Written by: Thejaswini M A

Compiled by: Saoirse, Foresight News

A central planner walks into a store, the shelves are empty. He says, 'See, there's no demand.' This is an old joke among economists, poking fun at the Soviet Union.

Today, neobanks are stuck in exactly the same trap. Hundreds of startups launched checking account services, with 1.4 billion people actually using them, but making a profit from this business is incredibly difficult. 76% of neobanks are still losing money. On average, each neobank earns only $45 per user per year, while traditional banks can achieve $350.

The root cause lies in the type of product these companies initially chose to build, a business with almost no profit margin to begin with.

To understand the choices made by the early players, one must first see clearly the flaws of the old system they wanted to escape.

Traditional banks continuously extract value from users, even charging fees at ATMs for withdrawing one's own salary. If you don't have much savings to begin with, the experience is even worse. When the first neobanks offered zero-fee accounts with no minimum deposit requirements, users naturally flocked to them.

Soon, hundreds of millions of users flooded onto these platforms. Today, Nubank serves over 60% of the adult population in Brazil. Local traditional banks have always treated ordinary customers as a nuisance, which made the explosive growth of neobanks inevitable.

But these neobanks themselves struggle to survive.

When you use your debit card at a coffee shop, the merchant pays a small transaction fee. Under the Federal Reserve's Regulation II, for a $40 purchase, the fee is capped at about 22 cents, which is divided among the card network, the bank, and the payment processor.

The profit share for neobanks is pitifully small. Millions of users only treat their neobank accounts as daily spending wallets, keeping their mortgages and investments with other institutions. The meager fees, even when accumulated, simply cannot support a business.

The core profit of traditional banks has never been users' daily spending; transaction-based revenue is just a drop in the bucket.

The true profit pillar of banking is credit—the interest generated from loans like mortgages and auto loans. Payment services are merely the daily entry point for banks to reach users; lending is the core method of extracting profit from them. This is also the fundamental reason why most neobanks continue to lose money: without a banking license, they cannot issue loans and collect interest on a large scale. In the early days, most neobanks were just tech platforms built on top of another bank's license, severely restricted by law in conducting large-scale lending.

Nubank started in Brazil in 2013, cracking the market open with a free credit card. At the time, large traditional local banks charged exorbitantly high interest rates, which presented an opportunity for Nubank. By 2026, it had amassed 131 million users.

Today, Nubank is valued at $60 billion. The free account is just a user acquisition tool to get people to download the app; the real profits come entirely from lending.

Last year, the vast majority of its $15.8 billion in revenue came from interest generated by credit cards and personal loans. The personal loan business grew rapidly and has become the largest profit segment. Nubank survived not through some disruptive new technology, but through lending; the slick, user-friendly app was just the bait to hook users.

Source: @sec.gov

Revolut charted another profitable path. In 2025, the company's net profit reached £1.3 billion, with revenue growing 46% year-over-year to £4.5 billion, achieving profitability for five consecutive years. Profits mainly came from foreign exchange fees, membership subscriptions, crypto assets, and its credit portfolio. Credit scale grew 120% year-over-year, reaching $2.9 billion. Early revenue from forex fees and subscriptions gave it ample time to steadily grow its lending business.

Chime took the longest to grasp this principle. In its early years, it relied almost entirely on card swipe fees to survive. In the US, user acquisition costs are extremely high, and the profit share from card transactions is thin. Revenue depended entirely on users continuing to spend. If users reduced their spending, revenue plummeted directly.

In 2025, Chime's revenue surpassed $2 billion, yet it still lost a billion dollars, with losses primarily from high stock-based compensation expenses during its IPO. The company went public with a valuation of $11 billion, but its stock price fell sharply within months. It wasn't until Q1 2026 that it achieved profitability for the first time in its 12-year history, with a net profit of $53 million. The turning point was the explosive growth of its lending products: its earned wage access business revenue is expected to exceed $400 million, and its instant micro-loan business volume surged.

