Author: Xiao Jing, Tencent Technology

Editor: Xu Qingyang

Two events happened simultaneously on the evening of May 26th.

Xiaomi released its Q1 2026 financial report. Total revenue was 99.1 billion yuan, down 10.9% year-on-year; adjusted net profit was 6.07 billion yuan, plummeting 43.1% year-on-year. Smartphone business revenue was 44.3 billion yuan, down 12.5% year-on-year, with gross margin dropping to 10.1%, a decrease of 2.3 percentage points compared to the same period last year.

During the earnings call, Xiaomi Group President Lu Weibing mentioned a number: the price of memory of the same specification has surged nearly 4 times compared to the same period last year. For a phone with 12GB LPDDR5 + 512GB UFS configuration, the memory cost alone increased by about 1,500 yuan. He said Xiaomi "will not pass on the memory price increase to consumers," but also predicted the price hike cycle would continue into 2027 or even 2028. To survive, Xiaomi proactively cut entry-level models, with quarterly shipments dropping to 33.8 million units.

The second event: Micron Technology surged over 19% in a single day, with its market cap breaking the $1 trillion mark. UBS raised Micron's target price from $535 directly to $1,625, an increase of about 204%, making it the highest target price among the 46 brokerages covering Micron.

A few days earlier, Citigroup had just raised Micron's target price from $425 to $840, and HSBC raised it from $750 to $1,100. Wall Street hasn't been this unanimous on a single cyclical stock in a long time. Twelve months ago, Micron's stock price was under $110. It has increased eightfold in a year.

On the same day, memory sellers enjoyed a trillion-dollar frenzy, while memory buyers saw their profits halved.

Goldman Sachs played a thought-provoking role in this frenzy. In December 2025, Goldman gave Micron a Neutral rating with a $205 target price. In Q1 2026, Goldman reduced its Micron position by nearly 20%.

On March 19th, the day Micron reported earnings, Goldman adjusted its target price from $360 to $400 but maintained Neutral, even though the stock price had already far exceeded $400. Micron then surged 40% in a week, and Goldman perfectly missed the rally.

On May 17th, Goldman issued a storage industry report, concluding it was the "most severe supply shortage in 15 years" and upgraded the overall sector rating. But for Micron, it remained Neutral with a target price of $400. As the outlier, Goldman is either the last sober person in this frenzy, or the one who missed out most severely.

But such a strong divergence is worth serious consideration.

01 Why the Crazy Surge? A New Story Called LTA?

The core argument of UBS analyst Timothy Arcuri's May 26th report is that Long-Term Agreements (LTAs) are fundamentally eliminating the cyclicality of the memory industry.

Memory chips are the segment of the semiconductor industry most akin to commodities. DRAM and NAND prices have followed a brutal pattern for four decades: two years up, two years down, with price collapses never absent. Profits of Micron, Samsung, and SK Hynix fluctuate like an EKG, and the market has never dared to value these companies based on "steady-state earnings." For forty years, the valuation fluctuation range for cyclical stocks has roughly been 8 to 15 times PE.

Chart: EKG-like Fluctuations in Micron's Financial Data

UBS's story is that these companies' "cycle curse" will be broken, and the protagonist behind it is "AI."

Cloud vendors like Microsoft, Google, Amazon, and Meta, to lock in HBM and DDR5 supply in the AI arms race, have started actively signing 3-to-5-year fixed-price long-term contracts with memory manufacturers, including prepayments. These contracts are not the traditional "intention-based" agreements in the semiconductor industry; they are binding purchase commitments, locking in volume, price, and even wafer capacity.

