Author: Yacht

X: @AttackOnTATAYA

From MSTR to STRC+: Where Is the Limit of the Strategy Universe?

"Strategy is a publicly traded company that bought a lot of Bitcoin" is an understanding from the last century.

Of course, Strategy remains the most typical Bitcoin Treasury company in the market. As of June 2026, Strategy holds 843,706 BTC, accounting for approximately 4.02% of the total Bitcoin supply; with BTC priced around $63,000, the value of its BTC reserves is about $53.243 billion. This scale of holdings is enough to make it an undeniable whale in the BTC market, and it also explains why every time Strategy buys BTC, raises funds, sells a small amount of BTC, or adjusts its preferred stock dividends, it is magnified by the market, triggering significant volatility.

But what truly merits study about Strategy is not just how much BTC it bought, but how it placed BTC on the traditional capital market's balance sheet, then used complex products like stocks, convertible bonds, perpetual preferred shares, and on-chain protocols to carve that BTC exposure into different financial products with varying risks, durations, and return preferences. From MSTR to STRC, and now to the on-chain STRC+ ecosystem, Strategy is attempting to upgrade "holding BTC" to "building a credit curve and on-chain yield infrastructure around BTC."

This article aims to address: Is the limit of the Strategy universe infinitely buying more BTC, or transforming its BTC holdings into a credit system acceptable to stock markets, fixed-income investors, and DeFi users alike?

Saylor's Operating Table: Transforming a Software Company into a Bitcoin Treasury

The story of Strategy's founder and executive chairman, Michael Saylor, reads like a reflexive textbook on capital markets. In Murmurcats' character profile, he is not first and foremost a crypto OG or an exchange founder, but a traditional tech entrepreneur. In 1989, he founded MicroStrategy, primarily focused on enterprise data analysis and business intelligence software. During the dot-com bubble, MicroStrategy's stock price soared, and Saylor's personal wealth peaked; subsequently, the company faced an SEC investigation due to financial reporting issues, its stock price plummeted, and he fell from grace.

This history profoundly influenced Saylor and explains why he later adopted an extreme, yet not arbitrary, approach to understanding capital markets. After 2020, against the backdrop of global monetary easing and declining fiat purchasing power, he shifted the company's cash reserves into BTC and gradually transformed MicroStrategy into a publicly traded company with BTC as its core asset. The company's renaming to Strategy was essentially an identity confirmation: this is no longer an ordinary software company, but a financial engineering company with BTC as the core of its balance sheet. A more direct way to put it is: Strategy's BTC purchases are not a simple "company using spare cash to allocate to BTC," but a sophisticated capital design. It raises funds by issuing stocks, bonds, convertible bonds, and preferred shares to convert capital into BTC; as its BTC holdings expand, the market then prices MSTR based on its BTC exposure per share, Saylor's narrative power, and potential financing capabilities; when the valuation is high enough, the company continues to raise funds and buy more BTC.

This was Strategy's earliest flywheel: BTC rises, MSTR stock price rises; MSTR stock price rises, the company's financing ability strengthens; after raising funds, the company continues to buy BTC; the BTC exposure per share and market narrative continue to strengthen; the market continues to give MSTR a premium.

In a bull market, this flywheel is very sharp. It transformed a software company whose operations were not inherently sexy into one of the most active and controversial BTC proxy assets in the U.S. stock market. As a result, MSTR's trading volume even surpassed NVIDIA's at one point, and the market began to confirm that what people were truly trading was not the software business, but the "leveraged BTC narrative in listed company form." But the flywheel's weakness lies within the same structure. As long as it relies on capital market premiums, it is inevitably constrained by the reverse forces of premium contraction, rising financing costs, and BTC decline. Strategy is not an auto-liquidating contract account, but it is a listed company with cash obligations, dividend obligations, and market confidence constraints.

