Four Years of Transformation: A Deep Dive into the Evolution of Coinbase's Business Model

比推Publicado a 2026-02-20Actualizado a 2026-02-20

Resumen

Coinbase has undergone a significant business transformation from 2021 to 2025, shifting from heavy reliance on retail trading revenue (88% in 2021) to a more diversified model. By 2025, retail trading contributed only 48% of total revenue, while subscription and service revenue grew to 41% of total revenue—driven largely by stablecoin income (19% of total revenue, via the Circle partnership), staking, and Coinbase One subscriptions.

Total revenue in 2025 increased by 9.4% year-over-year but remains 6.4% below the 2021 peak. Transaction revenue fell 40% compared to 2021. The company improved operational efficiency, reducing costs by 45% in 2023 through layoffs and restructuring, resulting in a 21% operating margin in 2025.

Coinbase's balance sheet is strong with $11.3 billion in cash, minimal debt cost (~1% interest), and significant crypto holdings. However, it faces risks including competition, regulation, market cyclicality, interest rate sensitivity, and concentration in its Circle partnership.

Compared to Robinhood, Coinbase trades at a lower valuation multiple despite a stronger balance sheet, presenting a potential opportunity for long-term crypto investors.

Source: DeFi Report

Author: Michael Nadeau

Compiled and Edited by: BitpushNews

Looking back to 2021, retail trading accounted for 88% of Coinbase's total revenue. By last year (2025), as the company diversified into subscriptions, services, and institutional infrastructure, this proportion had dropped to 48%.

This article will analyze Coinbase's ongoing transformation and what it means for the company's profitability, competitive position, and long-term valuation.

Let's begin.

