"We went from eggs to yen"—this financial reminiscence from CME legend Leo Melamed bears witness to a time when eggs were once one of the world's most active futures products.

In the first half of the 20th century, egg futures were among the hottest trading instruments in Chicago. Trading volume in some years was second only to grain varieties, and there were even instances where futures trading far exceeded the volume of physical circulation.

The predecessor of the Chicago Mercantile Exchange (CME), the world's largest derivatives market, was called the "Chicago Butter and Egg Board." This was the foundation of what would later become a derivatives empire, and as the name implies, the exchange initially traded only two things: butter and eggs.

After the 1970s, the U.S. egg-laying industry rapidly industrialized, cold chains matured, and price fluctuations were gradually "smoothed out." As uncertainty began to fade, the noise in the trading pits quieted down. In 1982, egg futures officially exited the Chicago Mercantile Exchange. It didn’t collapse dramatically; rather, it was as if the times quietly turned off the lights.

In 2013, the Dalian Commodity Exchange in mainland China reignited this product. At that time, mainland China's egg-laying industry was still highly fragmented, with sharp price fluctuations, making hedging needs real and urgent.

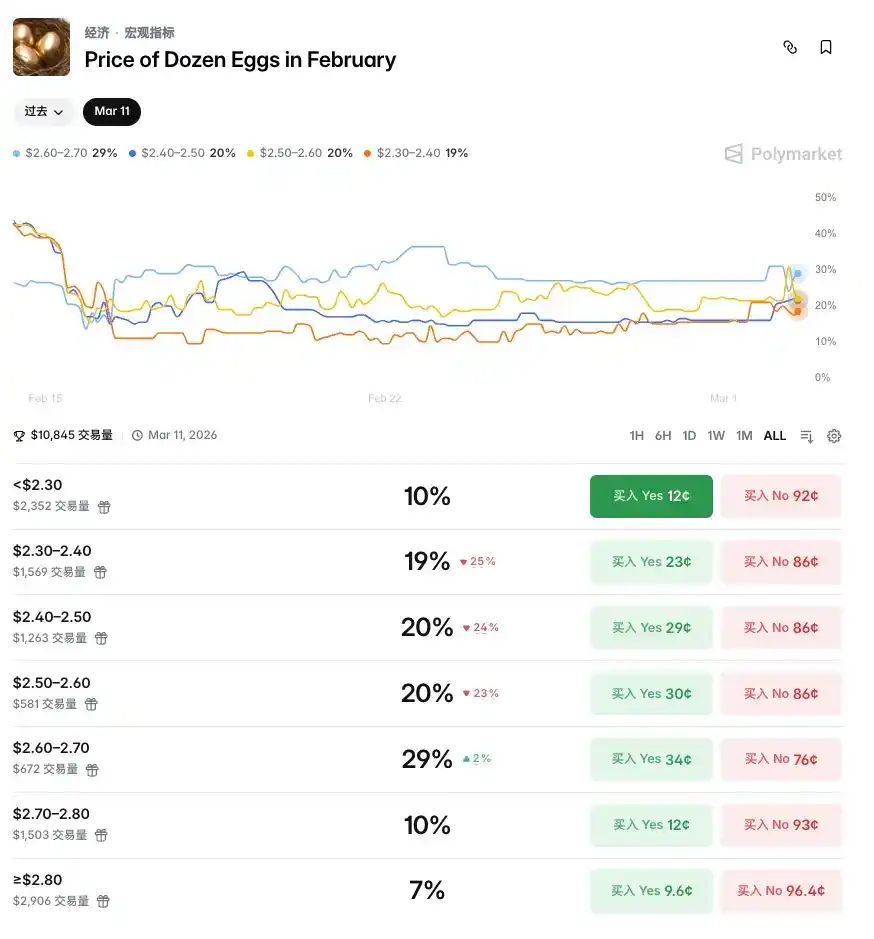

Egg futures trading did not disappear; it merely migrated. And today, this migration has taken another step forward. The venue for trading egg prices has moved to Polymarket.