The MSTR Flywheel Can Spin, But It Can Also Jam

Understanding Strategy requires understanding mNAV.

mNAV can be roughly understood as the multiple of MSTR's market value relative to its BTC net asset value. When mNAV is above 1, especially significantly above 1, the market values MSTR higher than the net value of its BTC on the books. At that point, if the company issues common stock to buy more BTC, although it dilutes equity, if the financing price is high enough, the newly added BTC may increase the BTC exposure per share, leading to "enhancement." This is the essence of premium issuance. Conversely, when mNAV falls or even drops below 1, issuing equity at a low price becomes awkward. The dilution from new shares may offset the benefits of buying BTC; when the company needs to pay preferred stock dividends, debt interest, or replenish cash, and mNAV is already at a low level, selling a small amount of BTC for balance sheet management may be more reasonable than issuing common stock at a low price.

Existing research tends to suggest that DATs share the characteristics of significant return exposure and sentiment-driven repricing. For example, Strategy has positive exposure to BTC returns, and BitMine Immersion Technologies also has positive exposure to ETH returns, but this exposure does not equate to stable linear amplification. A high mNAV may represent market heat and financing capability, but it may also represent valuation crowding and downside risk. This is crucial for investors. MSTR is indeed an equity-based exposure tool for BTC, but it is not an unconditional BTC leveraged ETF. It is simultaneously influenced by BTC price, equity market risk appetite, financing structure, mNAV status, Saylor's narrative power, and market sentiment. When BTC and U.S. stock risk appetite rise together, MSTR may receive dual support; when BTC rises but U.S. stocks weaken, or BTC falls and the market is no longer willing to give a premium, MSTR's performance may deviate from the simple "BTC substitute" logic.

The public may overreact to Strategy selling BTC, but Strategy selling BTC does not equal Strategy liquidation. It is more like a signal: when common stock financing is no longer economical, cash buffers are low, and preferred stock and debt obligations persist, the company begins to balance between the "continue buying BTC narrative" and "practical cash management."

This is the first layer of the Strategy universe—MSTR; but MSTR is just the entrance. What truly propelled Strategy from a BTC treasury company to a BTC credit system is the series of preferred shares and credit instruments it subsequently issued.

Strategy's Financial Product Chess Game

Strategy's product spectrum is no longer limited to MSTR; its scale is larger than you might imagine.

MSTR, as common stock, is defined by Strategy as "Amplified Bitcoin," i.e., leveraged BTC exposure. It absorbs the excess volatility and performance stripped from the credit instruments in the BTC holdings, aiming to increase Bitcoin Per Share over the long term. In other words, MSTR bears the most equity-like, volatile, and narrative-driven layer of risk.