Revenue Overview 2021 – 2025

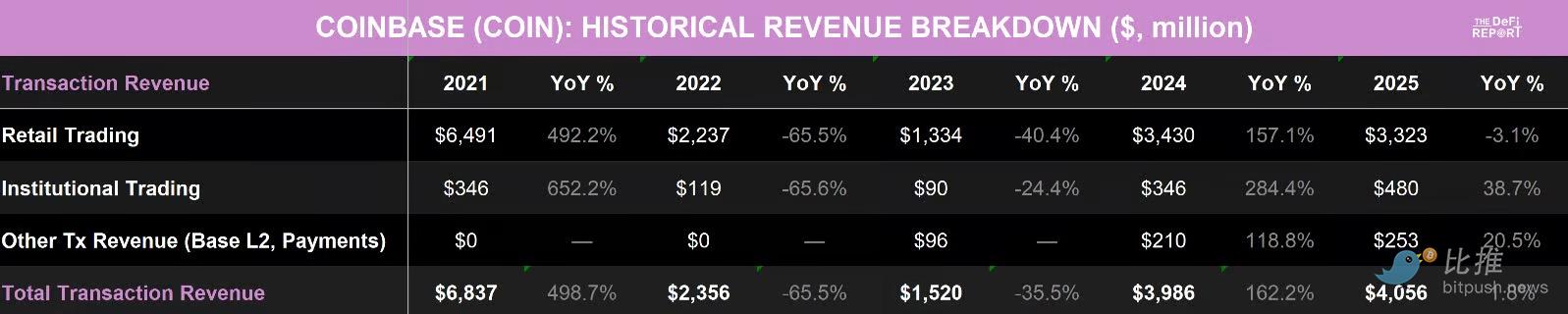

Transaction Revenue

Data Source: Coinbase 10k, SEC filings

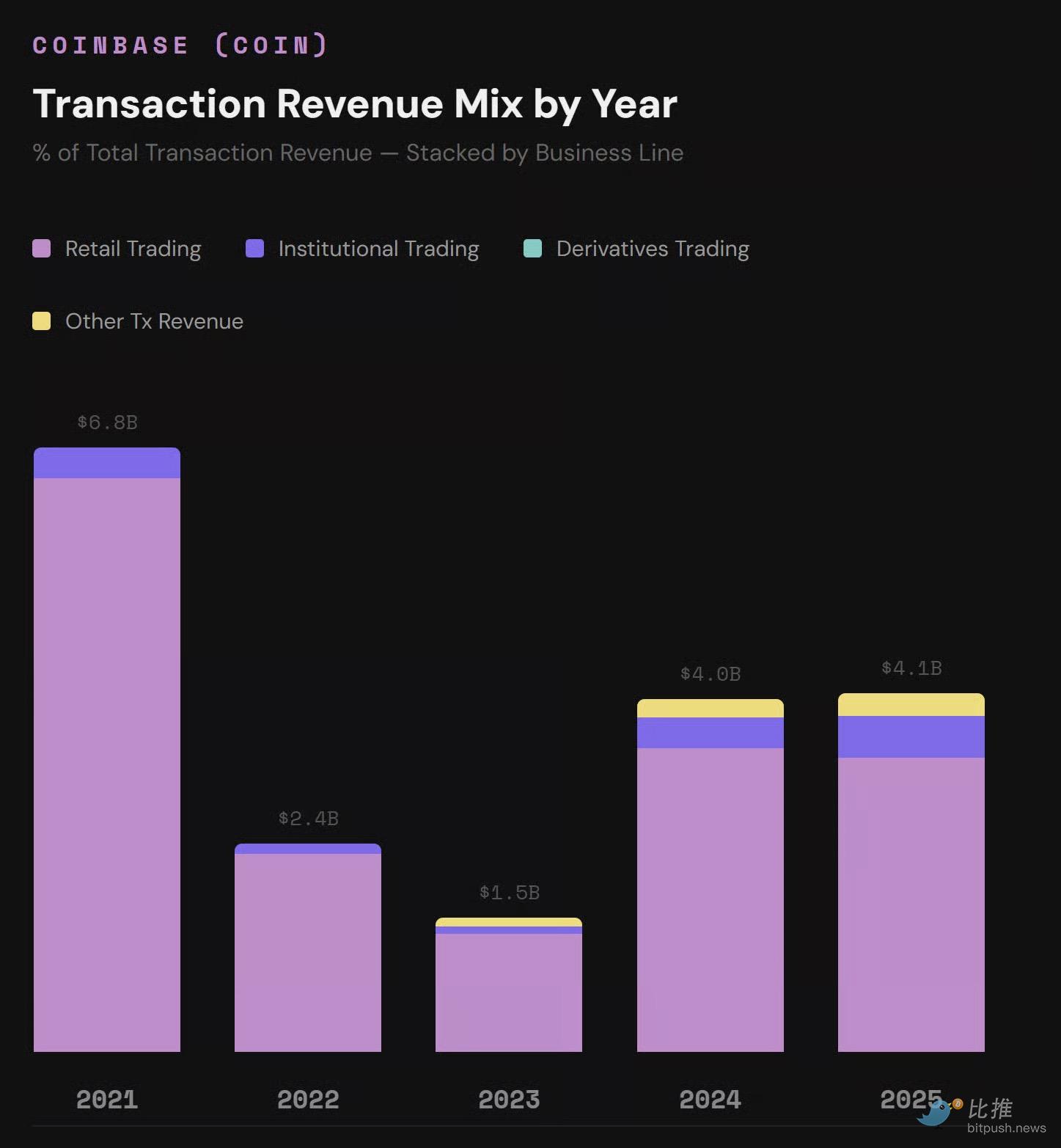

Revenue Composition Visualization:

(Based on Coinbase 10k and SEC filing data)

Key Takeaways on Transaction Revenue:

-

Retail Dominance Slowly Fading: In 2021, retail trading accounted for 95% of transaction revenue and 88% of total revenue. By 2025, these figures dropped to 82% of transaction revenue and 48% of total revenue, respectively.

-

Institutional Trading Share Growing: In 2025, institutional trading accounted for 12% of total transaction revenue, up from 5% in 2021.

-

Other Transaction Revenue: Currently accounts for 6.2% of total transaction revenue. This primarily stems from Base L2 sequencer fees and payment revenue—a new category that didn't exist before 2023.

-

More Resilient Revenue Structure: When retail trading slowed in 2022, Coinbase lost almost all its income. Today, revenue is supported by three streams rather than a single source, helping to smooth cyclical revenue fluctuations during bear markets.

-

Not Yet Back to Peak: Despite progress, transaction revenue has not returned to 2021 levels. In fact, 2025 transaction revenue was down 40% compared to 2021 (mainly due to a 48% drop in retail transaction revenue).