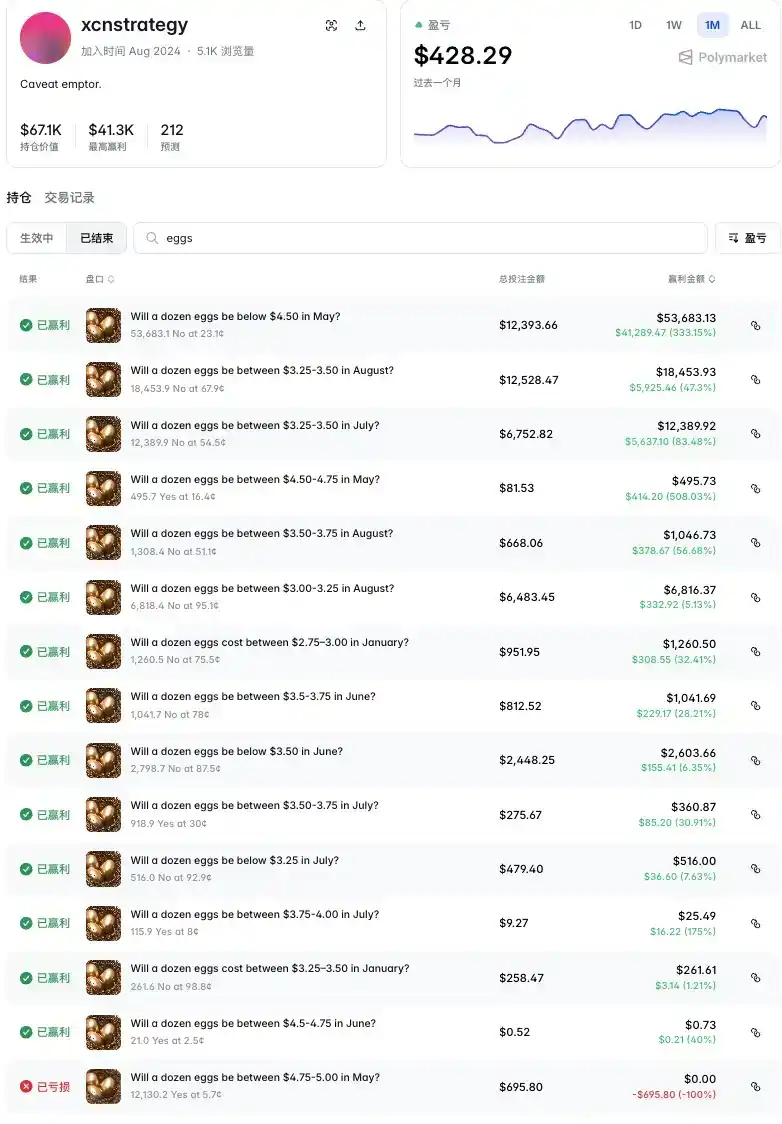

A trader with the ID "xcnstrategy" established positions in multiple expiration months—January, May, June, July, and August—for egg price predictions. The vast majority of these trades were shorting the "Yes" for certain price ranges, meaning betting that eggs would not reach certain price levels. The total betting amount was $44,800, with nearly $100,000 in profits. Out of 15 trades, all but the first were profitable.

The most recent trade was also the most profitable: a $12,393 bet on "No" for "a dozen eggs in May below $4.50," yielding a profit of $41,289 (+333%).

Speculations about xcnstrategy’s true identity, aside from possibly being an "egg enthusiast," include many who believe he is likely someone with a commodities market background or agricultural data research capabilities, analyzing that the U.S. avian flu-induced egg price surge starting in 2025 was a short-term phenomenon and that the market overestimated the probability of sustained high prices. Others think he is an industry insider in the egg supply chain, hedging against the volatility inherent in the industry.