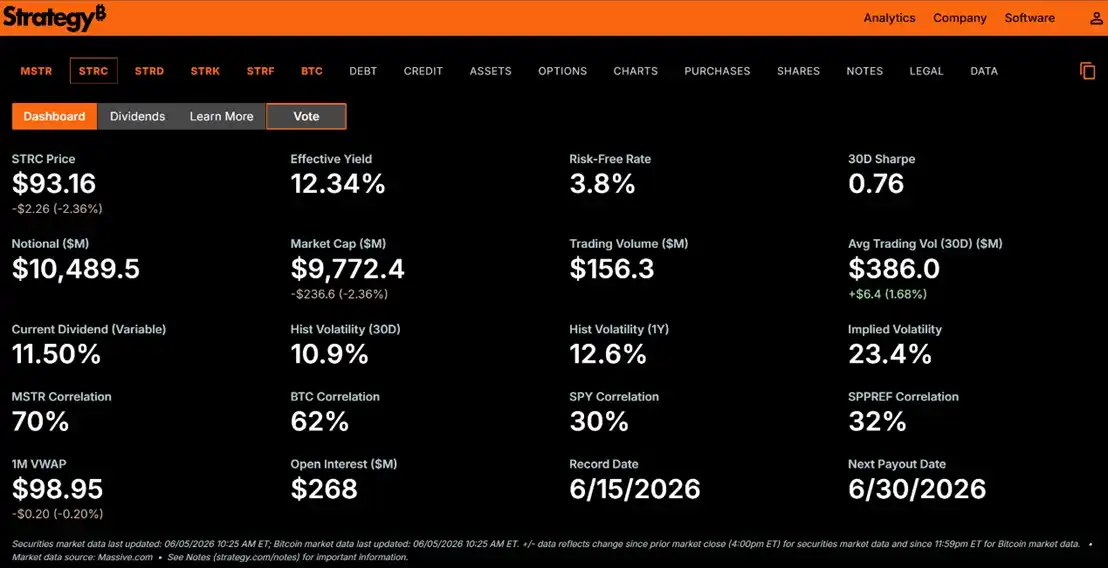

On this foundation, STRC is Strategy's perpetual preferred stock, positioned as "Short Duration High Yield Credit." Materials indicate that STRC currently pays an 11.50% annualized dividend, disbursed in cash monthly; the dividend rate adjusts monthly, aiming to encourage STRC to trade around a $100 par value and reduce price volatility. As the market corrected again, STRC's price fell to approximately $94, with an effective yield of 12.15%, a nominal size of about $10.4895 billion, a 30-day average trading volume of about $379 million, and a 30-day historical volatility of 10.2%.

STRD is Long-Term High Yield Credit, with a fixed annual dividend of 10%, paid quarterly, but due to a price discount, the effective yield in the snapshot reached 14.45%. STRK is Structured Bitcoin, convertible into MSTR common stock, combining preferred stock cash flow with participation in common stock upside, with a fixed annual dividend of 8% and an effective yield of 11.74%. STRF is a higher-level long-term credit instrument, with a fixed annual dividend of 10%, governance rights, and a step-up mechanism for missed dividends, with an effective yield of 10.44% in the snapshot.

The significance of this combination is: Strategy is slicing the same BTC balance sheet into different tiers of risk. Common stock MSTR takes the most complete upside and downside; STRC provides short duration, high yield, floating dividends, and monthly payments; STRD, STRK, and STRF respectively cater to different duration, conversion rights, priority, and yield needs.

STRC is the most critical layer. It turns "money seeking fixed income" into capital for Strategy to buy BTC. Traditional fixed-income investors may not want to buy BTC directly, nor bear the severe volatility of MSTR common stock. But if there is a tool that pays interest monthly, trades around a $100 par value, and offers yields significantly higher than traditional short-term bonds, they might be willing to participate. Strategy then uses this portion of funds to continue servicing its BTC balance sheet.

The innovation and controversy of STRC lie in this: STRC appears to be a high-yield money market product, but its risk does not come from U.S. Treasuries or a diversified credit portfolio; it comes from the single company Strategy's BTC asset coverage, capital structure, and mNAV status. What it offers investors is not risk-free returns, but relatively high cash dividends in exchange for bearing the risk of BTC declines eroding asset buffers, mNAV breakdown, and the dividend mechanism's repricing risk.

In other words, STRC is not "safe BTC," but a "credit product issued by a BTC treasury company."

Where Does STRC's 11.5% Yield Come From, and Who Bears the Risk?

The most attractive aspect of STRC is its yield, and the most easily misunderstood aspect is also its yield. If a product looks like a short-duration credit in traditional markets, offers an 11.5% annualized dividend, and attempts to trade stably around a $100 par value, investors naturally ask: Where does this money come from? Who bears the tail risk?

STRC's de-pegging could occur under the following scenarios:

Scenario One: BTC decline breaches the asset buffer. Strategy's underlying assets are primarily BTC. When BTC falls rapidly, the company's asset coverage declines, and leverage mechanically increases. Although STRC has priority over common stock, it is still preferred stock, not a risk-free bond. The deeper BTC falls, the thinner the safety cushion of STRC's priority claim on the remaining assets becomes, making it easier for its price to fall below the $100 par value.