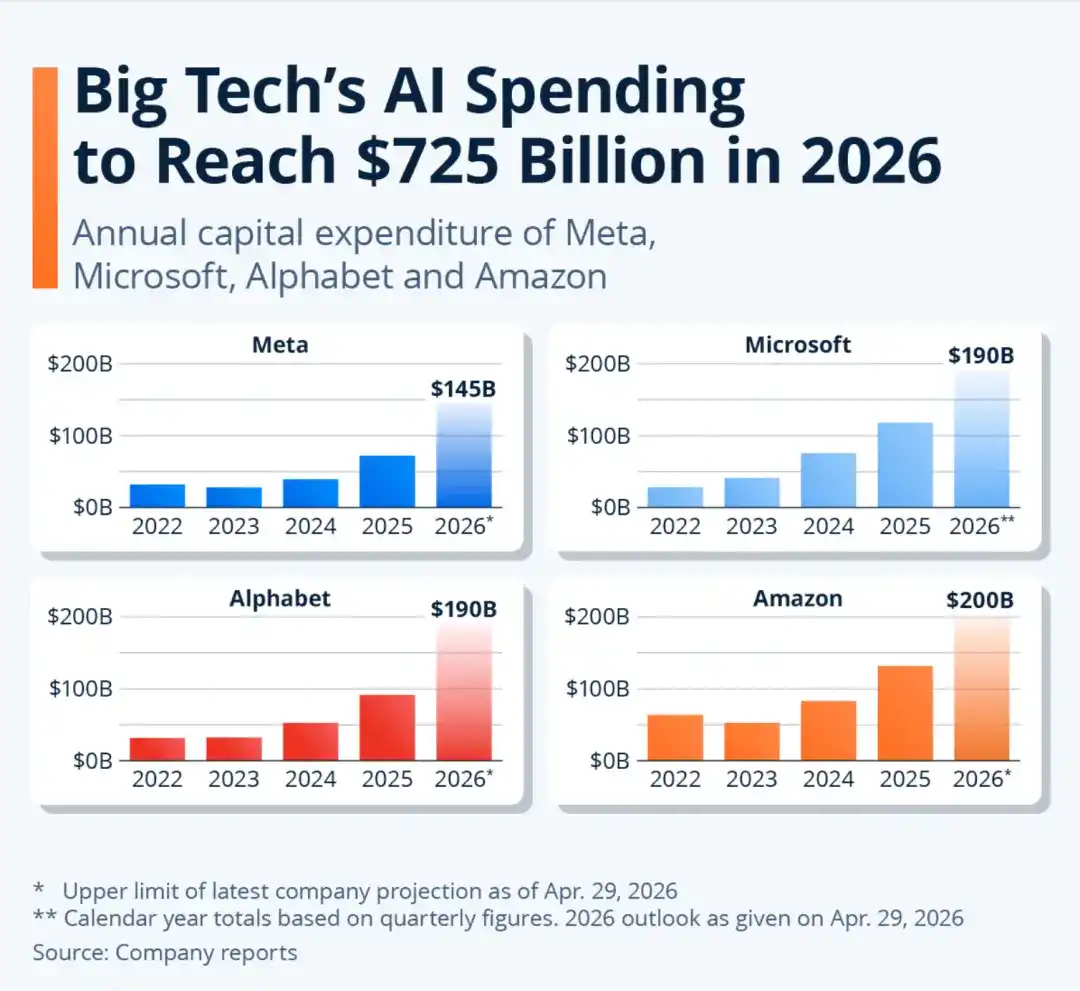

Chart: Major Tech Companies' AI Capital Expenditure (2022—2026E): Combined total for four companies expected to reach $725 billion in 2026. Individually, Amazon $200B, Microsoft $190B, Alphabet $190B, Meta $145B. 2026 data is the latest guidance upper limit from each company as of April 29, Microsoft's figure is a calendar year sum based on quarterly data.

In April, Microsoft and Google were reported to be in talks with SK Hynix for three-year DRAM contracts, with structures including prepaid deposits. Previously, manufacturers begged customers for orders; now, customers pay deposits to lock capacity. The power dynamic in the supply chain has reversed.

UBS's model calculations show that after incorporating LTAs into Micron's earnings forecast, even if DRAM spot prices crash 50% in FY2029, Micron's annual EPS can still maintain over $100. LTAs can narrow the DDR price fluctuation amplitude from peak to trough by about 50%. By 2027, 20% to 30% of the industry's total DDR bit shipments will be locked in fixed-price LTAs. For hyperscalers' DDR5 procurement, 60% to 70% may already be under fixed contracts.

From a valuation perspective, if cyclicality disappears, memory stocks should not be valued as cyclical stocks, but as infrastructure utilities, jumping from 8-15x PE to 20-30x PE.

