Author: Rejamong

Compiled by: AididiaoJP, Foresight News

Since its mainnet launch in 2015, Ethereum has been positioned by its founder, Vitalik Buterin, as a "World Computer"—a permissionless, globally accessible decentralized platform capable of running smart contracts like a giant computer, enabling applications such as asset transfers, decentralized finance, and supply chain tracking. With its transition to the Proof-of-Stake (PoS) mechanism in 2022, validator nodes have become the "gatekeepers" safeguarding the network's security. They are responsible for proposing blocks, validating transactions, and participating in consensus, directly determining the network's censorship resistance, message propagation speed, and overall resilience.

However, a critical question persists: Has Ethereum truly achieved its goal as a "World" Computer? Or does it resemble more of a "Western Computer"? The answer lies in the geographical distribution of its validator nodes. A recent in-depth analysis from the Four Pillars research team provides a clear answer using actual operational data. Drawing from extensive experience operating over 25,000 validators in Asia, the author reveals the current distribution imbalance and the underlying structural issues and future opportunities it conceals.

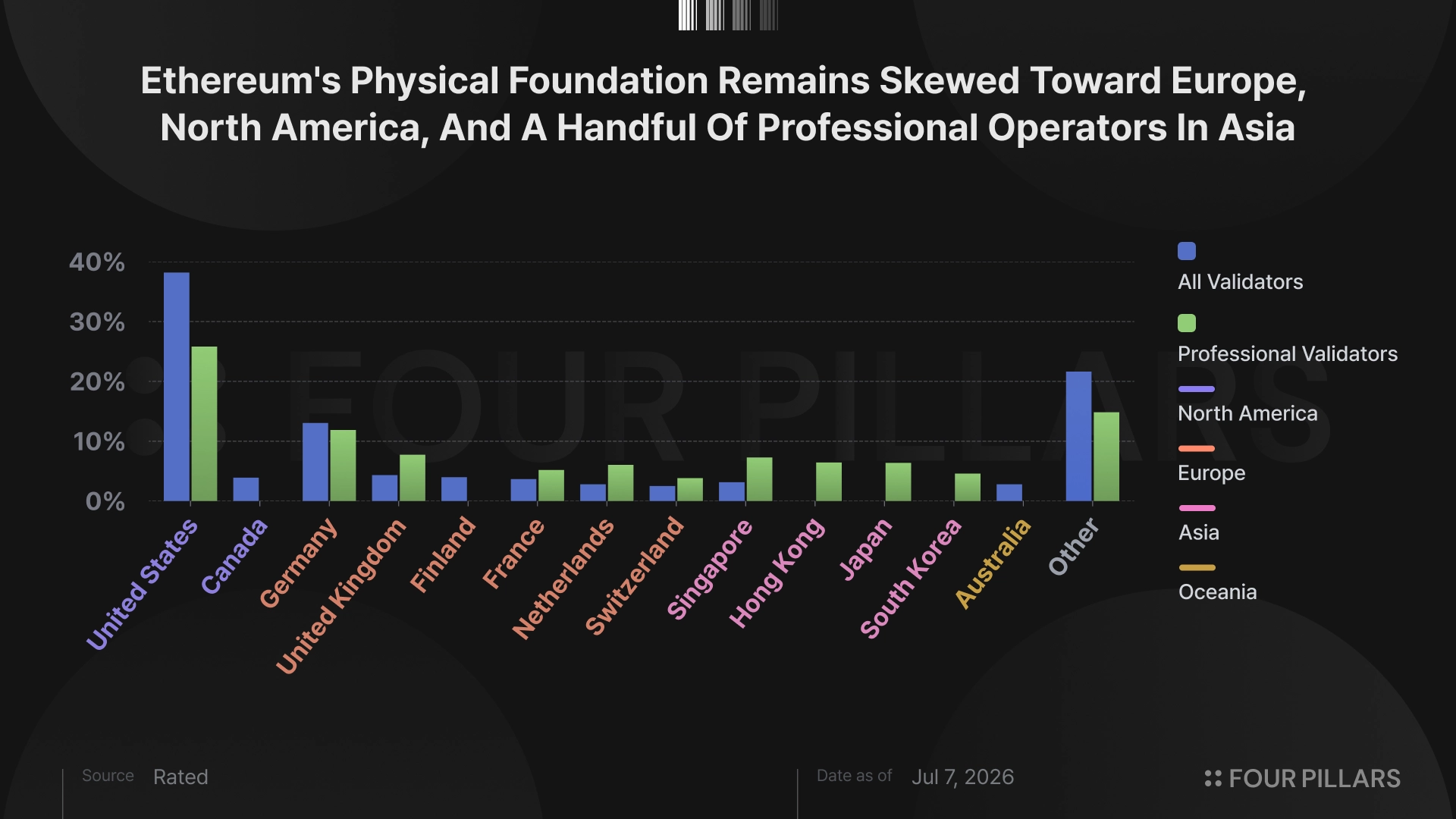

All Validators: US and Germany Dominate Half, Home Nodes a US Specialty

If we consider all validators (including both personal home nodes and institutional nodes) together, the United States alone accounts for 38.19%, followed closely by Germany at 13.04%. Combined, these two countries represent over half of the total network! Among the top ten countries, Asia is barely represented, with Singapore holding a mere 3.15% share.