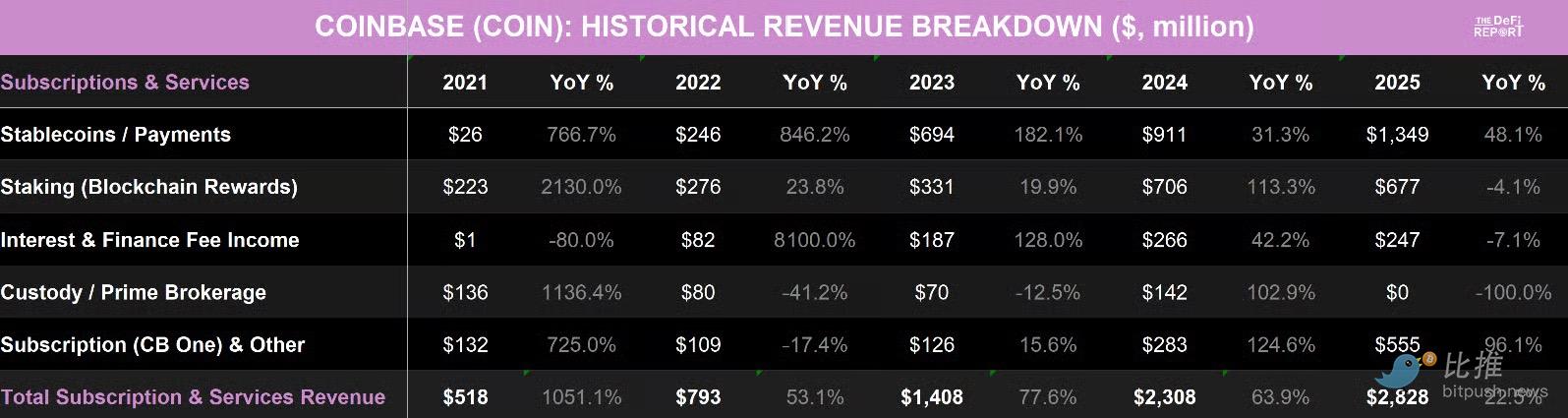

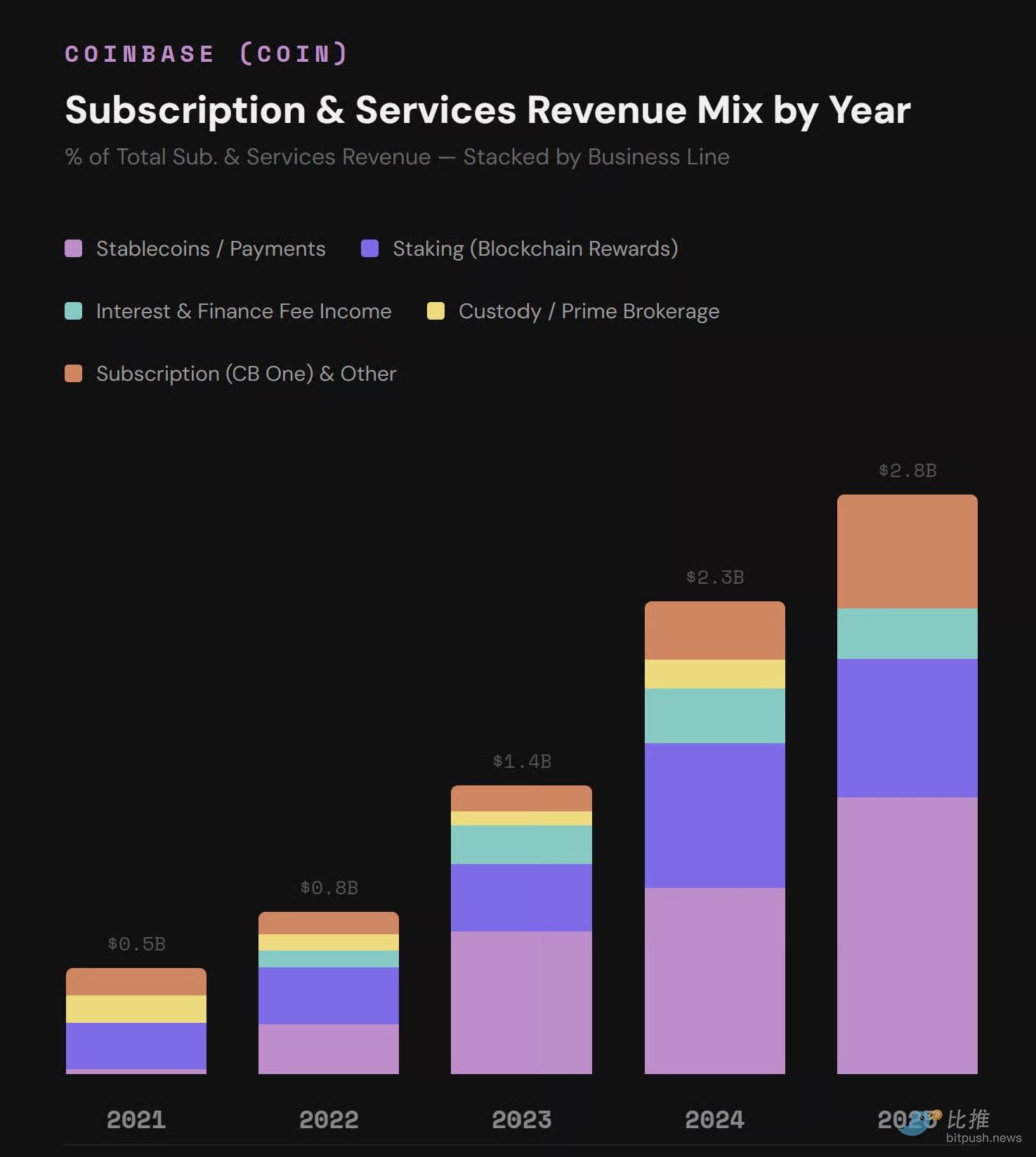

Subscription and Services Revenue

Data Source: Coinbase 10k, SEC filings

Revenue Composition Visualization:

<极简>

(Based on Coinbase 10k and SEC filing data)

Key Takeaways on Subscription and Services Revenue:

-

Strong Overall Growth: This segment grew 5.5x over the past 4 years, with a Compound Annual Growth Rate (CAGR) of 53%. Most notably, this business grew every year, even during the 2022 bear market.

-

Stablecoins Become a Pillar: Stablecoins have become the largest single revenue source in this segment, growing to $1.35 billion in 2025, a 52x increase from 2021, accounting for 19% of total revenue in 2025. This revenue comes from the partnership with Circle (USDC): Coinbase receives 100% of all USDC revenue generated on its platform (exchange, Prime institutional services, custody) and 50% of all residual interest earned on USDC reserves off-platform (other exchanges, DeFi, wallets, etc.). In fact, Coinbase earns more than half of Circle's revenue through this agreement.

-

Staking Business: Revenue peaked at $706 million in 2024 and declined by 4% in 2025. We attribute this primarily to the growth of DeFi and a significant decrease in ETH staking rewards.

-

Subscription Revenue (Coinbase One): Grew 96% in 2025, accounting for 7.7% of total revenue. Coinbase One now has over 1 million subscribers, generating SaaS-like recurring revenue. Note that custody fee revenue has been consolidated into this item starting in 2025.

-

Revenue Share: Subscriptions and Services now account for 41% of total revenue. This revenue is recurring, less volatile, and consistently growing, providing a good counterbalance to the declining and volatile retail transaction revenue.

Overall: Coinbase's total revenue grew 9.4% in 2025 but is still down 6.4% from the 2021 peak.

