Author: Tom Dunleavy, Head of Venture Capital at Varys Capital

Compilation: Yuliya, PANews

Editor's Note: The market currently commonly views Ethereum as a traditional enterprise, calculating its price-to-earnings ratio based on the fees it generates and concluding it is overvalued. However, Tom Dunleavy proposes a completely different framework: fees are not revenue but network friction; Ethereum is not a company but a "treasury" safeguarding hundreds of billions of dollars in assets, with ETH itself being the lock. The following is a compilation of the original text:

TLDR

-

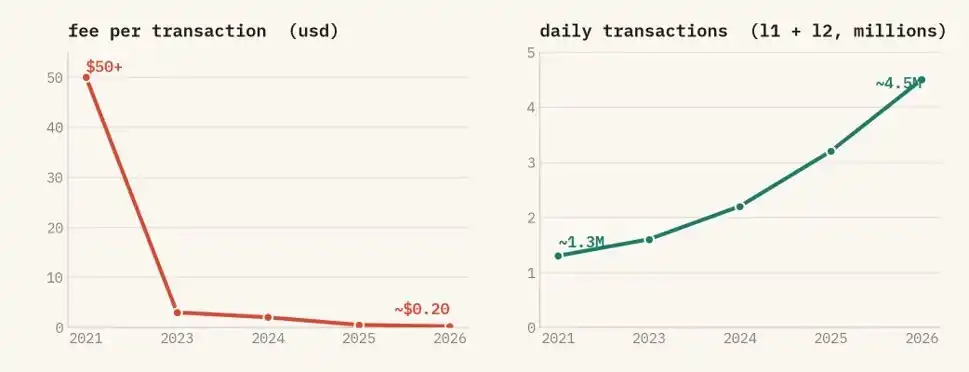

Stop focusing on fees to value Ethereum. Fees are a stumbling block; a successful network will inevitably strive to reduce fees to zero. ETH fees have dropped from over $50 at their peak in 2021 to around $0.20 now, while transaction volume has more than tripled. Plummeting fees signify network success, not failure.

-

After transitioning to Proof-of-Stake (PoS), ETH became the lock protecting the asset treasury. To attack Ethereum, you must control the staked ETH. Controlling one-third can paralyze the network; controlling two-thirds can falsify records. Either way, the cost of malicious action is calculated in ETH, and upon acting maliciously, this ETH is directly burned by the system. This tightly binds ETH's value to the network's security. No network operated this way before the staking mechanism existed.

-

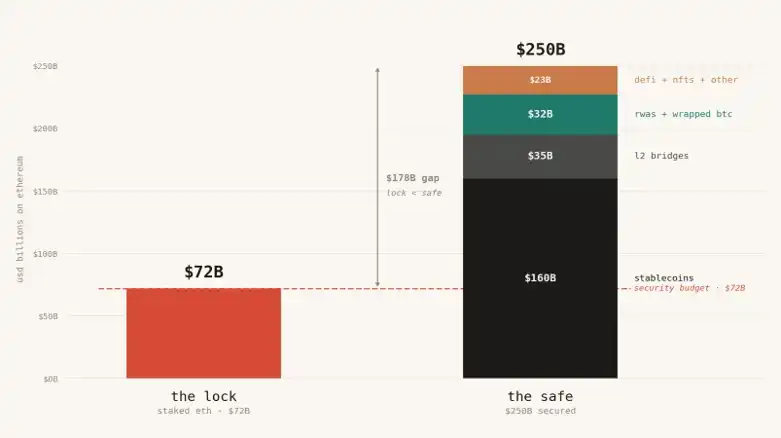

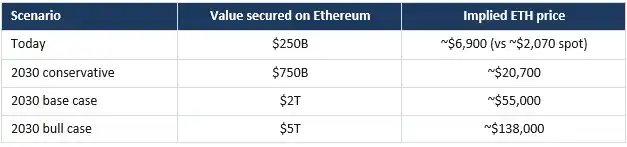

Currently, there are about $250 billion in assets on the Ethereum chain (including stablecoins, tokenized assets, L2 network cross-chain funds, etc.), but the total value of staked ETH protecting these assets is only about $72 billion. This is like using a cheap, flimsy lock to protect a safe full of gold bars. Logically, ETH's fair price should be around $6,900 (currently only $2,070). If on-chain assets grow to trillions in the future, ETH's price must rise to tens of thousands to match its security responsibility.