Scenario Two: The dividend increase trap. STRC's design goal is to bring its price back near par through monthly dividend adjustments. If STRC hovers between $95 and $99, the dividend rate may increase; if it falls below $95, the pressure to increase is greater. In the short term, this can attract yield-seeking buyers back; in the long run, each increase means higher cash outflows for Strategy. If the STRC scale continues to expand, the marginal cost of dividend increases will rise higher and higher.

Scenario Three: The flywheel breaks after mNAV falls below 1. Strategy's ideal deleveraging method is to issue common stock when mNAV is above 1 to buy BTC or improve the capital structure. But if mNAV remains below 1 for an extended period, common stock financing would dilute existing shareholders, forcing Saylor to choose among several uncomfortable options: continue issuing higher-cost preferred shares, unilaterally reduce or suspend the narrative of pursuing a stable par value, or sell BTC to replenish cash.

The discussion about Strategy selling BTC precisely illustrates the real-world shape of this risk. Strategy will not necessarily sell BTC on a large scale because BTC is the core of its valuation narrative; but when cash reserves are insufficient, mNAV does not support common stock financing, and preferred stock dividends and debt interest must be paid, selling small amounts of BTC may become part of balance sheet management. It is not contract liquidation, but a credit structure entering a stress zone. We draw a macroeconomic analogy with gold and BTC. In a liquidity crisis, neither gold nor BTC are necessarily true safe-haven assets; instead, they may become "ATMs": when the market needs cash, the most liquid and easiest-to-sell assets are sold. The gold market still has issues like partial reserves, opaque custodianship, and leasing systems; BTC's advantage lies in on-chain transparency and verifiability, but under financial market stress, it too can be used to raise liquidity.

Therefore, STRC cannot be explained solely by "BTC's long-term rise" when describing a credit product paying monthly interest. STRC's stability depends on three things holding true simultaneously: the BTC asset buffer is sufficiently thick, Strategy has the ability to continue paying dividends, and the market still believes in the MSTR/STRC financing flywheel. If any one of these weakens, STRC will be repriced from a "high-yield stable instrument" to a "credit product with BTC asset coverage risk."

STRC+: How to Bring Strategy Credit On-Chain

If STRC is the core security of Strategy's credit system, then Saturn and Apyx represent the next step: packaging the cash flows from preferred shares like STRC into on-chain stablecoin yields.

The Saturn project divides the new financial stack into three layers: the first layer is Digital Capital, i.e., BTC; the second layer is Digital Credit built by institutions like Strategy on top of BTC; the third layer is financial applications built on Digital Capital and Digital Credit. Saturn believes it is building the third layer—a digital currency layer within a BTC-backed financial system.

Saturn uses a dual-token structure with USDat and sUSDat. USDat is a stablecoin used for liquidity and settlement, with the initial reserve target being 100% allocation to tokenized U.S. Treasury products (M0), and users can mint and redeem it with USDC via the Saturn app. USDat itself does not directly generate yield; it's more like a settlement and liquidity layer. sUSDat is the yield layer. Users stake USDat to obtain sUSDat, and Saturn uses related funds to gain digital credit exposure. Documentation shows that during the launch phase, sUSDat's digital credit exposure is 100% allocated to STRC, with a target yield of 11%+. sUSDat's yield comes from dividends of digital credit instruments like STRC, reflected through the exchange rate growth of an ERC-4626 vault, eliminating the need for users to manually reinvest.

Saturn's risk control focuses on dynamic reserves. It uses the LTV of Strategy's digital credit strategy to determine the STRC allocation ratio: when LTV is low, indicating stronger BTC and equity buffers, it can increase STRC exposure to pursue yield; when LTV is high, it shifts toward U.S. Treasuries to enhance stability. The higher the LTV, the lower the STRC allocation for sUSDat, potentially dropping to 0% in extreme cases. This indicates Saturn is not simply "packaging full-allocation STRC yield," but attempting to dynamically switch between STRC yield and U.S. Treasury stability.