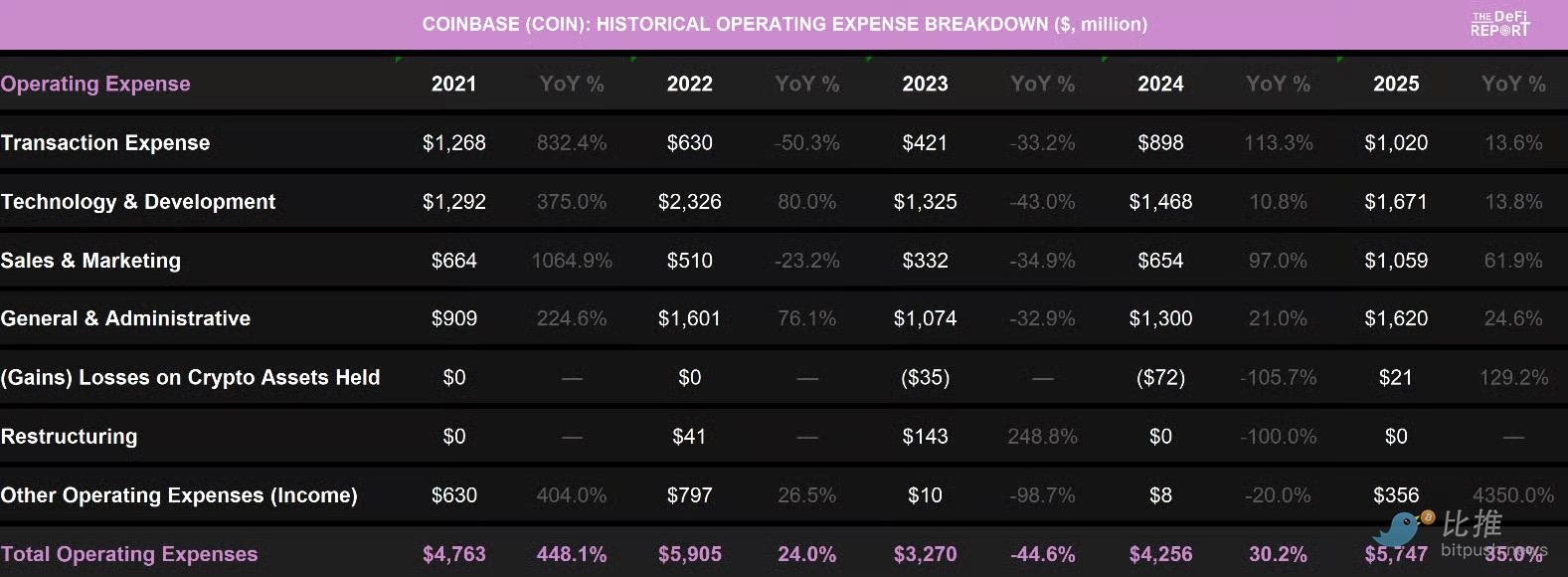

Operating Expenses 2021 – 2025

Data Source: Coinbase 10k, SEC filings

Expense Composition Visualization:

(Based on Coinbase 10k and SEC filing data)

Key Takeaways on Operating Expenses:

-

Once on the Brink of Bankruptcy: In 2022, Coinbase's operating expenses reached $5.9 billion, while revenue was only $3.2 billion. The company was burning cash at an alarming rate, with Technology & Development alone costing $2.3 billion and General & Administrative (G&A) $1.6 billion.

-

Structural Adjustment: This was addressed in 2023. By restructuring the workforce (laying off 950 employees), optimizing hiring processes, and refocusing on core products, the company cut operating expenses by 45%.

-

Operating Leverage Emerges: Although current operating expenses have returned to 2022 levels, the business is now twice the size it was then and has successfully turned an operating deficit into operating leverage. Coinbase's operating margin was 21% in 2025.

-

Expense Distribution: 17.7% of expenses are transaction-related (variable costs that scale with business size); 18.4% is for Sales & Marketing (this has grown consistently,主要用于 USDC rewards, NBA sponsorship, and Coinbase One customer acquisition).

-

Management & R&D: The remaining 57.3% comes from Technology & Development (up 13.8% in 2025) and General & Administrative (up 24.6%). Given that 2026 revenue expectations may decline, we believe Coinbase may again reduce headcount to lower fixed costs during a bear market.

