Original Title: AI Bubble Is Already Bursting

Original Author: Chengbei Xugong, Gelong

In recent days, the market has experienced severe volatility, with "AI bubble theories" swirling.

Ray Dalio, founder of Bridgewater Associates, said: There is a bubble in the AI market, and the level is "relatively high."

NVIDIA CEO Jensen Huang said: AI presents a massive opportunity, and the demand for computing power has just begun to explode.

Who to believe?

Both of them are correct.

Is there a bubble in the AI industry? Inevitably, yes.

However, bubbles in the technology field are often the only way society can pay homage to a disruptive advanced productive force.

It is not a purely derogatory term.

In the long run, this is an inevitable phenomenon at the beginning of the emergence of advanced productive forces.

Many people compare the current situation to the 2000 internet bubble, feeling deeply concerned.

The dot-com bubble did cause the Nasdaq to plunge nearly 78%, evaporating over $5 trillion in wealth.

But twenty years later, which industry can operate without the internet?

Today, the value of the internet industry far exceeds that of the bubble era.

The AI bubble, at least on the surface, appears to be a similar situation.

The bubble existing in the capital markets cannot stop virtually every industry in society from actively being empowered by AI.

AI+ is an unstoppable trend.

Just as all industries today are inseparable from the internet, all industries in the future will be inseparable from AI.

01

In that era where any company with a '.com' in its name could go public and raise money, the Nasdaq soared nearly 600% between 1995 and 2000. Subsequently, a financial storm lasting two and a half years ensued.

Those prominent names back then, like software company MicroStrategy, plummeted 62% in a single day due to accounting scandals and overblown promises; Pets.com (selling pet food online) and Webvan (the pioneer of fresh grocery e-commerce) went bankrupt outright.

......

Amid the panic, almost everyone condemned the internet as a scam.

However, the physical infrastructure left behind by the reckless spending of speculative capital often nurtures the next era's supergiants at extremely low costs.

The bubble burst not because of the internet technology itself, but because the pace of physical infrastructure construction couldn't keep up with the market's rhythm.

For example, the once-dominant telecommunications companies (like WorldCom, Global Crossing) invested heavily in laying global submarine cables and dense wave division multiplexing networks. While they went bankrupt, these cheap "information superhighways" became the perfect breeding ground for the later rise of Netflix, Zoom, and mobile internet.

Without the frenzied, ahead-of-its-time global investment in telecom infrastructure around 2000, there would have been no later explosion of YouTube's video streaming or the development of cloud computing infrastructure.

Amazon is the most typical example.

Its stock price plunged from a high of $107 in 1999 to $7 in 2001, a drop of over 90%.

But it survived because its underlying business logic, "reconstructing retail through the network," aligned with the direction of advanced productive forces.

This is a classic case of Amara's Law: overestimating the short-term impact of a new technology while severely underestimating its long-term impact.

In the early stages of a technological revolution, the frenzy of speculative capital inevitably leads to overinvestment, forming a bubble.

This is the intelligence tax that innovation must pay.

But when the bubble subsides, what remains will be a more indestructible advanced productive force.