But Saturn's risks are also clear. STRC holdings are off-chain digital credit, held through a BVI professional fund structure, and the custodian, fund manager, and audit/attestation mechanisms all become parts users must trust or verify. If Strategy defers STRC dividends in severe market conditions, sUSDat yields would also pause and accumulate; because STRC is cumulative perpetual preferred stock, deferral may not constitute immediate default, but the price could de-peg, and users would still face uncertainties in secondary market prices and queue processing upon exit.

The path of the Apyx project is more akin to a "stablecoin/savings protocol for a basket of DAT preferred shares." In the Apyx Docs, apxUSD is defined as an over-collateralized, dividend-backed synthetic dollar, different from traditional fiat-backed stablecoins like USDT or USDC. Its stability is supported by reserves of crypto-related, dividend-paying real-world assets, and redemptions are settled in USDC, not by directly delivering the underlying preferred shares.

Apyx also employs a dual-token structure. apxUSD is a non-yield-bearing synthetic dollar used for collateral, quotation, and liquidity in DeFi and CeFi; apyUSD is a savings-type stable asset that generates yield by absorbing dividends from DAT company preferred shares. Apyx describes itself as one of the Dividend-Backed Stablecoin protocols, initially supporting assets like STRC, the variable-rate perpetual preferred stock issued by Strategy. Its four core components are: Users, Offchain Treasury, Onchain Vault, and the Stock Market. Users obtain apxUSD with USDC, the Offchain Treasury allocates funds to low-volatility, dividend-paying perpetual preferred shares or high-liquidity cash equivalents, collects dividends, and converts them into on-chain distributable yields; the Onchain Vault then distributes the yield to holders by increasing the redemption value of apyUSD.

Compared to Saturn, Apyx's difference is that it's not just packaging a single asset like STRC on-chain, but attempting to build a basket of DAT preferred shares. apxUSD's collateral can be dynamically allocated among preferred shares issued by different DATs and rebalanced according to issuer concentration, liquidity, and coverage requirements. Its long-term goal is to transform preferred share cash flows from public markets into on-chain stablecoin yields.

The risks of Apyx lie in: apxUSD is not a strict 1:1 peg tool, apyUSD yields are not guaranteed, and neither are risk-free assets; users may face insufficient DEX liquidity, apyUSD redemption cooldown periods, underlying preferred share price volatility, off-chain custodial risks, and smart contract risks. In other words, Apyx brings yields on-chain, but also brings credit risk, liquidity risk, and execution risk on-chain along with them.

A New Scene in DeFi: Can BTC Credit Become an On-Chain Yield Underlying Asset?

The most imaginative aspect of Saturn and Apyx is that they offer DeFi a source of stablecoin yield different from traditional ones.

Common sources of high on-chain stablecoin yields in the past often came from funding rates, basis trades, lending spreads, LP subsidies, or protocol token incentives. These yields tend to be cyclical: funding rates are high in bull markets, basis opportunities are abundant, protocols are willing to subsidize, and yields appear high; once scale expands, trades become crowded, or the market cools, yields decline.

What STRC+ wants to tell is another story: yield comes from dividends of DAT preferred shares in public markets. In other words, BTC enters a listed company's balance sheet, the listed company issues preferred shares to raise funds, the preferred shares generate cash dividends, on-chain protocols purchase or hold these preferred shares, and then convert the dividends into on-chain stablecoin yields.