-

Statements like "Ethereum is like the free Linux system" or "like DTCC (Depository Trust & Clearing Corporation)" are incorrect. The security of Linux and DTCC is provided externally (e.g., the open-source community's goodwill or the legal backing of governments and banks). But Ethereum's security is purchased using its own token, ETH. Therefore, ETH must be valuable, while Linux does not need to be.

-

If ETH fails, Crypto will likely fail as well.

Fees Are Not Revenue, But Friction

Last week, Bankless founder David Hoffman said he finally sold all his ETH, causing a stir in the crypto community. While I respect David's decision, I believe the way people evaluate ETH and other PoS public chains is long outdated. I've discussed my new framework with many people on podcasts, but it seems it hasn't sunk in (perhaps due to my explanation), so today I'll lay it all out clearly at once.

New things require new perspectives. Here's introducing a brand new ETH valuation model.

Many view Ethereum as a company, treating the fees collected as its operating revenue. Seeing fees decrease, they think this "company" is failing and the token is overpriced. This is completely backward; once you understand it, you'll never see it that way again.

In reality, fees are like taxes; the higher they are, the less willing people are to use the network. Lower fees encourage more people to participate, leading to more applications and capital on-chain. The data doesn't lie: the fee per transaction has dropped from over $50 in 2021 to around $0.20 now, but transaction volume has hit new highs, more than triple that of 2021, with L2s handling about 85% of transactions now. It's cheaper to use, and more people are using it. A successful settlement network should aim to reduce tolls to zero.

Ethereum's fees have plummeted, yet transaction volume is at a record high. It's become cheaper, and more people are using it. L2s now handle roughly 85% of the throughput.

So, if fees are the wrong metric, what is the right one?

Ethereum Is a Grand Treasury, ETH Is the Lock

Stop viewing Ethereum as a company; think of it as a massive treasury. This treasury holds approximately $160 billion in stablecoins, $20 billion in RWAs (like U.S. Treasuries, money market funds, and private credit), $35 billion in L2 cross-chain assets (with L2 networks inheriting Ethereum's consensus by design). Additionally, there's about $12 billion in wrapped Bitcoin and around $20 billion distributed across DeFi positions, NFTs, and on-chain treasuries. That totals roughly $250 billion in on-chain assets, growing each quarter.

The safety of the treasury depends entirely on that lock. And everyone has miscalculated the value of this lock. On Ethereum, this lock is forged from ETH.

In the old Proof-of-Work (PoW) system, you used mining hardware to secure the network. The lock was bought externally; its cost wasn't tied to the token's value. But now, with staking (PoS), everything has changed. To attack Ethereum now, you must buy and control the staked ETH. The lock is made from the token itself. This means the treasury's security level and the token's market price become one and the same. You can't separate them.

The Current State: A Lock Cheaper Than the Safe

This is the issue the market is ignoring. Today, the total value of all staked ETH protecting Ethereum is only $72 billion. But the assets it protects are worth $250 billion. The money in the safe is worth over twice as much as the lock protecting it.

This is extremely dangerous. If what you're protecting is worth more than the cost of attacking it, your treasury is fundamentally insecure. For Ethereum to securely protect this $250 billion, the defensive staked capital must be greater than $250 billion, not less than one-third of it.

Currently, only about 30% of ETH is staked. So, simply to make this 30% stake equal the on-chain assets, ETH's total market capitalization would need to be over three times the on-chain assets (1 divided by 0.30). Currently, ETH's market cap is roughly equal to the assets it protects (around 1x). But by my logic, it should be over 3x. Calculating with the current $250 billion, ETH's fair price should be around $6,900, not the current $2,070. That is, even without a single new dollar entering, based solely on the assets it currently protects, ETH's price should more than triple. This aligns directionally with the model of BitMine Chairman Tom Lee.