02

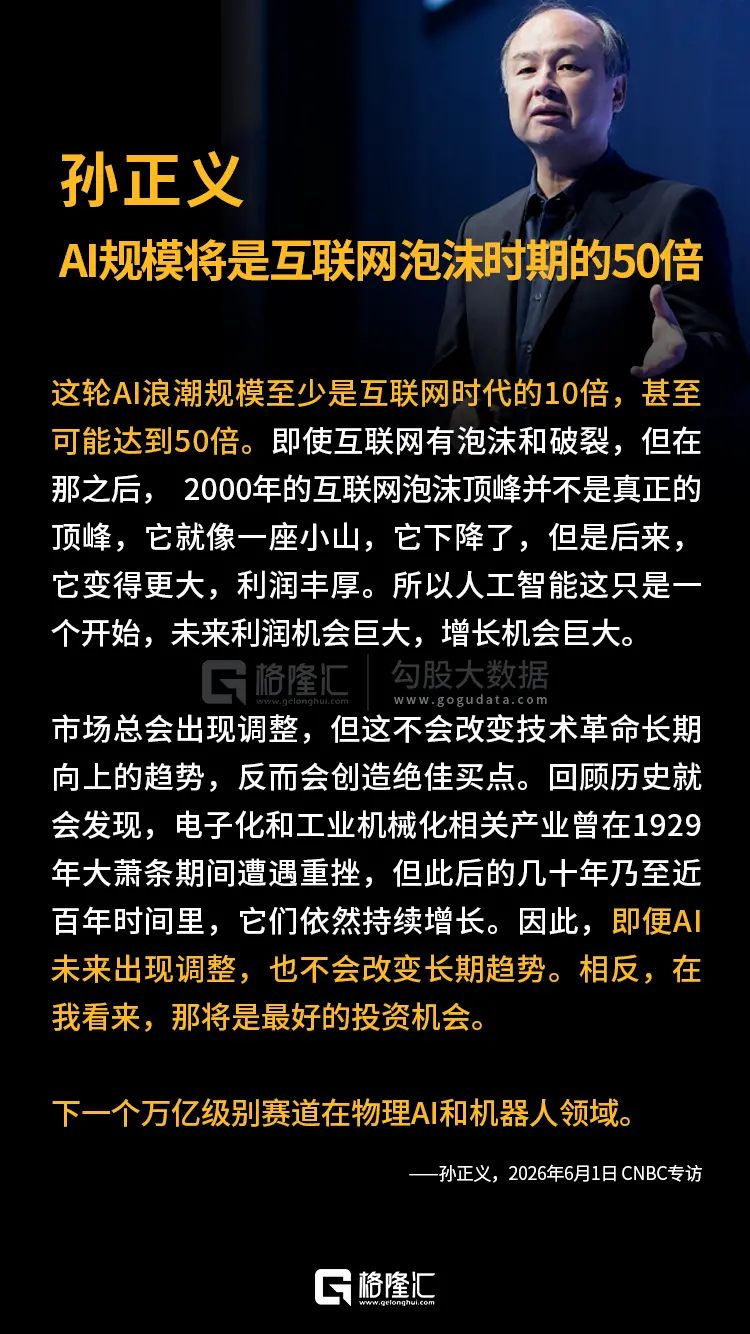

Returning to 2026, the bubble in the AI industry appears even larger.

Just the five major cloud service providers—Amazon, Google, Meta, Microsoft, and Oracle—are expected to have capital expenditures of $690 billion in 2026, with total AI infrastructure investment projected to reach $5.3 trillion by 2030.

Of this, only about 25% is spent on GPUs; the remaining 75% is invested entirely in physical infrastructure: liquid cooling systems, power transmission, network switches, optical modules, and land.

On the revenue side, the combined total revenue of all leading pure-play AI vendors like OpenAI, Anthropic, Cohere, Mistral, and Perplexity in 2026 is expected not to exceed $40 billion.

Nearly $700 billion poured into the foundational layer, only hundreds of billions returned from the application layer.

This severe asymmetry—what is it if not a bubble?

One cannot simply jump to such a conclusion.

There is a crucial point that cannot be overlooked.

In March 2023, when OpenAI released GPT-4, the blended cost per million input tokens was about $30.

By April 2025, thanks to model architecture optimization and inference computing improvements, the price for models with equivalent intelligence levels plummeted to $0.1-$0.15 per million tokens.

According to Stanford's "AI Index Report" and TokenCost data: AI inference costs have dropped over 99.7% in the past two years.

Following traditional linear thinking, with costs plummeting, corporate AI spending should decrease, right?

But the reality is, enterprise AI cloud spending tripled between 2024 and 2025.

Why?

Because when the marginal cost of "intelligence" approaches zero, AI is no longer just a simple text summarizer or chatbot; it has entered a new era of agents and multimodal augmented retrieval.

Companies are starting to let AI agents automatically run tasks thousands of times—writing code, scanning millions of legal contracts, simulating biological experiments.

Cheap tokens have unlocked a massive amount of long-tail demand previously uncommercializable due to cost constraints.

This point can also be gleaned by comparing NVIDIA in 2026 and Cisco, the network hardware kingpin of 2000.

Their ecological niches are strikingly similar, but their underlying financial health is worlds apart.