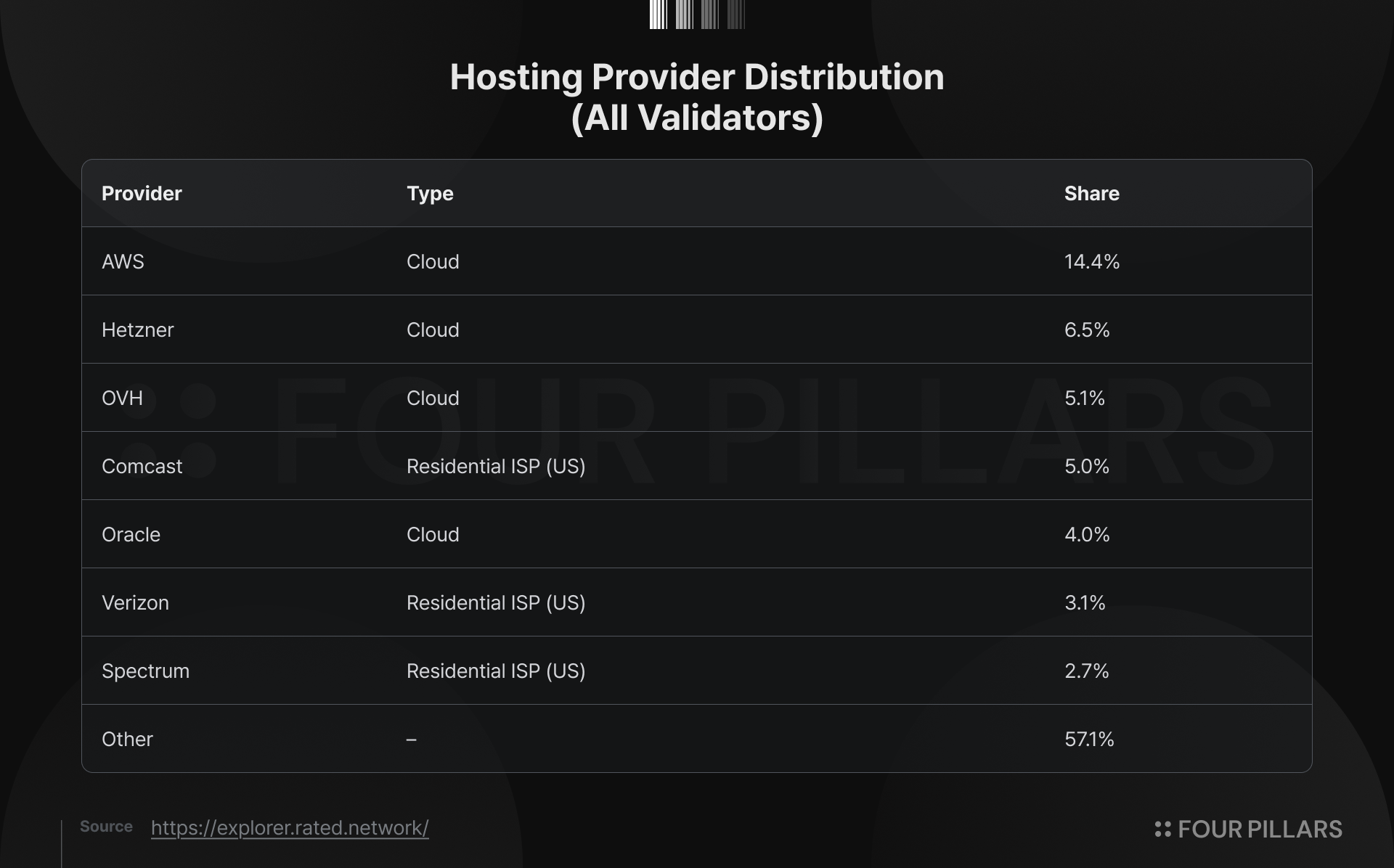

Finland (3.98%) and Canada (3.9%) also make the top ten, but not due to particular local enthusiasm for Ethereum. Instead, this is due to the presence of cloud hosting service providers. Germany and Finland host server regions of the well-known European cloud provider Hetzner, while Canada has a major OVH region. These cloud providers, favored for their affordability, stable bandwidth, and ease of deployment, are the preferred choice for global blockchain node operators. This is corroborated by the actual host distribution data: Hetzner hosts approximately 6.5% of validators, while OVH accounts for 5.1%.