"But Circle can freeze USDC, so it doesn't need ETH's protection at all."

Every time I say this, someone jumps in with this rebuttal, but it's fundamentally wrong. Here's why:

People think that if Ethereum is attacked, Circle, the issuer of USDC, can just freeze the attacker's address and reissue the tokens. So those hundreds of billions shouldn't count toward Ethereum's security responsibility.

But consider: Circle's freezing mechanism operates based on smart contracts; it executes on Ethereum and relies on Ethereum's ledger. If Ethereum's consensus is broken, there is no universally agreed-upon honest chain, and the freeze mechanism cannot function.

Furthermore, Circle could have chosen not to use Ethereum, opting for a private database instead. They chose Ethereum precisely for its neutrality, deep liquidity, and compatibility with other projects. Since they enjoy these benefits, the trade-off is: USDC's lifeline is tied to Ethereum's security. You want the benefits, you bear the dependency risk.

Moreover, people always assume the attacker wants to steal USDC. That's not it at all. If Ethereum collapses, that $150+ billion isn't stolen; it becomes trapped on a chain with no consensus, unable to be redeemed, with all loans and trades based on it thrown into chaos. The value of these assets isn't taken by a thief; it's destroyed. And that destroyed value is precisely the important factor for security considerations.

An attacker doesn't even need to steal money to profit. They can short ETH, short the entire ecosystem, or they could simply be a hostile actor profiting from paralyzing the network. The more money on-chain, the greater their incentive to cause destruction. Therefore, our security budget must grow alongside the total on-chain assets, not just guard against the small change a thief might steal.

As long as you put money on Ethereum, you consume its security, regardless of whether you have a "freeze" button. All the money must be counted.

"Ethereum is just Linux" or "Ethereum is DTCC."

Another rebuttal favored by the intellectually inclined.

-

First argument: Ethereum is like the Linux system. It's underlying infrastructure, powering the internet, but as an asset, it's worthless. Open-source infrastructure is a free public good; the money is made by the applications running on top, not the underlying protocol. So ETH will be the same: immensely important, yet utterly worthless.

-

Second argument: Ethereum is like DTCC (Depository Trust & Clearing Corporation), the infrastructure behind almost all U.S. securities transactions. DTCC processed $370 trillion in transactions in 2024, with revenues of about $2.5 billion but profits under $500 million. It's critically important, heavily regulated, but its value is only a tiny fraction of the transaction volume. Infrastructure is cheap; even if you can't live without it, even if Ethereum processes endless future transactions, it will only capture meager utility profits, nothing more.

Both arguments fail in the same place.

The security of Linux and DTCC is borrowed externally. Linux relies on the open-source community, reputation, and decades of code review. DTCC relies on U.S. law, federal regulators, and the backing of major banks with dollars and treasuries. Their security guarantees are outside the system. This is precisely why DTCC can settle massive wealth while capturing almost no value itself. It's a member-owned utility designed to operate at cost; it doesn't need a valuable token because trust is provided by the government and banks.

Ethereum has no such external shelter. No government enforces it. No member banks back it. No law can reverse stolen settlements. The only barrier between Ethereum and an attacker is the market value of the staked ETH used to secure it. Ethereum must purchase security for every block, in the open market, with its own asset.

This is the fundamental difference. Linux is software; no one is required to own a scarce asset to run it. DTCC provides collateral in dollars, external to itself. Ethereum's collateral is ETH, internal to itself. You cannot commoditize it to zero because security is not a line of code; it's a quantum of value that must be locked up and put at risk. Strip ETH of its value, and you haven't built a leaner Linux. You've built a chain with no collateral, one no one would trust with a single dollar.

So, stop comparing Ethereum to Linux or DTCC. You should compare it to the dollars and treasuries backing DTCC. No one values the dollar based on how many fees DTCC earns. You'd evaluate the clearing house's fees separately and evaluate the dollars and treasuries serving as the system's collateral—its monetary base—valued in trillions. ETH is not the clearing house. ETH is the collateral building the clearing house. That's the asset you're buying.