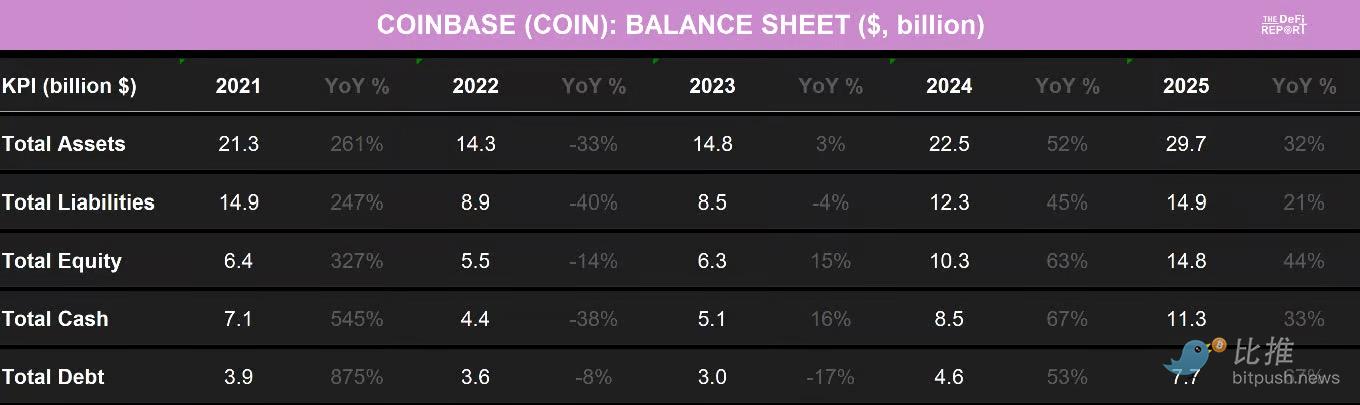

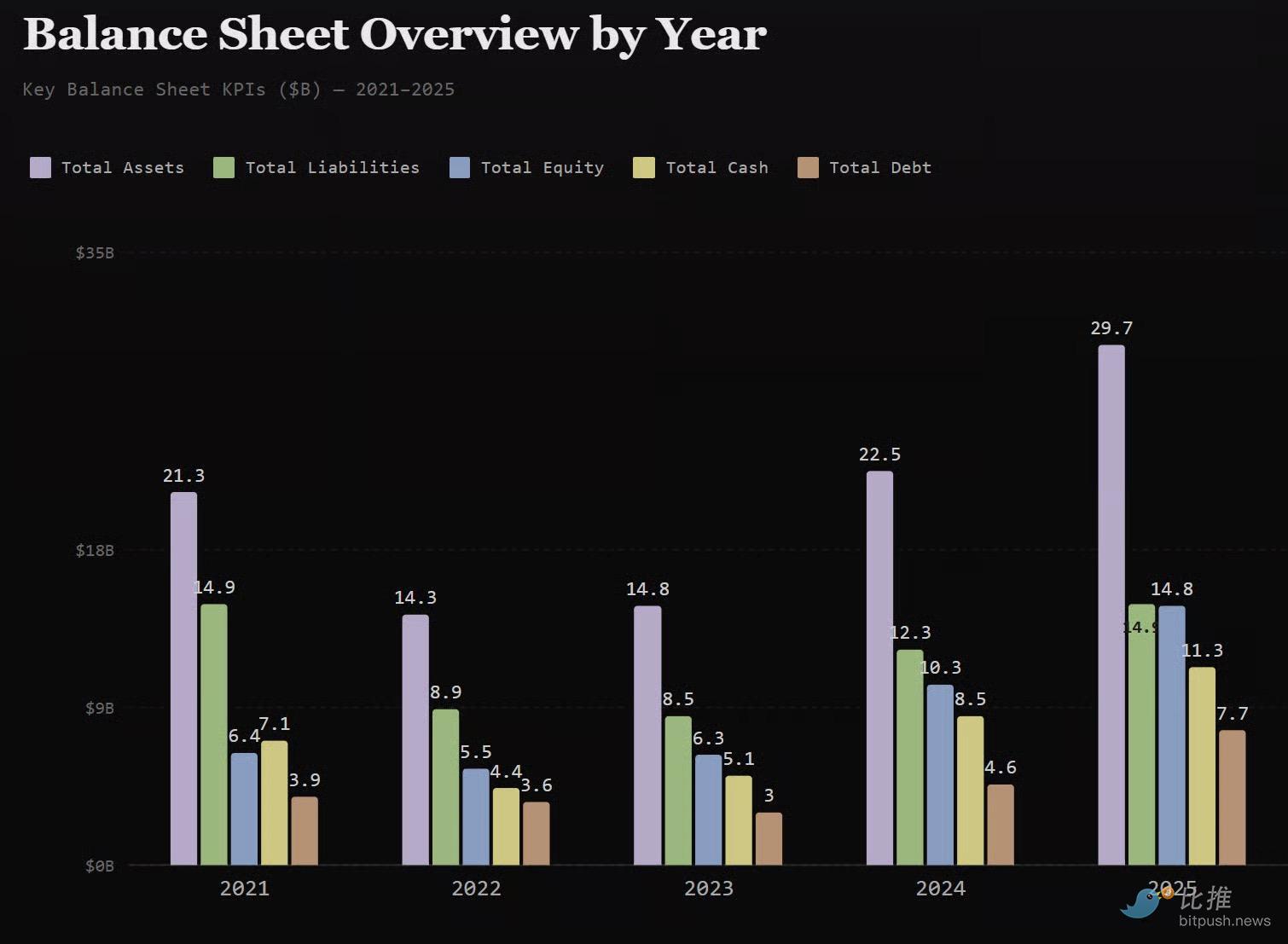

Balance Sheet 2021 – 2025

Data Source: Coinbase 10k, SEC filings

Balance Sheet Visualization:

(Based on Coinbase 10k and SEC filing data)

Key Takeaways:

-

Debt Situation: $1.27 billion in debt is due this June. Of the total $7.7 billion debt, about 40% is convertible debt with a 0% interest rate; another $1.26 billion is due in 2030 with an interest rate of just 0.25%. The annual cash interest expense on existing debt is approximately $65 million (a composite rate below 1%). For comparison, Coinbase earned $297 million in interest and other income in 2025 alone—4.5 times its interest expense.

-

Liability Composition: Of the $7.2 billion in total liabilities, $6.2 billion are "pass-through items" hedged by assets on the other side of the balance sheet (customer custodial fund liabilities and return of collateral obligations). The remaining $1 billion consists of current liabilities related to accounts payable and operations.

-