More notably, there is a strong presence of US residential internet service providers. Comcast accounts for 5%, Verizon for 3.1%, and Spectrum for 2.7%. This means that over 10% of validators are actually nodes run by ordinary American households using their home broadband, rather than professional equipment in data centers. This reflects a relatively mature grassroots participation culture in the US, where many individuals or small teams are willing to host validators at home, contributing to the network's decentralization.

Why does this concentration exist?

Cost, convenience, and infrastructure are the main reasons. In Europe and North America, cloud services are mature, electricity is cheap, and the legal environment is relatively friendly, making it easier for individuals and small teams to get started. In contrast, while internet penetration is high in many parts of Asia, challenges remain with dedicated server costs, cross-border compliance, and network stability. While home nodes increase diversity, they also bring issues like uptime fluctuations; a local network outage can affect validator performance.

Professional Institutional Validators: Asia Catching Up, More Balanced Institutional Deployment

When we shift our focus to validators operated by professional institutions (excluding the large number of personal home nodes), the picture changes significantly. The US share drops to 25.81%, while major Asian countries show a notable increase: Singapore at 7.28%, Hong Kong at 6.44%, Japan at 6.38%, and South Korea at 4.59%. Combined, these four Asian jurisdictions account for approximately 24.7%, nearing the level of the US.

What does this indicate? The geographical distribution of institutional-grade infrastructure is far more balanced than the overall validator set. Professional operators also face practical pressures of cost and convenience—the US and Europe remain the most cost-effective options. Yet, they actively deploy nodes in Asia, primarily for two reasons:

- To meet the jurisdictional requirements of institutional clients: Many Asian funds, family offices, or publicly listed companies require asset custody and staking to be conducted locally or within compliant jurisdictions to adhere to local regulations.

- Latency diversification strategy: Applications and transactions serving Asian users require lower network latency. Placing nodes locally can significantly improve user experience and transaction confirmation speed.

This proves that deployment in Asia is not "forced" but a deliberate strategic choice. Institutions see the demand and are willing to invest accordingly.

The Problem: How the P2P Network Creates "Geographical Blind Spots"

South America, the Middle East, and Africa are almost entirely absent from the top ten rankings. The Middle East is particularly noteworthy. Centered around the UAE, with rapidly forming regulatory frameworks and a massive influx of exchanges, funds, and custody businesses, the region has become one of the fastest-growing hubs for the global crypto industry. However, from an infrastructure perspective, the Middle East remains "peripheral." Capital and business have arrived, but the physical foundation of the network still primarily relies on Europe, North America, and Asia.

Ethereum's consensus layer peer-to-peer (P2P) propagation mechanism structurally disadvantages regions with low node density.

In simple terms, Ethereum uses protocols like gossipsub for message propagation. Critical information such as blocks and attestations spreads rapidly through a "mesh" network of nodes. Each node has a "peer score," which determines whether it can occupy a core position in the propagation network.

If a node is located in a region with low node density, messages arrive slightly later. Later message arrival → lower peer score → pushed to the edge of the mesh → even later message reception... This creates a vicious cycle. The result is that validators in these regions are more likely to miss block proposal or attestation deadlines, indirectly affecting staking rewards, and in extreme cases, even impacting network finality.

The current trend is not optimistic. The scale of large US-based staking companies and staking ETFs continues to expand, with substantial new staking capital still concentrating in the US, potentially further widening the geographical gap.

This is not just a technical issue; it is a test of the principle of decentralization.

If the network cannot serve global users equally at the physical level, the promises of "censorship resistance" and "global accessibility" become compromised. Regional network disruptions or regulatory interventions could disproportionately impact users in sparsely represented areas.

Opportunity: First-Mover Advantage in Peripheral Regions

The good news is that this also presents a tremendous opportunity.

If Ethereum is to truly become a global settlement layer and world computer, institutions in various regions will inevitably seek "localized" staking infrastructure. Whoever can first establish reliable validator nodes in the Middle East, South America, or Africa may gain a leading position in collaborating with local institutions.

Imagine this: A large fund in the UAE or Saudi Arabia wants to engage in compliant staking. They would prioritize local service providers that can simultaneously meet local regulatory requirements, data sovereignty, and low latency. In such a scenario, the few operators capable of providing complete solutions would no longer compete solely on price but operate in a landscape where "first-mover advantage becomes a barrier."

Asia has already demonstrated this—the increase in the proportion of professional validators is precisely a result of demand-driven deployment. Similar stories are likely to unfold in South America, the Middle East, and Africa in the future.