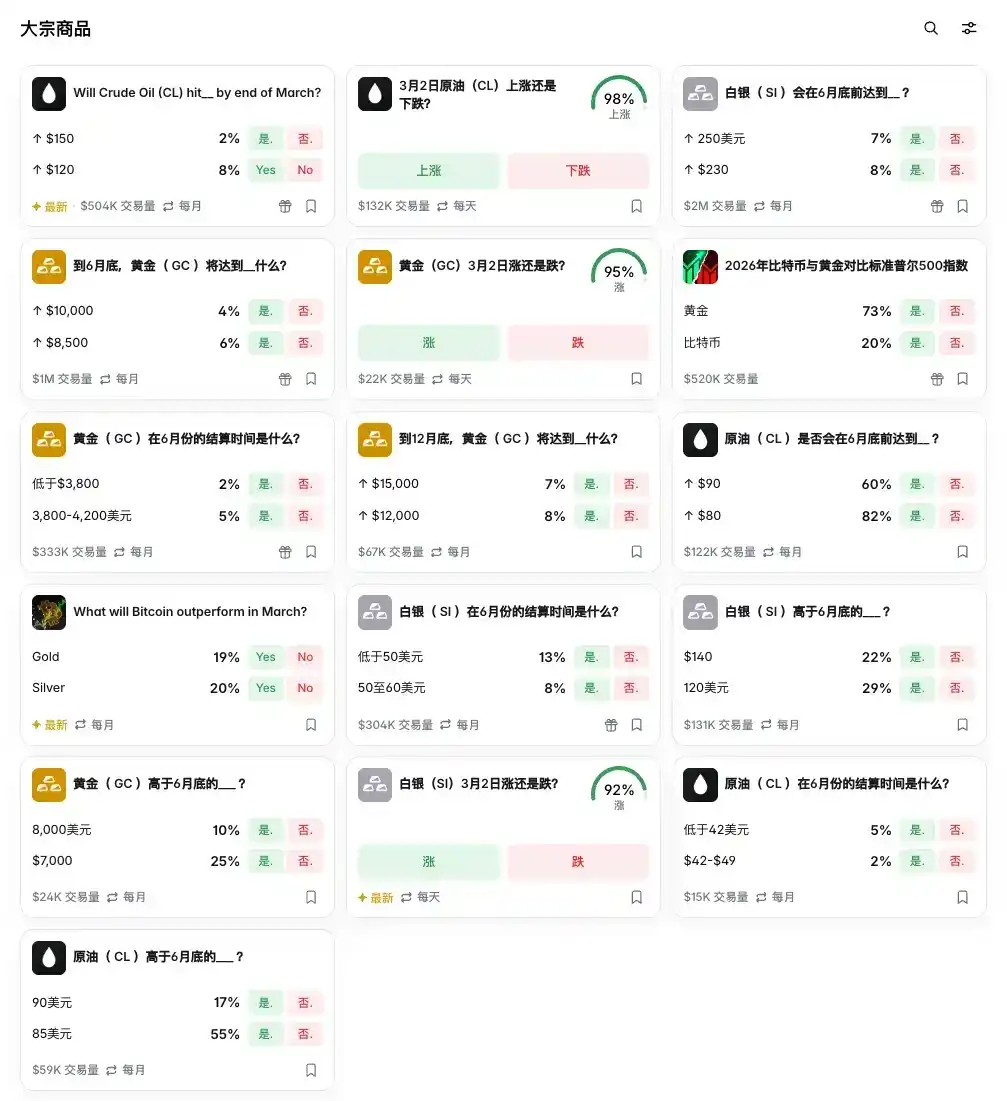

Eggs are just one example. The traditional asset标的 available for trading on Polymarket are far more diverse than one might imagine: from crude oil (CL), gold (GC), silver (SI), and other commodities to various foreign exchange rates and housing data—all can be found as markets on Polymarket.

Operating 24/7 without closing is one of the biggest advantages of trading such markets on Polymarket. This advantage is particularly evident during traditional financial market closures, as seen with the U.S.-Iran conflict escalation last weekend.

In this regard, Hyperliquid shares the same advantage. The perpetual contracts on Hyperliquid, linked to crude oil and gold, have no expiration dates and run continuously, 24/7.

This leads to an increasingly hard-to-ignore phenomenon: the crypto market is quietly taking on the price discovery function of traditional financial markets, especially when the latter are closed.

Traditional futures markets have fixed trading hours; CME's crude oil and gold contracts close on weekends, and foreign exchange markets see liquidity dry up late at night. This means that when geopolitical shocks erupt after Friday's close, participants are left in the dark—unable to hedge, express views, or price assets.

Last weekend's U.S.-Iran conflict escalation is the latest validation. According to Bloomberg, around the time the conflict broke out, a large number of traders flocked to Hyperliquid to trade perpetual contracts linked to crude oil and gold to hedge against the geopolitical shock—while traditional markets were shut, crypto derivatives markets were the only place with the lights on. Investment firm executive Avi Felman had previously predicted that "Hyperliquid will become indispensable for fund managers because it’s 24/7." This judgment was concretely validated during this conflict.

At the same time, gold tokenization is accelerating another logic: when gold exists in the form of on-chain tokens and is continuously priced in decentralized markets, it no longer needs to wait for the London Metal Exchange or CME to open. To some extent, the tokenized gold market is acting as a "shadow pre-market" for traditional gold markets, pricing gold over the weekend and allowing price discovery to occur before traditional markets open.

In 2020, then the world's second-largest trading platform, FTX, launched tokenized stocks, allowing platform users to trade Tesla and NVIDIA shares with stablecoins. The idea was to capture pricing power—when U.S. stocks were closed, FTX's Tesla tokens could fill the market void, allowing users to trade Tesla stock when the company announced new models on Saturday, thereby influencing Nasdaq's Monday opening.

Unfortunately, due to liquidity issues, the pricing effect ultimately did not materialize. Six years later, tokenization has come full circle back to this vision. Today, Polymarket and Hyperliquid are viewed not merely as cryptocurrency trading platforms. Polymarket is already officially recognized as a public opinion polling agency and information exchange hub, while Hyperliquid is seen as a new type of full-asset trading platform.

Price discovery power has always been one of the core powers in financial infrastructure.

Back in the day, Chicago butter and egg merchants established the CME because they needed a venue to discover prices and transfer risks. Over a hundred years later, the same logic is replaying on-chain, only the medium has changed.

You might think the market is trading eggs, but in reality, the market is fighting for pricing power.