Asset Composition: Besides cash (at an all-time high), Coinbase has $4.2 billion in goodwill related to the acquisition of Deribit, $2 billion in crypto assets (BTC & ETH), $623 million in strategic investments (including Circle equity), and $310 million in tradable investments. Another $3.3 billion consists of operating assets (receivables, loans, equipment).

-

Significant Change: The most notable change in 2025 stemmed from the acquisition of Deribit (a leading derivatives exchange). Goodwill jumped from $1.1 billion to $4.2 billion, and intangible assets increased from $47 million to $1.4 billion due to this transaction.

Overall Assessment: Coinbase's balance sheet is in its healthiest state ever. A net cash position of $3.6 billion (not including $2.9 billion in crypto and strategic assets) means it has ample fuel to weather storms, make strategic acquisitions, and invest in new product lines. Additionally, its debt structure is extremely cheap.

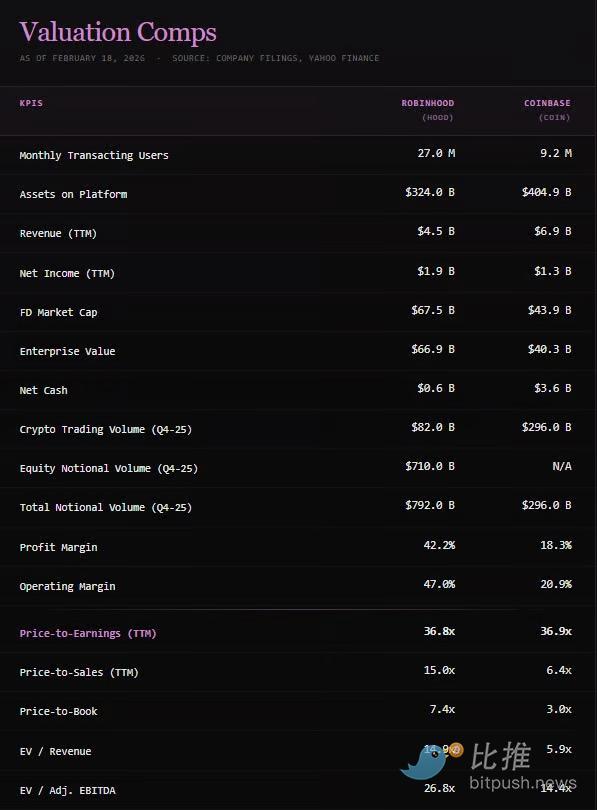

Competitive Landscape

Data Source: Yahoo Finance

COIN vs HOOD

When discussing Coinbase's competition, we focus on Robinhood. Both companies are founder-led, founded around the same time (Coinbase 2012, Robinhood 2013), both serve Millennials and Gen Z, and both are building financial rails based on crypto technology.