In June 2026, a Nubank developer accidentally triggered a push notification for a liquidation process during a routine system update. A large number of users received push notifications and emails stating that the central bank had liquidated the bank, instructing them on how to claim funds through the deposit insurance fund. Co-founder Cristina Junqueira had to publicly apologize on Instagram, calling it a bizarre operational error and assuring users that the bank and their funds were safe. But within just a few minutes, this erroneous notification made users think the platform was about to collapse.

To be fair, such technical glitches also happen in traditional megabanks—like mistakenly transferring a billion dollars by entering a wrong digit. But venerable institutions like Citigroup, founded in 1812, have a solid foundation. Even when they malfunction, users see it as an ordinary corporate mistake. However, when a startup digital bank spreads rumors of collapse, users immediately rush to withdraw. Old banks are just technologically backward, while emerging online platforms haven't yet learned how to operate as stably as real banks.

In April 2024, the intermediary service provider Synapse declared bankruptcy.

Neobanks are essentially just software service providers. To offer checking accounts, they must connect an entire supply chain of partners behind the scenes. Synapse was that middleman, connecting hundreds of neobanks with the traditional banks that actually hold the funds, handling ledger management, compliance checks, and asset ownership registration.

After Synapse collapsed, all its business records were lost, freezing approximately $265 million in user funds. Partner banks couldn't distinguish which user each sum belonged to. Subsequent audits found $95 million missing, with the entire system completely lacking accountability mechanisms. Users of popular digital banking apps like Yotta and Juno couldn't operate their accounts normally for months, with some even unable to pay their mortgages.

If a banking app's fund custody and intermediary clearing processes all rely on third parties beyond its control, then the system is fundamentally built on sand, destined to collapse.

In the end, the only safeguard against such systemic risks is a banking license. Yet, in the early days, all neobanks claimed they didn't need one at all.

Last October, I wrote that digital banks in the crypto space had real potential for development. At the time, regulatory frameworks were gradually becoming clearer, and a large number of users held on-chain assets and hoped to use them directly for daily payments. This view still holds, but I severely underestimated one thing: the underlying infrastructure built upon partner banks inherits all the potential risks of those partners.

