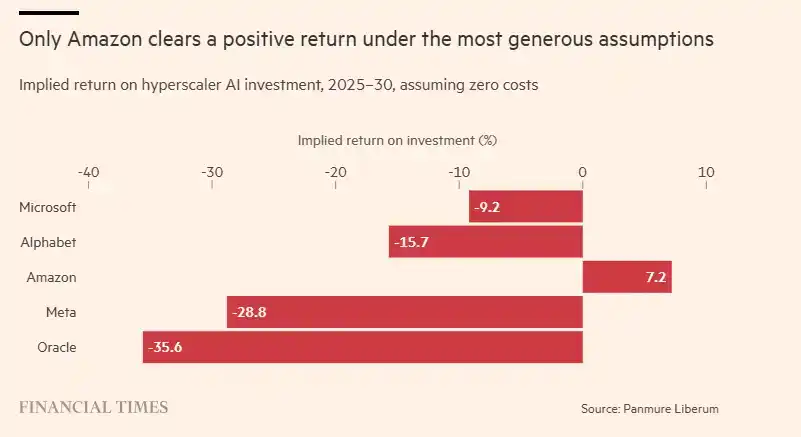

And that's precisely where the problem lies: the math behind the AI boom is starting to look tricky. For these hyperscale cloud providers, I gathered analyst consensus estimates for their capital expenditure and revenue from 2025 to 2030.

Over these five years, their capital investment is projected to grow at an annual rate of 20%, a pace never before seen in this industry. At the same time, revenue is expected to grow by 15% annually. If we make an extremely bold assumption—that these companies have no costs whatsoever—then the incremental revenue could be considered as profit from their new AI data center investments. However, even under this extremely optimistic assumption, my calculations show a highly negative implied return on investment for all companies except Amazon.

These numbers suggest that if hyperscale cloud providers continue on their current trajectory, the AI boom will evolve into one of the largest shareholder value destruction events in history. But they still have two ways out.

The first way out is that the rise of AI brings in far more revenue for these companies than currently expected. But this itself presents a mathematical challenge. Assuming these hyperscale cloud providers want to achieve a 10% return on investment, they would need to find an additional $2 trillion to $5 trillion in revenue annually. For a group of companies currently generating a total annual revenue of only $1.5 trillion, this is an almost impossible task.

The second way out is that the investments originally planned for data centers, chips, and other areas ultimately don't materialize. The reason could be that equity investors become more cautious about the industry, or debt financing for data centers becomes more difficult.

So, what happens if these companies announce cuts to their investment plans?

The stock prices of major companies across continents, from Nvidia to ASML, Samsung, and TSMC, are built on these investment plans and the demand expectations they create.

Let's not forget that current U.S. GDP growth is essentially entirely driven by rising tech spending. If this spending begins to decline, the U.S. economy will quickly fall into a recession. Even a modest decline in tech investment, say 4% to 6%, would have this effect. Historically, similar magnitudes of investment pullbacks occurred following the smaller-scale tech boom of the 1960s and during the 2009 recession.

Such a moderate correction in investment spending would still very likely push U.S., UK, and European stock markets into a new bear market. A repeat of the early 2000s tech stock crash is a real risk; back then, the market fell by 50% or more within the first year.

The next question is: when might we see these hyperscale cloud providers announce plans to cut investments?

I believe this scenario is unlikely to happen in 2026. Companies like OpenAI and Anthropic will still strive to maintain market hype, at least until their respective IPOs are completed, which may continue to support the boom in the short term. But what about after that? The 'impossible math' facing hyperscale cloud providers won't change, and marketing hype may eventually fade. In the end, reality will arrive.

Maybe not in 2026, but possibly in 2027 or 2028. After all, Greenspan spoke of 'irrational exuberance' in December 1996, and the bubble didn't truly burst until three years later in 2000.

From this perspective, the IPOs of these AI companies are likely just a massive transfer of investment risk: risk is being transferred from current owners to retail investors, pension funds, and other investors willing to pay for the narrative.