J.P. Morgan also issued a report with similar conclusions in mid-May, titled "LTAs are Eliminating the Memory Industry's Cyclicality." Citigroup's logic is that HBM production crowds out wafer capacity for ordinary DRAM, leading to long-term shortages in general memory.

Micron's stock surge welcomes the Davis Double Click of profit growth and valuation system switching.

02 This Memory is Not That Memory

Wall Street uses the "Memory Super Cycle" to tell a unified bullish narrative. But "memory" and "memory" are completely different.

The 2026 memory market shows a three-tier divergence.

The first tier is AI memory: HBM, server DDR5, enterprise SSD. Here, price hikes, shortages, and LTAs locking capacity occur simultaneously. TrendForce expects Q2 2026 DRAM contract prices to rise 58% to 63% QoQ, NAND Flash contract prices to rise 70% to 75% QoQ; Kioxia has also publicly stated that its 2026 capacity is basically sold out. This tier is the story behind Micron's trillion-dollar market cap.

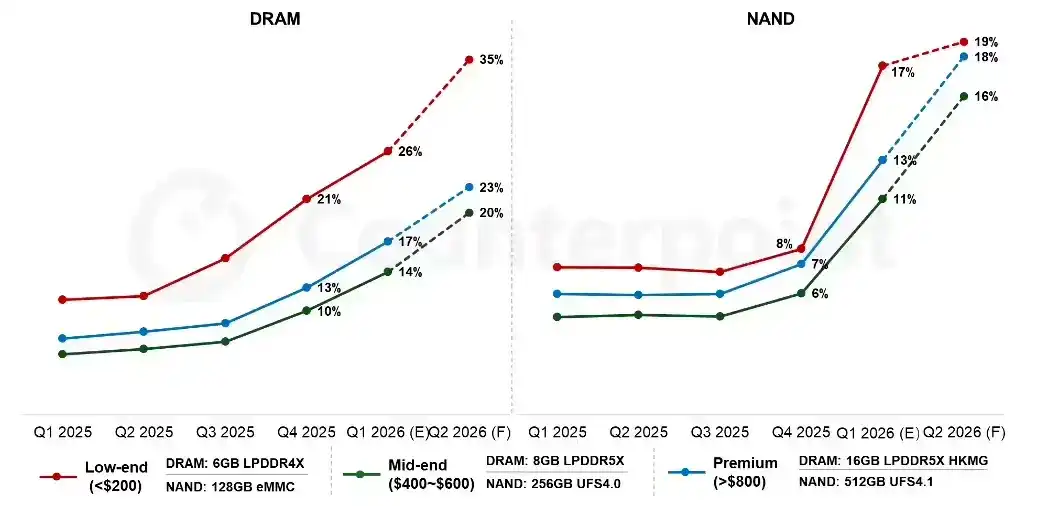

The second tier is mobile and embedded memory: mobile DRAM and mobile NAND. Prices here are also rising sharply. Counterpoint data shows DRAM prices rose over 50% QoQ in Q1 2026, NAND Flash prices rose over 90% QoQ. TrendForce reports show memory typically accounted for about 10% to 15% of a phone's BOM, now it has risen to 30% to 40%, with low-end models under more pressure.

Left chart DRAM (Memory) Trend: Low-end phones rise most sharply, climbing from initial lows to a forecast of 35% in Q2 2026; high-end to 23%; mid-range to 20%. Dotted portion (after Q1 2026) are forecasts.

Right chart NAND (Flash) Trend: All price segments remained relatively flat through Q3 2025, but began rising sharply from Q4 2025.

Xiaomi sits in this tier. Its pain is "AI has taken away capacity, leaving less for phones, and phone makers must pay higher prices for the remaining capacity."

Manufacturers give capacity priority to AI customers, leaving phone makers with few options for contract procurement. To ship, you have to buy at the new contract price; if you don't, production lines and new product schedules will be affected.

The third tier is PC retail spot: DDR5 modules, consumer SSD. Here, a counter-directional fluctuation occurred. TrendForce reports show that by late March in China, channel 32GB DDR5 modules dropped 500 to 1050 yuan from near 3000 RMB, with some clearance prices as low as 1950 yuan; Tom’s Hardware also wrote that some DDR5 products in Chinese and overseas retail markets retreated 25% to 30% from highs.