We believe both companies have the opportunity to reach a $1 trillion valuation and become leading financial institutions of the future.

Valuation Comparison with HOOD

Data Source: Coinbase 10k, SEC filings

Key Takeaways:

-

Valuation Divergence: Although the trailing P/E ratios of the two companies are almost identical at 37x, COIN is valued at roughly half of HOOD on almost every other metric. This suggests the market views Robinhood's earnings quality and growth trajectory more favorably than Coinbase's.

-

Reason Lies in Profitability: Robinhood's 47% operating margin and 42% net profit margin are more than double those of Coinbase (21% and 18%). This results in Robinhood generating 45% more operating income ($2.09 billion vs $1.44 billion) despite having 35% less revenue.

-

Two Points to Note:

-

Coinbase's 2025 operating expenses included $345 million in costs related to a data breach and Deribit integration costs, which are non-recurring.

-

Robinhood has stronger cost control and leaner operations. We believe this stems from focus: Robinhood focuses on retail customers, while Coinbase tries to cater to both institutional and retail segments, leading to a broader product line and higher operating costs.

Cash Flow: Coinbase holds $11.3 billion in cash (almost three times Robinhood's $4.3 billion).加上 crypto assets and strategic investments, total available resources of $14.1 billion provide a stronger survival buffer.

Nature of Debt: The vast majority of Robinhood's debt ($11.8 billion) is operational broker-dealer debt (securities lending hedges, etc.), with almost no long-term corporate bonds. Coinbase holds $7.7 billion in corporate debt, but at very low interest rates.

Buybacks & Selling: Robinhood began aggressive buybacks in Q3 2024 (repurchasing $910 million). Coinbase began buybacks in 2025 ($408 million) and stated it would look for opportunities during bear markets. Meanwhile, CEO Brian Armstrong's selling drew negative attention (selling approximately $550 million between April 2025 and January 2026). While the optics are poor, we believe the market overreacted, as this was part of a normal, pre-set selling plan for executives and represented only 3.3% of his holdings.

Risk Factors

-

Intensifying Competition: Traditional brokers (Schwab, Fidelity) are expanding crypto offerings;Binance remains庞大 internationally;BlackRock and Fidelity are building competitive infrastructure for institutional clients.

-

Regulation: Coinbase is playing a role in the Clarity Act negotiations. If new regulations favor traditional institutions, it could severely打击 native crypto services.

-

Cyclicality: Despite revenue diversification, 59% of revenue is still directly tied to crypto prices and market sentiment.

-

Interest Rate Risk: Stablecoins account for 19% of total revenue. If the Fed cuts rates significantly, it will directly impact this revenue. Coinbase warned in its Q1 2026 guidance that revenue could decline by $100-$150 million due to this.

-

Security Risk: The data breach in May 2025 resulted in a $345 million loss and reputational damage.

-

Concentration Risk with Circle: An often underestimated risk is that the potential GENIUS Act could render their partnership illegal. The legal争议点 is whether Coinbase, as the custodian of users' USDC, qualifies as a "holder" prohibited from receiving interest under the Act. While we believe it does not, investors should monitor this.

Conclusion

Despite a challenging fourth quarter, the underlying business structure of Coinbase is stronger than in any previous cycle. The company has $11.3 billion in cash reserves, a $2.8 billion base of subscription and services revenue (41% of total revenue), and leading positions in institutional custody and stablecoin infrastructure.

Currently, COIN is valued at roughly half of Robinhood on P/S, P/B, and EV/EBITDA multiples. Given its stronger balance sheet, we believe COIN offers an attractive risk-reward ratio for investors who believe in the long-term growth of the crypto capital markets.

We exited most of our COIN position in Q3/Q4 last year (with a 270% gain) but still hold a position with an average entry price of $99.58 and are looking for opportunities to add.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Group:https://t.me/BitPushCommunity

Bitpush TG Channel: https://t.me/bitpush

Original Link:https://www.bitpush.news/articles/7613394