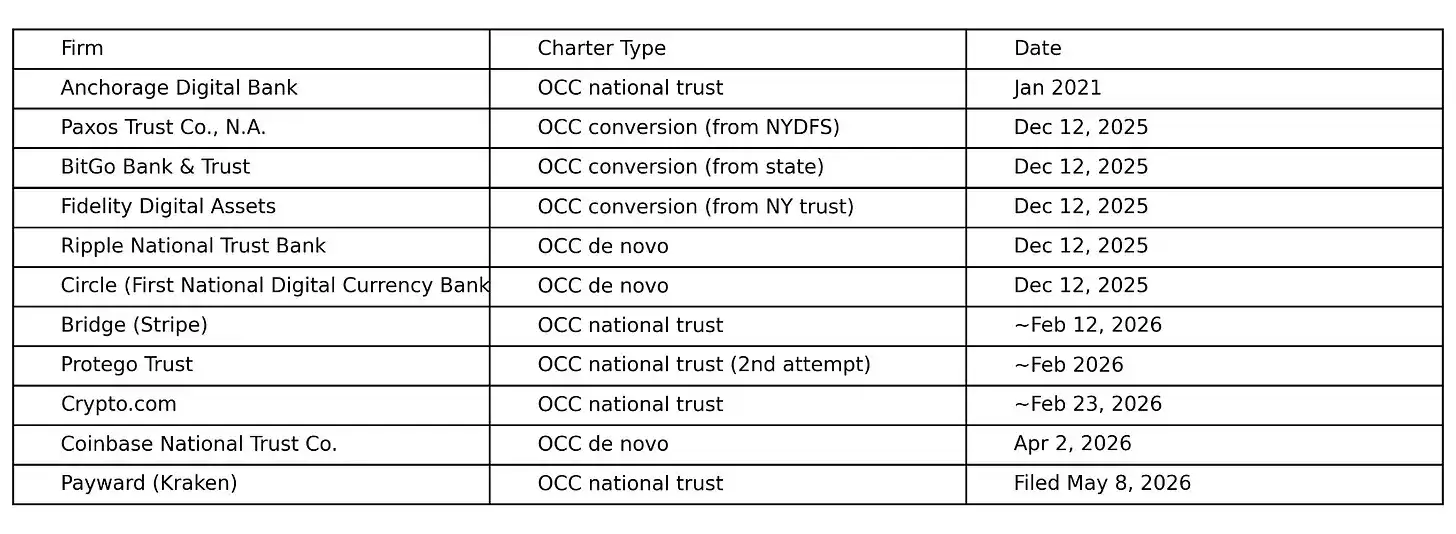

The crypto industry's response is to stop pretending and face reality. From December 2025 to May 2026, the U.S. Office of the Comptroller of the Currency (OCC) conditionally approved about ten national trust charters for crypto and fintech companies, more than the total of the past decade. Paxos, BitGo, Fidelity Digital Assets, Ripple, Circle, Bridge (acquired by Stripe for $1.1 billion), and Crypto.com have all submitted applications for similar charters—exactly the qualifications that neobanks once scoffed at and deemed unnecessary.

A national trust charter is the ultimate way out of the middleman trap. Holding a charter means receiving direct federal endorsement. The company can self-custody user assets, handle payment clearing, and operate across all fifty U.S. states under a unified set of regulations. There's no need to beg for survival from traditional partner banks anymore, nor to stake the entire company's fate on invisible intermediary service providers like Synapse.

Crypto companies have finally realized: if you want to move tens of billions in assets without being constantly constrained by the traditional banking infrastructure, you must obtain formal access qualifications from the federal regulatory system.

Payward, the parent company of Kraken, now has three layers of regulatory qualifications in the U.S.: a Wyoming financial license, a Federal Reserve master account approved in March 2026, and an OCC national trust charter application submitted in May 2026. SoFi acquired Golden Pacific Bancorp in 2022 to obtain an OCC charter. In December 2025, SoFi launched a USD-pegged stablecoin, the first stablecoin issued by a U.S. national bank and built on a permissionless public blockchain. By May 2026, its 14.7 million users could hold, spend, and exchange this stablecoin within the app, with Mastercard as its clearing partner. Coinbase, leveraging the Base public chain, conducts Bitcoin staking and lending business through the Morpho protocol, with over $1.4 billion in Bitcoin collateralized by early 2026.

SoFi's development path is highly representative: student loan servicer → digital neobank → licensed formal bank → stablecoin issuer, completing the entire industry evolution cycle.