Linux never needed a treasury. Ethereum's security budget *is* a treasury, and it's denominated in ETH.

Looking Ahead and Market Dynamics

Following this line of thought. This model doesn't look at fees or market hype at all. It focuses on one core question: How much money will be settled on Ethereum in the future? To protect that money, how much must ETH be worth?

Stablecoins are poised to break $1 trillion in the coming years. RWA tokenization could reach several trillion by 2030. Add in various on-chain applications, and the assets Ethereum protects could soar from the current $250 billion to several trillion. Maintaining that "over 3x" security ratio constant, you can calculate how high ETH's price must rise as capital grows.

Even if you're more pessimistic and lower the security ratio a bit, it doesn't matter. On-chain capital is growing (that's the variable), and the security ratio (that's the leverage)—no matter how you calculate it, the trend is upward.

"This is blind optimism. The market will never price it this way."

This is the most pertinent rebuttal. Indeed, I'm saying what ETH "should" be worth, not what the market will price it at immediately. There's no forced arbitrage mechanism to close the gap. And my logic of "ETH should rise" has indeed been contradicted by its price performance over the past few years. Let's address each point.

-

About what bridges the gap: Ethereum is not an arbitrage; it's demand for the asset that prices the entire system. As value settles on Ethereum, ETH is used as collateral, paired trading asset, and staked to earn the network's base yield. This demand grows with the activity it supports. Reserve assets aren't priced on revenue; they're priced by how desperately the surrounding system needs to hold them. Gold is worth over $18 trillion without generating any cash flow. ETH is the reserve asset of on-chain finance, and this framework merely measures how large that reserve must be.

-

About the staking multiplier: My mental model treats the staking multiplier as a range, not a fixed target. At the current staking rate, parity (staked ETH equals protected value) is around 3.3x. A reasonable range spans from a lenient 1.7x to a strict 5x, where the cost to attack via a two-thirds stake equals the entire protected value. Price tracks protected value at some multiplier within this band. Fixing it to a specific number undermines rigor; this is also where rational people can disagree without breaking the model.

-

About reflexivity: The model does have more than one equilibrium, and nothing definitively selects the highest one. Today, Ethereum is secure enough with below-threshold coverage because acquiring a one-third stake is illiquid, slashing is brutally punitive, and the social layer can fork out an attacker. This is real. But these defenses determine whether an attack succeeds, not whether coverage is sufficient as risks escalate. Thin coverage may be tolerable when protecting $250 billion. When it involves two or five trillion in regulated institutional capital, coverage is no longer an academic question. The gradient to close the gap increases monotonically with adoption.

Finally, the most contradictory aspect is ETH's price over the past 5 years. Logically it should rise, but it has consistently fallen. I think the main reason is: previously, there wasn't enough money on-chain for people to see security as a major issue. When there was only $50 billion on-chain, nobody worried; when it grew to $175 billion, people started feeling uneasy; when it reaches $1 trillion, the first question large institutions ask before entering will undoubtedly be: "Is this chain secure?" And the answer to that question depends entirely on ETH's price. My model can't predict the exact day it will rise, but it tells you that as on-chain capital grows, this upward pressure will intensify. And "on-chain capital is growing" is a point even bears cannot deny.

Some counter with Bitcoin, saying Bitcoin's security budget is negligible compared to its market cap. But Bitcoin primarily protects itself. Ethereum protects other people's dollars and various assets—a far greater responsibility! And the trend is clear: more ETH is being staked, compliant products are continuously buying ETH, and as on-chain activity grows, the burn mechanism is constantly destroying ETH. All of this corroborates the demand growth I describe.

Those who only focus on fees and cash flow will continue shouting that ETH is overvalued. They've completely reversed cause and effect. On-chain activity comes first, and then security is needed. ETH must be valuable to secure the entire ecosystem. Fees are stumbling blocks you should strive to eliminate, not the chips you use to value ETH.