If this logic holds, it has multiple implications. First, it introduces TradFi cash flows into DeFi. On-chain users receive not protocol subsidies out of thin air, nor exchange funding rates, but cash dividends from listed company preferred shares. Second, it transforms BTC from a "static store-of-value asset" into "collateral for a credit curve." BTC itself does not generate cash flow, but listed companies holding BTC can issue securities of different tiers around BTC, forming duration, yield, and risk rankings. STRC is an early product on this credit curve. Third, it adds a new source for stablecoin yields. Apyx documentation emphasizes that the stablecoin market is already large, but most stablecoins do not automatically pass reserve yields to holders; Apyx aims to solve the problem of "idle dollars earning no yield" using DAT preferred share dividends. Saturn separates USDat's liquidity layer from sUSDat's yield layer, letting users choose between stability and yield.

But the challenges on this path are evident. The underlying assets are off-chain securities, not native on-chain assets. Users must rely on custodians, fund structures, audits, NAV oracles, third-party attestations, and redemption processes. Even with high protocol transparency, it cannot achieve the fully atomic verification possible with on-chain spot assets. More importantly, the yield comes from STRC or other DAT preferred shares, which ultimately depend on the issuer's asset coverage and payment ability. Therefore, DeFi users in the STRC+ ecosystem bear not a single risk, but a composite set of risks: Strategy credit risk, BTC price volatility risk, mNAV contraction risk, preferred share secondary market liquidity risk, protocol redemption risk, off-chain custodial risk, and smart contract risk. High yields are not created out of thin air; they are merely split, packaged, transferred, and re-presented through on-chain interfaces.

Where Is the Limit of the Strategy Universe?

As for the ultimate outcome of the Strategy universe, let's make a few more assumptions.

In an optimistic scenario, Saylor successfully creates a BTC-native credit curve. MSTR continues as the high-volatility equity layer absorbing BTC upside and narrative premiums; STRC/STRF/STRK/STRD and other preferred and structured products meet the capital needs of different yield and risk preferences; protocols like Saturn and Apyx bring these cash flows on-chain. At that point, Strategy is not just a company buying BTC, but infrastructure connecting BTC, traditional capital markets, and the DeFi yield layer.

During market volatility, STRC becomes a high-risk, high-yield DAT credit product; the STRC+ ecosystem remains usable but with limited scale. Fixed-income investors are willing to bear some BTC-related credit risk for yields above 10%, and on-chain users are willing to allocate a portion to apyUSD or sUSDat. But such products always require high transparency, thick collateral buffers, and sufficient liquidity, and cannot expand indefinitely.

Closer to recent market movements is a pessimistic version: mNAV remains depressed long-term, BTC declines or trades sideways, dividend pressure rises, common stock financing becomes uneconomical, and the cost of continued preferred share expansion grows ever higher. The flywheel shifts from "financing to buy BTC" to "balance sheet defense." In this scenario, Strategy does not necessarily liquidate nor sell BTC on a large scale, but the market would repurpose its credit instruments: STRC would no longer be seen as a yield product close to money market funds, but as a high-yield preferred stock deeply tied to the credit of a BTC treasury company.

Regardless, Strategy's limit is unlikely to be "infinitely buying BTC." Infinite buying is just the first-stage narrative. The true limit is whether the market is willing to accept, in the long term, a new credit system where BTC serves as the underlying asset, mediated by a listed company's capital structure, with preferred share cash flows as the yield source, and then repackaged on-chain by DeFi protocols. If the market accepts it, Strategy will evolve from a BTC treasury company into an issuer of a BTC credit curve, and STRC+ will become one of the new underlying yield assets in the on-chain market. If the market does not accept it, STRC+ will be repurposed back into high-yield credit products: tradeable, configurable, yield-generating, but priced as risk assets, not as a stable yield myth.

This is the true boundary of the Strategy universe: whether BTC can be consistently recognized by capital markets as a type of collateral capable of issuing credit, paying dividends, and supporting on-chain financial applications.

(This article discusses market structure changes and does not constitute any investment advice, platform recommendation, or guidance for evading regulations. Discussions involving specific institutions and products are solely for illustrating different transaction models and infrastructure differences.)