This precisely validates the economic principle known as the "Jevons Paradox": technological progress improves energy efficiency, but instead of reducing energy consumption, it leads to greater demand due to cost reduction.

Even after experiencing the so-called "DeepSeek moment" early last year, the market quickly sobered up in the following months: the more optimized the algorithms, the lower the barrier for enterprise AI adoption, ultimately leading to an exponential increase in total computing power consumption.

It is precisely because of this that AI can gradually embed itself into virtually every traditional industry.

Just as all industries embraced internet+ over the past two decades.

From SaaS software to biopharmaceuticals, and then to advanced manufacturing robotics driven by embodied intelligence, in 2026, almost every industry is embracing AI+.

No one discusses "should we use AI," but rather anxiously questions "is our data properly cleaned? Do we have enough API call quota? Is our RAG architecture optimal?"

Currently, the AI industry does indeed have a bubble.

But for enterprises, if you don't embrace the bubble, you will be crushed by the times.

This has been proven over the past two decades of the internet era.

03

Currently, we are undoubtedly at an extremely critical node in the technology lifecycle: just before the "Trough of Disillusionment" on Gartner's Hype Cycle, or at a turning point in the theory of "Technological Revolutions and Financial Capital."

The AI bubble is already bursting, it's just that many haven't realized it.

Over the past few years, a large number of venture capital firms suffered from fear of missing out (FOMO).

Any new startup, with just a few dozen PPT slides, wrapping a layer of OpenAI's API, could raise money. Now, as the tide recedes, these companies with no moat, only concepts, are dying en masse.

This is the market self-cleansing, a manifestation of the bubble bursting.

But this is only the surface phenomenon.

Three profound evolutions are taking place in the market's underlying logic:

First, the shift of value from CapEx to OpEx

Currently, the money is being made by the shovel sellers—NVIDIA, TSMC, and those selling optical modules and server liquid cooling equipment have captured most of the gains.

But as computing power gradually becomes "infrastructural," like water and electricity, the real excess profits will gradually shift to the application layer.

Namely, those AI-native enterprises that can use extremely low-cost tokens to genuinely solve pain points in vertical industries and reshape business processes (OpEx optimization).

Second, valuation multiple compression and earnings digestion

The market's high valuation for AI infrastructure does not necessarily mean a crash.

In many cases, the high-speed growth of corporate earnings will gradually digest lofty valuations through a "time-for-space" approach.

As long as the revenue growth of cloud computing giants keeps pace with the depreciation rate of capital expenditures, this game of pass-the-parcel can evolve into an unprecedented industrial upgrade.

For example, global automotive manufacturing giants and chip giants, by introducing end-to-end AI twin technology, have shortened the R&D-to-mass-production cycle for new products by 35% and improved overall equipment effectiveness (OEE) by 18%.

Another example: in the financial industry, by 2026, quantitative trading, risk control, and credit assessment are fully dominated by multimodal agents. AI is not only processing macro expectations with microsecond timestamps but also deeply involved in micro-level asset pricing for each transaction.

In highly knowledge-intensive industries like law, healthcare, and auditing, AI has completed its evolution from "junior assistant" to "partner-level expert."

Among the over 1 billion active users of ChatGPT, Gemini, Claude, a significant portion uses it as a substitute tool for daily high-intensity intellectual labor.

Including you and me.

All of the above are tangible developments, visible to everyone.

04

Looking back at the grand history of technology, Schumpeter's "creative destruction" is always unfolding.

Capital markets are always impatient, hoping that $1 invested today will return $10 tomorrow.

When nearly $700 billion in infrastructure investment cannot be fully transformed into application-layer profits in the short term, the market is bound to experience a brutal reshuffle.

Eliminating those speculative, shell companies that rely solely on PPT presentations, and retaining those with real technological depth and viable application scenarios.

After the reshuffle, those cheap and massive computing centers, highly optimized model algorithms, will serve thousands of industries at extremely low cost.

After 2000, humanity entered a digital age where no industry could function without the internet.

Today, we are also irreversibly heading towards a fully intelligent era where all industries are governed and empowered by AI.

Amidst the noise of the bubble, the underlying momentum of productive force contains not a drop of water.