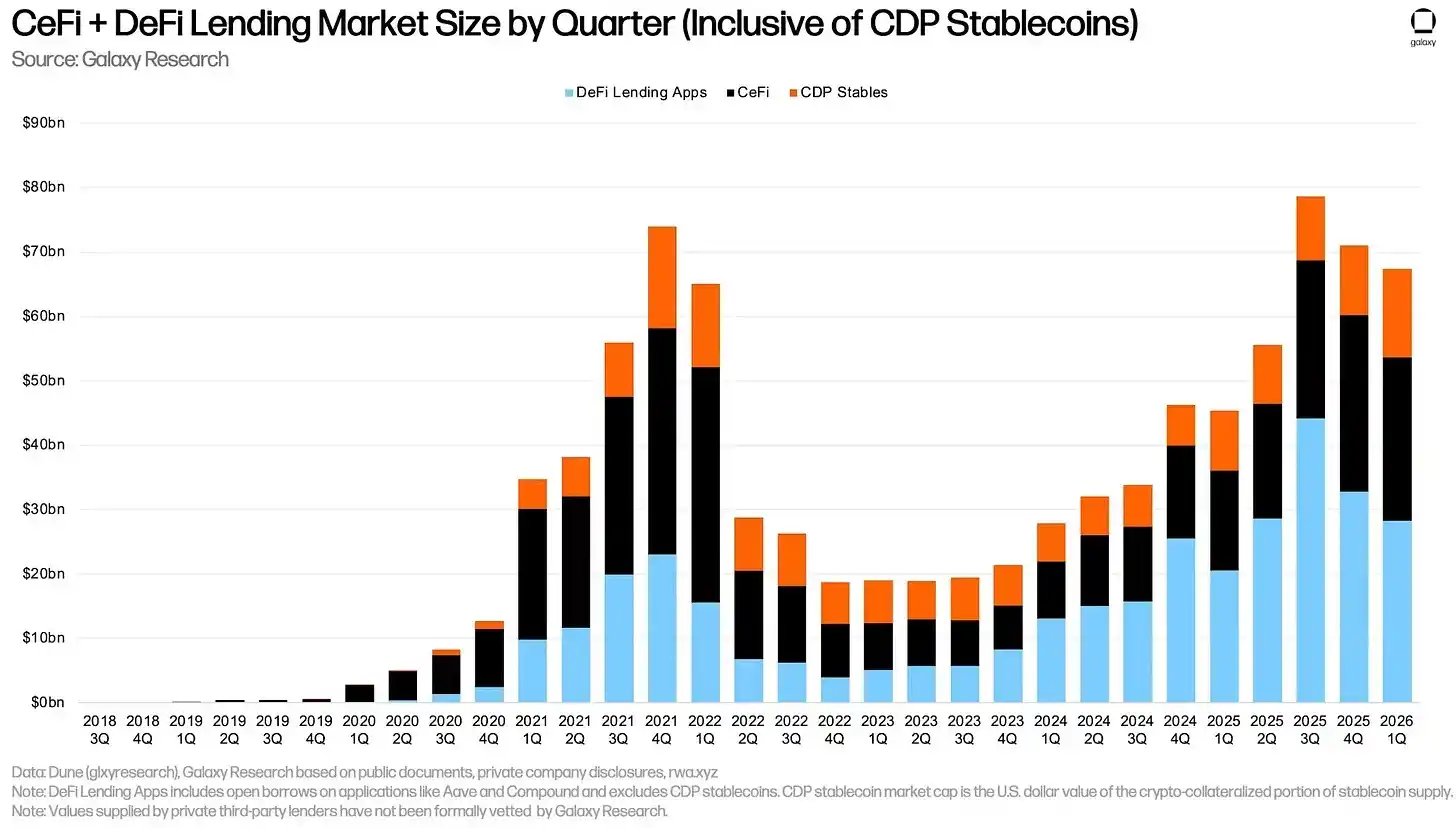

One major shortcoming remains in the industry: unsecured lending. The total scale of collateralized lending in CeFi and DeFi is $67.42 billion.

But the actual deployed scale of unsecured lending across the entire decentralized space is only $24 million. Protocols that once ventured into unsecured lending (Goldfinch, early Maple, TrueFi) have either fully switched to over-collateralized models or gradually shut down. Today, Maple, the largest DeFi lending protocol, has a collateralization ratio as high as 160%.

Blockchain addresses have anonymous attributes, and unsecured lending lacks viable mechanisms for default recovery. In the real world, if a user defaults on a loan, a bank can report it to credit bureaus and file lawsuits. The decentralized space lacks credit agencies and asset collection channels. If a borrower runs away with unsecured assets, they just need to abandon their wallet address, and the funds become completely irrecoverable. Some DeFi protocols tried relying on on-chain reputation data for risk control, but still experienced large-scale bad debts. Practitioners finally realized: without the constraints of real-world law, anonymous users have almost no incentive to repay voluntarily.

Nubank issues loans to its 131 million users, many of whom lack traditional credit history. The platform relies on user transaction behavior for credit risk assessment and approval. This type of business has real commercial value, but its operational costs are extremely high and implementation is difficult. If one wants to replicate such credit products on a blockchain at scale, obtaining a banking license is almost inevitable. It is expected that more and more companies will submit charter applications to the OCC in the future.

Last October, I wrote that crypto digital banks are replicating the development patterns of banking a century ago. Technology constantly iterates, but the underlying logic of how humans use and manage money remains constant. When I wrote that sentence back then, I felt there was a certain beauty in the pattern. Looking at it now, it reveals a different reality.

The essence of banking has always been profit through lending and collecting interest. The neobanks that survived initially promised to break this model, but the players that truly survived ultimately ended up on the path of lending—just with more user-friendly interest rates and smoother product interfaces, while the underlying business logic remained unchanged.

In the end, it all boils down to one sentence: everything changes, but the essence remains the same.