But this is mainly a split between retail spot and contract procurement. The PC channel has inventory to sell off; phone makers procure via contracts, with no sell-off option.

Within the same "memory" industry, three tiers, three directions. The essence of this divergence is that the three memory giants are shifting wafer capacity from consumer-grade to AI. HBM production crowds out ordinary DRAM wafers, enterprise SSDs crowd out consumer NAND supply, leaving less capacity for phones and PCs. Phone makers, forced to ship, are compelled to accept price hikes; the PC channel, with ample inventory, can slash prices for clearance.

Image generated with AI assistance

Micron & Co. have actively chosen to allocate capacity to AI customers willing to pay more. In the short term, this is a nice product mix upgrade. But it also means Micron is sealing off its retreat path; if AI demand slows, capacity may not switch back smoothly.

Micron's earnings report shows QoQ, DRAM bit shipments only grew mid-single digits, NAND bit shipments only grew low-single digits; growth mainly came from ASP increases. Micron's story today is only about "extreme shortages in this AI memory branch."

Micron is betting everything on this branch.

03 Can LTAs Really Eliminate the Cycle?

The LTA logic seems solid. Under the AI spending pace, the supply elasticity of memory chips is extremely low. HBM capacity takes 18 to 24 months from planning to production, and producing HBM crowds out general DRAM wafer capacity. Cloud vendors sign LTAs because they fear "AI project delays."

But LTAs eliminating cyclicality have a prerequisite: the demand side doesn't collapse.

Different institutions have different statistical calibers for AI CapEx, but the direction is consistent: AI infrastructure investment is moving from the hundreds of billions of dollars level to near a trillion dollars. According to some market models, this is a capital expenditure curve with near 40% to 50% annual growth.

However, nothing in the physical world grows at 40%+ forever. AI bubble bursting isn't needed; a slowdown from 45% to 20% growth could reverse the supply-demand balance for memory chips within 18 months. The three memory makers are all expanding capacity frantically; Micron's FY2026 CapEx is $25 billion, adding another $10 billion in 2027.

Another thing to face squarely: when a company's revenue growth relies entirely on price elasticity rather than volume elasticity, the story is fragile. Micron's shipment volume only grew 4% to 6%; its 196% revenue growth mainly came from price hikes. Prices can rise but can also fall, and they fall faster than they rise. This is the nature of cyclicality.

Let's do a simple arithmetic problem.

Micron's current market cap is $1 trillion. Micron has raised its FY2026 CapEx to over $25 billion, and expects capital expenditure to increase significantly in FY2027, with some market reports mentioning an incremental increase possibly over $10 billion.

Micron's Q2 FY2026 non-GAAP net profit was about $14 billion, simply annualized to about $56 billion, implying a PE of about 18x. If further price hikes and LTAs are extrapolated, PE could still be calculated at around 15x.

That might seem "cheap." But this PE's denominator is a super-cycle peak profit where DDR4 contract prices rose 10x in 15 months, HBM is sold out for the year, and gross margin jumped from 36% to 75%.

Multiplying a peak-cycle profit by a seemingly "reasonable" multiple to arrive at a seemingly "not expensive" valuation is precisely the classic valuation trap when cyclical stocks peak.

Cisco in 2000 also had a PE of "only" 60-some times, based on 15 consecutive quarters of 50%+ revenue growth. When growth slowed from 50% to 20% to 0%, EPS didn't need to fall much for the stock to drop 80%, because both the multiple and earnings contracted simultaneously.

From Davis Double Click to Double Kill.

History tells us one thing: in commodity markets, LTAs have never been a one-sided "floor." They protect buyers in an up-cycle and sellers in a down-cycle, but the premise is that both sides have the ability and willingness to fulfill them. The moment LTAs are most needed is precisely when they are most likely to fail.

This is not to say Micron is necessarily a bubble. AI's demand for computing and memory may truly be structural, LTAs may truly rewrite industry rules, and a trillion-dollar market cap may just be the starting point.

But when all of Wall Street simultaneously shouts "this time is different," it's at least worth pausing to ask: what happened the last time everyone was this certain?

In a sense, one must enjoy the frenzy of the bubble to make money.

But, it took Cisco about 25 years, until today's AI era, to finally surpass its closing high from the dot-com bubble period, and the internet indeed changed everything.